As Ben Franklin once famously said, There are only two certainties in life—death and taxes. Yet, one could make the somewhat morbid argument that people tend to dread the latter more than the former. For those who didn’t major in finances, paying taxes in the United States seems like the most needlessly complicated process ever. And if you go about it the wrong way, you could be paying too much and robbing yourself of hard-earned income.

Thankfully, you’ve come to the right place. We’ve broken down the ins and outs of tax-paying so that even the biggest tax-phobes can follow along.

What Are Taxes?

In the simplest terms, taxes are fees that we pay to the government to fund government spending. Taxes are collected by different levels of government, including federal, state, county, city, and township, and they can vary wildly depending on where you live. There are also various ways in which government institutions collect taxes.

Direct Taxes

Direct taxes are self-explanatory in that they are taxes we pay directly to the government. They can come in many forms but are most commonly associated with income taxes and property taxes. These taxes are also calculated on a sliding scale depending on factors such as how much money someone makes or the value of their property. That way, the taxpayer’s overall worth, based on income and assets, dictates their ability to pay direct taxes.

Income Tax

Income tax refers to the taxes taken out of our paychecks, and it's the money that the government collects from individuals and businesses throughout the year. It’s also the primary reason most people need to file yearly taxes. Again, how much income tax an individual pays is dependent on how much money they make in a year. So higher earners pay higher tax rates since they can afford to pay more money to the government.

Payroll Tax

Income tax isn't all that's taken out of your salary. Payroll tax, which is what's used to fund government programs like Medicare and Social Security, is also taken out by your employer and paid to the government. If you're looking at your paystub and you see money that's earmarked for FICA or MEDFICA, those are your payroll taxes. But unlike income tax, there are certain levels where the government stops taking that payroll tax. For example, once your earned income surpasses $147,000 for the 2022 tax year, you can stop paying into Social Security for the rest of the year.

Capital Gains Tax

While most people who receive a steady paycheck will pay income taxes, capital gains taxes aren’t something many people have to worry about (though high earners and white coat investors certainly might). Capital gains tax refers to money owed to the government out of any profits generated from selling assets such as stocks, bonds, real estate, and property. Similar to other types of direct taxes, how much tax is owed depends on the value.

For example, say you’re selling a used car. If you sell that car for less than you paid for it, no taxes are owed from that transaction. However, if you’re selling a valuable automobile that has significantly gone up in value since it came into your hands, any profits made in that transaction are considered “capital gains.” As such, you may be liable to pay taxes on them.

Indirect Taxes

In contrast, indirect taxes refer to taxes we pay on goods and services, such as sales and services taxes in the US. Some countries have value-added taxes (VAT), which are indirect taxes that work similarly to standards sales tax. The difference is that sales taxes are paid by the consumer at the point of sale, and 100% of the tax goes directly to the government. With VAT, the burden might fall between both the business owner and the consumer.

Unlike direct taxes, everyone across the board pays the same amount of indirect taxes. In other words, someone who makes $35,000 per year will pay the same amount of tax on the same items as someone who makes six figures.

When Are Taxes Due?

Generally speaking, individual income tax returns are due on Tax Day, which typically falls on April 15 every year. But if Tax Day occurs on a weekend or holiday, it will be delayed until the following Monday and could be as late as April 18, as was the case in 2022.

However, those who are self-employed or who have other sources of income might be required to pay quarterly estimated taxes, which are due on or after April 15, June 15, September 15, and January 15, respectively. Be aware that if you don't pay those quarterly estimated taxes, the IRS might punish you for it.

How to Get a Tax Extension

Anyone is eligible to file for a tax extension, which allows a six-month extension until October 15. People tend to file for tax extensions for common reasons such as general disorganization, incomplete tax documentation, or unexpected life events.

Filing for a tax extension is also relatively easy and straightforward—simply fill out the IRS Form 4868 and submit it by April 15, or whichever date the return was due.

