While it is entirely possible to finish an undergraduate education debt-free, that is becoming less and less likely for physicians, dentists, attorneys, and other high-income professionals all the time. This lengthy post is going to cover everything you need to know about managing those pesky student loans—from student loan forgiveness programs to the best deals on student loan refinancing and the need for future medical students to apply for private loans as well. Consider this Student Loans 101. We've divided the post by level of training, which will hopefully allow you to skip to those parts that apply to you. May this post bring some hope to those struggling under the burden of medical school debt.

Table of Contents

Student Loan Management During Undergraduate School

Student Loan Management During Medical School

Student Loan Management During Residency

What Happens to Loans in Bad Situations

Should I Really Pay Off My Loans Quickly?

Student Loans 101

What Is a Student Loan, and What Can Student Loans Be Used For?

Student loans are loans issued to students to pay for their education and associated living expenses. As such, it is considered fraudulent to obtain or use them for any other purpose. Unlike a mortgage or auto loan, these loans cannot be foreclosed on. Nobody is coming to do a craniotomy if you don't pay. However, in exchange for that fact, they have two conditions that make them rather onerous:

- They are offered at rates significantly higher than mortgage rates, especially for graduate/professional school (5%-10%)

- They are generally only discharged in the event of death or total disability, NOT bankruptcy (only discharged in extremely rare cases)

How Much Student Loans Should I Borrow?

Don’t borrow more money than you need for school. Some financial aid offices will recommend taking out additional loans to cover living expenses. Try to take out the least amount necessary to cover your living expenses. Some may even borrow more than they need to live a lavish lifestyle on their loans. This is never a good idea. To learn more about how to live with student loans, check out The Right Way to Use Debt in Medical School.

Recommended Student Loan Advisors

The decisions you make with your student loans can easily be worth tens or even hundreds of thousands of dollars. Managing them, however, is getting more and more complicated each year with rapidly changing federal repayment programs. I recommend you use this post as a learning tool and guide, but visit with White Coat Planning and its student loan advisors to make a plan for your unique situation. They know these programs inside and out and are up to date with the latest information to save you the most amount of money.

How to Get a Student Loan

Apply for a federal student loan by completing the Free Application for Federal Student Aid (FAFSA) form. Your results will dictate your financial aid offer.

Before receiving student loans, you’re required to receive entrance counseling to ensure you understand the obligations of loan repayment and sign a master promissory note, which is a binding contract in which you agree to the loan terms. Contact your school’s financial aid office for additional details.

The Need for Private Student Loans

The world of paying for medical school had a significant change with the passage of the One Big Beautiful Big Act (OBBBA) in the summer of 2025. New medical students for the 2026-2027 year are limited to borrowing just $50,000 in federal student loans per year ($200,000 for a four-year medical school). This cap on federal borrowing has created a “funding gap” which will obviously vary by school and student. But a significant portion of new MS1s are going to need private loans going forward, which hasn't happened for a couple of decades since federal borrowing limits went away in 2006.

The process for applying for a private student loan can vary, but most private lending applications are accessible through their websites.

How Do Student Loans Affect Credit Score?

Both federal and private student loans are generally treated the same as any other installment loan, such as a mortgage or car loan. If you make each payment on time, it can build your credit history and may even boost your credit score. If you are delinquent on payments or you default on your student loans, then your credit score can take a hit. Before you are ever close to delinquency or default, make sure you are enrolled in an appropriate Income Driven Repayment (IDR) plan to assure the affordability of payments.

Doctors with large student loans looking to buy a house may find it difficult to secure a mortgage due to their high debt-to-income ratio. An option to consider is using a physician mortgage loan (also known as a doctor mortgage). Physician mortgage loans are lending programs that give special treatment to high-income borrowers with a high student loan debt-to-income ratio. Physician mortgages are also often available to dentists, veterinarians, CRNAs, PAs, attorneys, etc.

Types of Student Loans

Student loans are divided into two main types—federal loans (also called direct loans) and private loans.

Federal vs. Private Student Loans

When deciding on how to borrow for your education, take out federal before private. Federal loans can offer lower interest rates initially, and they have an abundance of federal protections that private student loans don’t offer. Private loans don’t offer Income Driven Repayment, Public Service Loan Forgiveness, or IDR Forgiveness. Unlike federal student loans, which are always discharged upon death or total disability, private student loan discharge policies are less standardized and vary by lender.

Federal Student Loans

Federal loans generally have lower rates and also have special income-based payment plans and forgiveness plans. The general rule is to max out what you can borrow in the federal loan programs before taking on any private loans.

However, some foreign medical schools qualify for federal loans, and some do not. Be sure to consult the list on this page before applying and enrolling in a foreign medical school. Caribbean medical schools are notorious for not qualifying for federal loans, although the ones with the highest match rates (St. George's, Saba, American University of the Caribbean, Ross) do tend to qualify.

Federal student loans can be consolidated. In this process, numerous loans are all lumped together into one loan, and the interest rates are averaged and then rounded up to the nearest 1/8 of a point. This is distinct from the process of refinancing (available only with private lenders), where the interest rate is generally lowered.

Federal Student Loan Eligibility

Eligibility requirements include:

- Demonstrating financial need

- US citizen or eligible non-citizen

- Have a Social Security number

- Be enrolled in school part-time or more

- Be enrolled in a Direct Loan program

Subsidized vs. Unsubsidized Federal Student Loans

Subsidized loans are loans that the Education Department will pay the interest on for you for undergraduate schooling. Borrowers who qualify will demonstrate a financial need and will not have to pay accrued interest while in school. Graduate and professional degree programs no longer offer subsidized loans. Unsubsidized loans begin accruing interest the moment you receive them. PLUS Loans (Grad or Parent) are unsubsidized loans. You'll want to exhaust any subsidized options before ever taking out an unsubsidized loan.

Types of Federal Student Loans

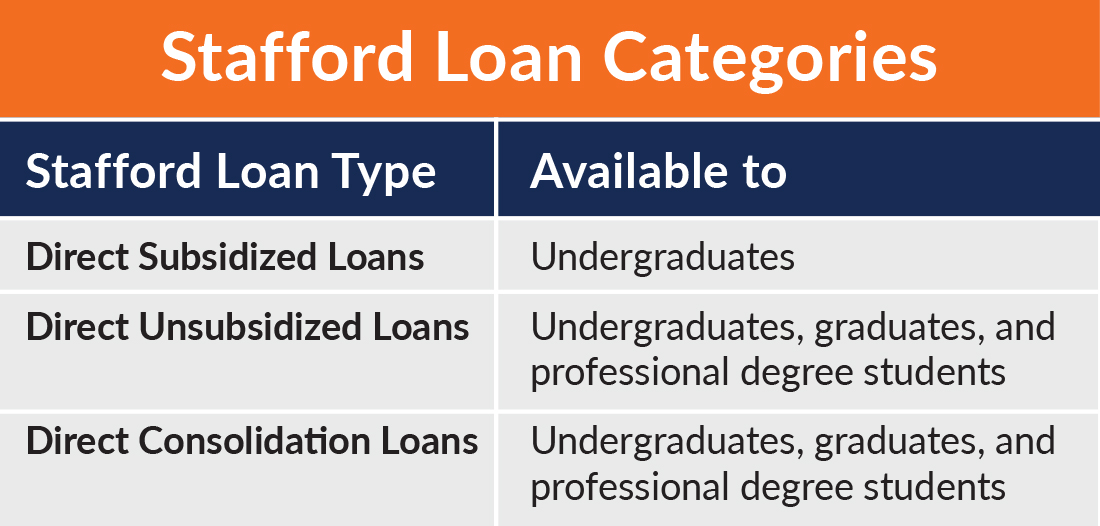

#1 Stafford Loans

Stafford Loans are also known as Direct Stafford Loans, and they come from the William D. Ford Federal Direct Loan (Direct Loan) Program. Direct Stafford Loans are the most common student loans and are currently being issued to help cover the cost of higher education.

