Sometimes people ask what I've been thinking about. Maybe people just spend more time thinking about pet peeves or things that annoy them, but here is what I'm seeing out there, worrying about, and arguing about lately (at least when I wrote this 13 months before it actually published today). In my opinion, the following are all mistakes, but if you can't find something in this post to argue with me about, you might not be paying attention. Each of these items is at least a little controversial, and reasonable people can disagree about them to a certain extent.

#1 Hyperconservative Withdrawal Rates

Among financial hobbyists, one of their biggest fights is about what the “safe” withdrawal rate is. The main issue is that people disagree on the definition of safe. But it can have real consequences when applied to people's lives, causing them to spend less than they would like to spend or work longer than they would like to work.

Studies using historical data are clear that spending about 4% of your portfolio, adjusted upward for inflation each year, was highly likely to result in the portfolio surviving at least 30 years. After 30 years, the portfolio, on average, was 2.7X the size of the original portfolio. But the future is not necessarily the past, and anxious people can be found dialing down that 4% number to 3.5%, 3%, and even lower, especially for expected retirements of longer than 30 years. I've seen people arguing for 2% or less. Given that you can buy a 30-year TIPS yielding 2.65% as I write this, a 2% withdrawal rate is, well, bonkers/ridiculous/nuts/stupid/whatever. Four percent is safe, and 3%-3.5% is pretty much bulletproof.

The latest argument I'm seeing isn't that people ran out of money spending some reasonable percentage. It's that they wouldn't like that the portfolio had “too much drawdown,” and that made them feel anxious. It's your money. Do what you want with it. But if you decide that it's just too much stress to spend any more than 2.5%, you probably ought to put a lot of your nest egg into SPIAs and a TIPS ladder, and you should definitely delay Social Security to 70 for at least the high earner. And let your heirs know they've almost surely got a big fat inheritance coming. Remember the Rich, Broke, or Dead graph.

More information here:

The Silliness of the Safe Withdrawal Rate Movement

#2 Underdiversified Portfolios, Due to Tracking Error

Given the run-up in US large cap stocks, particularly growthy “tech” stocks, people no longer seem to care as much about diversification. They're bummed that the S&P 500 made 25% in both 2023 and 2024 and that they only made 10%-15% in their overall portfolio. They no longer want the other 3,500 stocks in the US, much less international stocks, bonds, small value stocks, or real estate. Nobody can seem to remember 2000-2010, when the S&P 500 had a return of about 0% per year.

Trees don't grow to the sky, and the pendulum will swing back at some point. I mean, why stop at just investing in the S&P 500? Why not put it all into the S&P 100? Or a tech ETF? Or just buy the individual Magnificent 7 stocks directly? Or put it all into NVIDIA? Now, I fully realize that the performance of an S&P 500 index fund really isn't all that different from a total stock market index fund and that the correlation between the two is very high, but there is a reason Jack Bogle's (and my) favorite mutual fund is the total stock market fund.

More information here:

Don't Abandon Your Diversification

Why Staying the Course is Hard

150 Portfolios Better Than Yours

#3 Massive 529s (and College Costs)

529s are a tax break for the wealthy since average Joe can't afford to put much, if anything, into one. But some people carry this particular account to extremes. They apparently envision their tiny tot (or even an unborn child) attending the most expensive college in the country, followed by dental school and maybe even a dozen years of private K-12 thrown into the mix. Even though the parent received scholarships and worked during school and even though they now have a high income with which they can help, they somehow think they have to have the entire sum of the education saved up in advance and sitting in cash on the day their child graduates from high school. If not, they have failed as a parent.

Worse, they think they need to “max out” a 529, not realizing that both parents and four grandparents can all open a 529 for each child in every single state and that the “max” is well over a billion dollars—if it exists at all. I don't quite get it. I ask them what their parents gave them, and the answer is often “nothing.” Let me get this straight: you received no help from your parents and seem to have done just fine, but your kid needs $800,000 in a 529 or they'll fail in life?

