Student loan debt is increasingly becoming a contributor to stress, burnout, and even suicide in doctors and other high-income professionals. Refinancing private student loans is a no-brainer anytime you can lower your interest rate, even as an intern. Direct federal student loans should be refinanced as soon as you decide not to go for Public Service Loan Forgiveness (PSLF) and find an interest rate lower than your effective rate.

It is best to refinance medical school loans early and often, any time interest rates drop or another company offers a lower rate than your current lender. If you refinance through the links on this page, you will also get a cash bonus. WCI gets advertising compensation from these companies when you use these links. It is a win-win. As you pay down your loans, your credit score and debt-to-income ratio will improve, possibly lowering your rate even further.

Have you visited any of these lenders from a different website? Clear the cookies in your web browser before you click any of the WCI links below to ensure you are identified as a WCI reader (and get our best rates and bonus cash back).

† Bonus includes cash rebates and value of free course. Borrowers who refinance more than $60,000 in student loans using the WCI links will be enrolled in The White Coat Investor’s flagship course, Fire Your Financial Advisor: ATTENDING for free ($799 value). Borrowers will still receive the amazing cash rebates that WCI has negotiated with each lender. Offer valid for loan applications submitted from May 1, 2021 through October 31, 2026. Free course must be claimed within 90 days of loan disbursement. To claim free course enrollment, visit https://www.whitecoatinvestor.com/RefiBonus.

You can do this, and WCI can help! We want you to be successful, so we are giving anyone who refinances more than $60,000 in student loans through the WCI links free access to The White Coat Investor’s Flagship course, Fire Your Financial Advisor: ATTENDING (A Step-by-Step Guide to Creating Your Own Financial Plan). Get amazing cash rebates that we have negotiated AND another $799 in value with the course. Join thousands of other professionals who have created their own financial plan with the help of The White Coat Investor.

*Free course offer valid for loan applications submitted from May 1, 2021, through October 31, 2026. The course must be claimed within 90 days of loan disbursement. If you are already a customer of one of our partners, you may need to refi with a new partner to be identified as a WCI reader and be eligible for the free course. Course access instructions are sent out on a monthly basis.

Get Free CourseDoctors often accumulate multiple loans from both private and federal loan programs to fund their medical schooling. Student loan refinancing is when you seek out a private lender to replace those loans with a brand new loan at a new interest rate and terms. Refinancing is free. It can be done over and over. And it can save you a lot of money by lowering your interest rate.

Student loan refinancing is NOT the same thing as a Federal Direct Consolidation Loan. Consolidation is the process of combining multiple federal student loans into one federal loan.

