There are 195 countries in the world today. However, when it comes to publicly traded stocks, 60% of the market capitalization is in the United States, as of late 2022.

It hasn't always been that way. In fact, Japan in 1989 had a higher market capitalization than the US did. It has been highly variable over the last century plus.

Yes, the US has been a huge player, but it has never been the only game in town. Despite that fact, people these days are making arguments not to invest in international stocks at all. These arguments include:

- US companies do business all over the world.

- Jack Bogle said you don't need international stocks.

- The US has the strongest property laws so they will have the best long-term returns.

- International markets are corrupt.

But let's be honest, the real reason that people are avoiding international stocks and justifying their behavior is simply that

- Over the last 15 years, the US stock market has returned 9.7% per year, and international stock markets have only returned 2.93% per year.

It's just performance chasing.

Every mutual fund is required to put a statement in its prospectus that says something like . . .

“Keep in mind that the Fund’s past performance (before and after taxes) does not indicate how the Fund will perform in the future.”

They have to put it in there because it's true, even if nobody believes it.

The Case for International Stocks

The primary reason to invest internationally is diversification. While the stock markets of the world have become more correlated over time, they are not perfectly correlated. They perform differently and provide important diversification benefits. Imagine being an investor in the Russian stock market in the 1910s. It was going great right up until the time the Reds beat the Whites and capitalism was abolished. A similar thing happened to investors in the 1940s Chinese stock market. The Japanese stock market might not have imploded after the 1980s, but it certainly didn't do its investors any favors. How about the German stock market after Stalingrad? You get my point.

While it seems very unlikely, the US could be the next Russia, China, Japan, or Germany. Why put all your eggs in one basket? Even if you only look at the individual companies, keep in mind that 8,000 of the 12,000 publicly traded companies in the world are not in the United States. Why would you exclude two-thirds of the companies from your portfolio?

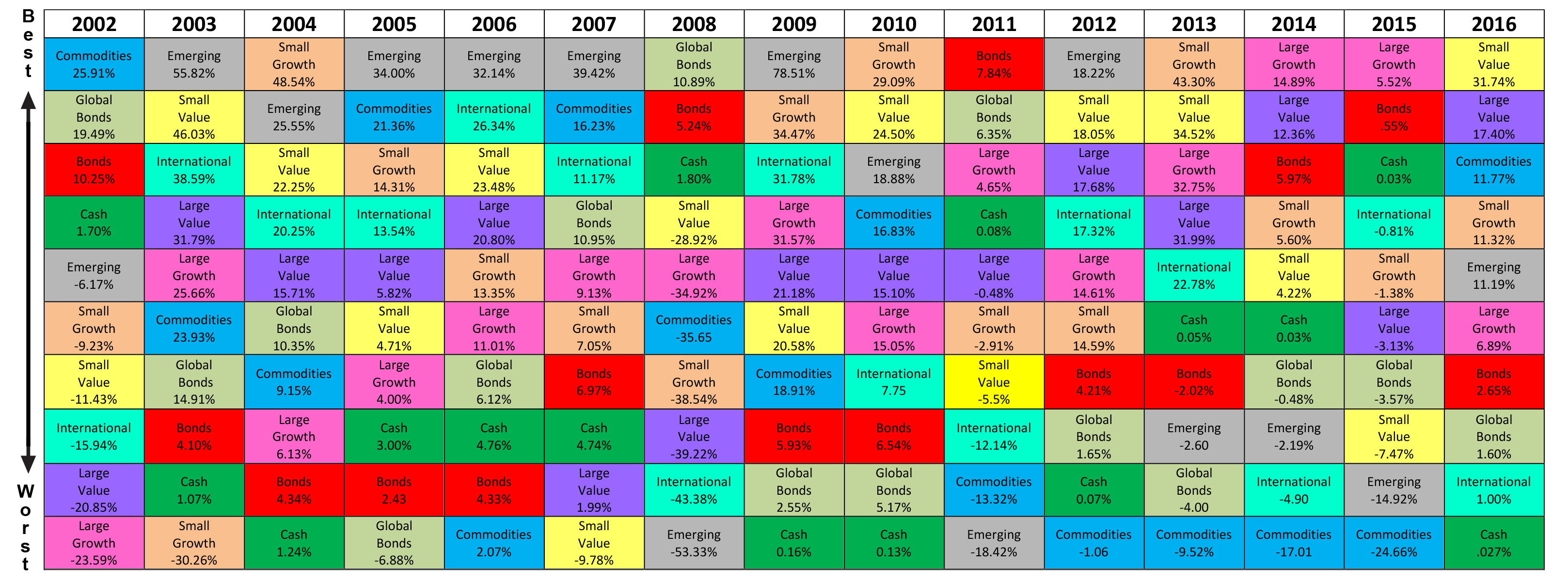

If you look at the historical data (and the best data for international stocks only goes back to 1973), you can see that sometimes US stocks outperform and sometimes international ones do.

In this chart, the red bars are where international outperformed and the yellow bars are where the US outperformed. As you can see, it swings back and forth, but one can remain the winner for many years in a row before you see a “return to the mean” or “mean reversion” and the other outperforms for a while. But it doesn't take a genius to see where the recent trend has been. Since 2008, international stocks have only won four times and never convincingly.

More information here:Why Have US Stocks Outperformed International Stocks So Much Recently?