There are three categories of Stafford Loans:

- Direct Subsidized: Available to undergraduates

- Direct Unsubsidized: Available to undergraduates, graduates, and professional degree students.

- Direct Consolidation: Available to undergraduates, graduates, and professional degree students.

Prior to consolidation, Stafford Loans are eligible for:

- Standard Repayment Plan

- Graduated Repayment Plan

- Extended Repayment Plan

- Income Driven Repayment Plans

- Public Service Loan Forgiveness (PSLF)

- Income Driven Repayment Forgiveness

#2 PLUS Loans

PLUS Loans, aka Grad PLUS Loans, come from the Direct and FFEL Loan programs. Borrowers are issued these loans after exhausting Stafford Loans to cover tuition. Grad PLUS loans were discontinued for those who started borrowing for the program after June 30, 2026.

Prior to consolidation, Direct PLUS Loans are eligible for:

- Standard Repayment Plan

- Graduated Repayment Plan

- Extended Repayment Plan

- Income Driven Repayment Plans

- Public Service Loan Forgiveness (PSLF)

- Income Driven Repayment Forgiveness

Prior to consolidation, FFEL PLUS Loans are eligible for:

- Standard Repayment Plan

- Graduated Repayment Plan

- Extended Repayment Plan

- Income Based Repayment

- Income Driven Repayment Forgiveness via Income Based Repayment

After consolidation, FFEL PLUS Loans are eligible for:

- The remaining Income Driven Repayment Plans: RAP, ICR (and PAYE if borrowed after Oct 1, 2007, and have a federal loan disbursed on or after Oct 1, 2011)

- PSLF

- Income Driven Repayment Forgiveness via RAP, ICR, PAYE

#3 Parent PLUS Loans

Parent PLUS Loans are issued to parents to finance their child’s education. They are offered for undergraduates, graduates, and professional degree students. Previously, there was no limit on borrowing for Parent PLUS loans. However, the One Big Beautiful Bill Act (OBBBA) implemented a borrowing cap of $65,000 per child, with up to $20,000 per year.

Prior to consolidation, Parent PLUS Loans are only eligible for:

- Standard Repayment Plan

- Graduated Repayment Plan

- Extended Repayment Plan

After consolidation, Parent PLUS Loans are eligible for:

- Income Contingent Repayment

- Income Driven Repayment Forgiveness via Income Contingent Repayment

Note that per OBBBA, Parent PLUS loans had to be consolidated prior to July 1, 2026, to remain eligible for IDR programs. Loans consolidated or borrowed after that date are not eligible for any IDR plans. The Income Contingent Repayment (ICR) plan has historically been the only IDR plan available to parent borrowers. In the past, borrowers often had to navigate the complex and cumbersome double-consolidation process to access more generous IDR plans. Now, so long as the Parent PLUS loans have been consolidated before July 1, 2026, they would become eligible for the more generous Income Based Repayment plan, after they have made one payment in the ICR plan. The double consolidation loophole is no longer a factor for parent borrowers.

#4 Family Federal Education Loans (FFEL)

Before 2010, the Family Federal Education Loans (FFEL) program was the main source of federal student loans. The program ended in 2010, and all loans are now issued under the Direct Loan program referred to above.

Prior to consolidation, FFEL Loans are eligible for:

- Standard Repayment Plan

- Graduated Repayment Plan

- Extended Repayment Plan

- Income Based Repayment (not to be confused with Income Driven Repayment)

- Income Driven Repayment Forgiveness via Income Based Repayment

After consolidation, FFEL Loans are eligible for:

- The remaining Income Driven Repayment Plans

- RAP, ICR (and PAYE if borrowed after Oct 1, 2007, and have a federal loan disbursed on or after Oct 1, 2011)

- PSLF

- Income Driven Repayment Forgiveness via RAP, ICR, PAYE

#5 Perkins Loans

The Federal Perkins Student Loan program was created to provide money for college to students with a particular financial need. The program ended on September 30, 2017.

Perkins Loans are not eligible for a number of federal programs, like IDR or PSLF, until they are consolidated.

After consolidation, Perkins Loans are eligible for:

- Standard Repayment Plan

- Graduated Repayment Plan

- Extended Repayment Plan

- All Income Driven Repayment Plans (and PAYE if borrowed after Oct 1, 2007, and have a federal loan disbursed on or after Oct 1, 2011)

- PSLF

- Income Driven Repayment Forgiveness

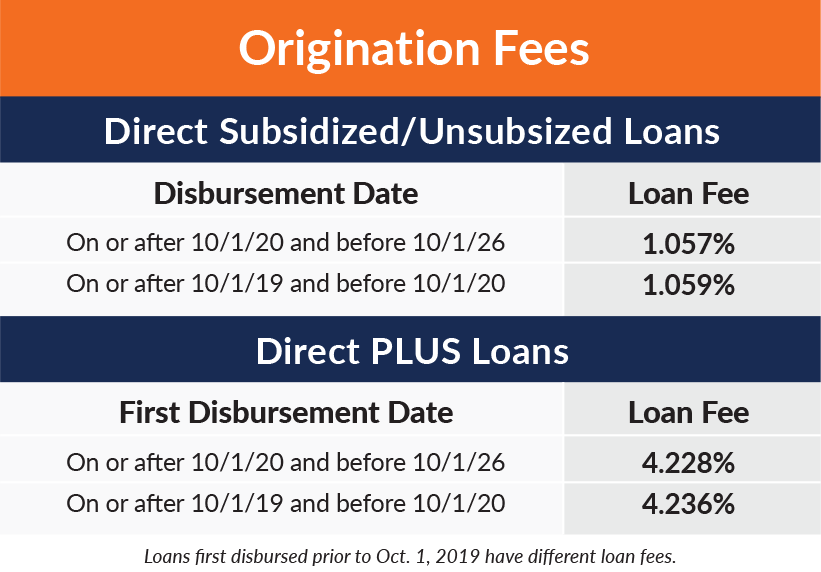

What Is a Federal Student Loan Origination Fee?

Most federal student loans hit you with loan fees when disbursed. The fee is deducted proportionately from each loan disbursement you receive while enrolled in school. Which means the money you receive will be less than the actual amount you borrow. AND you’re responsible for repaying the entire amount you borrowed, not just the amount you received.

Private Student Loans

In the past, private student loans were generally used only after a borrower reached the maximum federal loan limits, with Grad PLUS loans filling most remaining funding needs. For students beginning borrowing in fall 2026 and beyond, Grad PLUS loans will no longer be an option, meaning private loans are likely to be used much earlier in the borrowing process. An exception remains for students attending certain international medical schools that are NOT eligible for federal loans at all, where private loans may be the only option.

