While the most common question I get here at The White Coat Investor is “Should I invest or pay down debt?” This post is the answer to many of the other most common questions I receive such as:

- How should I invest my 401(k)?

- What mutual fund should I invest in?

- How should I invest?

- How do I know which stocks to pick?

- How do I invest this inheritance I just received?

While it is easy and tempting to give a quick off the cuff answer, it is actually a disservice to these well-meaning but financially illiterate folks to answer the question they have asked. The best thing to do is to answer the question they should have asked, which is:

How can I reach my financial goals while taking the least possible amount of risk?

The answer to all of these questions then is…

You Need an Investing Plan

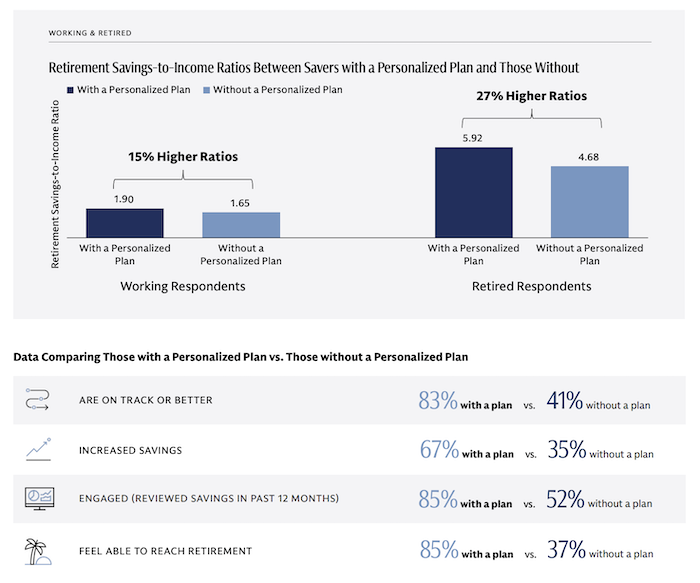

Once you have an investing plan, the answer to all of the above questions is obvious. You don't try to reinvent the wheel every time you get paid or have a windfall. You just plug the money you have into the investing plan. It can even be mostly automated. A study by Charles Schwab and Strategic Insights showed that those who make a plan retire with 2.7X as much money as those who do not. Perhaps most importantly, a plan reduces your financial stress, which according to the American Psychological Association, is the leading cause of stress in America. Don't believe me that you really need an investing plan? Check out this study from the Goldman-Sachs Retirement Survey and Insights Report 2025:

How to Get an Investing Plan

There are a number of ways to get an investing plan. It's really a spectrum or a continuum. On the far left side, you will find the options that cost the least amount of money but require the largest amount of interest, effort, and knowledge. On the far right side are the most expensive options that require little knowledge, effort, or interest. Here's what the spectrum looks like:

There are really three different methods here for creating an investment plan.

#1 Do It Yourself Investment Plan

The first method is what I did. You read books, you read blog posts, and you ask intelligent questions on good internet forums. This can be completely free, but usually, people spend a few dollars on some books. It will most likely require a hobbyist level of dedication. That's okay if you have the interest, being your own financial planner and investment manager is the best paying hobby there is. On an hourly basis, it usually pays better than your day job. I have spent a great deal of time over the years trying to teach hobbyists this craft.

#2 Hire a Pro to Create Your Plan

On the far side of the spectrum is what many people do, they simply outsource this task. This costs thousands of dollars per year but truthfully can require very little expertise or effort. In order to reduce costs, some people start here and have the pro draw up the plan, then they implement and maintain it themselves. I have also spent a lot of time and effort connecting high-income professionals with the good guys in the industry who offer good advice at a fair price.

#3 WCI Online Course

However, after a few years, I realized there was a sizable group of people in the middle of the spectrum. These are people who really don't have enough interest to be true hobbyists, but they are also well aware that financial services are very expensive. They simply want to be taken by the hand, spoon-fed the information they need to know in as high-yield a manner as possible, and get this financial task done so they can move on with life.

They're not going to be giving any lectures to their peers or hanging out on internet forums answering the questions of others. So I designed an online course, provocatively entitled Fire Your Financial Advisor.

While more expensive than buying a book or two and hanging out on the internet, it is still dramatically cheaper than hiring a financial advisor and so is perfect for those in the middle of the spectrum. Plus it comes with a 1-week no-questions-asked, money-back guarantee. To be fair, some people simply use the course (especially the first module) to gain a bit of financial literacy so they can know that they are getting good advice at a fair price. While for others, the course is the gateway drug to a lifetime of DIY investing.

And of course, whether your plan is drawn up by a pro, by you after taking an online course, or by you without taking an online course, it is a good idea to get at least one second opinion from a knowledge professional or an internet forum filled with knowledgeable DIYers. You wouldn't believe how easy it is to identify a crummy investing plan once you know your way around this stuff.

