Low interest rates punish savers and benefit borrowers. My investment career started in 2004 when I was an intern. For most of the last 20 years, interest rates have been quite low. Over the last couple of years, though, the Federal Reserve has raised short-term interest rates dramatically, reversing this trend somewhat. We do not know whether this is a long-term situation, but I fear that many people will not adjust their mindset and attitudes about saving, investing, and borrowing appropriately as the interest rate environment changes.

Historical Interest Rates

I can distinctly remember earning 5.25% on cash in the Prime Money Market Fund (MMF) in 2007 just before interest rates were cut in response to the global financial crisis. It seems that, at that point, interest rates had just returned to normal from the cuts the Fed made during the dot.com-associated bear market of 2000-2002.

Our first mortgage was 8% in 1999. Our second was 6.25% in 2006. By the time we paid off our final mortgage in 2017, it was 2.75%. I had medical school classmates who refinanced their student loans at 0.9% in 2003 when we graduated. When I started The White Coat Investor in 2011, student loans were at 6.8%, and they could not be refinanced anywhere. In recent years, many docs have refinanced their loans at sub-2% rates.

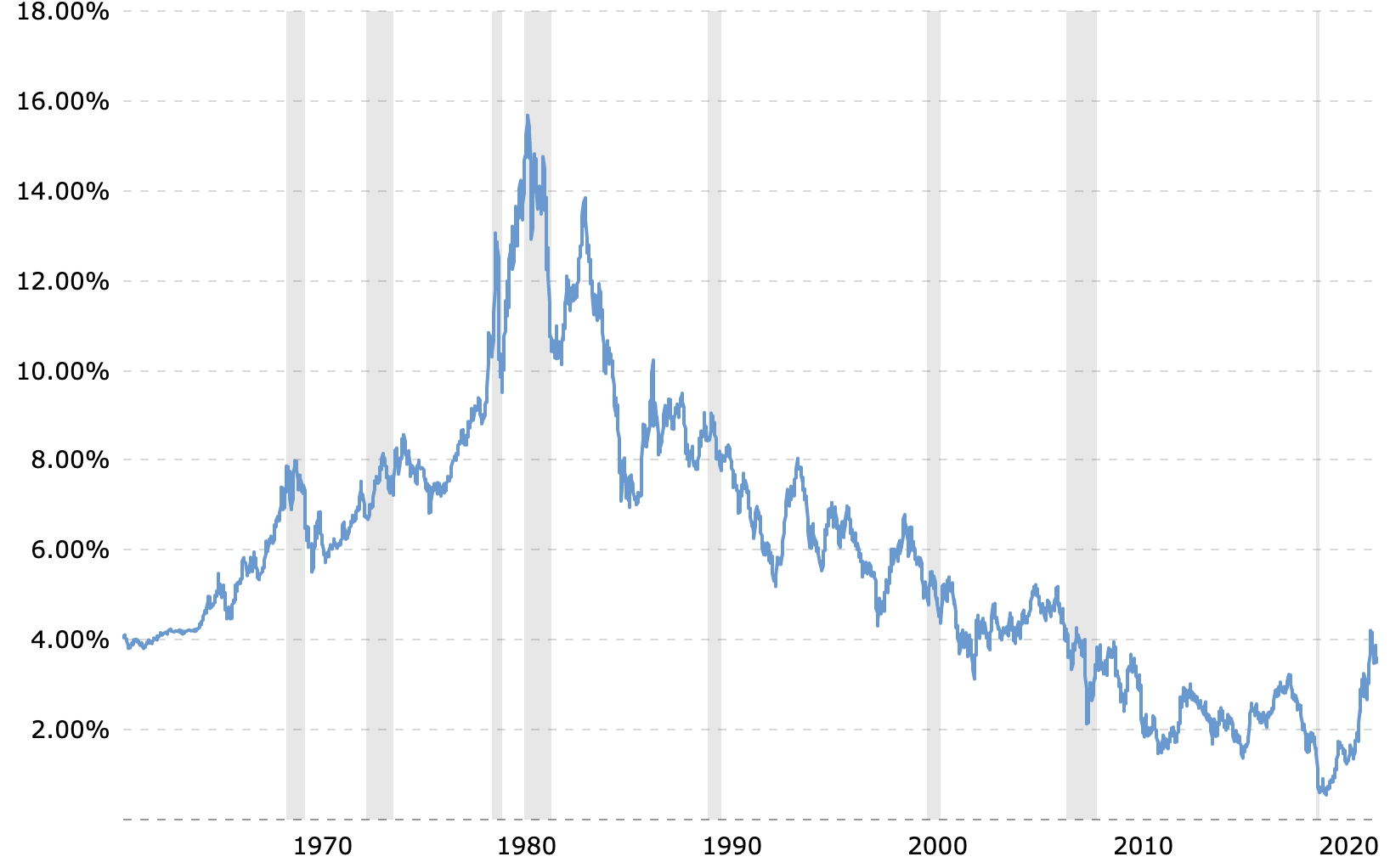

It is important to understand the history of interest rates. For example, here is a historical chart of the Federal Funds Rates, i.e. the rate at which institutions lend money to each other overnight. This is very short-term interest and the one over which the Fed exerts maximal control.

