We had a slow shift in the ED a few months ago. That means different things to different people, but in my ED when I'm on, it means we talk finance. While trying to prepare for a Zoom presentation I had that evening to a group of docs and APCs, I was cornered by a nurse, a clerk, and an X-ray tech. Before I get into the conversation, I need to provide you with a little background information.

First, I've helped five or ten ED nurses set up their 401(k) asset allocation over the last five years. That means showing them how to change from a portfolio that ranged from 100% cash to a dozen expensive actively managed mutual funds into what is typically a handful or less of low-cost, broadly diversified index funds in a stock/bond mix that ranges from 60%-90% stock. This is typically accompanied by a 1-2 hour discussion about successful long-term investing and an emphasis on increasing the contribution rate to the account (since most of them have a five-figure balance at mid-career).

Second, this conversation took place on October 18, 2022. The financial world is rapidly changing and who knows what it will look like by the time you read this. On the day of this conversation, here is what it looked like:

- YTD stock return: -23.27%

- YTD bond return: -16.49%

- Utah housing prices: Prices down 8.5%, days on market up from eight to 38 in the last five months

- YTD Bitcoin return since its last peak: -72%

- Ten-year Treasury rate: 4.02%

- Inflation rate: 8.20%

- Ally Bank savings account yield: 2.25% (plus a 1% bonus for new money up to $50,000 invested now and left in the account for six months)

- Vanguard Federal Money Market Fund yield: 2.83%

- Vanguard Municipal Money Market Fund yield: 2.28% (3.62% equivalent for those in the 37% bracket)

Bear Market Behavior

The conversation began with a nurse who told me what she had done with her 401(k) and asked me what I thought. Uh oh. My big worry was that she had panic-sold, selling after everything had gone down in price and going to cash. It turned out that was not the case. What she had done was cut her contribution rate from 16% of her salary (perhaps the highest of any nurse I have talked to) to 6%. Why had she done that? Her initial excuse was that “I could really use the money.” Well, there's probably some truth to that, especially given inflation over the last year. But that wasn't the real reason. When we drilled down on it, she had checked her balance four months ago, and she could calm her jitters then. But when she did it again recently, it was too much. It felt like she was stuffing money that she had really sacrificed today for her future down a rathole, and it hurt too much to see it then go down more in value.

What followed next was a long conversation that slowly drew in more and more staff members. The gist of the conversation was based on this quote from Warren Buffett:

“A short quiz: If you plan to eat hamburgers throughout your life and are not a cattle producer, should you wish for higher or lower prices for beef? Likewise, if you are going to buy a car from time to time but are not an auto manufacturer, should you prefer higher or lower car prices? These questions, of course, answer themselves. But now for the final exam: If you expect to be a net saver during the next five years, should you hope for a higher or lower stock market during that period? Many investors get this one wrong. Even though they are going to be net buyers of stocks for many years to come, they are elated when stock prices rise and depressed when they fall. In effect, they rejoice because prices have risen for the ‘hamburgers' they will soon be buying.

When vacations, cars, and groceries become cheaper, we buy more of them. Why do we buy fewer stocks when their price goes down? Simply because we naturally extrapolate recent past returns into the near future. Because they have gone down, we assume they will continue to go down. And when they go up, we assume they will continue to go up. To a certain extent, this is even true, at least for a while. (It's called momentum investing.) But in the long run, buying shares at lower prices provides better returns.

Some of the highest-returning investments I have ever made came from the money I invested between October 2008-April 2009. The same goes for investments made in September 2011, December 2018, and March 2020. I have no doubt that the investments I made into stocks and bonds in September and October 2022 are going to have excellent long-term returns. That doesn't mean that stocks won't go down even further in the first six, 12, or even 18 months after being invested. But I'm not investing money that I need in six, 12, or 18 months. The investor matters more than the investment. How you behave in down markets is far more important than your particular chosen asset allocation. Don't just learn this lesson. Internalize it.