However, filing for an extension does not get you out of paying your taxes on time. Those who anticipate a refund can receive an extension penalty-free; the only downside is that you’ll have to wait longer to get your payment. But if you know you’re going to owe money with your tax return, a good rule of thumb is to estimate how much taxes you’ll owe and pay the amount when you file the extension form.

Even if you can’t afford to pay your taxes, it’s still better to file an extension than not. The penalty for failing to file is typically about 5% of the total amount owed per month, although it could be as much as 25% depending on your tax bracket. On the other hand, the late payment penalty is only 0.5% owed of the monthly amount.

When Will I Get My Tax Refund?

Getting your tax refund is quicker and easier than ever if you file electronically and set up direct deposit, which the IRS recommends. Typically, you can expect to see your refund issued within three weeks of e-filing your tax return though any filing errors could delay things. You can even use free tools provided by the IRS to determine precisely when your refund will show up.

Although everyone loves a tax refund, many argue that it’s actually better to owe money than receive it. Otherwise, you’re essentially giving the government an interest-free loan. Overpaying taxes can take a chunk out of your income that could be better spent paying off loans or saving for your retirement, so you may want to adjust the withholdings on your W-4 form accordingly.

How Much Tax Do I Pay?

We’ve already established that income tax is based on income—and that higher earners fall into higher tax brackets and therefore pay higher rates of taxes. However, to ascertain precisely how much you’ll owe in taxes, there are plenty of free and convenient income tax calculators online, which calculate based on your income, location, and filing status.