Eligibility Requirements for Private Student Loans

- Underwriters will look at credit score, debt-to-income ratios, income, and employment history to determine creditworthiness.

- Typically, borrowers (and cosigners) need to be US citizens or permanent residents.

- Borrowers must meet minimum legal age requirements which vary by state.

Private Student Loan Cosigner Requirements

Cosigners are not required when taking out private student loans, but they can help borrowers secure a loan and obtain better terms. Some criteria for co-signers include:

- Good credit history. A number of private refinancing companies require a minimum credit score of 680-720. The better their credit score, the better the rate.

- Co-signer relationship to borrower. Parents, spouses, or other family members are generally cosigning on student loans. However, ANYONE with a good credit history can act as your cosigner. However, co-signers need to know that by signing their name on the dotted line, they are legally responsible for loan payments. They run the risk of ruining their credit if the borrower fails to make payments or if they default. Ruined relationships are also a risk that cosigners and borrowers run with these loans.

- Good health. Some private refinancers require loans to be paid immediately if a cosigner passes away.

- Stability. This encompasses a number of things we’ve addressed above, but consider credit, income, job history, savings, debt, etc.

We've been working with lenders for years, mostly to help doctors refinance their student loans. These same lending partners giving docs the best deals on refinanced student loans are also now doing private student loans. Yes, they make money when you borrow from them. Yes, we make money when we refer you to them. But if it's the best deal for you, it's the best deal for you, and as near as we can tell, it is.

We have several partners right now offering private student loans. Some of them offer you cash back when you go through our links. We will throw in the student version of our flagship Fire Your Financial Advisor online course for all of them. Either way, it's a better deal than you will get by going directly to the lenders, and you get to support WCI at the same time.

Spread the word. Here are our lending partners:

† Bonus may include cash rebates and value of free course. Student loan borrowers who use the WCI links will be enrolled in The White Coat Investor’s flagship course, Fire Your Financial Advisor: STUDENT for free ($99 value). Borrowers may still receive the amazing cash rebates that WCI has negotiated with lenders. Offer valid for loan applications submitted from May 1, 2026 through October 31, 2026. Free course must be claimed within 90 days of first loan disbursement. To claim free course enrollment, visit https://www.whitecoatinvestor.com/loanbonus.

We recommend you check with two or three of these companies and go with the one offering you the lowest interest rate and best terms. And don't forget to max out the federal student loans FIRST before taking out private loans.

Student Loan Management During Undergraduate School

Let's start at the very beginning. How much should you take out in student loans? The truth is that you don't have to borrow for undergraduate school, and we think that very few should. There is a very wide range in the cost of attendance of undergraduate institutions, far wider than the range in the actual quality of the education. By making a few smart decisions and working hard as an undergraduate, most of those who will eventually become doctors can avoid having any undergraduate debt at all. Steps you can and should take to finish your bachelor's degree debt-free include:

- Choose a school you (or your family) can afford to attend without borrowing. If you will be receiving no help at all from your family, this may mean attending a state university in YOUR state or even spending a couple of years “doing generals” at a community college.

- Go where you can get a meaningful amount of scholarship money. It's rare that those who are academically talented enough to get into medical or dental school aren't talented enough to get some kind of academic scholarship somewhere, often for full-tuition or even a full-ride. Your part-time job as a high school junior or senior is applying for scholarships.

- Live at home. One of the largest expenses of college is your living expenses. These can be cut dramatically by living at home, saving on room, board, and even laundry costs. This might require increased transportation costs, but you'll usually come out way ahead and get better grades anyway.

- Work hard during the summers. Bust your butt working for tips, working overtime, or even working two jobs when you are out of school. It is not unusual at all for an undergraduate student to return to school in the fall with thousands of dollars in their pocket.

- Consider a part-time job during the school year. If you're the type of person who's going to have the ability to handle the academic load in medical school and survive residency, you can handle 16 credit hours of science classes along with a part-time job. Many of your peers in medical school had a job, played on a sports team, AND managed a high GPA and a strong MCAT score. You can do it also, although it might require cutting down on social activities.

If you do end up borrowing for your undergraduate degree, try to only take on subsidized debt. That way, the interest won't be building during medical school and residency. If you will be borrowing for medical school, consider taking out a loan toward the end of your senior year of undergraduate for that purpose. Not only will the interest rate be lower (6.52% instead of 8.07% for the 2026-2027 school year), but the first $5,500 will also be subsidized.

Student Loan Management During Medical School

The best student loan is the one you never take out. Here are a number of techniques for lowering the amount of debt you take on for school.

- Choose the least expensive school you can get into in the least expensive cost-of-living area. It is difficult to live in Washington DC, the Bay Area, and Manhattan with a middle-class wage. Trying to do it on borrowed money is a good way to ruin yourself financially.

- Consider taking out the maximum loan amount possible as a senior undergraduate student to decrease how much you borrow as a first-year medical student. Not only do undergraduate loans carry lower interest rates than graduate school loans, but they are also subsidized.

- For students starting medical or dental school in fall 2026, federal student loan borrowing is capped at $50,000 per year, with Graduate PLUS loans no longer available. Those already enrolled may continue using the older rules that allow borrowing up to the full cost of attendance.

- Apply to New York University, Columbia University, Albert Einstein College of Medicine, and any other schools that may offer free tuition in the future.

- Live frugally. Get roommates. Ride a bike. Minimize meals out, vacations, expensive hobbies, and recreational shopping. Buy used books and equipment.

- Take advantage of any possible family resources. Your parents may be in a position to help with their own savings or current cash flow. If married, your spouse should take a job, preferably with the university, which may reduce your tuition.

- Apply for scholarships like The White Coat Investor Scholarship.

- Consider “contract scholarships” like the Health Professions Scholarship Program, National Health Service Corps, Indian Health Services, or state primary care programs.

- Don't take out your loans until you must. Medical school loans are no longer subsidized, and you begin accruing interest as soon as you take them out. Some students have even taken advantage of 0% credit card offers to further delay the date when they receive their student loans.

- Consider your student loan burden when choosing a specialty. While finances should not be the primary driver of specialty choice, a $600,000 student loan burden is not compatible with private practice pediatrics.

- As you near medical school graduation, federally consolidate right after graduation and enroll in an Income Driven Repayment Program ASAP. Many doctors have regretted their decision to put their student loans into forbearance or deferment.

Federal Student Loan Borrowing Caps

Federal student loan borrowing for medical and dental students has undergone major changes since the One Big Beautiful Bill Act was signed into law in July 2025. The federal Grad PLUS program was eliminated for those beginning borrowing after June 30, 2026. For nearly two decades, Grad PLUS loans allowed graduate and professional degree students to borrow up to the full cost of attendance and beyond standard Direct Unsubsidized limits. Now, that option no longer exists for those starting programs in fall 2026 or later. If you started borrowing prior to that date for your program, you will be grandfathered in to the older borrowing rules.

Federal borrowing for graduate and professional education (medical/dental school) will be limited to direct unsubsidized loans. Unsubsidized borrowing is capped at up to $50,000 per year with a $200,000 lifetime limit for medical or dental school. Graduate school will be capped at $20,500 per year with a lifetime limit of $100,000. The lifetime limit for all federal borrowing (undergrad/grad/professional) is $257,500. With the lower federal caps in place, many students will have to look at supplementing the cost of their education from institutional and private student loans.