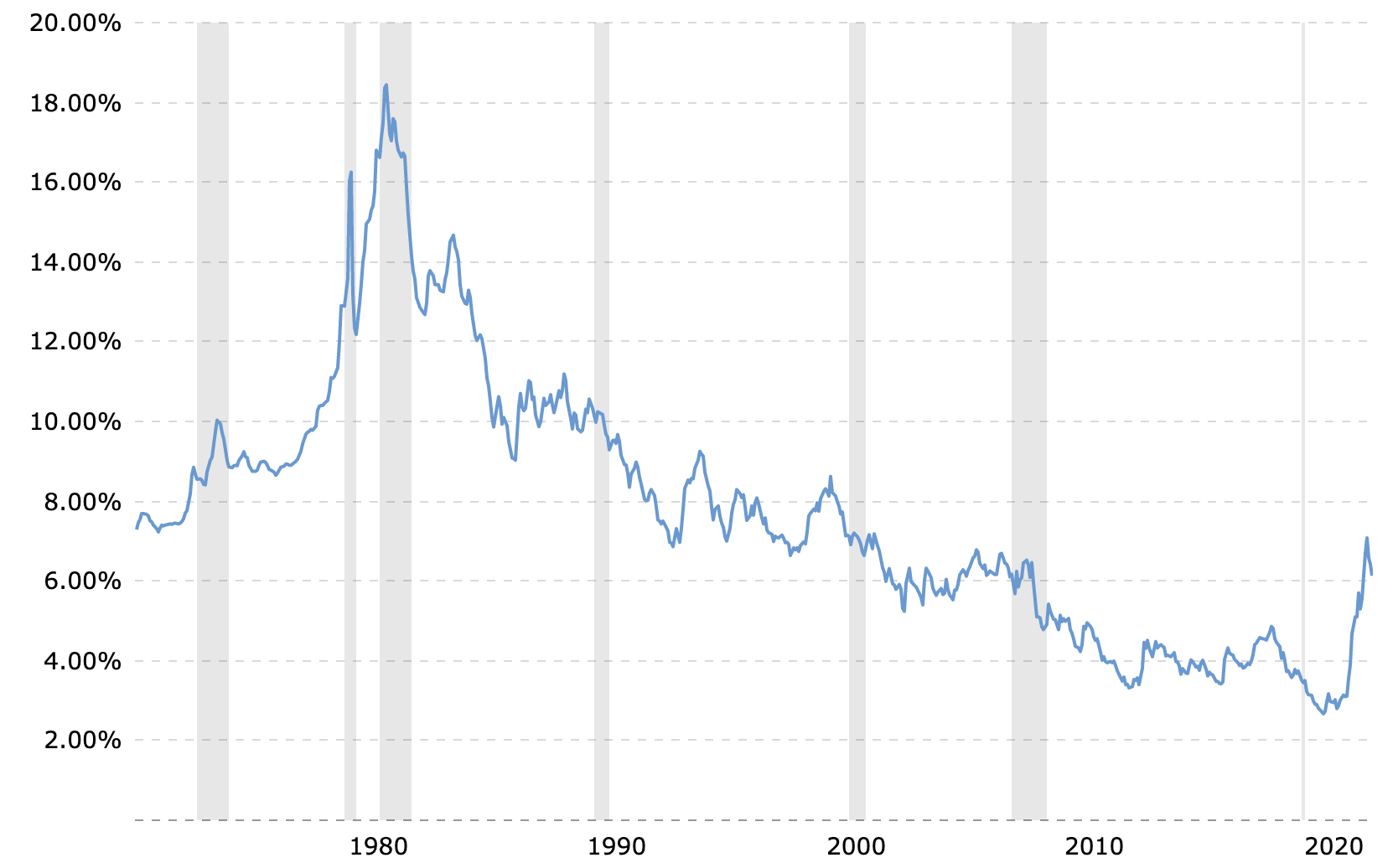

An impressive amount of variation, right? But that's not true in the 10 years following the global financial crisis. In fact, it was pretty much 0% most of the time from 2008-2022. It is easy to forgive a relatively new investor who might think this sort of thing is normal. It's not anywhere near normal. Four percent is far more the normal level, and there have been decades where it averaged twice that. Let's take a look at some other interest rates. How about the 10-year Treasury yield?

That's right, earning 2% on Treasuries is not normal. In fact, for most of history, bonds beat inflation. Hard to believe, right? Yields between 4%-8%? Pretty normal. Yields that are sub 2%? Not normal. How about mortgages?