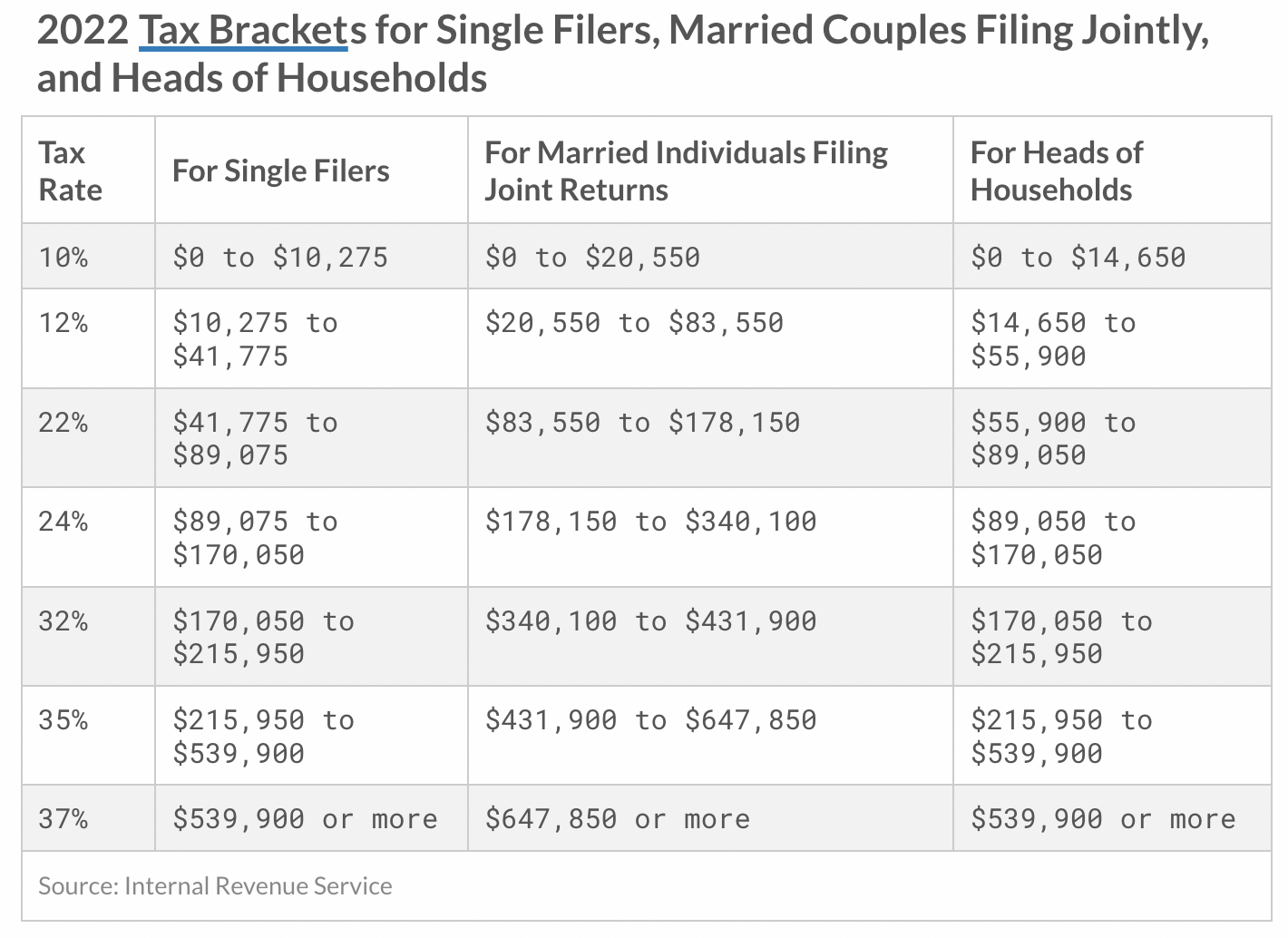

How Do Tax Brackets Work?

The percentage of your taxable income is calculated with marginal tax rates, otherwise known as your tax bracket. So, relative to how much a taxpayer earns, they might pay a marginal tax rate of anywhere from 10%-37% on the last tax dollar owed.

The following chart breaks down the 2022 tax brackets for unmarried individuals, married individuals filing jointly, and heads of households [visit our annual numbers page to get the most up-to-date figures].

Although it seems straightforward, many people don’t understand how tax brackets work and often overestimate how much they pay.

For example, if an individual earns $75,000 per year, they don’t pay the marginal tax rate on the total amount of their salary—but 10% on the first $10,275; 12% up to $41,775; and so on. In other words, they only pay the full 22% on anything over $41,775.

Marginal Tax Rates vs. Effective Tax Rates

We’ve already established that your marginal tax rate refers to individual tax brackets—or the amount of tax that applies to each level of income.

On the other hand, effective tax rates refer to the total share of annual income that a taxpayer needs to pay. To determine your effective tax rate, simply divide your total tax liability by your yearly gross income. In other words, if someone made $100,000 per year and paid $25,000 in taxes, their total effective tax rate would be 25%.

How to Pay Less in Taxes

We all want to pay less in taxes—that’s the dream, right? Fortunately, there is no shortage of legal ways to skirt the government legally, but the easiest is simply to open a tax-deferred retirement account such as your employer’s 401(k) plan or a cash balance plan. Since a tax-deferred retirement account, like a 401(k) or a 403(b), uses pre-tax money, your taxable income that is used to determine how much you owe on Tax Day is reduced. The smaller your taxable income, the less you pay in taxes.

If you don’t have a 401(k) plan—or even if you do and are exploring additional tax-deferred retirement plans—traditional and Roth IRAs are another great way to keep as much of your money from Uncle Sam.

Other ways are to take advantage of a Health Savings Account (HSA), which allows for tax exemptions on income spent on health care. Many employers offer HSAs as part of their healthcare plans; however, independent contractors can also arrange to have them put in place.

But those are just a few of many ways to pay less in taxes, and if you’re unsure, it might be worth consulting with an experienced tax strategist to learn how you can stretch your income as far as it will go.

Tax Deductions

In addition to the methods described above to pay less in taxes, there are other ways to get creative with tax deductions to pay fewer taxes.

Those who are self-employed can also deduct health insurance premiums, home office space, and other business-related expenses—such as travel, meals, equipment, supplies, and communication expenses—to save big bucks.

