Trump accounts, aka 530A accounts or 530As, were created as part of the One Big Beautiful Bill Act (OBBBA) passed in July 2025. Accordingly, I cranked out a post we published just a few days later about these revolutionary new investing accounts. The problem was that, back then, nobody really knew exactly how these 530A accounts were going to work.

We still don't know everything. Over the last year, the government has figured out more of the details about these accounts, and since we can actually start using them on July 4, 2026, it's time to really start learning and discussing these accounts on this blog. As you dive into the details, you will discover that I was right when I originally wrote that these accounts would be great for two groups of people: the very poor and the very wealthy.

What Is a Trump (530A) Account?

A 530A is, first and foremost, a “baby bonus” account. These types of accounts have had bipartisan support for many years, but this is the first one actually passed into law. If you have a child born between 2025-2028, the US government will give you $1,000 to be placed into a 530A. I guess this encourages people to have kids (although I assure you they will cost far more than $1,000 by the time all is said and done) and helps to support parents and families.

Seems great, right? No wonder it has bipartisan support. This is what I mean when I say these accounts are great for the very poor. One thousand dollars might not seem like much, but it is $1,000 more than this kid is otherwise going to have. In fact, it's likely to be far more than $1,000 by the time the kid gets it. You see, a key provision of a 530A is that the child (who, like with a UTMA, is both owner and beneficiary) cannot withdraw the money until age 18—$1,000 invested at 10% for 18 years grows to $5,560.

But wait, there's more.

Who Can Contribute to a Trump Account?

The government will contribute $1,000 to a 530A for a child born between 2025-2028 (who are we trying to kid, though; this one is going to be popular enough that it will surely be extended by Congress in the future).

Parents, guardians, relatives, and friends can also contribute to a child's 530A. The total annual contribution is $5,000 (not counting the government contribution), which will start being indexed to inflation in 2028. Employers can also contribute to 530As, up to $2,500 per year per employee (not per employee child) that counts toward the $5,000 limit.

Nonprofits can also contribute to 530As, and their contributions do not count toward the $5,000 limit. But don't think you can start a nonprofit just to put more money into your kid's 530A. They can only contribute equally to one of the following classes of people:

- All account beneficiaries under the age of 18

- All account beneficiaries under the age of 18 who reside in one or more qualified geographic areas (such as a US state)

- All account beneficiaries under the age of 18 who were born in a specific calendar year

- How to Save for Your Children (UTMA vs. Trump Account)

- With Our Expanding Family, We’ve Had to Break Our Financial Plan – Twice

- My Children’s Inheritance

How WCIers Should Use 530A Accounts

None of that explains why WCIers have been so excited about 530A accounts that they have been emailing me every week about them for the last year. The reason they were so excited has to do with what happens to 530A accounts when the child turns 18. At 18, the account is no longer a 530A but a traditional IRA. That means all the IRA rules apply, and all the IRA options exist. The most significant option? Roth conversions. Imagine a parent funds a 530A with $5,000 per year from age 0 to age 17, and that money grows at 10% per year. How much is that worth when they turn 18?

=FV(10%,18,-5000) = $228,000

That's pretty cool, but since it's an IRA, it's designed for retirement. There is a 10% penalty on withdrawals prior to age 59 1/2. What happens if you let this account continue to ride until age 65?

=FV(10%,47,0,-228000) = $20.1 million

You've just funded a very luxurious retirement for your child. Even if the account only earns 5% real over those 65 years, it still adds up to $1.4 million in today's dollars, far more than most people have when they retire. And it only costs you $5,000 * 18 = $90,000.

But what about those Roth conversions? Well, 18-year-olds don't tend to be in high tax brackets. Maybe your kid is in college from 18-22 with no other significant earnings. Imagine they do a $60,000 Roth conversion every year. How much would that cost in taxes? After the $16,000ish standard deduction, $12,000ish would be converted at 10% and the rest at 12%. That means a tax bill of something like $5,000 on a $60,000 Roth conversion. With inflation of the tax brackets over the years, the bill might be even lower.

