Using a cash back or rewards credit card is a key step for optimizing your financial life. By using the right credit card, you can get 2%, 3%, 5%, or even more back on every purchase you make. Given that the average American spends $5,200 per month using their credit card, you could easily be leaving hundreds, if not thousands, of dollars on the table each year by not using a rewards card. Your biggest expense, rent or mortgage payments, is most often paid by bank transfer or check. However, some credit cards are designed to reward you for using them to pay your rent.

Can You Pay Your Rent or Mortgage with a Credit Card?

Paying your rent or mortgage with a credit card may sound unusual. After all, most people pay their bills using an electronic funds transfer or by check, and many landlords and mortgage companies specify precisely how you need to send payment.

However, that doesn’t mean that there aren’t ways that you can use a credit card to pay your rent. Some services will let you pay a bill via credit card and send a check or electronic transfer on your behalf, but most of these services charge a fee that exceeds the rewards you will earn.

A better choice for people who want to earn points by paying their rent or mortgage is a card designed expressly for that purpose, like Bilt Card. While the Mesa Card used to exist as a rewards credit card designed for homeowners to pay their monthly mortgage, that credit card went defunct at the end of 2025.

More information here:

Are Credit Card Points Worth the Investment?

The 5 Worst Credit Cards You Absolutely Should Not Get

The Bilt Card

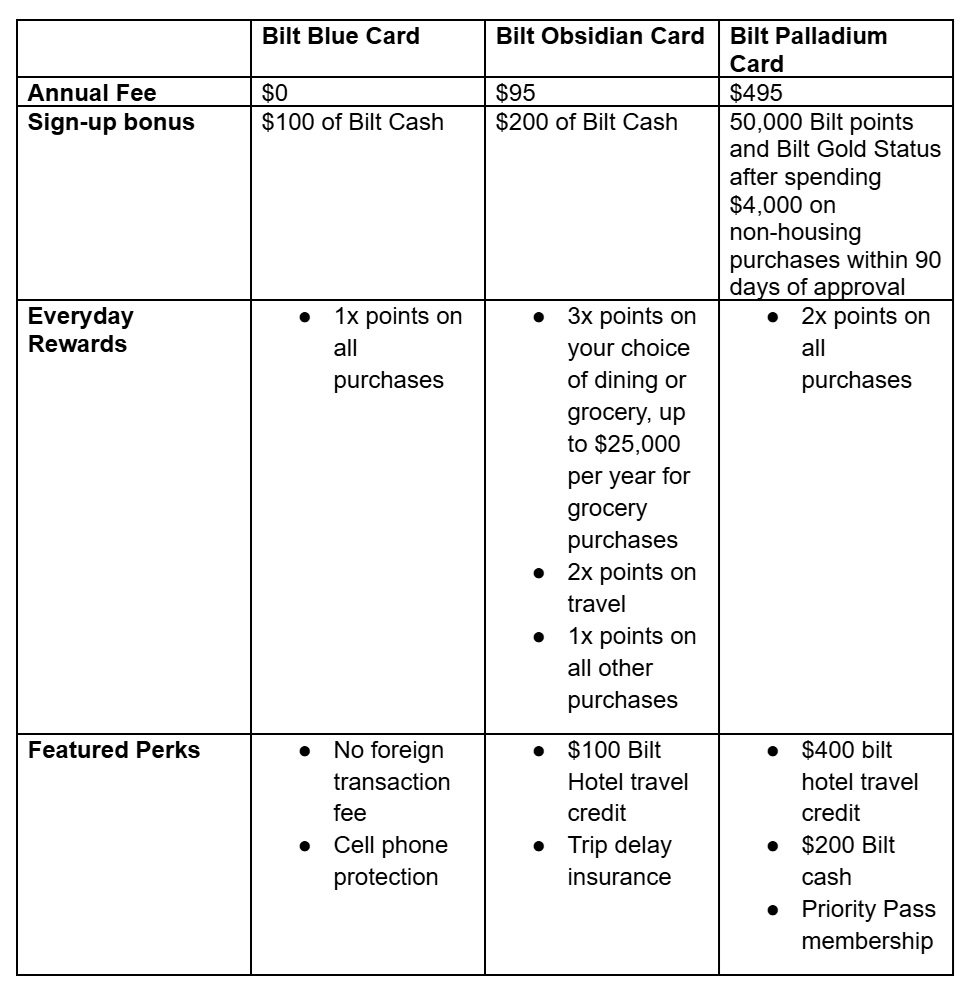

The Bilt Card, which is designed for paying your mortgage or rent directly, recently rolled out an update to its offerings, giving consumers three cards from which to choose:

- Bilt Blue Card: No annual fee and basic features

- Bilt Obsidian Card: $95 annual fee with better rewards and perks

- Bilt Palladium Card: $495 with top-tier rewards and greater travel-related perks

All three cards are focused on people who want a card they can use to pay for their rent or mortgage, offering no transaction fees on housing payments. This table compares the three cards.

Bilt Bonus Reward Options

Regardless of which card you select, when you open an account, you will choose one of two bonus rewards options that apply in addition to the everyday rewards you can earn: Housing-Only or Flexible Bilt Cash.

With the Housing-Only option, you earn Bilt points on all housing payments at a rate between 0x-1.25x points per dollar spent, depending on how much you also spend on non-housing payments using the card. The more you spend relative to your housing payment, the higher the multiplier. To earn the maximum rewards, you must spend at least as much as your monthly housing payment on everyday purchases with the card.

You can redeem Bilt points for statement credits against your card’s balance once you’ve earned a minimum of 1,000 points.

With the Flexible Bilt Cash option, you earn 4% in Bilt Cash on all non-housing purchases made with the card. You can use that cash to unlock Bilt points earnings from housing payments at up to 1x points per dollar spent, or you can redeem the cash for other Bilt benefits.

Redemption options for Bilt Cash include credits for Lyft, Walgreens, Grubhub, Priority Pass guest passes, or hotel bookings. Importantly, you cannot use Bilt Cash for a credit against your card’s balance.

There’s no hiding that this rewards structure is complicated. In some ways, it can feel like it defeats the point of getting a card to pay for housing costs.

To get the best possible rewards from using your Bilt card on your rent or mortgage, you have to use the card on everyday purchases, potentially earning fewer rewards than you’d get from other credit cards. That means that Bilt’s offering most appeals to heavy-duty optimizers who can track their spending closely and ensure they get the most value possible.

Risks of Paying Your Mortgage or Rent with a Credit Card

Paying your rent or mortgage with a credit card is not risk-free. There are some downsides that you should keep in mind.

For one, many of the options that let you use your credit card to pay your rent or mortgage charge a fee for the service. That fee may exceed the rewards you can expect to earn, so it could make it not worth doing.

Even if you use a card designed for paying your rent or mortgage and don’t have to pay a fee, risks exist. In general, credit card interest rates are much higher than mortgage interest rates. In effect, you’re refinancing low-cost mortgage debt into high-cost credit card debt.

You need to be certain that you can pay your credit card bill in full before you decide to use it to pay your rent or mortgage.

More information here:

From Wedding Planning to Owning 16 Credit Cards

Travel Hacking for Students, Residents, and Those Entering the World of Credit Card Rewards

The Bottom Line

Rewards credit cards can help you save hundreds or thousands of dollars each year, but many people struggle to use them to get rewarded for their biggest monthly expense—their rent or mortgage payment.

These days, Bilt is the biggest player in this space, and its offerings are a bit complicated. If you’re willing to do the work to optimize your spending, you may find that the card can offer solid value. If you’re not ready to put in that effort or you simply want to keep your financial life a bit less complicated, you’ll likely want to pass on this idea.

The White Coat Investor is filled with posts like this, whether it’s increasing your financial literacy, showing you the best strategies on your path to financial success, or discussing the topic of mental wellness. To discover just how much The White Coat Investor can help you in your financial journey, start here to read some of our most popular posts and to see everything else WCI has to offer. And make sure to sign up for our newsletters to keep up with our newest content.