Newsflash! Most children of WCIers are not going to attend the most expensive colleges, most of them aren't going to dental school, and most of them are going to get some sort of scholarship. And you likely have a better use of money than a hyperfunded 529. College costs what you are willing to pay, but paying 10 times as much does not result in an education 10 times as good. Most of the time, it just results in an education that is “different.” You'd better value that difference highly if you're going to spend that much.

More information here:

#4 Stocks Suck

I have met real estate investors, many of them successful, who have some weird views about stocks. They seem to think they are the equivalent of putting it all on red in a casino, denigrating them as “paper assets” and deriding their volatility. I'm shocked to learn that many of them don't own stocks at all, despite the ease, convenience, liquidity, and low cost (now practically free) of owning a diversified portfolio of the most profitable corporations in the history of the world. I don't care how much you love real estate; putting 20% of your serious money into stock index funds is probably going to improve your portfolio.

More information here:

Real Estate Investments vs. Stocks

10 Reasons I Invest in Index Funds

#5 Real Estate Sucks

I see the opposite issue among many investors in “traditional” investments. They seem to think that it is impossible to own real estate without having to plunge toilets at 3am, that nobody has ever become financially independent primarily via real estate, that all leverage is incredibly risky, and that success is all about luck. They can talk at length about mutual fund correlations and withdrawal rate studies, but they couldn't tell a cap rate from a triple net lease.

While real estate is optional for building a portfolio and achieving financial success, I see little reason to avoid it. Solid long-term returns and low correlation with stocks and bonds; what's not to like? Sometimes I see the argument that “I already own real estate since a total stock market fund includes real estate companies.” While that's true, are you aware that if all you invest in is the S&P 500, you have twice as much money in NVIDIA as in real estate? An even worse argument is that your home is a real estate investment rather than a consumption item.

More information here:

How to Succeed at Private Real Estate Investing

Private Real Estate Lending Funds

How to Invest in Real Estate With a Retirement Account

#6 Minutiae Really Matter

Plenty of investors miss the forest for the trees. They mistakenly think that things that don't matter at all or only matter a little are really important. Some examples include credit card/travel hacking, frequent or complex rebalancing, chasing brokerage transfer bonuses, searching out lower-than-already-rock-bottom expense ratios, adding another asset class or three to a perfectly adequate portfolio, buying the dips, and more. In reality, what really matters in investing is:

- Your income

- Your savings rate

- Choosing a reasonably risky portfolio

- Staying the course

Everything else is, at best, icing on the cake and, at worst, a giant distraction.

More information here:

How to Think About Credit Card Hacking

Does Expense Ratio Really Matter?

Rebalancing Your Investment Portfolio

Why Performance Chasing Is an Investing Error

#7 Automatic Roth Conversions

Some people seem to think that Roth conversions are always good. Why wouldn't you want more Roth money? Well, all else being equal, sure, Roth money is great. But all else is never equal.

Prior to doing an expensive Roth conversion, at least take a few moments to think about and guess who is going to be spending that money and what tax bracket they are likely to be in when they do so. Lots of people my age and younger have taken advantage of Roth IRAs and Roth 401(k)/403(b)/457(b)s for their entire careers and already have more Roth money than they should. One of the greatest mistakes in finance is making Roth contributions or doing Roth conversions while in high tax brackets and then having the money end up in the hands of a charity or an heir in a low tax bracket.

Even if you expect to spend the money yourself, there's a very good chance, if you're like most people, that you can withdraw it at a substantially lower marginal tax rate than your rate at the time you made the initial contribution. “Pay taxes on the seed, not the harvest” is some of the worst Roth contribution/conversion advice ever given.

More information here:

Should You Do Roth Contributions or Conversions?

