By Dr. Jim Dahle, WCI Founder

By Dr. Jim Dahle, WCI FounderWe've spent lots of time discussing annuities here at The White Coat Investor over the years. Annuities are insurance products where cash value grows in a tax-protected way but where gains are paid at ordinary income tax rates upon withdrawal. Since they are designed for retirement, like IRAs, the Age 59 1/2 rule applies.

Reasonable Use Cases for Annuities

Unbiased, knowledgeable people have identified four reasonable “use cases” for annuities and four “good annuities” appropriate for these use cases. Not all use cases are equally common, but as a reminder, here they are.

#1 Buying an Income

If you want to take a lump sum of money and turn it into a pension (i.e. a guaranteed source of life-long income), this is called annuitization. There is an annuity designed to do this called a Single Premium Immediate Annuity (SPIA). It's very straightforward. As an example, a 65-year-old man gives an insurance company $100,000, and that insurance company pays him $635 a month or $7,620 a year (as of July 2024) for as long as he lives. With a SPIA, you're essentially putting a floor under your retirement spending. This should be the most common use for an annuity.

#2 Longevity Insurance

A similar annuity is a Deferred Income Annuity, or DIA, some of which are QLACs. This is like a SPIA, but it doesn't start paying you for many years. For example, that 65-year-old man could buy a $100,000 DIA that starts paying in 20 years just in case he lives a long time. It would pay him $4,398 per month ($52,776 a year) from age 85 until death. Having this annuity in place gives the man “permission to spend” his current assets, whatever they might be, very aggressively because he knows he has this income coming to take care of him later in his life.

#3 CD Alternative

A third type of reasonable annuity is a Multi-Year Guaranteed Annuity (MYGA), a type of deferred fixed annuity. MYGAs come with a term ranging from 1-10 years and sometimes—especially for the longer time period—pay more than bank certificates of deposit (CDs). Unlike a CD, you have the option to reinvest the income without paying tax on it. Plus, when the term is up, you have the option to exchange it tax-free into a new MYGA (or SPIA). If the rates are similar or better, a MYGA can work out better than a CD. The big issue with MYGAs is that most people saving for retirement should only be putting a small percentage of their savings into conservative investments like CDs or MYGAs. They need their money to do much of the heavy lifting, and that requires more risky investments like stocks and real estate.

#4 Investing Fees vs. Taxes

There are also some niche uses for variable annuities (VAs) with low fees and good investments (it's definitely not the majority of VAs). For example, some people who were suckered into buying whole life insurance realize their mistake, exchange it into a low-cost VA, and let it grow back to basis tax-free prior to surrendering the whole life. There might also be times (admittedly pretty rarely) when the tax benefits (and potentially asset protection benefits) of the VA can outweigh the additional costs of the VA when investing for retirement.

More information here:

Why Mixing Insurance and Investing Causes So Many Problems

Which Annuities Are Actually Sold?

If we look at all four of these use cases, most would agree that the most common use case by far would be Buying an Income, i.e. immediate annuities. There would be some MYGA purchasers out there and then (rarely) a few people buying DIAs and good VAs. But what do we actually see when we look at which annuities are being purchased (sold?) Take a look at the data from the Life Insurance Marketing and Research Association (LIMRA).