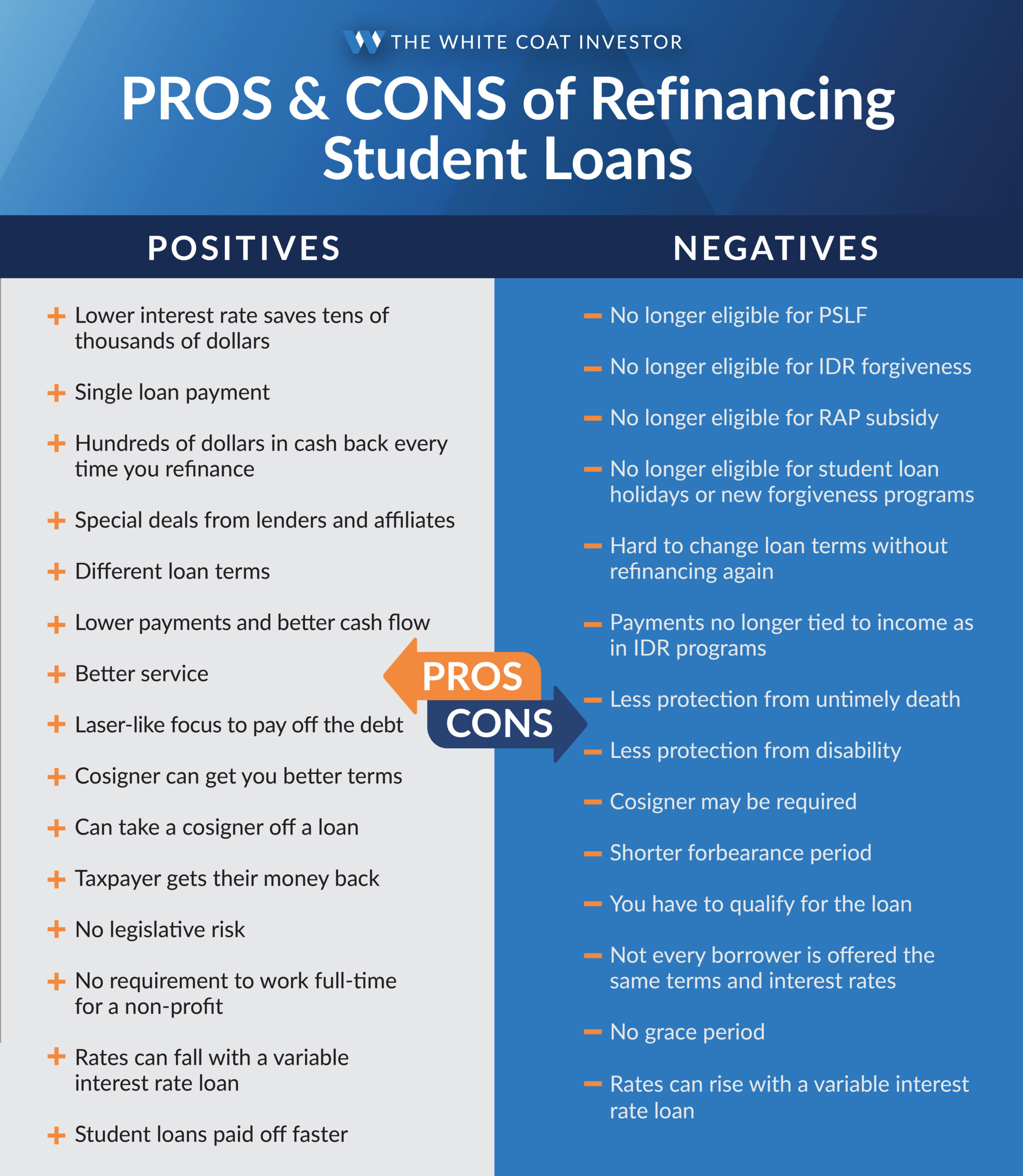

En route to debt elimination, most professionals should take advantage of the ability to refinance their debt with a private company. It is usually a no-brainer (assuming loan forgiveness is not an option), because you can lower your monthly payment and the amount of money you owe over the life of the loan—in addition to paying it off quicker.

Eliminating your student loan debt at the beginning of your career will increase your happiness and speed your way to financial freedom, allowing you to take advantage of future opportunities, both professional and personal.

If you have $300,000 in student loans at an average rate of 7% and refinance that to 2.5%, you will spend $13,500 less in interest in the first year alone. That is $13,500 that can go toward principal instead of interest. The same monthly payment that would pay off a 7% loan in 20 years pays off a 2.5% loan in less than 10 years. A 10-year loan becomes a 6 1/2-year loan. A five-year loan goes away in less than four.

As if saving tens of thousands of dollars in interest isn't enough, WCI has negotiated a special deal for you with each of the main refinancing companies. When you refinance, you get some money back (and you help support this site). If you're smart, you'll throw those dollars saved into paying off your loans.

No company is ever perfect, but compared to the service you were getting from your federal loan servicer, these guys might seem like it. You can get people on the phone, can use an actual functioning website, and can easily make extra payments to pay your loans off even faster.

When refinancing companies first showed up in 2013, there were lots of kinks to work out. Well, they've all been worked out. Now you can get a preliminary quote from most of them online in five minutes or less.

If you have all of your loan paperwork handy, you can usually upload it electronically in a few more minutes. Once you've gathered the paperwork to refinance with one lender, checking your rate with a couple of others is no big deal either (and we recommend you do so).

We don't know how long it takes you to make $13,500, but refinancing your loans will take much less time, especially since it is all after-tax money.