And it turns out that a lot of that 530A money will be non-taxable basis, too (see “Complications” section below). At any rate, for another $10,000 ($100,000 total) or so, you can give your kid $20 million+ in TAX-FREE money to retire on in 65 years. Pretty nice gift. Now you see why all these optimizing WCIers are so excited about this account. Even if the baby bonus thing goes away after 2028, the rich folks still get to set their kids up for life with a mere $100,000 thanks to the miracle of compound interest. And this doesn't even keep them from funding Roth IRAs equal to their teenage earnings. Despite the fact that a 530A becomes a traditional IRA, the contribution limits are completely separate.

Families like mine, of course, have a bit of a dilemma. As I write this, we have kids who will turn 22, 19, 17, and 11 this year. Do we really want to do something for the younger ones that we didn't (and couldn't) do for the older ones? Well, I have always told them that life isn't fair, and this is another great example of why it sucks to be the oldest child.

How Are 530A Accounts Invested?

One of my favorite parts about 530A accounts is that they have to be invested in low-cost (<10 basis points) US stock index funds. Where was that rule when so many other accounts were designed?

Who Can Open the Account?

It depends. The child can't. Usually, it'll be the parent, but it doesn't have to be the parent. In fact, if not claiming the baby bonus money (officially called the pilot program), any of the following people can open the single account that the child is allowed to have:

- Legal guardian

- Parent

- Adult sibling, or

- Grandparent of the child, in that order of priority.

But if you're claiming the baby bonus money, it has to be the person who can claim that child as their “qualifying child” on their tax return. Note that to get the baby bonus money, the child must be a US citizen with a Social Security number.

Where Will the Government Open My Trump Account?

This part is still a little unclear to me, but it appears that the government itself will open and manage these accounts at trumpaccounts.gov. However, Trump account rollovers are allowed, so presumably most people in the know will subsequently roll their 530As over to someplace like Vanguard, Fidelity, or Schwab, all of which say you can open accounts on their sites by July 4, 2026.

At the time of this writing, there is no information available on the Vanguard or Fidelity websites explaining how to open a Trump Account there, and there is no way on Form 4547 to designate the baby bonus funding to go anywhere but the government site. Perhaps in a few months, I'll add a section to this post right here with screenshots of me opening a 530A at Vanguard for my two youngest.

More information here:- How Trump’s $100,000 H-1B Visa Fee Will Affect Doctors

- Trump Will Allow You to Make Dangerous Moves in Your 401(k), Including Adding Crypto