Student Loan Management During Residency

Upon completion of medical school, it is best to divide student loan management into two categories—private loans and federal loans.

Private Student Loan Management and Repayment

As a general rule, doctors are going to pay back their private student loans, so minimizing the interest that accrues is key. The best way to do this is to refinance those student loans as soon as you get out of medical school. There are a few companies that offer “resident programs” where you can lower your interest rate AND enjoy a lower payment than you would otherwise have to make ($0-$100 per month). While that payment doesn't cover the interest accruing on the loan, you will end up paying less interest overall because you will have lowered the interest rate from 6%-10% to 3%-6%. The following WCI partners offer special resident student loan refinancing programs:

Laurel Road: $100 per month payments

SoFi: $100 per month payments

Splash: $100 per month payments

Private Student Loan Payment Methods

Private student loan lenders typically offer four main ways to repay loans during residency. Remember, although some programs will let you defer payments to varying degrees while still in school, interest will still accrue beginning on the day you or your school receives the funds from the loan.

#1 Immediate Repayment

Payment begins immediately from loan disbursement, even when enrolled in school. This is the lowest cost of the four payment options that allows you to begin paying down both principal and interest from Day 1.

#2 Interest-Only

In this program, you will pay interest only while enrolled in school. Although the loan balance won't be paid down, you will keep up with the interest payments and won't have a larger loan balance at the end of your schooling.

#3 Partial

This option will require you to make a low fixed payment while enrolled in school. You'll have a larger loan balance at the end of residency, but you will make progress toward reducing the overall amount owed.

#4 Full Deferment

If you choose to fully defer, you will not be required to make any payments during school—including a six-month grace period after graduation. This is the most expensive of the four payment options.

Federal Student Loan Management Repayment and Forgiveness Programs

Many federal student loan borrowers enroll in a standard 10-year payment program for loan repayment—paying off your loan in 120 fixed payments over 10 years. These monthly payments, based on loan amount and interest rate, are much higher than what a typical low-income resident with six-figure debt can afford. Income Driven Repayment (IDR) Programs, however, are payment plans that allow borrowers other options to repay their loans based on income and family size.

Income Driven Repayment (IDR) Programs

IDR programs are highly beneficial to residents, who literally cannot afford to make the standard payment on their student loans. With payments based on a percentage of discretionary income, the monthly amount due may be as low as $0, but it is more likely in the $100-$400 range. Once per year, you'll be required to certify income (typically submit a tax return or pay stub) to stay compliant with IDR plans.

In addition, IDR programs are eligible repayment programs for federal loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) and long-term income driven repayment forgiveness.

A major downside of some IDR plans is their inability to cover accrued interest. Given that a $200,000, 6% student loan accrues $1,000 per month in interest, IDR payments typically do not even come close to covering the accruing interest, leaving a loan that will continue to grow in size during residency. Later on, we will introduce the IDR plan called Repayment Assistance Plan (RAP) that does subsidize interest.

IDR programs add an enormous amount of complexity to federal student loan management. It is vital for a borrower to understand the options available to find the most affordable payment with the least amount of accrued interest and the greatest level of forgiveness. The federal government periodically changes IDR plans, most recently through the OBBBA signed into law in July 2025.

Please note that with any of the IDR programs, you’ll want to file a tax return for the last year of medical school, even if you don’t have income. This will allow you to have very low payments (~$0-$10) your first year in any of the IDR plans.

#1 Income Contingent Repayment (ICR)

Income Contingent Repayment or ICR is really more of a legacy program. We've rarely run into doctors enrolled in this program. In ICR, payments are 20% of your discretionary income. The one advantage ICR has over other programs is that it may be used with Parent Plus loans after they have been consolidated. Unless you have parent loans, you will likely find one of the other income-based payment programs (discussed below) offering better payment options than ICR.

This payment program will sunset in the summer of 2028 due to OBBBA. At that time, you'll need to look into another IDR plan. If you are a parent borrower who is only eligible for the ICR plan, you can make one payment in the ICR plan and then immediately switch into the more favorable IBR program.

Eligibility: No partial financial hardship is required, and it doesn’t matter what date your loans were first issued.

Who should consider: Parent borrowers

#2 Income Based Repayment (IBR)

Income Based Repayment (IBR) was a new and improved ICR. The main features are:

- Payments capped at 10% of discretionary income for new borrowers on or after July 1, 2014 (New IBR)

- Payments capped at 15% of discretionary income for loans taken out before July 1, 2014 (Old IBR)

- Payments capped at the standard 10-year repayment plan level, even if your income rises (as it will for many attendings)

- You can use IBR with Federal Family Education Loans (FFEL) (although those may be eligible for PAYE or RAP after consolidation)

- Interest is not capitalized until you leave the program

- If you file taxes Married Filing Separately, you can exclude your spouse’s income from your payment calculation.

Eligibility: Previously, the IBR plan had an income requirement called a Partial Financial Hardship. This rule was phased out with the passing of OBBBA. Borrowers can enroll in IBR at any income or debt. Old IBR applies to borrowers who have at least one outstanding federal student loan before July 1, 2014. New IBR applies to borrowers who either began borrowing federal student loans on or after July 1, 2014, or who have fully repaid all prior federal loans before taking out a new loan on or after that date.

Who should consider: Dual-income borrowers and those going for loan forgiveness. However, if you qualify for Old IBR, you may want to consider the PAYE or RAP plans discussed below to have lower monthly payments.

#3 Pay As You Earn (PAYE)

Pay As You Earn was a new and improved IBR. Main features of PAYE include:

- Payments are 10% of discretionary income.

- Payments are capped at the standard 10-year repayment plan level, even if your income rises as an attending.

- Married folks can file their taxes Married Filing Separately. While this likely increases their tax burden, it may significantly decrease the required payments. That may, in turn, increase the amount of their loans left to be forgiven.

- Interest is not capitalized if you switch to another federal program. Leaving the IBR plan will trigger capitalization.

This payment program will sunset in the summer of 2028 due to OBBBA. At that time, you'll need to look into another IDR plan.

Eligibility: A partial financial hardship is required. So make sure you’re enrolled in PAYE before you become an attending. To qualify for PAYE, you must have taken out your first federal loan after September 30, 2007, and received a loan disbursement after September 30, 2011. FFEL loans are not eligible for PAYE unless they are consolidated through a direct federal consolidation loan.

Who should consider: Dual-income borrowers and those going for loan forgiveness.

#4 Repayment Assistance Plan (RAP)

The Repayment Assistance Plan (RAP) was created by OBBBA in July 2025 and was made available on July 1, 2026. Here are the main features:

- Monthly payments are based on a sliding scale of 1%-10% of a borrower’s Adjusted Gross Income (AGI), rising with higher income brackets. For AGI > $99,999, payments will be 10% of income (common for docs).

- No payment cap like IBR and PAYE.

- Married folks can file their taxes Married Filing Separately to exclude spousal income.

- If a borrower’s required payment does not cover the monthly interest, the remaining interest is waived, and the government also provides up to a $50 monthly credit toward the loan principal.

- It's the only IDR plan available to those who disburse a federal student loan after June 30, 2026.