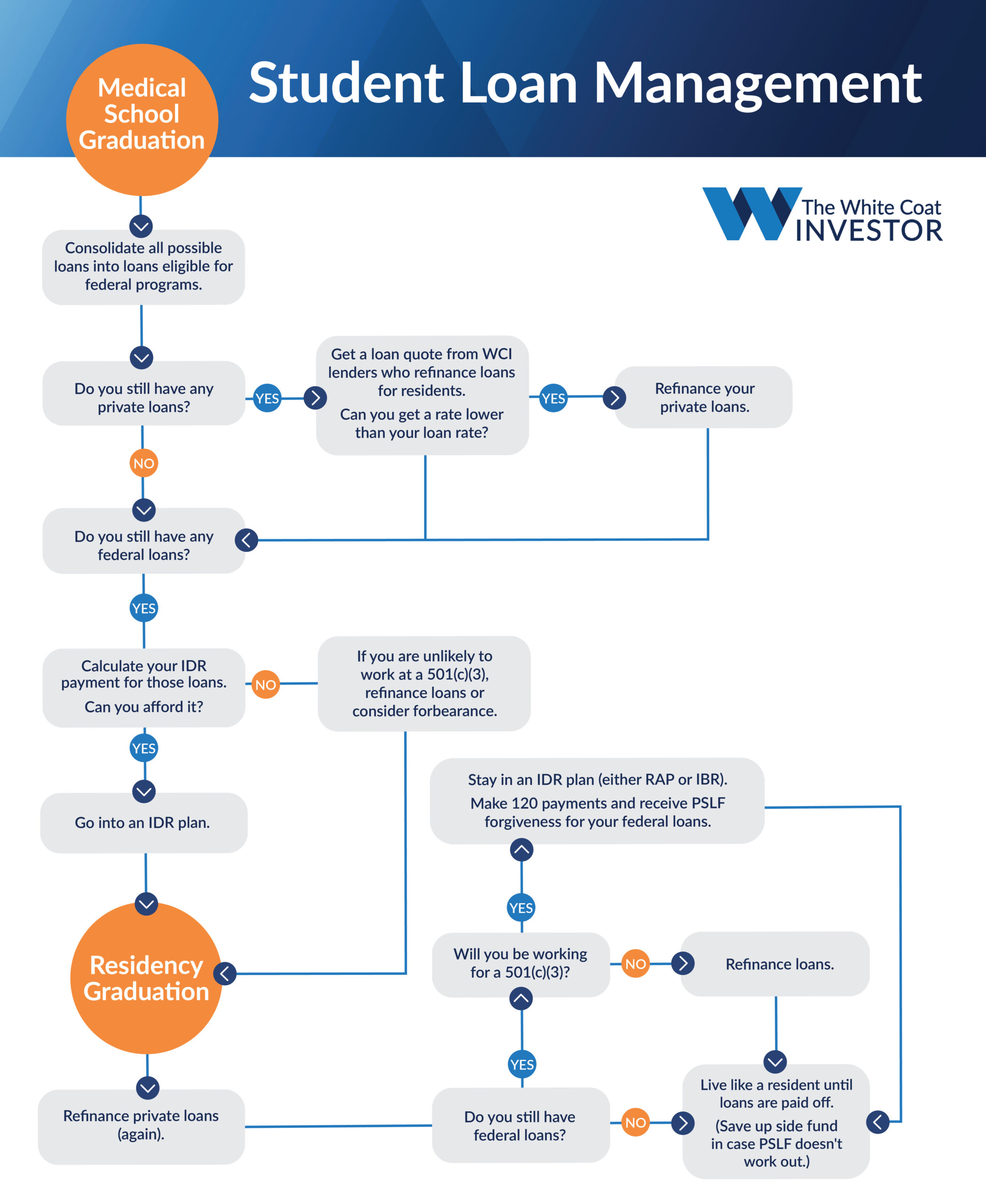

These include any private medical school loans you may have taken out. Those aren't eligible for PSLF, so you might as well refinance them if you can get a lower rate (which you usually can).

