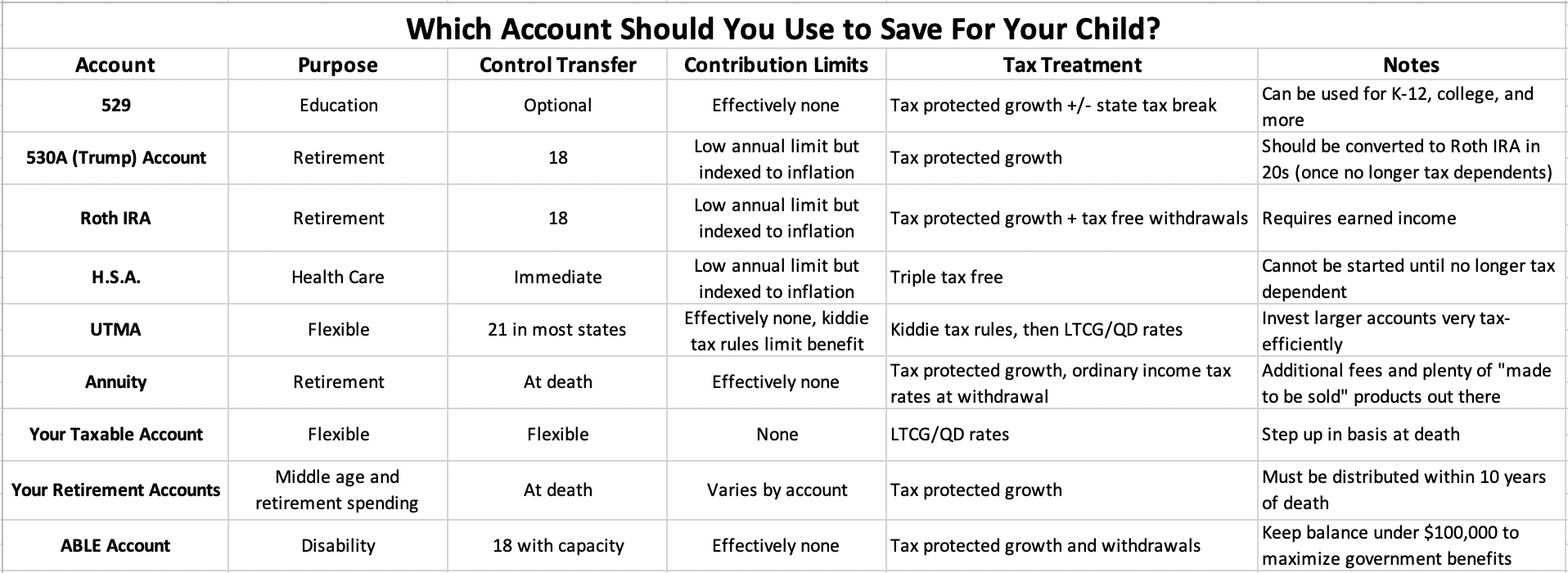

After a recent post about 530A (Trump) accounts, I was inundated with questions about whether to use this account or that account and about the differences between the various “child” accounts. I thought it would be helpful to put together a post (including a great chart) comparing them all. Let's start with the chart (click on it to expand it):

Now that you've seen that, let's get into a few details, strategies, and additional thoughts.

529 Accounts

529 accounts (and their country bumpkin cousin Coverdell Education Savings Accounts [ESAs]) were originally designed for college savings. But they can now also be used for K-12 (although you might not want to do that in New York) and plenty of other educational purposes. They offer some sort of state tax deduction or credit at contribution in about half of the states, and so long as the money is used for education, all earnings come out state and federal income tax-free. Not even New Jersey taxes those earnings.

Overfunded accounts can have the beneficiary changed to a sibling, grandkid, or even yourself, and up to $35,000 of an overfunded 529 instead of cash can be gradually contributed to the beneficiary's Roth IRA if they have earned income (subject to annual IRA contribution limits). While many people only put in the gift tax amount each year ($19,000 in 2026, but indexed to inflation), there really is no limit since you, your spouse, and anyone else can all open accounts for the same beneficiary and can do it in all 50 states. You can also front-load a 529 with five years' worth of contributions. The owner of the account can be the parent or the child, and that can be changed at any time.