Roth vs Tax-Deferred: The Critical Concept of Filling the Brackets

Supersavers and the Roth vs. Tax-deferred Dilemma

#8 Accredited Investor Investments When You're Not Really an Accredited Investor

The legal definition of an accredited investor is mostly someone with:

- At least $1 million in investable assets OR

- At least $200,000 in income ($300,000 with your spouse) in each of the last two years

That's almost all white coat investors, at least eventually. However, real accredited investors possess both of the following attributes:

- Can evaluate the merits of a private investment without the assistance of an advisor, accountant, or attorney AND

- Can afford to lose their entire investment without it affecting their financial life in any meaningful way

This is a much smaller subset of WCIers, and many will never be in this category. That's OK, though, because all investments that require you to be an accredited investor are optional anyway. Plenty of bad deals exist among private investments, and scammers and fraudsters are much more likely to be found there than in the highly regulated public markets. If you can't afford to build a diversified portfolio of investments with $100,000 minimums, have a strong preference for simplicity in your portfolio, or would be devastated to see an investment go to zero, just stick with index funds or buy your rental properties directly.

Invest in the private world long enough, and something you bought will go to zero, no matter how much due diligence you do. That said, many people consider their private investments to be their best-performing investments, whether that's a real estate fund or an ambulatory surgical center.

More information here:

10 Things To Know Prior to Purchasing an Accredited Investment

#9 Ridiculous RMD Fear

I find it amazing that everyone likes getting a raise before retirement but nobody likes it afterward. Somehow, having $600,000 in taxable income as a 50-year-old doctor is awesome, but having $600,000 in taxable income as a 75-year-old retiree is a problem. It's worse when people start doing dumb things to avoid having large Required Minimum Distributions (RMDs), such as:

- Pulling money out of retirement accounts early

- Never contributing to retirement accounts at all

- Deliberately trying to have low returns or even losses in a retirement account

- Doing Roth conversions at very high tax rates when that money is likely to be withdrawn at lower rates

Most people probably should spend their RMDs with zero guilt. If you really don't need or want them, consider giving them to charity via a Qualified Charitable Distribution (QCD) of up to $111,000 per year [2026]. However, you don't have to spend an RMD. An RMD is really just a notification from the IRS that you have maxed out the benefits of investing in a tax-deferred account. You now have to give the IRS its portion (hopefully you get to keep some of their portion due to an arbitrage between tax rates at contribution and withdrawal) and reinvest your portion in your taxable account. If you don't spend it and invest it tax-efficiently, there won't be much loss between the day you take the RMD and the day your heirs get a step up in basis anyway.

More information here:

How to Think About the ‘Other' RMD Problem

How to Take a Required Minimum Distribution at Vanguard

#10 Stock Picking

Yes, people are still out there investing in individual stocks. Look, if you are sufficiently talented to pick stocks well enough to beat an index fund when adjusted for risk and the value of your time, you shouldn't just be managing your own money. You should be managing billions and charging very high fees to do so. If you think it's fun, maybe calculate how much your fun is likely costing you. Is it that fun? Or would you rather spend those millions on an around-the-world cruise this summer with your grandkids? Or on a NetJets subscription? Or a home renovation?

Once compound interest does its thing with your (likely) lower returns, those are the sorts of expenses that have a cost equivalent to your stock-picking hobby.

More information here:

Picking Individual Stocks is a Loser's Game

Why Talking About Individual Stocks and Sectors Makes You Look Dumb

Uncompensated Risk vs. Compensated Risk

A Die-Hard White Coat Investor Buys an Individual Stock — An M&M Conference

#11 Market Timing

Market timing is so tempting until one realizes their crystal ball is cloudy, and so is everyone else's. Not yet convinced that you cannot predict the future accurately? Start keeping a little journal of your predictions, and then go back and look at them in three months or three years and see how you did. If you're like most, you'll quickly convince yourself that you shouldn't invest your serious money in a way that requires you to accurately predict the future.