Complications

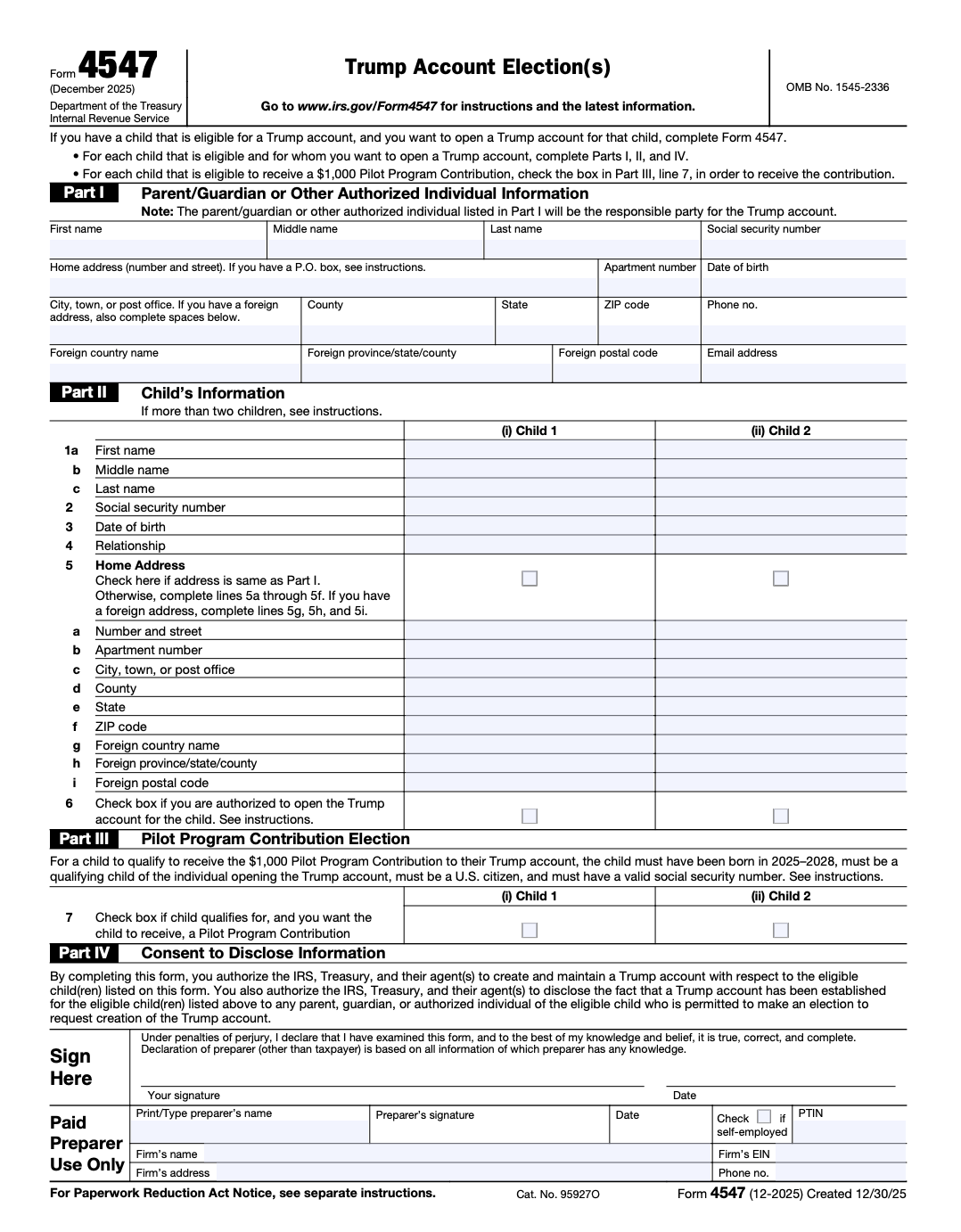

A few complications exist that you need to know about. The first is that if you have had a kid born in 2025 or you anticipate one born in 2026, you can get the government's $1,000 in the summer of 2026, but only if you file IRS Form 4547. Which must be filed with your 2025 tax return. Which you've probably already filed. You can still go back and file the form. Even if you may need to include a 1040X with it, which isn't entirely clear, that's really not a big deal. Otherwise, you have to wait until next year to get your $1,000.

The form isn't terrible. It's only one page.

Even the instructions are only five pages long. And you only have to file this form once per kid. Be sure to check the box in Part III to get that $1,000 baby bonus money if you qualify for it, but you may have to fill out this form to open a 530A, whether or not your kid will qualify for the baby bonus money. I'm not really sure. Ask me in July after I open one for my kids. It wouldn't surprise me if there were an easy way provided to file this form AFTER you file your taxes (since it won't affect anyone's tax bill). If there is, you can learn about it at trumpaccounts.gov, and we'll try to update this post to include that information.

The next complication to consider is gift taxes. Under current law (which I expect to change eventually), a contribution to a 530A is apparently not yet a completed gift. That's nice in one way, I suppose. In 2026, you could put $19,000 into a 529, your spouse could put $19,000 into a UTMA, and the two of you could still put $5,000 into a 530A. But it's bad in another way, because, at some point, the 530A contributions WILL become a completed gift.

The American College of Trust and Estate Counsel outlines the problem well:

“The Act “To provide for reconciliation pursuant to title II of H. Con. Res. 14.” (the “Act”), 3 was enacted on July 4, 2025. The Act provides for the creation of ‘Trump accounts' to encourage saving for a child’s future. The provisions relating to Trump accounts are in section4 530A. Section 530A is silent regarding the gift and generation-skipping transfer (“GST”) tax treatment of a contribution to a Trump account. B. Problem Absent an exclusion, a gift tax is imposed on the transfer of property by gift. Section 2501(a)(1). Exclusions from such treatment are described in section 2503. In particular, section 2503(b) describes the annual exclusion, which is $10,000 per donor per donee as adjusted for inflation. For gifts made in 2026, the annual exclusion is $19,000 per donor per donee. 5 The annual exclusion only applies to gifts that are gifts of “a present interest in property.” Section 2503(b)(1).