530A (Trump) Accounts

530A “baby bonus accounts,” new in 2026, are best thought of as a way to pre-pay your child's retirement. While any child born between 2025-2028 can get a free $1,000 from the federal government, the real benefit here is the $5,000 (and indexed to inflation) annual contribution that can be made by parents, an employer, or other entities. The money must be invested in a low-cost index fund, and it can't be touched prior to age 18. At that point, it becomes a traditional IRA owned by the child, and it is eligible for conversion to a Roth IRA.

Just as soon as the child is financially independent (tax-wise) of the parent (<50% of support), the account should be converted to a Roth IRA while the child is still in a low tax bracket. I calculate that done perfectly, this could result in your child having $20 million (nominal dollars) in their retirement account by age 65, all for the price of just $90,000 in today's dollars. This is a dramatically better way to save for their retirement than an annuity (discussed below) because fees are lower and withdrawals are all tax-free. It is also dramatically better than their own Roth IRA because a Roth IRA requires earned income to contribute, but a 530A does not. You can, of course, also do a Roth IRA for their teenage earnings.

More information here:- Trump Will Allow You to Make Dangerous Moves in Your 401(k), Including Adding Crypto

- How the ‘One Big Beautiful Bill’ Act Will Affect Doctors

Roth IRA

Roth IRAs are great. Most, if not all, of what a kid can earn prior to age 18 can be contributed, and you can give them a “parent match” of the same amount of money as a gift to spend. It's a great way for them to get started saving for retirement and build good habits. Unless, of course, you already paid for their retirement with a 530A. It's possible to withdraw Roth IRA money early without paying tax or penalties, but it's generally best to leave this money for retirement (post age 59 1/2) if possible.

Health Savings Account

The only “triple tax-free” account, a Health Savings Account (HSA) is designed for healthcare expenses, either now or later. Getting money into this account for your child requires some trickery. If they are still covered by your family's High Deductible Health Plan (HDHP) but are no longer your financial dependent tax-wise, you (they, but you can gift them the money) can make a family-size contribution ($8,750 in 2026 but indexed to inflation) to their own HSA in addition to the one you made to your HSA.

Like any HSA, that money can be invested, and if they're healthy, it will likely have grown into a six-figure amount before they really start spending any of it. You could potentially make these contributions each year from age 19 to age 26.

Uniform Transfer to Minors Account (UTMA)

Originally, the Uniform Gift to Minors Account (UGMA) but now transitioned to the almost equivalent Uniform Transfer to Minors Account (UTMA) in most states, this is a taxable account for your child. That comes with all the downsides of a taxable account (taxed as it grows, freely available to creditors), but it also has the upsides (immense flexibility). In most states, this account becomes the child's at age 21, to do with whatever they want. That might include “good” things like missions, weddings, honeymoons, cars, educations, summers in Europe, and house down payments, but it might also include “bad” things like getting high and sitting in an apartment playing video games instead of getting a job.

Like any taxable account, if invested tax-efficiently, earnings are generally only subject to Qualified Dividend (QD) and Long-Term Capital Gains (LTCG) rates, which can be 0% for most young people in their 20s (and even many people after their 20s). The two benefits of a UTMA over just maintaining control of the money in your own taxable account are that 1) some of the income from the account is only taxed at your child's tax rates (all of it with a typical five-figure account invested tax-efficiently) and 2) the money is now outside of your estate, providing protection from your creditors while minimizing potential estate and inheritance taxes.

More information here:Annuity

You can buy your child a low-cost annuity and invest it aggressively to pay for their retirement. Prior to 2026 and the institution of 530A accounts, this might have been the best way to provide a retirement account to your child. Unlike a Roth IRA, there are no contribution limits, and there is no earned income requirement. The tax treatment, while substantial over decades, is not nearly as good as a Roth IRA or a 530A account that can become a Roth IRA. It might also provide asset protection from your child's creditors (and of course your own), depending on the state. Penalties for withdrawals before age 59 1/2 do apply.