Eligibility: Any borrower with direct federal student loans.

Who should consider: Borrowers with student debt that exceeds their income and/or those considering loan forgiveness.

Saving on a Valuable Education (SAVE)

The Saving on a Valuable Education (SAVE) program was introduced in the summer of 2023, replacing the old Revised Pay As You Earn (REPAYE) Program. The program ultimately ended in December 2025, following the resolution of a long-standing lawsuit brought by the state of Missouri. That litigation, which began in the summer of 2024, placed approximately 7 million SAVE borrowers into a processing forbearance. Initially, the forbearance paused both payments and interest accrual through August 2025; once interest resumed, many borrowers began evaluating alternative repayment options for their federal student loans. Eventually, all those still in SAVE were forced to select another IDR plan or be automatically moved.

Partial Financial Hardship

Partial Financial Hardship (PFH) is an eligibility requirement under the Pay As You Earn Repayment (PAYE) plan. To qualify, your monthly payment in PAYE must be lower than the standard 10-year repayment plan. If your payment in PAYE is above the standard 10-year payment, you do not qualify for a PFH.

However, if you’ve enrolled in PAYE while you qualified for a PFH, you can continue in the plan even if your income grows and would make you ineligible thereafter. This is very common when income jumps as trainees become attendings.

PFH Example #1 Eligible Borrower

Resident income = $60,000

Student loan debt = $300,000

Interest rate = 7%

Household size = 1

Standard 10-year payment = PMT(7%/12,120,300000,0,0) = $3,483

PAYE monthly payment = $60,000 – $23,940 = $36,060 × 10% = $3,606 / 12 = $301

The payment cap is $3,483 for this borrower. The monthly payment in PAYE is below the standard 10-year payment and is eligible for a Partial Financial Hardship.

PFH Example #2 Ineligible Borrower

Attending income = $450,000

Student loan debt = $300,000

Interest rate = 7%

household size = 1

Standard 10-year payment = PMT(7%/12,120,300000,0,0) = $3,483

PAYE monthly payment = $450,000 – $23,940 = $426,060 × 10% = $42,606 / 12 = $3,551

The monthly payment in PAYE has passed the standard 10-year payment due to the large increase in income as an attending. Since the monthly payments are higher than the standard 10-year payment, this borrower no longer qualifies for a Partial Financial Hardship. They are no longer able to enroll into PAYE.

However, if the borrower enrolled in PAYE as a resident or before their income jumped, they can stay in the program as long as they don’t switch repayment plans.

PFH Example #3 Borrower Breakeven Point

Attending income = $441,900

Student loan debt = $300,000

Interest rate = 7%

household size = 1

Standard 10-year payment = PMT(7%/12,120,300000,0,0) = $3,483

PAYE monthly payment = $441,900 – $23,940 = $417,960 × 10% = $41,796 / 12 = $3,483

The breakpoint is reached when your payment in PAYE equals the standard 10-year payment.

Interest Capitalization

Interest capitalization occurs when unpaid interest is added to the principal amount of your federal student loans. This increases the principal balance on the loan. The interest rate is now charged on that higher principal balance, increasing the overall cost of the loan.

Example #1 Interest Charges Prior to Interest Capitalization

Principal balance = $200,000

Accrued interest = $50,000

Total balance = $250,000

Interest rate = 7%

Annual interest charge = $200K × 7% = $14,000

Example #2 Interest Charges After Capitalization

Principal Balance = $250,000

Accrued Interest = $0

Total Balance = $250,000

Interest Rate = 7%

Annual interest charge = $250,000 × 7% = $17,500

After the accrued interest of $50,000 capitalizes, the annual interest charge will increase by $3,500.

Interest Capitalization Triggers

Interest capitalization can be inevitable, but it should be avoided when possible. Here's when this happens:

- Exiting a grace period (typically six months after graduation)

- A direct federal consolidation

- Refinancing federal loans to private

- Ending certain deferments or forbearances

- When switching out of the IBR plan

- Student loan default

Federal Student Loan Forgiveness Programs

In addition to the more well-known Public Service Loan Forgiveness (PSLF) program, several of the IDR programs have their own forgiveness programs. Remember that none of these federal programs have anything to do with private or refinanced loans.

IBR Loan Forgiveness Program

The IBR forgiveness program requires 20-25 years of payments, but you may make them while working for any employer or not working at all. New IBR is over 20 years, and Old IBR is 25 years. There are two issues with this forgiveness program.

First, most physicians will have paid off their loans completely in less than 20-25 years, because after they finish training, their payments will be equal to those under the standard 10-year repayment program. Perhaps that would not be the case for a very poorly paid physician with a very high student loan burden (3, 4, or 5x their income), but for most, there just won't be anything left to forgive.

Second, the forgiveness is taxable, and after 20-25 years, the “tax bomb” could grow to as much or more than the original debt, at least on a nominal (non-inflation adjusted) basis.

PAYE Loan Forgiveness Program

PAYE offers forgiveness after just 20 years. However, it is still fully taxable at your ordinary income tax rate in the year you receive forgiveness. PAYE is being phased out in the summer of 2028, so if you are hitting forgiveness after that date, you need to look at IBR or RAP as an alternative. And depending on when you started borrowing, you could end up with more years of payments and a higher monthly payment.

RAP Loan Forgiveness Program

RAP has a generous interest subsidy, but it is the longest IDR forgiveness track at 30 years. RAP would likely have a lower loan balance leftover for the tax bomb vs. PAYE and IBR, but it is really only going to work out if you have massive loans as compared to your income. And do you really want to carry your loans around until you reach your 60s?

Long Term IDR Forgiveness Program Tracker

Staying up to date on IDR forgiveness can be tough, especially since the timeline can span decades. Temporarily, there was a tracker on studentaid.gov, but the Department of Education took it down.

Public Service Loan Forgiveness (PSLF)

Public Service Loan Forgiveness is the granddaddy of the federal forgiveness programs and the only one most doctors should be looking at. Not only does it offer tax-free forgiveness, but it also offers it after just 10 years of payments. If you make a bunch of tiny IBR, PAYE, or RAP payments during your training, you may only have to make 3-7 years of “full” payments as an attending before having the rest forgiven.

There is a catch, however. You have to be directly employed full-time by a nonprofit (501(c)(3)) while making all of those payments in an eligible payment program—or they don't count. You also have to make sure you can prove you made all of those payments since the federal student loan servicing companies have a nasty habit of not being able to count payments accurately.

Student Loan Deferment and Forbearance

Many residents are tempted to put their student loans into deferment or forbearance during residency and/or fellowship. This is almost always a mistake. Nothing makes us cry more than to run into a doctor who should only be 2-3 years away from receiving PSLF but who had their loans in forbearance during a lengthy training period. We hate breaking the news to them that they've basically thrown away a benefit worth hundreds of thousands of after-tax dollars. It's like working for a year or two as a doctor without being paid at all. Deferment is slightly better than forbearance for some people, but they are both very similar for most high-income professionals with loans—you make no payments, but the debt continues to grow, sometimes very quickly.

Student Loan Deferment

Deferments are granted in six-month increments by your loan servicer, and subsidized loans don't accrue interest. Unsubsidized loans both accrue and capitalize interest. There are several reasons you can get a deferment, but the main one most residents would use is economic hardship, which is limited to just three years. Other reasons include active-duty military, unemployment, and going back to school.