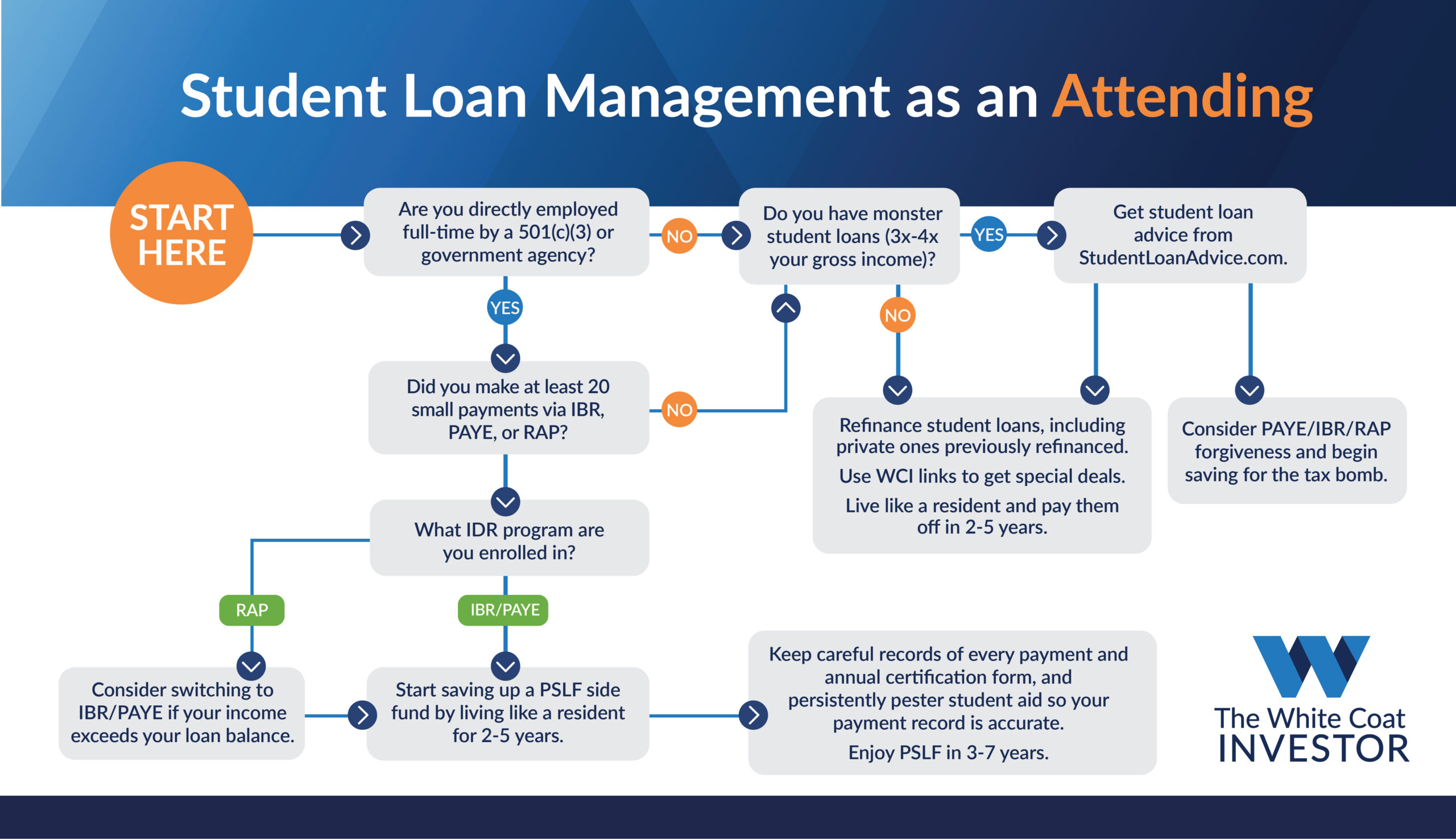

PSLF is a program where any remaining direct federal student loans are forgiven tax-free after you make 120 on-time monthly payments in a qualifying program while working full-time for a qualifying employer.

If you're absolutely positive that working at a 501(c)(3) and going for PSLF is not in your future, you can consider refinancing federal loans. If you're not sure, don't refinance!!

You can learn more about PSLF vs. refinancing by reading Refinance and Pay off or Go for PSLF. If you're needing help understanding federal student loan programs like PSLF, RAP, IBR, IDR, etc., you'll also want to familiarize yourself with our Ultimate Guide to Student Loan Debt Management. If you don't want to wade through blog posts and DIY your student loan management, set up an appointment with one of our consultants at StudentLoanAdvice.com. You'll have an experienced professional to answer your questions and guide you through your best options.