Your Taxable Account

Not quite ready to give money to your child yet? Maybe you're worried you might need it yourself. Maybe you're worried your child will blow it on a lifestyle with which you don't agree. But if you just invest the money tax-efficiently in your own very flexible taxable account, you can always give it to them later. Gift tax rules apply to large gifts, of course, but since most people won't ever have an estate tax problem, that just means filling out IRS Form 709, a gift tax return, which isn't that big a deal. If your child is in the 0% LTCG bracket, that gift might be completely income tax-free.

Your Retirement Accounts

If you're absolutely sure you don't want them to have the money prior to your death, just stick it in your own retirement accounts. Then, you can use it if needed, it will grow faster than in a taxable account, and it will be protected from your and their creditors. The downside, of course, is that you probably won't die until your 80s, and that means they won't get the money until they're 50 or 60; by then, they may not even need that money. They can stretch the tax benefits of that retirement account for another 10 years, though. Be aware that you can't give a retirement account to someone else. You can pull the money out of the account, pay any taxes and penalties due, and give it away, but it will never be a tax-protected account to them unless you die and they inherit it.

ABLE Accounts

If your child is disabled, creating a small Achieving a Better Life (ABLE) account for them is a good idea. Others can also create an ABLE account for them. Most WCIers will also want to create a Special Needs Trust, but ABLE accounts work great for amounts under $100,000. If it gets larger than that, they start losing government benefits like disability payments and Medicaid until it is spent down. A 529 can be converted to an ABLE account as well. Think of an ABLE account as a 529 for a disabled person's regular living expenses.

Which Account Should I Choose?

This is not an either/or exercise. You can choose to use all of these accounts, none of them, or any combination in between. The three primary questions you'll need to answer to make the right decision are:

- What is the purpose of this money?

- How much do I want to contribute each year and in total?

- How much control do I want to have over the money after giving it?

Once you know those answers, use the chart above to help you decide what combination of accounts to use for your savings designated to help your children. In our case, we've chosen to use 529s, Roth IRAs, UTMAs, HSAs, and our own taxable and retirement accounts. Now, for our younger two children, we'll also utilize 530As. But we have a lot less in 529s than many WCIers since our kids attend or are interested in attending inexpensive colleges. Some WCIers have more in 529s than we have in all of the accounts set up for our children.

More information here:Isn't This Economic Outpatient Care?

Much harder questions to answer are how much money you should give to your child and when. Some people fear, correctly, that their child will make different life decisions if they receive too much money too early in their life. That's almost surely true, but some of those decisions will not necessarily be bad ones. I mean, I donated plasma for grocery money as a college student, and I didn't want my children to have to do that. But I also worked hard at jobs in high school and college, and I'm sure I learned some good lessons doing so. We had to learn to live frugally, and we saved a lot in our 20s and 30s, both of which are useful habits to pick up early in life.

Stanley and Danko discussed this issue in The Millionaire Next Door, a personal finance classic published in the 1990s, in a chapter called Economic Outpatient Care. They argued that adult children who are given money tend to accumulate much less money than they otherwise would. On the other hand, Bill Perkins, in his newer classic Die With Zero, argues that an inheritance is most useful when received between ages 25-35, that most people die as wealthy as they've ever been, and that we can turn money into happiness far more effectively earlier in life than later.

You'll have to walk a balance between these two warring concepts. It helps to know your children well and give them smaller “test amounts” first, while also providing just as much financial literacy education as you can. You also want to make sure you're not impoverishing yourself just to help them. You can best help others from a position of strength. You need to make sure you pay off your own student loans and that you are saving for your own retirement adequately before designating additional savings for your children. They might appreciate you paying for their dental school, but they won't appreciate it so much when you run out of money and you move in with them while they're trying to raise their own kids.

In many ways, the world has changed. Housing is dramatically more expensive than a decade ago, and higher education hasn't gotten any cheaper. The longer that money has to compound, the cheaper it is to pay for a retirement. Relatively small amounts of money now can give your child huge financial advantages in life over their peers. As always, the rich get richer, and passing along both wealth and the wisdom to use it well is one way we can show love to those we care about. If you're worried you'll turn them into selfish little brats, consider also making them the successor advisor for your Donor Advised Fund (DAF) or putting them on the board of directors for your charitable foundation.

When giving money to your kids, take advantage of the tax benefits of the various accounts you can use for that gift.

What do you think? Which of the above accounts will (did) you use? How much are you giving to your kids and why? When and how will you give it?