So, figure out where you are on this spectrum. If you find yourself on the right side, here is my list of WCI vetted financial advisors that will give you good advice at a fair price.

If you are looking for the most efficient way to learn this stuff yourself, I highly recommend WCI's Fire Your Financial Advisor course.

For the rest of you, keep reading and I'll try to outline the basic process of creating your own investment plan.

How Do You Make an Investing Plan Yourself?

#1 Formulate Your Goals

Be as specific as possible, realizing that you’ll make changes as the years go by. Examples of good goals include:

- I want $40,000 for a home downpayment by June 30, 2013.

- I want to have enough money to pay the tuition at my alma mater in 13 years when my 5-year-old turns 18.

- I want to have $2 Million saved for retirement by Jan 1, 2030.

Any goal is better than no goal, but the more specific and the more accurate you can be, the better.

#2 Set Up a Plan for Each Goal

The plan consists of identifying what type of account you will use to save the money, choosing the amount you will put toward the goal each year, working out an asset allocation likely to reach the goal with the minimum risk necessary, and identifying a plan B for the goal in case the returns you’re planning on don’t materialize. Let’s look at each of the goals identified in turn and make a plan to reach them.

Investing Plan Goal Examples

Goal #1 – Save Up for a Home Downpayment

Choose the Type of Account

In this case, the best option is a taxable account since it will be relatively short-term savings and you don’t want to pay a penalty to take the money out to spend it. A Roth IRA may also be a good option for a house down payment.

Choose How Much to Save

When you get to this step it is a good idea to get familiar with the FV formula in excel. FV stands for future value. There are basically 4 inputs to the formula-how much you have now, how many years until you need the money, how much you will save each year, and rate of return. Playing around with these values for a few minutes is an instructive exercise.

Also, knowing what reasonable rates of return are can help. If you put in a rate of return that is far too high (such as 15%) you’ll end up undersaving. Since you need this money in just 2 ½ years you’re not going to want to take much risk, so you might only want to bank on a relatively low rate of return and plan to make up the difference by saving more. You decide to save $1400 a month for 28 months to reach your goal. According to excel, this will require a 1.8% return.

Determine an Asset Allocation

This is likely the hardest stage of the process. Reading some Bogleheadish books such as Ferri’s All About Asset Allocation or Bernstein’s 4 Pillars of Investing can be very helpful in doing this. In this case, you need a relatively low rate of return. The first question is “can I get this return with a guaranteed instrument”…i.e. take no risk at all.

Usually, you should look at CDs, money market funds, bank accounts, etc to answer this question. MMFs are paying 0.1%, bank accounts up to 1.2% or so, 2 year CDs up to 1.5%, so the answer is that in general, no, you can’t.

One exception at this particularly unique time is a high-interest checking account. By agreeing to do a certain number of debits a month, you can get a rate up to 3%-4% on up to $25K. So that may work for a large portion of the money. In fact, you could just open two accounts and get your needed return with no risk at all.

A more traditional solution would require you to estimate expected returns. Something like 0% real (after-inflation) for cash, 1-3% real for bonds, and 3-6% real for stocks is reasonable. Mix and match to get your needed return.

“Plan B”

Lastly, you need a plan in case you don’t get the returns you are counting on, a “Plan B” of sorts. In this case, your plan B may be to either buy a less expensive house, borrow more money, make offers that require the seller to pay more of your closing costs, or wait longer to buy.

Goal #2 – Saving for College

4 years tuition at the Alma Mater beginning in 13 years. Let’s say current tuition is $10K a year. You estimate it to increase at 5%/year. So 13 years from now, tuition should be $19,000 a year, or $76K. Note that you can either do this in nominal (before-inflation) figures or in real (after-inflation) figures, but you have to be consistent throughout the equation.

Investment Vehicle

You wisely select your state’s excellent low cost 529 plan which also gives you a nice tax break on your state taxes.

Savings Amount

Using the FV function again, you note that a 7% return for 13 years will require a savings of $4,000 per year.

Asset Allocation

You expect 3% inflation, 5% real so 8% total out of stocks and 2% real, 5% total out of bonds. You figure a mix of 67% stocks and 33% bonds is likely to reach your goal. Since your Plan B for this goal is quite flexible (have junior get loans, pay for part out of then-current earnings, or go to a cheaper school,) you figure you can take on a little more risk and you go with a 70/30 portfolio.

“Plan B”

Have junior get loans or choose a cheaper college.

Goal #3 – $2 Million Saved for Retirement by Jan 1, 2030

Let’s attack the third goal, admittedly more complicated.

You figure you’ll need your portfolio to provide $80K a year (in today's dollars) for you to have the retirement of your dreams. Using the 4% withdrawal rule of thumb, you figure this means you need to have portfolio of about $2 Million (in today's dollars) on the day you retire, which you are planning for January 1st, 2030 (remember it is important to be specific, not necessarily right about stuff like this–you can adjust as you go along.)

