By TJ Porter, WCI Contributor

By TJ Porter, WCI ContributorWith so many different financial products and account types out there, it can be difficult to figure out the best way to manage your money. Many doctors are looking for the most effective way to protect their families and save for their goals. Two key financial products for accomplishing those goals are life insurance and 529 accounts. Let's compare and contrast these two components of finance.

What Is Life Insurance?

Life insurance is an insurance product that is designed to protect your loved ones from the worst-case scenario. In exchange for paying monthly premiums to an insurer, the insurance company promises to make a payment to your named beneficiaries when you die. Your beneficiaries can use the benefit they receive for anything from covering funeral costs to replacing your income and paying for living expenses.

There are many different types of life insurance out there, but policies tend to fall into two basic camps.

Term life insurance policies last for a set period of time, called the term. During the term of the policy, you pay a monthly premium. As long as you keep paying the premium, you’re covered throughout the term. At the end of the term, you stop paying premiums, and you are no longer insured.

Whole life insurance policies last for your entire life. You pay premiums throughout your life, and as long as you keep paying those premiums, your insurance never expires. Whole life premiums are typically larger, but the policy also accrues a cash value. You can typically borrow against the value of your insurance coverage, and there can be tax advantages. For example, the cash value of your insurance can grow over time, and any loans you take against its value are tax-free.

More information here:

Term Life Insurance Strategies for Physicians

Should You Keep Whole Life Insurance Policy and How to Cancel

What Is a 529?

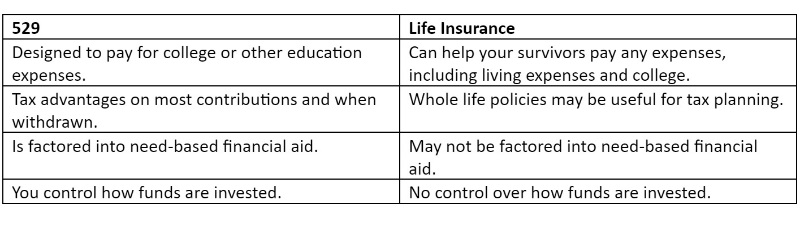

Where life insurance is a financial product, a 529 is a type of investment account. 529s are education-focused accounts. When you put money into a 529, you’re earmarking it to be used to pay for educational expenses—such as private elementary and high school tuition, trade school, or college costs.

529s are state-sponsored accounts, but they offer both state and federal tax incentives. What those incentives are will depend on where you live.

On the state level, you can typically deduct contributions made to 529s from your income when you file your taxes. The amount you can deduct varies. For example, Illinois lets you deduct up to $10,000 ($20,000 if filing jointly) while Massachusetts only lets you deduct $1,000 ($2,000 when filing jointly). Other states offer credits rather than deductions.

On the federal level, you don’t get a tax break when contributing to a 529 account. However, money in the account grows tax-free, and it is not taxed when withdrawn if it’s used for qualifying expenses. Non-qualifying withdrawals are taxed and subject to a 10% penalty.

Why Compare Life Insurance and 529s at All?

Life insurance and 529 accounts are very different things, so it’s natural to wonder why you’d compare them in the first place. The answer is that they’re both useful tools for people who want to provide and care for their families.

However, each is designed for a very different purpose. 529 accounts are intended for helping your children pay for their education while life insurance is designed to help your loved ones replace your income or cover final expenses after you die. Still, in a pinch, a whole life policy may also be used to help pay for educational costs.

What’s Right for You?

If you want to provide for your family, you may be tempted to consider buying a whole life insurance policy and using its cash value to help pay for your children’s tuition. After all, if you take a loan from your insurance policy, you can just pay it back and still have coverage that will provide a benefit to your heirs when you’re gone. However, the key thing to remember is that life insurance and 529s are designed for very different purposes, and the one you choose should be based on your goals.

While you can use the cash value of whole life insurance to help pay for college costs, it is far less efficient than using a 529 account. 529s offer far more control over how the money is invested, more flexibility, and tax incentives specifically designed for paying for education.

As a plus, if you overcontribute to a 529, it’s easy to resolve that problem. You can change the beneficiary of the account, helping another child or relative pay for education costs. You could also roll over up to $35,000 from the 529 into a Roth IRA, giving your child a jumpstart on saving for retirement.

Similarly, while the balance of a 529 could help your family cover living costs should you die, the account isn’t designed for that. The amount you save in a 529 is likely to be significantly less than the amount of life insurance you could purchase for a reasonable price. You’ll also have to deal with tax penalties for non-qualifying withdrawals.

In the end, term life insurance instead of whole life insurance is a much better way to protect your income, and while whole life insurance might have some estate planning features that can be useful, the vast majority of people, including doctors, don't need those features.

You should choose a 529 if you’re trying to help someone pay for educational costs and life insurance if you’re trying to protect your family should you die. Of course, if you want to do both, there’s nothing stopping you from buying a life insurance policy and setting up a 529 for your child.

More information here:

Despite Our Student Loan Debt, Here’s How We’re Filling Our Kids’ 529s

Is Whole Life Insurance a Scam?

The Bottom Line

While 529 accounts and life insurance are financial tools designed to help people care for their loved ones, they are very different things that should be used for very different purposes. Given that each is designed for a different reason, consider your goals to help figure out which you should use (or if you should just use both).

The White Coat Investor is filled with posts like this, whether it’s increasing your financial literacy, showing you the best strategies on your path to financial success, or discussing the topic of mental wellness. To discover just how much The White Coat Investor can help you in your financial journey, start here to read some of our most popular posts and to see everything else WCI has to offer. And make sure to sign up for our newsletters to keep up with our newest content.