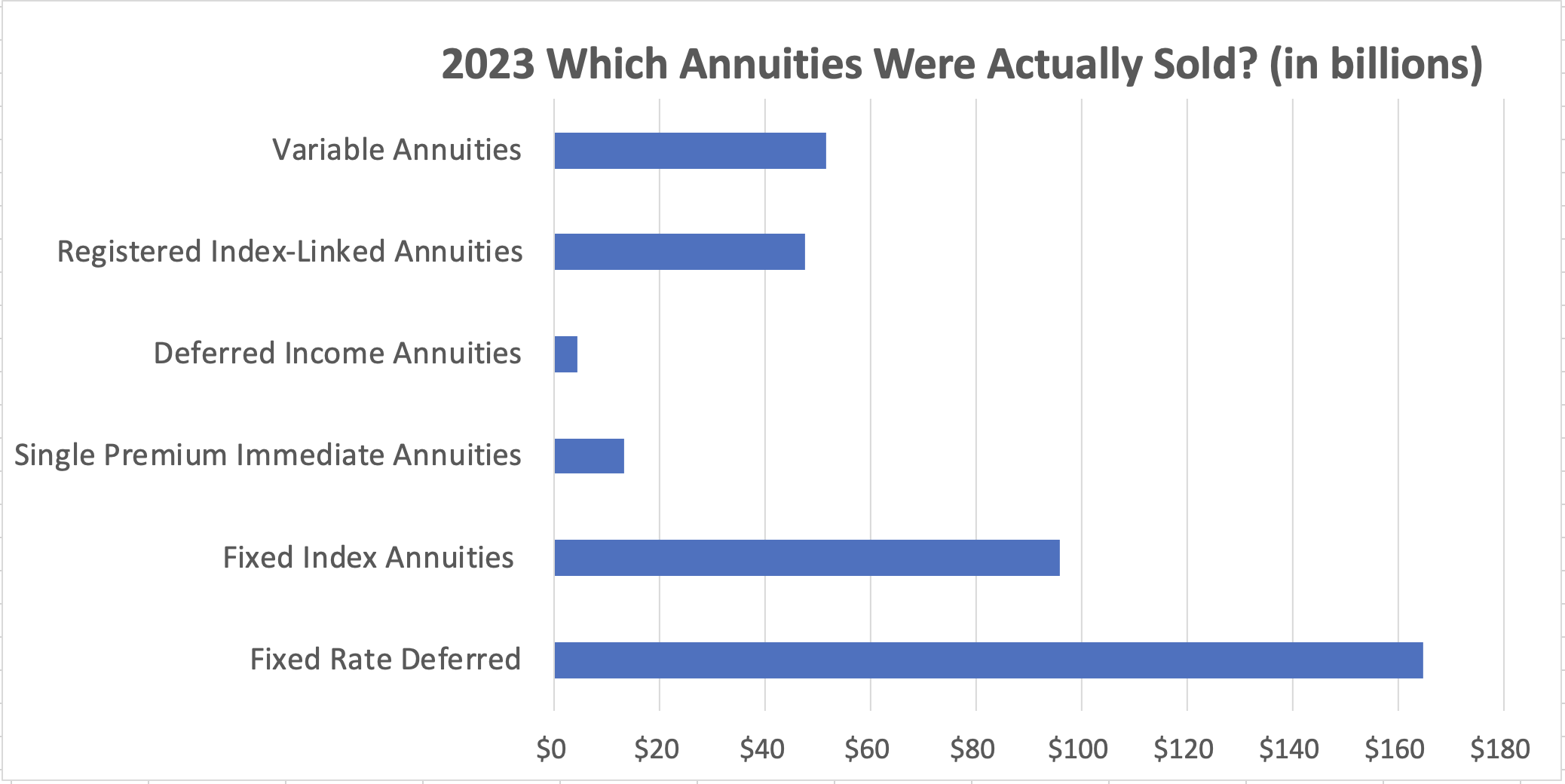

In 2023, $385 billion in annuities were sold in the US. Which ones, you might ask?

As you can clearly see from the chart, only $13 billion of that $385 billion consisted of SPIAs, which are frankly the best use case for annuities. This should be the most common use case, too. It shouldn't even be close. But just 3% of annuity sales were SPIAs. The amount of DIA sales seems appropriate enough, but after that, this chart is bonkers. Both categories of index annuities are basically garbage, as are most variable annuities and fixed-rate deferred annuities. Yet they comprise 96% of annuity sales.