Student Loan Forbearance

With forbearance, interest accrues on both subsidized and unsubsidized loans. Just think of it as a 12-month pause on payments. For most medical students, it is no less attractive than deferment, and it is easier to get. There are two types of forbearance.

- General Forbearance: This is where the lender gets to decide whether to give it to you. Typical reasons you may get it are financial difficulties, medical expenses, or a job change.

- Mandatory Forbearance: This is where the lender MUST give it to you if you ask for it, include residency training, if your monthly payment is more than 20% of your monthly gross income (only good for three years), if you are serving with Americorps or activated through the National Guard (and ineligible for military deferment), or if you qualify for special teacher or Department of Defense forbearance programs.

We tell you about these two programs and give you these links because people wonder about them, not because we think people should actually use them. If you are seriously considering deferment or forbearance, you would almost surely be better off with an IDR plan. Not only would your payments count toward possible forgiveness down the road, but they may be as low as $0 a month anyway. In RAP, if your payments don't cover all the interest, all of that interest is forgiven by the government and is NOT added back to the loan amount.

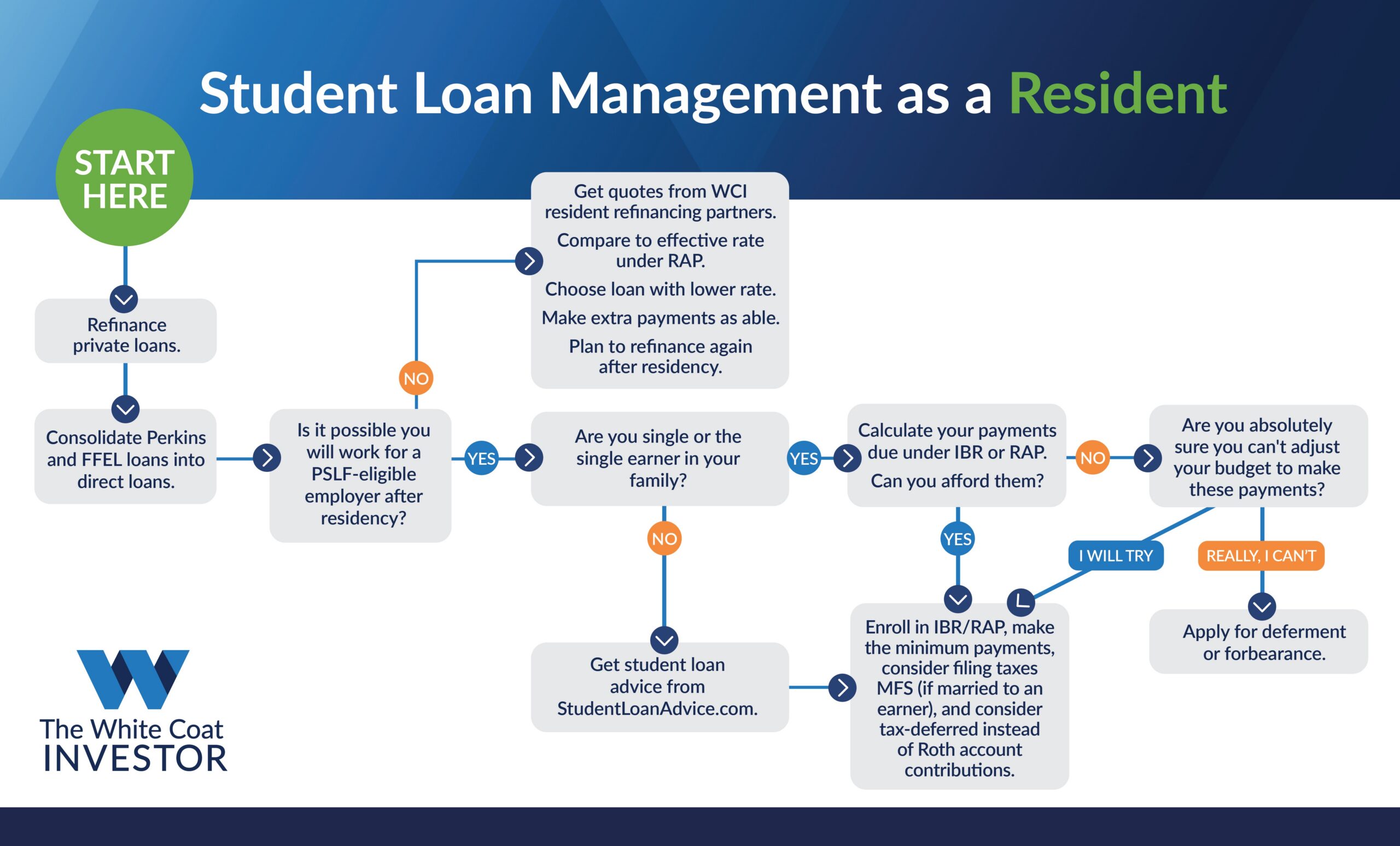

Resident Student Loan Management Flowsheet

Let's summarize what to do with your student loans if you are a resident. The sooner you know if you are going for PSLF, the easier your decisions become. If you are single or the sole earner in a married couple, it can also be very easy. But many people would benefit from getting formal advice from a specialist in student loan management. If you are married to another earner and one or both of you is going for PSLF, consider shelling out a $400-$700 one-time fee as an intern to get advice. It could save you tens or even hundreds of thousands of dollars. It is relatively easy for them to identify the red flags that indicate you're doing things wrong, and they can help you run the numbers to make the difficult student loan management decisions that involve choosing an IDR program, choosing how to file your taxes, and even choosing whether to use a traditional or Roth IRA or 401(k).

Attending Student Loan Management

In contrast to residency—where student loan management can be very complicated, involving your taxes and even your retirement account contributions—management as an attending is generally very simple.

Paying Off Your Student Loans

Your private loans, which you probably should have refinanced in residency, can be refinanced again and again as long as you can get a lower rate (and you usually can as a new attending). Obviously, refinancing doesn't actually make them go away, but it helps make more of your monthly payments go toward principal instead of interest. The way you make them go away is by living like a resident and dumping a huge sum on them every month. Even $500,000 in student loans doesn't last long against a five-figure monthly payment assault.