If you're not going for PSLF, then refinance today! With companies’ cashback bonuses, it really makes the decision easy.

Each student loan refinancing company is unique, but the bottom line is that you should apply with several of them. Assuming the service you receive is adequate, take the one that offers you the lowest rate with the best cashback bonus.

Lenders take many factors into consideration, including your:

The better you are in each of these categories, the better the rate you will generally receive.

Private practice physicians who refinance often have a combination of these factors:

Yes, you can refinance federal student loans, but should you refinance them? When the federal student loan interest rate was 0% during the pandemic, many borrowers held off on refinancing federal student loans. Zero percent was obviously a great deal, but now interest rates have gone back to normal.

Are there key considerations when moving from federal to private loans?

Yes. The government offers very real, very legitimate benefits, such as:

When moving from a federal to a private loan, you’ll lose some benefits. If you’re going to lose federal benefits, you better get the best deal.

A couple of disadvantages of moving to private loans include:

Yes, always shop for better interest rates on your student loans! It is always worth it to see if you can save even more money by refinancing them again.

Get off your duff and get this important financial chore done; then get busy living like a resident to pay them off. Even if you have refinanced previously, you can do so again. And you should whenever rates drop (and if you go through a different company, you can even get another cashback bonus). There is no break-even period since there is no cost to you to refinance, so keep refinancing over and over until you have obliterated those student loans!

Compare Your Rates and Get Cash Back

Perhaps you didn't get the best rate when you refinanced due to your credit score. Or perhaps interest rates have dropped. Or now you qualify for a five-year term or you decide to change to a variable rate loan. There is absolutely nothing stopping you from refinancing again.

In fact, it's probably a lot easier since you now only have one loan. And yes, you get the bonus money every time you do it. Even the refinancing companies probably like it when you do this. They've already sold your previous loan off to investors. Doing it all again means more business for them.

Yes. But remember that subsidized loans will not accrue interest while you’re enrolled in school. Once they are converted to private student loans, they will likely begin to accrue interest.

No, you can refinance one or all of your loans.

It depends. Some refinancers will work with you while you’re in residency. Others wait until you’re an attending.

Yes. Private loan servicers can consolidate all your federal and private loans together. They can even consolidate your partner’s student loans with yours into one loan.

Refinancing and paying down your med school debt in less than 10 years (and preferably less than five) can be a wonderful way to race to financial freedom. Once you’ve refinanced, however, you can’t go back. The refinancing decision warrants an abundance of caution if you have a combination of these characteristics:

Remember that when you refinance your medical school loans, they are no longer eligible for the Income-Driven Repayment programs (lower payments with a taxable forgiveness option after 20-25 years) or the PSLF program (tax-free forgiveness after 10 years). So, don't refinance federal loans until you're absolutely sure you won't be going for loan forgiveness.

For many borrowers, refinancing is an easy decision. For others, it is important to be sure that it will not have a negative impact on future plans. Weigh your decision by examining these pros and cons:

Although these terms are often lumped together, they are very different things and both require your consideration.

Consolidation is the process of combining multiple federal student loans into one federal loan.

Student loan refinancing is when you seek out a private lender to replace federal or private loans with a brand new loan at a new interest rate and terms.