No wonder unbiased, informed advisors default to just saying “avoid annuities.” I mean, sure, some small percentage of those fixed-rate deferred annuities are the best-priced MYGAs out there, and some tiny percentage of VAs consist of appropriately sold, low-fee, good investing option VAs. But this chart is an indictment of an entire industry. It's financial malpractice to be selling this garbage to people in these quantities.

A Case Study

Jason Zweig wrote a column recently in the Wall Street Journal that could be considered a case study of what the industry will do when it can. Since Zweig's column is behind a paywall, I'll summarize what happened for you.

In 2008, Paul and Sue Rosenau won the Powerball lottery. When all was said and done, they walked away with about $60 million. Unfortunately, like most Powerball players, the Rosenaus weren't particularly financially literate. However, they were very charitable. They decided to use $26 million of their winnings to start a foundation to research a cure for and help families with Krabbe disease. Yeah, I didn't remember from medical school what it was either, but if you look it up, you'll see that it is a genetic enzyme deficiency that leads to demyelination, spasticity, neurodegeneration, and usually death before age 4. Their granddaughter had it.

So, the Rosenaus go to a local “financial advisor,” who happens to be an annuity salesman employed by Principal. Recognizing a “whale” when he saw it, he promptly arranged for the Rosenaus to be flown out on a private jet to Principal headquarters to meet with the bigwigs. The end result was that 93% of the assets of the foundation were “invested” into variable annuities. This, of course, is nuts. It's financial malpractice. The primary benefit of investing in a variable annuity is that it grows in a tax-protected manner. However, ALL ASSETS of a charitable foundation are already growing in a completely tax-free manner. Charities don't get taxed at all. The annuity wrapper was doing NOTHING other than generating commissions. It gets worse, the “advisor” then starts churning the annuities, selling some and buying others, generating new commissions each time. When all was said and done, a total of $47 million in variable annuities had been purchased, generating commissions of approximately $3.3 million.

The worst part of all this is that these didn't seem to even be annuities with good investment options. Zweig explains:

By year-end 2011, [the advisor] had sunk $28.3 million of the foundation’s assets into variable annuities. Six years later, that pool had shrunk to $26.3 million—even though the stock market had more than doubled over the period.

I estimate the foundation could have earned $12 million-$25 million more between 2011 and 2017, when it finally pulled its money away from [the advisor] if it had invested instead in a simple balanced index fund with 60% in stocks and 40% in bonds.”

The cost of this mistake wasn't $3 million; it was more like $20 million. The story just gets worse from there. Sue died of ovarian cancer in 2018. For some reason I can't understand (just kidding – it was for the commission), the advisor also talked the foundation into buying a $3 million life insurance policy on Sue before her diagnosis. What luck! Finally, something financially good happens, even if it was out of sheer luck. But wait, the “advisor” then recommended the foundation sell the life insurance policy for $1.46 million in 2017, just a year before she died. Rosenau says the “advisor” consulted with a doctor who accurately told him that Sue was likely to be dead within two years prior to recommending that sale.

There are no winners in this story. The “advisor” was fired by Principal in 2019 and then died by suicide in 2020. The foundation went to arbitration with Principal through FINRA and was awarded $7.3 million, more than twice what they collected in commissions to start with. Meanwhile, there's $20 million less in the world to fight Krabbe disease.

More information here:

A Doctor’s Review of the Retirement Income Style Awareness (RISA) Profile

The Bottom Line

It's a pretty good rule of thumb to not trust anybody who sells annuities. If you find that you have a good use case for an annuity, shop around carefully and consider enlisting the assistance of a knowledgeable fee-only advisor to help ensure you're getting the best possible annuity to do what you're looking to do. And for heaven's sake, don't let charities you're associated with buy annuities at all.

In need of help on your financial journey? Over the years, The White Coat Investor has carefully curated a recommended list of professionals who have been thoroughly vetted and trusted by thousands of readers. Explore our handpicked selections today, and get the exceptional support you deserve.

What do you think? Why do you think the wrong annuities are being bought and sold? Has somebody ever tried to sell you one?