As a physician, it can be hard to know what to do first with your money. Should you pay off debt? Invest in retirement? Save for a house? And those in the medical field probably have a more difficult time than many other professions, since physicians have a wide range of incomes throughout their journey through medical school, residency, and the rest of their career. An investing order of operations is a simple way to decide. It gives you a clear order for where your money should go, step by step. By making and sticking to a plan, you can make steady progress and avoid costly mistakes.

What Is an Investing Order of Operations?

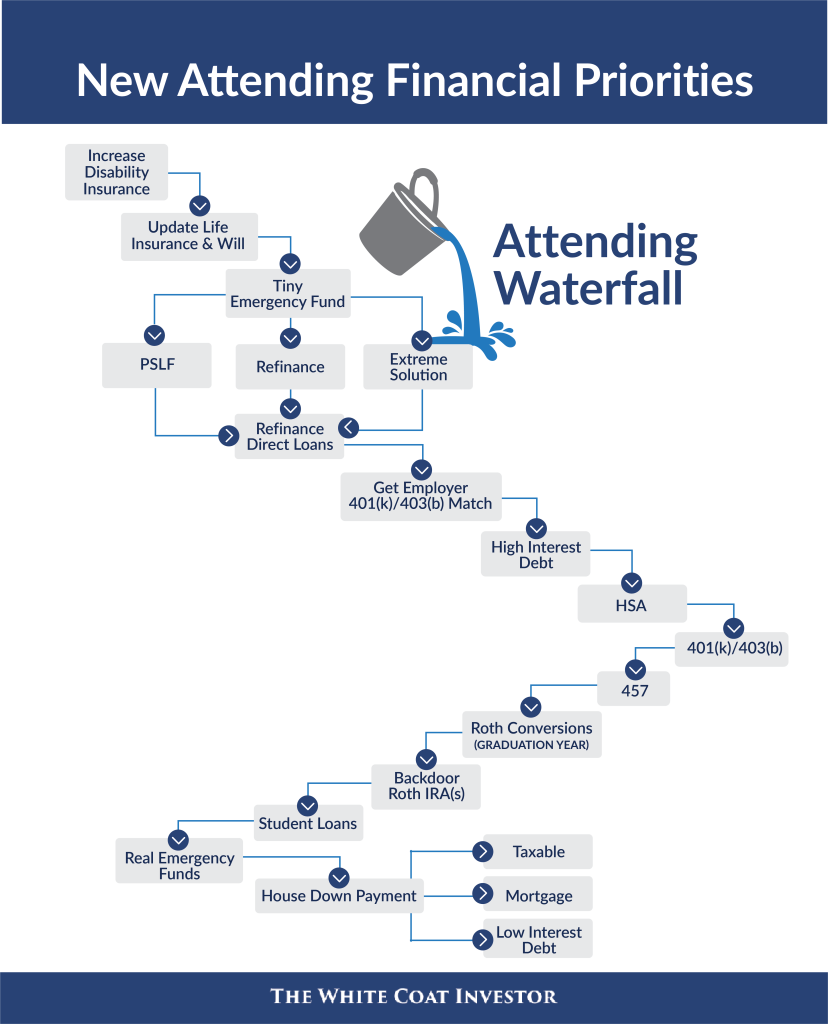

The term “investing order of operations” refers to the order in which you should allocate any excess money that you have. A similar term is a “money waterfall,” which we've covered before. You can think of it as your money flowing down from one bucket to another, depending on how much extra money you have.

Here's an example of a waterfall for attending physicians.

An investing order of operations tells you one order of how to allocate your money. While not everyone's investing order of operations will be the same, this can be a good framework to consider and tailor to your own specific needs.

What to Do Before Investing

Before you start investing ANY of your money, you'll want to make sure that you've taken care of a few other chores.

The first is to make sure you have sufficient insurance. This should include disability insurance to cover you in case you are injured and term life insurance if you have dependents or others who depend on your salary.

The next thing to do before investing is to set up a small emergency fund. You don't necessarily need a huge fund (like 3-6 months of expenses) right away, but a smaller one makes a lot of sense. You want to at least have enough savings to cover smaller expenses, like your water heater needing to be replaced or an unexpected car repair. You can revisit your emergency fund after you've taken care of some of the other higher-priority items on your list.

More information here:

Physician's Quick-Start Guide to Personal Finance

Investing Doesn’t Have to Be Complicated

The Wildcard: Student Loans

Before we start with a true investing order of operations, a word on student loans. Most residents and even new attending physicians have some degree of student loans. You have options for repaying your student loans, such as working for a 501(c)(3) institution to take advantage of PSLF. As part of your investing order of operations, you'll want to make sure you have a plan for your student loans. If you're not sure what to do, consider getting student loan advice to help you get on the right path.

Do This First: 401(k) Match, Pay Down High-Interest Debt

Once you have taken care of all the preparatory items, you'll want to take a look at your 401(k) or 403(b) plan, if you have one. Many of these plans offer a match, where your employer might match 50% or even 100% of your contributions up to a specific level. This is free money, and it should be one of the first places you invest any excess cash that you have. A 100% employer match is like getting a 100% return on your investments, something you'll be hard-pressed to get anywhere else.

Another priority area to focus on is paying down any high-interest debt that you have. This would be any debt with interest rates above around 5% or so. We are talking about credit card balances, relocation loans, car loans, etc.

Maximizing Your Retirement Accounts

One of the next areas that you'll want to focus on is maximizing your retirement accounts. This could include a Health Savings Account (HSA). This can be a great option since it is triple tax advantaged. You can deduct your contributions. Then, the money in the account grows tax-free, and you don't pay taxes on withdrawals for qualifying healthcare expenses.

A Roth IRA is another great option, especially for residents or new attending physicians, since you're likely to be in the lowest tax bracket of your life. Remember that you can also contribute to a non-working spouse's Roth IRA out of your income. Maximizing your 401(k)/403(b) contributions is another great use of your money, using the Roth option if you can.

What Comes Next?

After you've started maximizing your HSA, 401(k), and other retirement accounts, you're well on the way to securing your financial future. What comes next after that will depend on your specific financial and life situation. Some things to consider might be:

- Saving for a down payment for a house

- Investing in taxable brokerage accounts

- Building a “real” emergency fund

- Buying rental real estate

- Eliminating any other (low-interest) debt

- Paying off your primary mortgage

More information here:

The 15 Questions You Need to Answer to Build Your Investment Portfolio

Best Investment Portfolios — 150+ Portfolios Better Than Yours

The Bottom Line

An investing order of operations is not about being perfect—it is about being intentional. By taking care of the basics first and then moving through your priorities one at a time, you can build wealth in a smart and steady way. The exact order may look different for each person, but having a clear plan makes it much easier to move forward with confidence.

The White Coat Investor is filled with posts like this, whether it’s increasing your financial literacy, showing you the best strategies on your path to financial success, or discussing the topic of mental wellness. To discover just how much The White Coat Investor can help you in your financial journey, start here to read some of our most popular posts and to see everything else WCI has to offer. And make sure to sign up for our newsletters to keep up with our newest content.