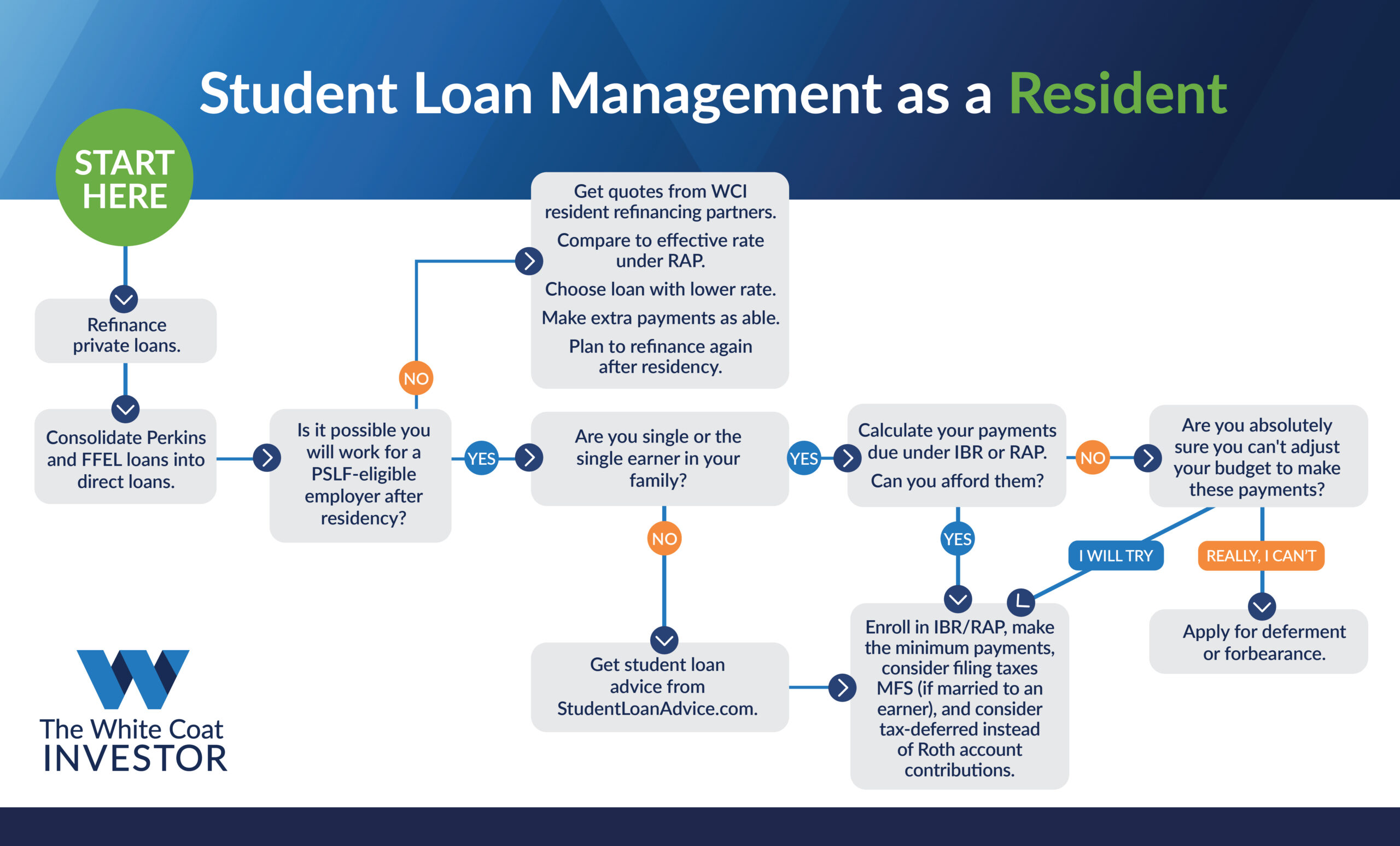

It’s best to make the decision to consolidate or private refinance at the end of medical school.

Look to refinance your private student loans once you have graduated, started residency, and aren’t pursuing loan forgiveness.

If you are going for PSLF, then, if at all possible, stick with an IDR plan. If you finished borrowing prior to July 1, 2026, you’ll need to choose carefully between IBR and RAP. If you borrowed a loan on July 1, 2026 or later, RAP will be your payment plan.

If you are not yet sure about PSLF, then, if at all possible, stick with RAP. Otherwise, run the numbers with reasonable assumptions and take your best guess between RAP and IBR (assuming you qualify for it).

If you are sure you're not going for PSLF, then get refinancing quotes ASAP from the recommended private refinancing list and compare them to your effective interest rate under RAP. Go with the lower rate, realizing that the variable rate may be the best deal, even with the additional risk.

More information here:

A Step-by-Step Guide to Refinancing Your Student Loans During Residency

By refinancing your medical school loans, you can save tens of thousands of dollars over the life of the loan, in addition to lowering monthly payments.