Charitable contributions are also tax-deductible. In addition to monetary donations, you can also calculate everything from expenses incurred with donating your time volunteering to the value of items donated to Goodwill—and even associated travel costs. TurboTax even provides a free ItsDeductible calculator to help determine the value of donated items, making the process streamlined and straightforward.

How Many Allowances Should I Claim on My W-4?

When you start a new job and fill out a W-4 form, that indicates to your employer how much money should be withheld from your paycheck for taxes. But that number is not set in stone, and claiming allowances gives you some wiggle room for how much or how little is withheld from your paycheck.

A good rule of thumb is that the more allowances you claim, the less money is withheld from your paycheck. On the flip side, claiming fewer allowances means that more money is withheld from your paycheck, and you’ll be more likely to receive a refund.

It makes sense for a single filer with one job and no children to claim just one allowance, whereas a married couple who each has a job will likely claim two allowances. Generally, those with two or more children can claim an allowance per child.

How to File Taxes

To prepare your taxes, whether you're filing yourself or working with a professional, the first step is to gather your various tax documents. These include your W-2 forms for full-time employees, 1099 forms for independent contractors, mortgage interest statements, investment income statements, and charitable contribution statements.

You also need to determine your tax filing status, which we’ll outline below, and then decide how you want to file your taxes. If filing yourself, the IRS recommends e-filing with tax preparation software such as TurboTax or H&R Block for the easiest and most accurate returns.

More information here:

How Do Student Loans Impact Your Taxes?

Tax Filing Status

Single—Those who are unmarried, divorced, legally separated, or even widowed previous to the tax year will most likely file as a single taxpayer.

Married Filing Jointly—Most married couples opt to file a joint tax return, which typically saves money and time.

Married Filing Separately—There is no requirement for married partners to file a joint return, and they may file separately if they so wish, for one reason or another.

Head of Household—To file as head of household, an individual must have covered more than half of the household expenses for the qualifying year and have a child or dependent, such as an ailing family member.

Qualifying Widow(er)—If a spouse dies, the surviving spouse can opt to file jointly with the deceased spouse two years following the year of death, as long as they don’t remarry and live with a qualifying dependent.

More information here:

How Does Married Filing Separately Affect Student Loans?

What Is a Tax Audit?

Tax audits typically occur when the IRS notices an error or discrepancy with your tax return and reaches out for clarification to determine whether your income and deductions are accurate. While no one wants to be on the receiving end of an audit, you can take solace knowing that they’re increasingly rare and can usually—but not always—be resolved relatively quickly.

The most common form of tax audit is a mail, or “correspondence,” audit, in which the IRS requests additional documentation to clarify that the information you entered is correct. In many instances, these audits are sorted out simply by mailing in additional forms or information, such as proof of deductions.

In more extreme situations, the IRS may conduct office or field audits conducted in person at a local IRS office, your home, or place of business. However, these audits generally arise when the IRS is questioning more than a deduction or two. In that case, the IRS will thoroughly examine most or all line items in your return. You also have the right to legal representation in these instances.

But if audits are uncommon in general, office and field audits are even rarer, and there are very likely legitimate concerns for the audit to happen in the first place.

In many cases, white coat investors choose to go through the process of paying taxes on their own. But for those high earners who are involved in complex investments or who are building real estate empires or who like to dabble in cryptocurrency, hiring a tax strategist can be a smart move. If you're in the latter category, WCI has a number of vetted professionals who can help you figure out the tax landscape and assist you in lowering how much in taxes you actually have to pay.

The White Coat Investor is filled with posts like this, whether it’s increasing your financial literacy, showing you the best strategies on your path to financial success, or discussing the topic of mental wellness. To discover just how much The White Coat Investor can help you in your financial journey, start here to read some of our most popular posts and to see everything else WCI has to offer. And make sure to sign up for our newsletters to keep up with our newest content.