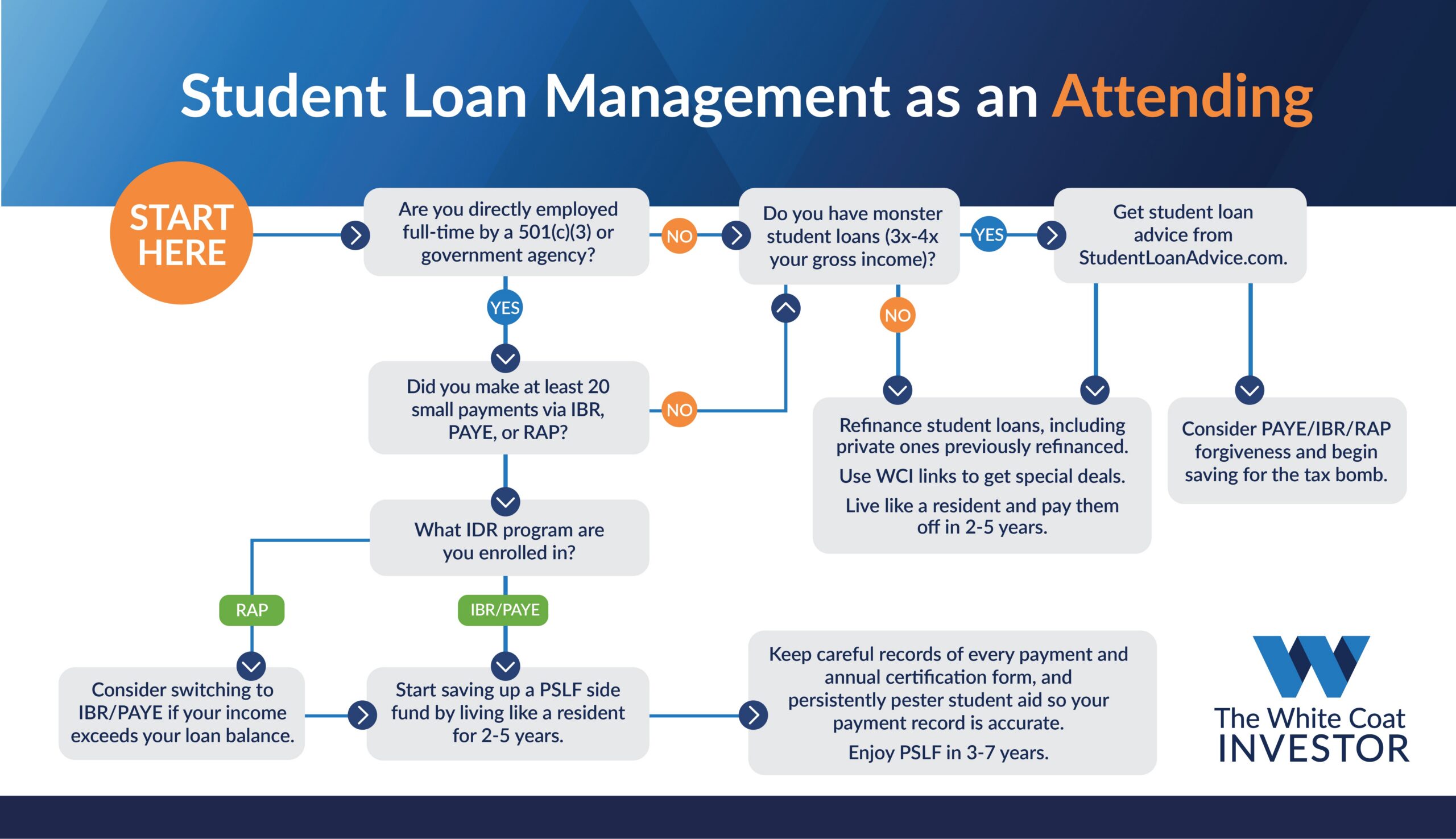

Regarding your direct federal loans, you need to finalize your decision on whether to go for PSLF. This is usually relatively easy. If you can answer BOTH of the following questions positively, you should go for PSLF:

- Are you directly employed full-time by a nonprofit (501(c)(3))?

- Did you make a bunch (it varies, but in general 20+) of tiny IBR, PAYE, or RAP payments while in training?

If you cannot answer both of those questions positively, refinance your student loans and live like a resident for 2-5 years until they are gone.

Best Place to Refinance Student Loans

Here are the best deals on student loan refinancing we've managed to negotiate with the top student loan refinancing lenders:

† Bonus includes cash rebates and value of free course. Borrowers who refinance more than $60,000 in student loans using the WCI links will be enrolled in The White Coat Investor’s flagship course, Fire Your Financial Advisor: ATTENDING for free ($799 value). Borrowers will still receive the amazing cash rebates that WCI has negotiated with each lender. Offer valid for loan applications submitted from May 1, 2021 through October 31, 2026. Free course must be claimed within 90 days of loan disbursement. To claim free course enrollment, visit https://www.whitecoatinvestor.com/RefiBonus.

Refinancing Your Student Loans

The secret to refinancing your student loans is to do it early and often. If you ask your fellow White Coat Investors for their regrets, many say they wish they had done it earlier because it was much easier than they thought. While it may appear intimidating at first, most of the companies will give you an accurate estimate of the rate you will eventually receive in 2 minutes online. You'll need to gather and submit some paperwork, but it's mostly all the same for all of the companies. Once you gather it and submit it to one, it is very easy to submit it to two or three more (or even all of them). Then, just take the one that offers the lowest rate.

The rates offered to you will depend on your credit score, your debt-to-income ratio, and your desired loan terms. Unlike the federal government, which loaned you money just for getting into school, these private companies actually want to make a profit. They only want to loan money to people they think can pay back the money.

The best way to get the lowest rate is to accept a five-year term and a variable rate. If you are willing to live like a resident for 2-5 years after residency and pay off your loans quickly, these terms should be acceptable to you. While there is some legitimate fear of rising rates with a variable rate loan, the truth is that rates have to rise dramatically and/or early in the term for you to come out behind with a variable rate loan. If you can afford the worst-case scenario, we would at least consider a variable rate loan, and run the math under various interest rate scenarios.

Think of a fixed-rate loan as a variable-rate loan plus an interest rate insurance policy. Since you should only buy insurance against financial catastrophes, someone planning to throw $10,000 a month at their loans every month for two years should not pay extra for a fixed rate. Just having a little more of your payment go to interest instead of principal for a few months is not a catastrophe. Even if rates rise early and dramatically, it will likely only delay paying off the loan by a month or two for someone truly committed to getting rid of them.

Some doctors fear refinancing because they are worried about what will happen to them if their income drops, if they die, or if they become disabled. This is a good reason to avoid putting a co-signer on your loans, but if you read the fine print, you will see that most private companies have some accommodations for these situations. Often, they will give you up to a year without payments in difficult situations (although the interest will continue to build). Loans are also often forgiven at death and sometimes even for disability.

Be sure to read the fine print before signing on the dotted line so you know what to expect if any of these unlikely situations happen to you. Even if the company does NOT offer a death or disability plan, realize that purchasing enough term life insurance or disability insurance to cover the loans or its payments is likely cheaper than paying the extra interest in the government programs!

Consolidate vs. Refinance Student Loans

Some people get confused about loan consolidation and use the term consolidating when they mean refinancing.

Student Loan Consolidation

Consolidating generally means taking a bunch of loans and making one loan out of them. While that may increase the convenience of management, it does not actually reduce the interest rate. In fact, it may increase it. With federal loans, the weighted average of your loans is taken and rounded UP to the nearest 1/8 of a percentage point. You can consolidate your loans with the federal government, but to refinance them, you must go to a private company and lose the benefits of federal loans, such as the income driven repayment programs and the forgiveness programs.

Should I Consolidate My Student Loans?

Why would anyone consolidate their loans if it increases their interest paid? Aside from the benefit of only having one loan to manage, the main reason is that you can turn some loans that were NOT eligible for IDR plans and PSLF into loans that are. The classic examples are Federal Family Education Loans (FFEL) and Perkins loans. By themselves, they are not eligible for those programs, but if consolidated into a direct loan, they become eligible. If you fall in this situation and want to use the IDR or PSLF programs, consolidate here.