You have $200K saved so far. So using the FV function, you see that you have a couple of different options to reach that goal in 19 years. You can either earn a 5% REAL return and save $49,000 a year (in today's dollars), or you can earn a 3% REAL return and save $66,000 a year (again, in today's dollars).

Remember there are only three variables you can change:

- return

- amount saved per year

- years until retirement

Fix any two of them and it will dictate what the third will need to be to reach the goal.

Investment Vehicle

Roth IRAs, 401(k), taxable account

Savings Amount

$49,000/year

Asset Allocation

After much reading and reflection on your own risk tolerance and need, willingness, and ability to take risk, you settle on a relatively simple asset allocation that you think is likely to produce a long-term 5% real return:

35% US Stock Market

20% International Stock Market

20% Small Stocks

25% US Bonds

“Plan B”

Work longer or if prevented from doing so, spend less in retirement

You have now completed step 2, setting up a plan for each goal. Step 3 is relatively simple at this point.

Select Investments

The next step is to select the best (usually lowest cost) investments to fulfill your desired asset allocation. Using all or mostly index funds further simplifies the process.

Investment Plan Example #1 – Retirement Portfolio

Let’s take the retirement portfolio. You have $200K in Roth IRAs and plan to put $5K a year into your IRA and your spouse’s IRA each year through the back-door Roth option. You also plan to put $16.5K into your 401K each year. Unless your spouse also has a 401K, you're going to need to use a taxable account as well to save $49K a year. Your 401K has a reasonably inexpensive S&P 500 index fund which you will use as your main holding for the US stock market. It also has a decent PIMCO actively managed bond fund you can use for your bonds. You’ll use the Roth IRAs for the international and small stocks. So in year one, the portfolio might look like this:

His Roth IRA 40%

25% Total Stock Market Index Fund

20% Total International Stock Market Index Fund

Her Roth IRA 45%

20% Vanguard Small Cap Index Fund

25% Vanguard Total Bond Market Fund

His 401(k) 5%

5% S&P 500 Index Fund

His Taxable account 5%

5% Vanguard Total Stock Market Index Fund

As the years go by, the 401K and the taxable account will make up larger and larger portions of the portfolio, necessitating a few minor changes every few years.

After this, all you need to do to maintain the plan is monitor your return and savings amount each year, rebalance the portfolio back to your desired asset allocation (which may change gradually as you get closer to the goal and decide to take less risk), and stay the course through the inevitable bear markets and scary economic times you will undoubtedly pass through.

Investment Plan Example #2 – Taking Less Risk

Let’s do one more example, just to help things sink in. Joe is of more modest means than the guy in the last example. He works a blue-collar job and can really only save about $10K a year. He would like to retire as soon as possible, but he admits it was hard to watch his 90% stock portfolio dip and dive in the last bear market, so he isn’t really keen on taking that much risk again. In fact, if he had to do it all over again, he’d prefer a 50/50 portfolio.

He figures he could get 5% real out of his stocks, and 2% real out of his bonds, so he expects a 3.5% real return out of his 50/50 portfolio. Joe expects social security to make up a decent chunk of his retirement income, so he figures he only needs his portfolio to provide about $30K a year. He wants to know how long until he can retire. He has a $100K portfolio now thanks to some savings and a small inheritance.

Goal

A portfolio that provides $30K in today’s dollars. $30K/.04=$750K

Type of Account

He has no 401K, so he plans to use a Roth IRA and a SEP-IRA since he is self-employed.

Savings Amount

He is limited to $10K a year by his wife’s insistence that the kids eat every day.

Asset Allocation

He likes to keep it simple, so he’s going to do:

30% US Stocks

20% Intl Stocks

25% TIPS

25% Nominal bonds

He expects 3.5% real out of this portfolio. Accordingly, he expects he can retire in about 29 years. =FV(3.5%,29,-10000,-100000)=$760,295

Plan B

His wife will go back to work after the kids graduate if they don’t seem to be on track

Investments

Year 1

Roth IRA 30%

VG TIPS Fund 25%

TBM 5%

Taxable account 65%

TSM 30%

TISM 20%

TBM 20% (he’s in a low tax bracket)

SEP-IRA 5%

VG TIPS Fund 5%

So now we get back to the questions like those in the beginning of this post: “I have $50K that I need to invest. Where should I put it?” The first consideration is why haven’t you invested it yet? You should be investing the money as you make it according to your investing plan. If your retirement accounts have already been maxed out for the year, then you simply invest it in a taxable account according to your asset allocation.

A few last words about developing an investment plan:

If you fail to plan, you plan to fail.

Any plan is better than no plan.

The enemy of a good plan is the dream of a perfect plan.

There are no old, bold [investors].

What do you think? What is the best way to get an investment plan? Why do so many investors invest without a plan?