There are a lot of factors that explain the most recent outperformance for US stocks, but the most significant one is simply the strengthening of the dollar over that time period. Check out this historical chart of the euro/US dollar exchange rates:

In 2008, you needed $1.60 to buy a euro. More recently, they've traded at 1:1. The euro has lost 38% of its value in comparison to the dollar. The pound sterling has fallen from $2.10 to $1.20. The yen, yuan, Canadian dollar, Australian dollar, Indian rupee, and Mexican peso all tell a similar story. The international stock performance reported to you by Vanguard and other mutual fund companies and brokerages include the effects of currency fluctuation. It isn't that these companies aren't profitable and growing. It's simply that they are not as profitable in US dollars as they were when the US dollar was weaker.

Think of it as a headwind for international stocks and a tailwind for US stocks. It hasn't been that long since we had our own problems. Remember that “lost decade” of the 2000s, when the S&P 500 had a total return of -0.95% per year? Well, developed market stocks returned 1.17% per year, and emerging markets stocks returned 9.78% per year that decade. If you had decided after that performance that the future of the world was in emerging markets and swapped your US stocks for EM stocks that year, you would have been punished for your performance chasing.

The pendulum swings. Obviously, timing the market perfectly and jumping between them would be very profitable, but since your crystal ball is likely as cloudy as mine, getting that timing just right is going to be pretty tricky.

More information here:Where Should You Hold International Stocks?

International Stocks Are Smaller and More Valuey

The Fama-French 3 factor model for equity argues that stock returns are primarily explained by market risk, size risk, and value risk factors. Over the last 10+ years, large growth stocks have outperformed. However, just like the relative value of the dollar to foreign currencies is cyclical, so is the performance of large stocks to small stocks and growth stocks to value stocks. However, what many people do not realize is that the US market is far more of a large growth market than the international market. Consider the Morningstar X-rays of the US Total Stock Market Fund:

The US market is 33% large growth. More broadly, it is 40% growth to just 22% value and 72% large to 9% small. The X-ray of the Total International Stock Market Fund looks significantly different:

Only 21% large growth and the overall ratio is 27% growth to 31% value. While the X-ray does not seem to show that TISM is smaller than TSM, the median market capitalization is significantly smaller: $29.5 billion to $109.5 billion. The Price to Earnings (P/E) ratio is a ratio of valueyness (the lower the ratio, the more valuey the company). TSM has a P/E ratio of 18.1 and TISM has a ratio of 11.2.

When the pendulum inevitably swings away from large growth stocks toward small value stocks, that will provide a boost to international stocks.

Trees Don't Grow to the Sky

My crystal ball is cloudy. I don't know WHEN international, small, and value stocks will outperform US, large, and growth stocks for a significant period of time. What I do know is that it will happen. If something cannot continue forever, it must stop. Trees don't grow to the sky. It was within my relatively short investing career that the US made up less than half of world market capitalization. It is now about 60%. The US is not going to become 99% of the world market capitalization. Right now, you can buy a dollar of earnings overseas for just $11.20. That same dollar of earnings in the US will cost $18.10. That spread usually exists, but it has never been as large as it is now.

This is clearly NOT the time to abandon international stocks. That's just performance chasing, and it usually leads to regret.

More information here:Best Investment Portfolios – 150 Portfolios Better Than Yours

Future Return Forecasts

Forecasting the future is notoriously difficult, particularly in the short term. It's a little easier in the long run, though, because valuations start to matter more. As Benjamin Graham famously said,

“In the short run, the market is a voting machine, but in the long run it is a weighing machine.”

What do market forecasters think about future international stock returns? Well, let's take a look at the most recent forecasts from Vanguard.

There is a lot to learn from a chart like this. The first is that it is a probabilistic chart. There is a 90% chance that US stock returns will be between -1.3% and 12.9% per year over the next 10 years. But that's obviously a huge range. For international stocks, that same range is 2.2% to 14.9%. The best guess is 8.4% for international vs. 5.7% for US, but it is entirely possible that predicted returns for both US and international stocks can be accurate (i.e., within the middle 50%) and US stocks could still outperform international. I wouldn't bet that way, though. Valuations have limited predictive power, but they do have some. Plus, international stock valuations are just far more attractive right now than US stock valuations.

What Should You Do?

I hope I sound like a broken record when I say this, but my recommendation is that you set up a fixed (static) asset allocation for your portfolio, fund it adequately, and then hold it through thick and thin. A reasonable allocation for international stocks for a US investor ranges from 10%-50% of equity. My own ratio is 33%. When international stocks underperform, you should put more of your new investing dollars into them to bring your asset allocation back in line with your written investing plan. When US stocks underperform, you should do just the opposite. If things really get out of whack and you can't rebalance just with new money, you should sell (preferably in a tax-protected account) some of the assets that have done well and buy some of the assets that have done poorly—at least once every two or three years.

What you should not do is say to yourself, “Man, these performance numbers for international stocks look terrible. I'm going to quit investing in them.” That is highly likely to lead to regret. Maybe not this year. Maybe not even five years from now. But eventually, you are likely to regret investing while looking in the rearview mirror.

If you need help getting a real investing plan, either hire a good fee-only advisor who charges a fair price for good advice or take our Fire Your Financial Advisor online course. There's even a version that qualifies for CME.

What do you think? Are you making any changes to your international stock allocation? Why or why not? Do you think international will eventually outperform US stocks?