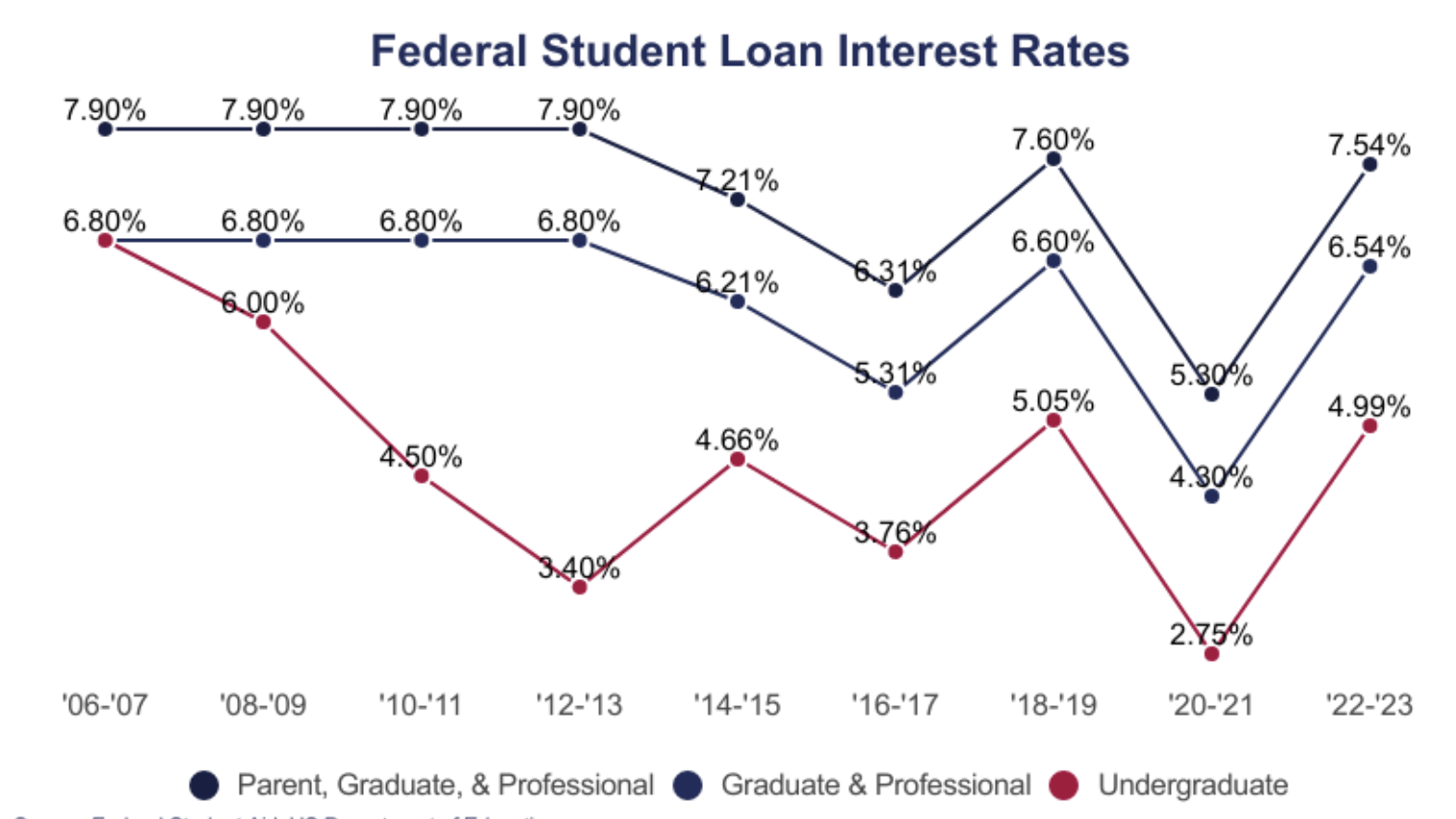

Same story as the other rates. Mortgages that are 6%-10%? Normal. Mortgages with sub 4% rates? Not normal. Similar data is available for student loans.

While this chart's history isn't as long as those other ones, the point remains that even during times of low interest rates, medical students have been borrowing at 6%-8% for their schooling. As/if rates continue to climb, those interest rates are likely to be higher than what is in this chart, not lower. The formula for medical school loan interest rates is the 10-year Treasury yield plus 3.6%. Add 1% more for PLUS loans. Expected rates right now for 2023-2024 are 7.26% and 8.26%, respectively. Do you have any idea how quickly loans grow at 8.26%? If you make minimal payments during four years of med school and six years of fellowship, that $100,000 you borrowed for your first year of school will grow to $221,000 by the time you finish training. If you borrowed $100,000 for each of those four years of school at 8.26%, the interest alone on the debt could be something like $60,000 a year by the time you're an attending.

More information here:My Fear

My fear is that people will have developed habits; rules of thumb; and ideas about interest rates, debt, and proper money management in this low interest rate period that will not serve them well in a more historically normal period of interest rates. Let me go through some of these ideas and why they may not be accurate going forward.

Cash Is Trash

For years the yields on cash, especially after-tax and after-inflation, have been pathetic. As a result, many people, even retirees, have not held cash in their portfolios, have minimized the size of their emergency fund, and have poured their money into investments—any investment—in hopes of a better investment return. Low interest rates fuel speculative bubbles. Perhaps the crypto/NFT/meme stock mini-bubbles would not have blown so big if investors could have gotten a steady 5% out of their money market funds and savings accounts.

While inflation reached as high as 9.1% in 2022, inflation has been falling rapidly. Current yields (5% as we publish this in December 2023) have finally outpaced inflation (3.1% at the end of November 2023), and since cash usually outpaces inflation—at least pre-tax—we're just returning to normal here.

Some investors have been just letting their money languish in a checking account or pathetic local bank savings account earning a yield that rounds to zero. It hasn't mattered in the last few years. Even if you found the best cash investment out there, you might not have been earning 1%. Well, now it matters.

