As an investor in international stocks via several index funds, I’ve considered and reconsidered in which account I ought to hold those funds.

The primary goal of asset location is to increase the tax-efficiency of your portfolio, at least it will be for most people. You want to pay the lowest amount of tax on your chosen asset allocation.

That “al” is an important distinction. Asset allocation determines what you own and in what percentages. Asset location defines in which accounts you hold the assets you own.

My assumption has been that the taxable brokerage account is the best place for international funds for a few reasons that I’ll discuss below, but I have never put that theory to the test.

With the aid of—what else—a spreadsheet, we’ll determine what is the optimal location for your international stock allocation.

International Stocks and Asset Location: Is Taxable or Tax-Advantaged Best?

In terms of asset location, there are two broad categories of account types: a taxable brokerage account and a tax-advantaged account.

The latter can be further broken down into tax-deferred accounts in which you typically get a tax deduction upfront and owe tax upon withdrawal or a tax-free account in which you place after-tax monies and pay no tax upon withdrawal.

Both tax-advantaged account types benefit from tax-free growth. You pay no taxes on dividend payments and owe no taxes on capital gains when you sell assets as long as the proceeds remain in the account.

Examples of tax-deferred accounts include the traditional IRA and 401(k). Tax-free accounts include the Roth IRA and Roth 401(k). A Health Savings Account (HSA) is a hybrid giving you the best of both account types when the money is spent on eligible healthcare expenses.

The taxable brokerage account can act a lot like a Roth IRA, but as long as you’re earning dividends and/or realizing capital gains, there will be some tax drag. You don’t get the tax-free growth that tax-advantaged accounts offer.

Hypothesis: International Stocks Belong in a Taxable Account

I’ll admit to not knowing much about investing when I first had real money to invest. I knew enough to avoid big mistakes, but I never considered a more advanced question such as the one we’re answering today.

I had read somewhere that owning international stocks in a taxable account allowed you to take advantage of the Foreign Tax Credit, and that was good enough for me.

You see, when you own non-U.S. stock funds as a U.S.-based investor, those funds pay taxes to foreign entities, and as a shareholder, you’re indirectly paying those taxes. You don’t have to write a check or file any forms; it’s just an operating expense that impacts the total return of your holdings.

As a result, the IRS gives you credit for those foreign taxes paid when you fill out Form 1116 as part of your 1040. As you may have seen when I released my 2019 tax return, I received a $1,665 foreign tax credit that year, thereby paying $1,665 less than I would have if I didn’t own any international stocks in my brokerage account.

Clearly, my original hypothesis based on something I read somewhere—and then acted upon with hundreds of thousands of dollars—is correct, right?

Calculating the Tax-Efficiency of International Stocks

Like so many “yes or no” questions, the answer is neither of those words.

How do the trusted Bogleheads answer the question in their wiki?

“If all else is equal, the existence of the credit may make it advantageous to prioritize these funds in the taxable account. Whether or not the foreign tax credit is sufficient depends on such factors as the the percentage of the fund’s foreign source income component, the foreign tax rate, the percentage of the foreign dividends that are qualified, and the the US marginal tax bracket of the fundholder.”

They start with the same hypothesis that I did with a key caveat: “if all else is equal”. Whether or not that’s true depends on a number of factors.

Prior to looking back at that Bogleheads page on tax-efficient fund placement, I had put together a spreadsheet to do some calculations using all of those variables and then some.

Since I keep most of my money with Vanguard, I was able to choose popular index funds in the international and domestic stock categories that I currently have or have previously held in my own accounts.

On the international side, I looked at the Emerging Markets index fund, Total International Stock index fund, and the Developed Markets fund. Those were ordered in what I believed to be the least to most tax-efficient.

On the U.S. side, I chose the Small Cap Value index fund as a less tax-efficient fund, the Total Stock Market index fund, and the S&P 500 index fund. Again, these are ordered based on my preconceived notions of least to most tax-efficient.

Testing the Hypothesis

Most of the information required can be gathered from either Vanguard or Morningstar, and this post reflects year-end data from 2020.

I used Morningstar to obtain the annual dividend yield of each fund over the last year [as of August 2021], reported as Trailing Twelve Month yield on the “Quote” tab.

Vanguard gave me the percentage of dividends that were qualified dividends versus ordinary, non-qualified dividends. Vanguard also has a PDF file containing the foreign tax paid by each fund as a percentage of the dividend yield.

Finally, I had to determine how the dividend yield would be taxed, as tax drag will be an issue in the taxable brokerage account, but not in a tax-advantaged account.