Are you still asking yourself if it is worth it to refinance student loans? Not only can you save money by refinancing through our partners, but we’ve also negotiated to get you cash back when you refinance through one of our links. And we’ll throw in our flagship FYFA course ($799 value) at no additional cost if you private refinance at least $60,000 using our links.

If you want the lowest rate possible, that means you're going to have to commit to a variable five-year term and run the interest rate risk yourself. That means if interest rates go up dramatically soon, you may end up paying more in interest than if you had taken a fixed-rate loan.

However, it's a risk worth running for anyone willing to commit to living like a resident for 2-5 years until the loans are gone. If rates only rise a little, or rise slowly, or don't rise for a few years (or at all), you're going to come out ahead. Once you run the numbers on just how much and how quickly rates have to rise for you to lose this bet, you will likely be much more comfortable with it.

Also, if you're committed to living like a resident and getting out of debt quickly, you likely have A LOT of slack in your budget and can easily cover the worst-case scenario. Plus, you now have a little more motivation to live efficiently and get out of debt. A variable-rate loan not only gives you a mathematical tailwind to speed you to financial independence but a behavioral one as well.

The process to refinance your medical school student loans should be simple and only take a few weeks.

You don’t need to go it alone! Navigating complicated and ever-changing student loan programs when such large numbers are at stake is a daunting DIY project, to say the least. That's why we created StudentLoanAdvice.com, a White Coat Investor company created to help doctors, dentists, and other high earners tackle and defeat their student debt.

Contact our experienced team to review your student loan situation, run the numbers and strategies available to you, and help you come up with an optimized plan. Get the personalized answers you need for one flat fee. You can do this, and we can help!

In IDR, married borrowers can generally reduce their student loan payments by separating their income and filing taxes Married Filing Separately. After loans are refinanced, however, monthly payments toward your now private student loans are based on the loan size, interest rate, and term instead of your income. Filing separately will no longer have the potential to reduce your payments. If you are married, you'll want to file your taxes in the most advantageous way for your situation, which is likely Married Filing Jointly.

If you are undecided about going for loan forgiveness or private refinancing, take a deep dive into our Ultimate Guide to Student Loan Debt Management for Doctors.

Many WCI readers have refinanced with SoFi® over the years because of their competitive rates and flexible payment terms. SoFi offers competitive rates with flexible terms for medical and dental professionals as well as residents. Additionally, SoFi offers a 0.25% autopay discount. There is no upper limit to the loans you can refinance, but certain minimums apply.

Doctors and dentists with loan balances over $150,000 are eligible for our best refinance rate, not available to residents (You can only take the Doctor/Dentist rate discount or the cash bonus, not both). Residents are able to refinance their loans with SoFi over the course of their residency (up to 54 months) and only pay $100 per month‡ (see terms).

Juno offers doctors an opportunity to refinance their student loans with exclusive benefits tailored specifically for medical professionals. Through Juno’s group negotiation model, doctors can access discounted interest rates, reducing the overall cost of their loans and securing better terms than they would typically receive on their own.

In addition to lower rates, Juno provides its members up to $1,000 in cash back bonuses when refinancing. This extra cash can be used to pay down debt faster or for other financial goals. Whether doctors are just finishing residency or are already established in their careers, Juno’s refinancing options make it easier to manage student debt more effectively.

See if you could save money1 on your student loans by refinancing2 with Earnest. WCI readers receive a .25% rate discount. Choose custom terms to fit your budget—like picking your exact monthly payment or selecting fixed and variable rates. Earnest allows you to customize your loan–choose your rate, term, and payment amount that works for your budget. Make a plan that fits your needs and start working your way out of debt. You won’t be penalized for making payments early. Get $500* when you sign a loan with Earnest using links on this page and refinance loans >$50K. (Can lend in DC and all states except MS). Variable rates are not offered in AK, IL, MN, NH, OH, TN and TX. Bonus not available to residents of KY, MA, or MI.)

1Choosing to refinance to a longer term may lower your monthly payment, but increase the amount of interest you may pay. Choosing to refinance to a shorter term may increase your monthly payment, but lower the amount of interest you may pay. Review your loan documentation for the total cost of your refinanced loan.

2Please note that you will lose benefits associated with your underlying federal loans, such as federal Income-driven Repayment Plans, Economic Hardship Deferment, Public Service Loan Forgiveness, or other deferment and forbearance options, if you refinance into a private loan. If you file for bankruptcy, you may still be required to pay back this loan.