100% Stock Portfolios

As interest rates fell, bonds, much like cash, became less and less desirable. As a result, plenty of investors adopted a 100% stock portfolio. Real interest rates (TIPS yields) were negative for a while. Even nominal interest rates were negative at one point on one- and three-month Treasury bills as the pandemic hit. You've got to really wonder about an investment whose expected return is less than stuffing Benjamins in the mattress.

As a result of low rates, investors piled money into stocks. Some people even treated dividend stocks as a bond alternative. Stock returns in the 2010s and early 2020s were above historical averages. That pendulum swings, though, and many inexperienced investors would probably be surprised by lower returns on stocks in the mid to late 2020s than they saw in the first part of their investment careers. The same thing happened to people who started investing in the 1990s and mistakenly thought they were supposed to make 20%+ a year. I can't tell you how many docs I met early in my career who were day trading dot-com stocks between patients, only to suffer through a lost decade of returns in US stocks in the 2000s. Same phenomenon, different generation.

Not Refinancing Student Loans

This one isn't just interest rate-driven. While I was really happy for indebted white coat investors who got to enjoy 0% interest rates and $0 PSLF-qualifying payments for three years due to the pandemic, the moral hazard induced by both implemented and proposed student loan policies is severe. In coming years, how many students will hold on to 7%, 8%, and 9% student loans in hopes of another student loan holiday or a new forgiveness program, only to be disappointed and saddled with career-lengthening and burnout-inducing levels of educational debt?

Dragging Out Student Loans

Dragging out student loans at 1%-2% might make sense. Presumably, your investments will earn more than that. If not, we've all got bigger problems. In fact, you can guarantee returns better than that these days. That's not the case when interest rates are 6%-10%. Those are the historical returns on stocks, which are anything but guaranteed.

Paying off an 8% student loan is a fantastic guaranteed investment return. Higher interest rates make living like a resident and wiping out that debt quickly even more important. If that advice has sounded old-fashioned to you at some point in the last decade, I bet it won't 10 years from now. Conservative, traditional ideas stick around for a reason. They're usually right, at least in the long run. Change is not always progress.

High Loan-to-Value on Investment Real Estate

You've probably noticed some of your physician colleagues making a killing on real estate in the last 5-10 years. Cheap money increases the value of real estate and allows your money to go further when buying it. Tax policies like bonus depreciation (now phasing out) compounded the effects. If a little leverage is good, more must be better. Conservative borrowing practices have not paid off in the last few years. That will probably change. Interest rates matter. Nobody ever declared bankruptcy without debt.

Buying a Home Always Works Out

On a related note, the real estate boom has made conservative advice like

“Only buy a home you will stay in for at least five years”

“Don't buy a house during residency”

“Rent for 6-12 months to make sure the job is working out before buying”

seem silly. Homebuyers worried that if they didn't buy now, they could NEVER afford to buy a home in that area. This is another classic pendulum. Homes didn't appreciate much from 2000-2003. Then, they appreciated a lot from 2003-2006. Then, they fell sharply from 2007-2010. Buying in 2011-2013 worked out great. It's hard to imagine that there will not be one of these classic pendulum swings associated with the most rapid change in interest rates since the 1980s.

Debt Is a Tool, Not Something to Be Feared

This idea about debt being “just a tool” rather than something dangerous gets pumped out frequently, particularly when interest rates are low. The truth is that debt is a tool but a dangerous one. The people I meet who build lasting wealth tend to both invest and pay off debt. Show me someone with zero fear about debt, and I'll show you someone who has not been playing this game very long. There are no old, bold pilots. Investing is about risk control. One of the biggest proponents of using debt to invest is Thomas Anderson who wrote a series of books called The Value of Debt. You cannot come away from his books without a healthy respect for the downsides of investing with borrowed money. The books are full of caveats and warnings.

More information here:Future historians may call the 2022-2023 era The Revenge of the Savers. Make sure you haven't been lulled into complacency and bad habits by a long period of low interest rates.

What do you think? How should investor/borrower behavior change now that interest rates have risen dramatically?