The qualified dividends are taxed at a lower rate than the ordinary, non-qualified dividends unless you have very little in the way of income and your rate for both is 0%. Your total income from all sources would have to be less than the standard deduction [$12,550 in 2021 for single filers, $25,100 for those married filing jointly — visit our annual numbers page to get the most up-to-date figures] for that to be true.

I started with tax rate assumptions from my most recent tax return. My long-term capital gains rate, which is equal to my qualified dividends tax rate, is 15%. I have a modified adjusted gross income (MAGI) of over $250,000, so I pay the 3.8% Net Investment Income Tax (NIIT) on all dividends. Finally, I’m in Michigan, and we pay a flat 4.25% state income tax.

For the ordinary, non-qualified dividends, I use my marginal income tax rate of 24% and add in the NIIT and state income tax.

Here’s what I came up with.

Results

This spreadsheet shows us what we get for every $100,000 invested in a taxable brokerage account.

Based on the dividends and resulting taxes alone, the total international fund is the least tax-efficient. It spits out $2,440 in dividends, with 72% of those being qualified dividends.

Given my income level and state of residence, that dividend payout results in me owing $624 in taxes for every $100,000 I have in that fund (when owned in taxable).

Since the assumption is that this is held in a taxable account, I will get the benefit of the foreign tax credit. If I held it in a tax-advantaged account, that benefit is lost and cannot be reclaimed. That’s worth $228.02 for every $100,000 invested. The net result of owning $100,000 in VTIAX in the taxable account is a tax burden of $624 – $228 = $396.

How does that compare to a tax-efficient U.S. stock fund like the S&P 500 index, VFIAX?

The dividend yield is quite a bit lower, and all of those dividends are qualified. My total tax on $100,000 of the S&P 500 fund is $300. There’s no foreign tax credit, but even so, the tax burden as compared to the emerging markets fund is nearly 25% lower.

What about a more tax-efficient international fund? It turns out that in 2020, the Emerging Markets index fund (VEMAX) was more tax-efficient than usual. This results from a lower dividend payout than normal and a higher foreign income tax paid as a percentage of the dividend yield.

VEMAX kicked back $2,080 in dividends per $100,000 invested. About 46% of those were qualified dividends.

After subtracting a $244 Foreign Tax Credit from the $581 in taxes on the dividends, it would have cost me $337 to own VEMAX in a taxable brokerage account. That’s not quite as good as the $300 cost of owning the S&P 500 index, but it’s not much more. A $37 difference per $100,000 invested is quite small.

If one were to look at the total tax per dollar received as a dividend, the Emerging Markets fund actually wins with an 16.2% tax rate versus 23% on the S&P 500 dividends. I don’t think that’s the best way to look at it, though, since dividends don’t increase your net worth. They’re just the transfer of your marbles from one jar to another.

Your goal is to have as many marbles as possible, not to lose the smallest percentage when they’re moved around.

Discussion

Among these popular Vanguard funds, the two most tax-efficient funds are domestic U.S. funds, and the least tax-efficient, even after accounting for the Foreign Tax Credit, is an international fund, the Developed Markets fund. Yet, the asset location decision is not cut and dry based on the data above. The Emerging Markets fund is clearly more tax-efficient than the US small cap fund.

Let’s say someone’s asset allocation is a 50/50 split between the Total [U.S.] Stock Market index fund (VTSAX) and the Total International Stock index fund (VTIAX). Let’s also say that this person has room for $1 Million each in a brokerage account and a 401(k).

If our multimillionaire friend held the international fund in the 401(k) and the U.S. fund in taxable, she’d owe $2,879 in taxes (with the income and state of residency assumptions above).

Conversely, if she held the U.S. stock fund in the 401(k) and the million dollars in international stocks in a taxable brokerage account, she’d owe $3,957.

Keeping the international allocation in the taxable brokerage account where she can “take advantage” of the Foreign Tax Credit costs her $1,078 a year in this scenario.

So… do we have our answer? International belongs in tax-advantaged accounts?

What if I assumed I never left my full-time job in Minnesota and had great clinical income plus online income, launching me into the top tax bracket for the first time in my life.

Results for Big Money in Minnesota

In this example, the only adjustments I made are to the tax rate assumptions. Those who fortunately, find themselves in the top federal income tax bracket at 37% in 2021 also pay an additional 5% tax on qualified dividends and long-term capital gains.