More information here:

Should I Try to Time the Market?

Should I Be Nervous About Lump Sum Investing When the Market Is at an All-time High?

How Market Timing Lost Me $200,000

The Best Way to Time the Market

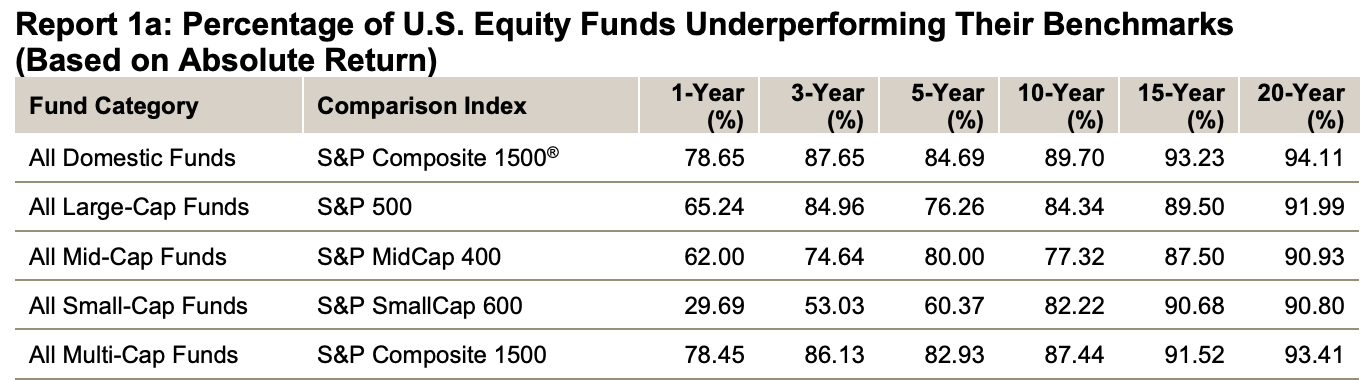

#12 Actively Managed Mutual Funds

The word is definitely out about index funds at this point. Almost 50% of mutual fund assets are currently invested in index funds, and many think it will be as high as 70% within a decade. Took long enough. Still, many people are throwing money away trying to choose active fund managers in a vain attempt to beat the market. The latest SPIVA report is just as damning as all the ones before it. And those numbers are before tax and the cost of “advice.” And if there were 25-, 30-, and 60-year numbers, they'd look even worse for actively managed funds.

More information here:

People Still Believe in Active Management?

Analyzing Winning Mutual Funds

#13 Huge Allocations to Speculative Investments

My definition of a speculative investment/instrument is one that produces no earnings, dividends, interest, rents, or other financial streams. Your investment return is 100% reliant on someone else paying you more than you paid for the investment. We're talking about things like precious metals, Beanie Babies, empty land, cryptocurrencies, art, and NFTs.

I occasionally get into long arguments with an investor about the merits of Bitcoin or some other speculative asset, only to find out that the person only has 1% of their portfolio in it anyway. Fine, if you're limiting the total amount of speculative investments to a single-digit percentage of your portfolio, I don't have a problem with that. In fact, I tell a few of them to quit being a wimp and bump it up to 5% if they really believe Bitcoin is going to $4 million in the next decade or so. But if your portfolio is 50% NVIDIA and 50% Bitcoin, that's a mistake. Don't take risks you don't need to take in order to make money you don't need so you can buy things you don't want to impress people you don't even like.

More information here:

What Are the 4 Types of Investments?

Best Speculative Assets to Hedge Your Portfolio

I Figured My Childhood Obsession Would Make Me a Millionaire; Boy, Was I Wrong

Financial literacy matters, and investment mistakes are common. The combination of financial literacy and financial discipline is so rare in our society today that if you possess both, it's like having a superpower.

What do you think? Which one of these 13 mistakes listed above isn't really a mistake? What other mistakes do you see people making?