Another reason to consolidate your loans is when you’re fresh out of med school and enrolling in IDR. Consolidation would allow you to opt out of your grace period and begin making payments 3-4 months earlier. Consolidating Direct federal student loans after you've made payments doesn't reset your progress. Instead, your new consolidation loan receives a weighted average of your existing qualifying payment counts.

PSLF as an Attending

Things are a little more complicated for attendings who wish to go for Public Service Loan Forgiveness. These are generally academicians, or at least people who are willing to be academicians for a few years at the beginning of their careers. However, working for the military or the Veterans Administration or other government agencies can also count. There are also a few nonprofits out there that directly employ their docs who should qualify for PSLF. Often these jobs pay less than a private practice job, so you need to take into account that sometimes you would be better off with a higher-paying job and paying off your loans instead of going for forgiveness.

The big downside of going for PSLF is that you cannot refinance your loans. Only direct federal loans can be forgiven. In the event that legislative or regulatory risk rears its ugly head and changes the program or that you simply change your career goals such that you no longer qualify for it, you will end up paying more interest than you otherwise would have. But for those who stand to get tens of thousands of dollars forgiven, we think it is worth running those risks.

To maximize how much is forgiven under PSLF, you want to make as many tiny loan payments as possible. That means getting started as soon as possible, and that may be even earlier than you think. The more time you spend in training, the more you stand to have forgiven. If you spend five years in a surgery residency and then do a one-year burn fellowship and a one-year trauma fellowship, you may only make three years of “full” attending-size payments, leaving the vast majority of your debt to be forgiven tax-free.

When going for PSLF, you must continue to make payments in an eligible program. For up to a year after leaving residency, those might still be relatively small payments, further increasing the amount eligible to be forgiven. But eventually, as an attending, you'll be making “real” four-figure payments toward your loans. At this point, IBR or PAYE might be the best program to be in because of the cap on the payments at the standard 10-year repayment program amount. That means if you were using RAP during residency and/or fellowship, you might want to switch to PAYE/IBR. Mortgage-sized student loan payments will start quickly as you juggle several competing financial priorities:

- Saving up an emergency fund

- Down payment on a home

- Moving expenses

- Buying into a practice

- Maxing out retirement accounts

- Roth conversions

However, it is probably worth it. Of course, if you were in a situation in residency where you weren't going to qualify for a significant RAP subsidy anyway (usually due to a high-earning spouse), you should just use PAYE (or IBR if ineligible for PAYE) instead of RAP all the way through. But remember, under RAP, you could file under Married Filing Separately to avoid having to use the income of your high-earning spouse.

Another major complaint of those going for PSLF is that the student loan servicing companies, such as MOHELA, provide terrible service. Make sure you stay on top of everything. Not only do you need to be an expert at the requirements of the PSLF program (which of your loans qualify, which repayment programs have payments that qualify toward the 120 required monthly payments, and working full-time for a 501(c)(3)), but you must keep track of all the paperwork, including evidence of every single payment AND a copy of your annual certification forms. The certification is now done electronically (highly recommended over the paper form) and tracked through the studentaid.gov dashboard.

Remember, you could end up going to court with the government to receive your promised forgiveness. Make sure you have the evidence you need.

The PSLF Side Fund

In addition, you cannot just assume you will receive forgiveness. Not only could the program change and you not be grandfathered in, but your employment plans could go in a different direction. Going for PSLF does NOT excuse you from living like a resident for 2-5 years out of residency. However, instead of sending those big four- or five-figure payments to your federal loan servicer, you need to send them to yourself. To your investment accounts, to be specific, creating a “PSLF Side Fund.” This way, even if PSLF doesn't happen for you, you're not behind on paying off your loans.

Hopefully, by living like a resident, you can max out your retirement accounts AND save up this side fund in a taxable account, and you can simply liquidate the taxable account and use the proceeds to pay off the loans. But even if most of that savings ends up in retirement accounts and you can't (or don't want) to immediately eliminate the loans at that point, at least your net worth will be where it should be.

Attending Student Loan Flowsheet

Let's summarize what to do with your student loans as an attending. Private loans should be refinanced whenever possible and paid off quickly by living like a resident. Federal loans should also be refinanced and paid off quickly unless you are directly employed by a 501(c)(3) AND made a lot of tiny payments during your training.

Student Loans and Bad Situations

If you die or are disabled, what happens with your private loans will be dictated by the terms on their promissory notes. Worst case scenario: if you die, they are assessed against your estate. Your parents or siblings are never responsible for your loans, but your heirs could be indirectly.

What Happens to My Student Loans If I Die?

In the event of death, your federal loans are discharged. With Parent Plus loans, the loans are discharged if the student OR the borrower dies.

Are Student Loans Forgiven If I Become Disabled?

In the event of permanent disability, federal loans are also forgiven. In a temporary disability, however, you may be limited in the use of the IDR programs, deferment, or forbearance.

Bankruptcy and Student Loans

Student loans generally survive bankruptcy, meaning you cannot wipe them out simply by declaring bankruptcy. However, if you can prove undue hardship, you could possibly have them discharged. Defining undue hardship is going to be up to the judge, but we can assure you that if you qualify for it, you're going to be in a terrible place financially either way.

Depending on what happens to your loans at death and disability, consider carrying a little extra term life and disability insurance coverage to make up for it.

Closed School Discharge

In the event of school closure, you might have your loans discharged. This tends to come up more in for-profit institutions, but it’s very rare.

False-Certification Discharge

In the event of the school falsely certifying your eligibility to receive a loan, you may be eligible for loan discharge. But this is very complex and unusual.

Should I Pay Off My Student Loans Early?

Some people with low-interest rate student loans wonder if they should really pay their loans off rather than invest. While it is intuitively attractive to borrow at a low rate and earn at a higher rate, this decision often ignores two factors.

The first is that most people simply don't invest the difference. Behaviorally, it is more difficult to maintain focus on building wealth once you have decided to make minimum payments and end up spending the money instead of investing.

The second is that an investment that provides a rate of return higher than the guaranteed return available by paying off your loans usually involves a significant risk of loss. However, if you would like to carry your loans a little longer in order to invest inside retirement accounts, we think that's OK. But we would still plan to have them paid off within five years of finishing training. The financial muscles you develop by paying off your loans quickly are the same ones you will use to build wealth toward financial independence afterward. We do not recall ever meeting a physician who regretted paying off their student loans quickly. In fact, most express a feeling of massive relief, such as this email Jim received a while ago from a two-doctor couple who paid off over $700,000 in student loans in 16 months:

“This student debt problem is so huge and overwhelming. I had many poor nights of sleep during training fretting about, ‘How do we pay off this 3/4 million dollar debt?' I feel now an immense stress has been lifted. We can now go forward and make some real decisions about how we want to live out the rest of our lives.”

You can slay the student loan dragon. Sit down and get started today. Figure out where you stand; list out your loans by amount owed, payment, and interest rate, and add up the total. Then start working on a plan to handle them. You can do it, the entire White Coat Investor community is rooting for you!

What do you think? What other information belongs in the ultimate guide to managing physician student loans? Have you paid off your loans? What other advice do you have about them for your fellow white coat investors?

[This updated post was originally published in 2019.]