If you’re lucky enough to live in Minnesota with a six-figure income, you’ve also got a marginal state income tax rate of 9.85% levied on both ordinary income and all dividend income. I realize I could have gone even higher in California and another state or two, but I chose an example closer to home.

This example would appear to seal the deal. The discrepancy in total tax burden only grows in favor of the domestic stock as income climbs. All three US funds cost less to own than the international funds, even after granting the Foreign Tax Credit

Once again, the least tax-efficient U.S. fund is the Small Cap Value index fund, but with higher tax rates on both our qualified and ordinary, non-qualified dividends, VSIAX is cheaper to own than any of the international funds, which top out at $711 per $100,000 for the Developed Markets fund.

The most tax-efficient fund in the basket, the Total Stock Market fund, only costs this Minnesota taxpayer $422 per $100,00.

What if, on the other hand, I made less money?

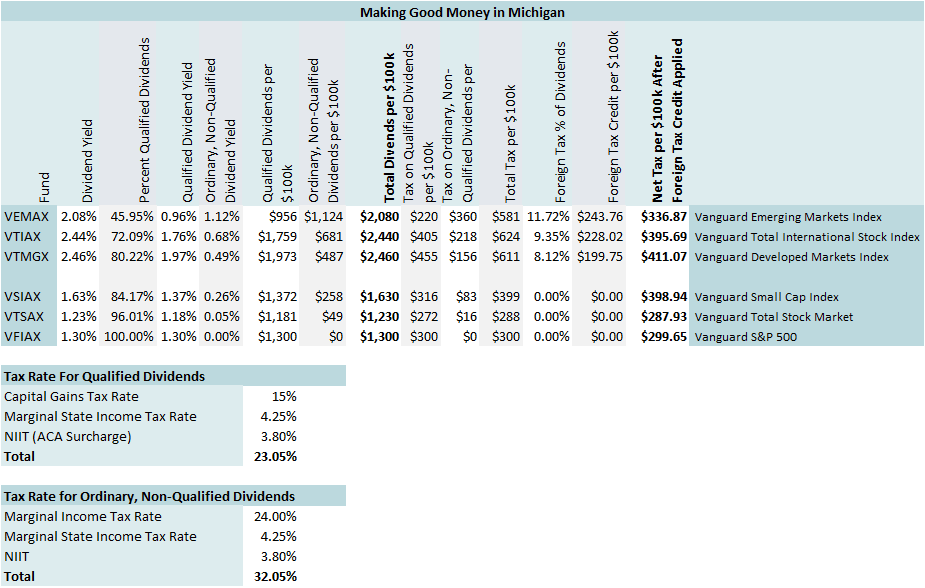

For the next example, we’ll see what happens if I’m back in the moderate-tax state of Michigan without the $250,000 in MAGI that subjects me to the NIIT.

We’ll use the 22% federal income tax bracket which represents an income in the range of $81,051 to $172,750 for a married couple filing jointly in 2021.

Results for Decent Money in Michigan

The gap between the taxation on the two types of dividends has narrowed to only a 7% difference (19.25% versus 26.25%). How does that impact what we owe?

Interesting. The tables seem to have turned at this income level.

The most tax-efficient fund is now VEMAX, the Emerging Markets fund, and the least tax-efficient fund is the US small cap index, VSIAX. The range is pretty narrow, with a difference between the lowest and highest tax burdens on these funds being $97 per $100,00.

I think it’s fair to say that, at this income level, it doesn’t matter much where you keep your international funds in terms of tax-efficiency. We’re now talking about dozens of dollars.

What will this spreadsheet look like for someone like me who was once a low-income resident at the University of Florida? Or if we were to retire to any no-state-income-tax state with less than $80,000 in taxable income?

Results for the Florida Medical Resident or Retiree

Nevermind that the medical resident won’t have $100,000 to invest in a taxable brokerage account and that many retirees won’t either.

Just know that it’s quite possible for the taxman to leaveth with income taxes disappearing entirely, even for a millionaire retiree.

Look at that!

Finally, we can see a situation in which there is a decided advantage to holding international funds in a taxable account. The IRS will, in fact, pay you to do so.

It is important to note, however, that the Foreign Tax Credit is not a refundable tax credit. That means if you truly have a federal income tax burden of zero, you won’t get a refund check.

If, however, you owe at least a little something at the end of the year, having international stocks in a taxable brokerage account will indeed lower your tax owed to the federal government. The same cannot be said for U.S. stocks (unless you sell them at a loss—more on that later).

Again, you should be able to find all of the information you need to fill in data for funds you own at Morningstar and at the brokerage that sells the funds.