More information here:The Value of a Financial Advisor

Next, the clerk mentioned that she and her husband had recently met with their financial advisor. The advisor had come into town and reached out to take them out to drinks. He opened the conversation with, “I like to meet with you both when I have good news . . . and when I have bad news.” The bad news, of course, was that their investments (along with the overall markets) had gone down sharply. I have no idea if the advisor is what I would describe as someone “giving good advice at a fair price” (probably not, given the level of assets we're talking about, this is almost surely a commissioned salesman masquerading as an advisor).

However, the advisor did at least one thing right: he reached out to prevent bad behavior (i.e., selling low in a bear market). For a typical investor, this may be the most valuable function that an advisor performs, and if it prevents panic-selling, it's worth all of the fees and even commissions that the investor has paid over the years.

More information here:Short-Term Savings Yields

The conversation turned from the subject of long-term investments to short-term investments as the radiology tech wondered if her savings account was any good. I asked the name of the institution. She shared the name of a local credit union. In fact, it turned out that all of the staff members had their savings in one local credit union or another. This is what I said:

“If you have not deliberately placed your cash into a non-local institution specifically to earn a higher yield, the return on your savings account rounds to zero.”

I was confident that would be the case, and sure enough, as we looked up the rate pages of each of the institutions, we found that they were all earning 0.05% on their savings. At one credit union, they could get that number as high as 0.40% if they had $250,000 or more sitting in the account. But not one of them was offering a yield over 1% no matter how much was in the account. Meanwhile, the going rate on cash at any reasonable, national, high-yield savings account or solid money market fund was 2%-3%. Mine, sitting in the Vanguard Municipal Money Market Fund, was earning the pre-tax equivalent of 3.62%, approximately 72 times the yield they were earning. This was something they could do in the midst of this bear market that would actually make a difference in their financial lives. Plus, it might distract them from selling low.

A quick internet search showed that there were 10-20 institutions nationwide offering 2%+ yields on savings accounts (as of January 2023, you could find plenty of institutions that were offering more than 3% and at least one offering more than 4%). Many were at institutions that I had never heard of, but there were plenty at trustworthy household names like Citi, Barclays, Capital One, Ally, and SoFi. They were all backed by the FDIC. The highest yield we found was at a place called UFB Direct, paying 3.11% at the time.

I told them that they didn't need to continually chase rates, moving money from one of these high-yield accounts to the next every month or two. The rank order was different last month, and it will change again next month as banks seek to fine-tune their deposit levels in a competitive environment. But they did need to pick one of them and link it to their checking account so that cash they didn't need for a few weeks or months could earn a higher yield than something that rounds to zero. They told me my next book should be called “Rounds to Zero.”

Money Market Fund Yields

The other alternative, of course, was to use a money market fund. I'm not talking about a money market account at your local bank or credit union. These seemingly misnamed accounts might pay more than the savings account (so you earn 0.10% instead of 0.05%), but it's still pathetic. I'm talking about going to Vanguard and buying shares of any of their excellent money market funds. Once I started talking about buying shares, some got intimidated.

“I don't know how to buy shares. That sounds hard.”

I logged into my account and showed how it literally takes 30 seconds and looks exactly like moving money between a savings account and a checking account. The barriers to successful investing can be surprisingly small.

Savings account yields tend to lag behind money market fund yields. When rates go down, money market yields typically fall first. When rates go up, money market yields typically rise faster. But the only way to know which one is higher at any given time is to actually look. I find that I tend to swap between my Ally Bank savings account and a Vanguard money market fund about once a year or so as yields fluctuate. Rates have been rising rapidly lately, so the Vanguard Federal Money Market Fund is currently outpacing the yield at every high-yield savings account at an institution I have actually heard of before. But that might not be the case in six or 12 months.