KeyBank is one of the nation’s largest full-service banks, offering banking, lending, and student loan solutions for healthcare professionals at every stage of their career.+

WCI members are eligible for a $550 discount on student loan refinancing through KeyBank. This benefit is designed to help healthcare professionals simplify repayment and potentially reduce the overall cost of their student loans.+

Medical Resident & Fellow Student Loan Refinancing

Created for medical residents and fellows, this KeyBank refinancing option offers low monthly payments during training with no compounding interest during residency or fellowship. Eligible residents may pay as little as $100 per month while in training.+

All products offered by KeyBank N.A. ©2026 KeyCorp®. All Rights Reserved.

Credible is not a lender, but a marketplace where lenders compete for your business. They’ll show you actual prequalified rates from multiple lenders and they don’t share your information with lenders until you choose the specific lender you want to pursue. Credible is free and easy to use with one simple form for 13 lenders. For medical residents, Credible also partners with multiple lenders that offer graduated repayment plans—that means you can defer full payments until you complete your training .The minimum amount to refinance is $5K and with most companies there is no maximum. Use the link above and receive a $500* WCI bonus when refinancing through Credible. (*To receive the $500 welcome bonus, readers must refinance a balance equal to or greater than $100K. If refinancing a balance below $100K, readers are eligible for a $300 welcome bonus. Payment of any Welcome Bonus will occur either via a credit through TangoCard.com sent to the email address provided, as applicable, or by any other means determined by Credible.) ^Close with a better rate than you prequalify for on Credible and get a $200 gift card. Terms apply.

Splash Financial is a leader in student loan refinancing for doctors. They also offer a special refinancing program for residents and fellows, which allows you to pay only $100 a month during training which has a different range of rates that may be higher. Splash partners with credit unions, banks, and other leading lenders to offer competitive rates. Hundreds of WCI readers check rates through Splash each month. In as little as three minutes, you could get pre-qualified rates and it won’t impact your credit score. There are no costs—no application or origination fees and no prepayment penalties.

The minimum borrowing amount is $5,000 and there is no maximum. If you refinance $100,000 or more, you are eligible to receive a $500 cash bonus. The bonus will be paid between 90-120 days after the loan closes and is available for first-time customers only. Bonus offer for WCI readers only if you use our link.

*current rates may include autopay discount of 0.25%

ELFI has come highly recommended from readers for low rates. They offer student loan refinancing and consolidation to both recent graduates as well as parents with Parent PLUS and private student loans. ELFI offers low rates even without the automatic payment discount that many lenders offer. Loan amounts start at $10,000 and up for qualified borrowers. ELFI offers repayment terms of 5, 7, 10, 15, and 20 years. These wide range of options provide borrowers with the flexibility they need to choose the optimal product to fit their budgets. Those with high income may opt for a shorter repayment term, saving them money over time. Those who want lower monthly payments, on the other hand, can choose a product with lower rates than they are currently paying. The minimum to refinance is $10,000. There is no maximum. For parents, ELFI offers repayment terms of 5, 7, and 10 years. They also offer Student Loan Advisors who are dedicated to each borrower providing individual assistance throughout the refinancing process.

Refinance with ELFI and receive a bonus applied to your loan balance. $400 for loans equal to or greater than $50,000* but less than $100,000. $599 for loans equal to or greater than $100,000*.

*Only one such bonus shall be paid per borrower regardless of how many loans taken out (please refer to their disclosure on the terms and conditions page below.) In the event borrower chooses to refinance multiple student loans rather than consolidating, bonus benefit will apply to the first completed and processed application resulting in a refinanced loan.

Start your Brazos refinance application through this page and you will get a $600 cash bonus after your loan funds! Texas residents only. Brazos is a nonprofit with over 45 years of experience with student loans. As a nonprofit, Brazos’ rates can be better than the national lenders. The maximum refinance loan amount is $250,000 for borrowers with up to a bachelor's degree and up to $400,000 with a graduate, law, medical or other professional degree. The minimum amount to refinance is $10,000. If you’re a Texan, visit studentloans.com now and start saving.