Further Discussion

We’ve learned a few things in this exercise.

First, no there’s no right or wrong answer to the question of where your international allocation is best kept. If anything, we’ve disproved my hypothesis that the taxable brokerage account is the way to go.

If you do have five figures of taxable income or less, there is probably a slight advantage to holding international funds in taxable.

However, the benefit of doing so fades as your income increases into the low six figures, and if you’ve got multiple six-figures of income or more, you’ll see a bit of a disadvantage to keeping international stocks in taxable. Your mileage may vary depending upon the particular funds you select and the type and amount of dividends they pay.

Tax-Efficiency Is Not the Only Thing

In answering the question of optimal asset location, the only criteria we’ve used is tax-efficiency. What else is there to consider?

Cash Flow

Since the international index funds we looked at (currently) pay a higher dividend than their U.S. counterparts, owning them in a taxable account gives you more cash flow that’s easily accessible.

No, that’s not very tax-efficient, but if your goal is to have spending money, that goal is more easily accomplished with higher dividend-payers in taxable. And the Foreign Tax Credit does make an international fund more tax-efficient than a domestic stock or fund with the same dividend yield and ratio of qualified dividends.

Future Returns

Another consideration is the potential future return of the asset. If you expect strong returns from your small cap value fund, emerging markets fund, or any other asset, you may want to hold it in a Roth IRA because you’ll never have to pay taxes on any of that growth.

Taxable is another reasonable place to hold it, particularly if you think you may donate it or pass it on to an heir (with a stepped-up cost basis). There are several ways to avoid capital gains taxes completely.

A traditional, tax-deferred retirement account is not the ideal place to hold an asset that could give you great returns. One day you (or an heir) will be paying ordinary income taxes on that money when it’s withdrawn (or converted to Roth). The only exception is if you donate what would have been your RMD in the form of a Qualified Charitable Distribution directly to charity (up to $100,000 and not to a donor-advised fund).

Volatility and Tax Loss Harvesting

Finally, volatility can be a good thing when you hold it in a taxable account. Large price swings give you the opportunity to tax loss harvest (TLH).

Tax loss harvesting is exchanging one asset with a capital loss (worth less than what you paid for it) for another asset that is similar but not “substantially identical.” Doing so allows you to offset realized capital gains and deduct $3,000 against ordinary income per year. These efforts will save you thousands of dollars in taxes.

In the March of 2020, I was able to tax loss harvest with my admittedly tax-inefficient emerging market allocation in my Vanguard taxable brokerage account. For a complete guide on how to do this, please see my guides for TLH at Vanguard and TLH at Fidelity.

For example, when the markets were tanking in early 2020, I sold VEMAX shares on March 3rd and 9th, buying shares of IEMG (IShares Core MSCI Emerging Markets ETF) with the proceeds. I “banked” just over $5,000 in paper losses with these moves.

As the market continued to plummet, I sold the IEMG shares to buy SPEM (SPDR Portfolio Emerging Markets ETF). This resulted in an additional $17,125 in paper losses.

In three weeks, with this volatile asset class in a very volatile time, I have enough capital losses to deduct $3,000 against ordinary income for 7+ years. That can easily lead to $7,000 to $10,000 in tax savings over a 7-year timeframe.

Note that I remained invested in that asset class, so I didn’t lock in actual losses by selling and staying out of the market. As you probably know, the stock market rebounded nicely, and this is why my SPEM balance looks like six months after the transactions above.

The $127,530 worth of VEMAX is now $175,279 worth of SPEM as of August 2021, and I reported $22,175 in capital losses for 2020 in this asset class.

It’s true that most equities took a deep dive in that timeframe (I harvested a total of about $170,000 paper losses that month), but emerging markets are historically among the more volatile asset classes.

Where Should You Hold Your International Stocks?

I’ve held mine in my taxable account. Looking back, I realize that doing so actually cost me a bit of money over the last maybe 6 to 8 years when I had both a high income and a growing taxable account.

However, I was also preparing for an eventual retirement with a low taxable income—less than 20% of my portfolio is in tax-deferred accounts—and keeping international stocks in taxable does appear to be a good idea in that scenario.

There is also the benefit of cash flow in early retirement from those higher dividends, and perhaps the ability to tax loss harvest the more volatile emerging markets more frequently.

However, if tax-efficiency trumps all other factors and you plan to have a high taxable income along with a substantial taxable account balance, you may consider tucking that international allocation away in a tax-advantaged retirement account.

Where do you keep your international funds? What’s your rationale?