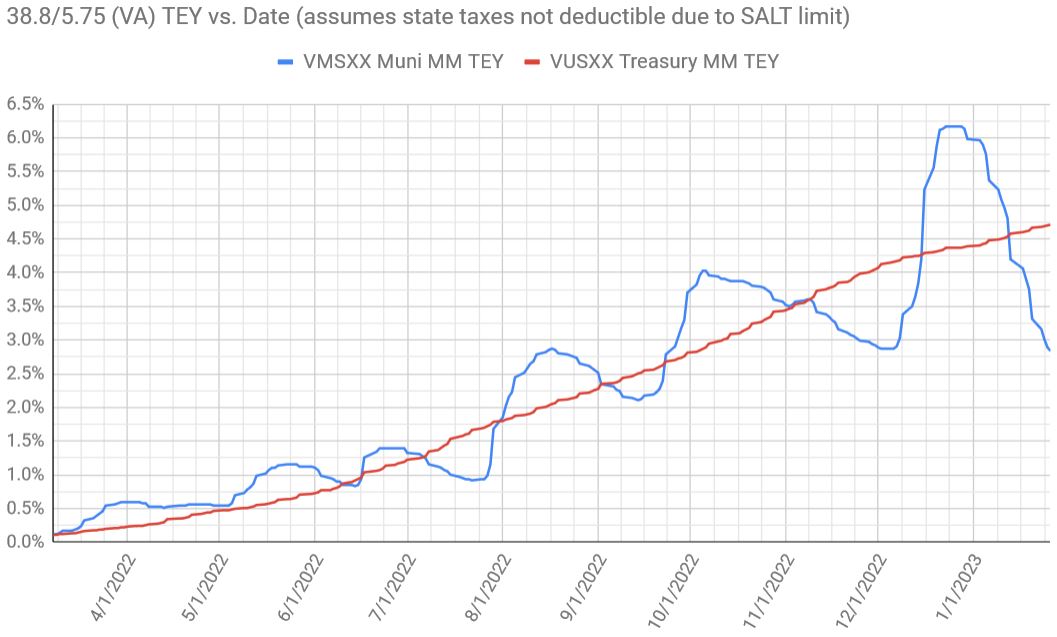

I didn't bother getting into a discussion about municipal (muni) bonds vs. non-muni bonds (and, of course, a muni money market account vs. a regular one), but that discussion is worth having here among white coat investors. Remember that the yield (i.e. the interest paid) on muni bonds (including the very short-term ones in a muni market fund) is always free of federal income tax. If the bonds are issued in your state, they are also free of state and local income tax, so it may be worth looking at a state-specific muni bond/money market fund if it is available.

You have to adjust the yield of a muni money market fund to a comparable pre-tax yield to know where to invest. Alternatively, and perhaps more accurately, you can adjust the taxable yields to get a post-tax yield. To be truly accurate, you should also include state taxes. In my case, my federal tax bracket is 37% and my state tax bracket is 5% for a total marginal tax rate of 42%.

- My after-tax yield on my savings account at Ally Bank is 2.25% * (1-42%) = 1.31%.

- My after-tax yield on the Vanguard Federal Money Market fund is 2.83% * (1-42%) = 1.64%

- My after-tax yield on the Vanguard Municipal Money Market fund is 2.28% * (1-5%) = 2.17%

We have a pretty clear winner.

If it is easier, you can simply calculate the pre-tax yields on your municipal money market funds.

- My equivalent pre-tax yield on the Vanguard Municipal Money Market fund is 2.28%/(1-37%) = 3.62%

Obviously, that compares very favorably to 0.05% at the credit union, 2.25% at Ally, and even 2.83% in the federal money market fund. Muni bond yields are doing particularly well compared to non-muni bonds lately. That's not always the case. The only way to know is to look at the yields and do the calculations every now and then.

To be technically correct, you would also have to correct the yields for the fact that treasuries, including the short-term treasury bills held in many money market funds, are state tax-free, but the difference is usually so trivial it can be ignored.

Whether to use a regular money market fund or a muni money market fund depends both on current yields and on your tax bracket. Let's just consider federal income tax for this exercise.

As you can see, if you were in the 22% bracket or higher on October 18, 2022, you would be better off in the municipal money market fund than the federal money market fund. That's probably a little abnormal. More typical would be that you would need to be in the 32% bracket or higher to benefit from using municipal securities. But you can see that the only way to be sure that your money is always earning the best yields is to compare rates and do calculations frequently.

What do you think? How do you help others to stay the course in a bear market? Where do you keep your short-term cash?