Absent an exclusion, a GST tax is imposed on the transfer of property to a skip person (generally a person assigned two or more generations below the transferor). Sections 2601 and 2612(c). Section 2642(c) describes the GST annual exclusion, which is $10,000 per donor per donee as adjusted for inflation. For gifts made in 2026, the GST annual exclusion is $19,000 per donor per donee. The GST annual exclusion applies only to gifts that are nontaxable gifts, which means that the transfer is not treated as a taxable gift by section 2503(b) or section 2503(e). When Congress created qualified tuition program accounts (“529 accounts”) to provide a savings mechanism for education, the authorizing statute included section 529(c)(2) describing the gift tax consequences of a gift to a 529 account. Section 529(c)(2)(A)(i) provides that for purposes of chapters 12 and 13 (the gift tax and the GST tax, respectively) a contribution to a 529 account on behalf of a designated beneficiary ‘shall be treated as a completed gift to such beneficiary which is not a future interest in property.' This language qualifies contributions to a 529 account for the annual exclusion from gift tax and the GST annual exclusion.

The legislation enacting Trump accounts does not include similar language. We believe that this was an oversight. In the absence of specific language qualifying contributions to Trump accounts for the annual exclusion for gift tax and GST tax, such contributions would not so qualify because they are not gifts of a present interest in property. As a result, any contribution to a Trump account will require the donor to file a federal gift tax return reporting the contribution and requiring the donor to either use a portion of his or her lifetime exemption to cover the contribution or (if the donor has no remaining lifetime exemption) pay gift tax. If the beneficiary was a skip person, the donor would also be required to use a portion of the donor’s lifetime GST exemption or (if the donor has no remaining lifetime GST exemption) to pay GST tax.”

The bottom line is that unless something changes soon, anyone using these 530As is going to have to file a bunch of gift tax returns (Form 709) and burn their estate tax exemption—and it might be on the huge amount at age 18 rather than the small amount that goes in each year. I think Congress will fix this issue, and I suspect it'll be done before the end of the year. But keep an eye on it. Form 709 is way more painful to fill out than Form 4547.

Another potential complication is the fact that individual 530A contributions are after-tax money. You won't get a tax deduction when you put that $5,000 into your kid's 530A every year. Contributions from employers, the government, and nonprofits, however, ARE pre-tax dollars. My point is that someone is going to have to keep track of how much of the account is basis. How that will be tracked is not clear, but in the worst-case scenario, you will need to keep track of it yourself. Hopefully, the account provider (Vanguard, Fidelity, Schwab, etc.) will track it, or it will at least be tracked somewhere on your tax return each year, like it is with IRAs using Form 8606.

Inherited 530A accounts are a bit like HSAs. That is to say, they don't exist after you die. So, try not to die before you turn 18. After 18, it's an IRA. It becomes an inherited IRA, and it can be stretched by heirs.

All together, when you look at all these complications, it seems like a pretty good year to file an extension on your taxes if you don't typically do so. Let this all shake out this summer, and then file your taxes with your 4547.

Should I Use a Trump Account or a UTMA (or a 529)?

The most common question received after this blog post was published was from people wondering which account they should use. So I did an entire additional blog post on the topic. It won't be “hard-published” (sent out as an email and promoted widely) for a while, but it can be read here.

Update: July 2026

Trump accounts are now active and can be funded. I have started one for each of my two minor children (“How to” post with screenshots has been written and will be published soon.) The IRS issued some rules and regulations about them, summarized here. As expected, contributions made to 530As usually won't require one to file a gift tax return as some were worried it would. The Bottom Line

WCIers who are already maxing out their other tax-protected accounts and using accounts like 529s and UTMAs are probably going to want to open a 530A for each of their kids as well. Get Form 4547 filed this year, and get that compound interest going ASAP.

What do you think? Are you starting Trump accounts? Why or why not?