I know a lot of people have trouble wrapping their minds around investing, retirement accounts, and the tax code, but I was appalled to see a pair of tweets recently. It wasn't that the idea behind the tweets was unusual (although obviously wrong), it was that they were made by a Certified Financial Planner (CFP) with an MBA who describes himself as a “wealth manager” and per his ADV2 has 250 clients and $80M under management. The tweets were in response to another advisor who was (correctly) surprised to learn how many investors had started a taxable account before even maxing out their retirement accounts. Here are the tweets:

I blanked out the advisors' names because I wanted to focus my post today on the arguments, not the people. But if you find yourself getting advice from an advisor making this argument, you should probably fire them. Let's list all the things that are wrong in just two short tweets:

- “Pay less taxes over your lifetime”—Not even close to true and easily debunked.

- “Have more flexibility”—True in some ways, but not worth it. Real flexibility comes from having much more money.

- “Have an asset to leverage for other wealth building”—Somewhat true but misleading.

- “The RMD trap”—Dramatically overblown, but even if you have an “RMD problem”, preferentially using a taxable account isn't the right move.

- “Forced to retire later”—Nobody is ever forced to retire later. They usually make that choice themselves.

I am appalled that I need to write a post defending retirement accounts. The advantages here are so obvious to me that I would expect these sorts of arguments to be made by a beginning investor, not someone who is managing $80M for 250 people. I'm actually feeling really badly for those 250 people right now because I suspect that at least some of the advice they have been given over the years is bad advice. At any rate, let's dissect each of these arguments for a few minutes.

#1 Retirement Accounts Allow You to Pay Less in Taxes

The first argument here is the weakest and the only possible conclusion I can draw here is that the advisor mistakenly compared apples to oranges. If you compare apples to apples, this isn't even close. If you preferentially invest in retirement accounts, you will pay less in taxes over your lifetime and have more money to spend, give, or leave to heirs. How much less? Well, take a look at James Lange's chart from his book Retire Secure (which comes from very reasonable assumptions):

The bottom line is that if you use a retirement account, your money grows faster in the accumulation stage and lasts longer in the distribution stage than if you simply invested in a taxable account.

The main reason for this is that in a retirement account, the money is not taxed as it grows. Distributions of dividends, interest, and capital gains are not taxed each year. If you sell something with a gain, that isn't taxed either. Avoiding this “tax drag” allows the money to grow faster. Even a very tax-efficient investment like a total market index fund will grow about 0.3-0.5% per year faster inside a retirement account.

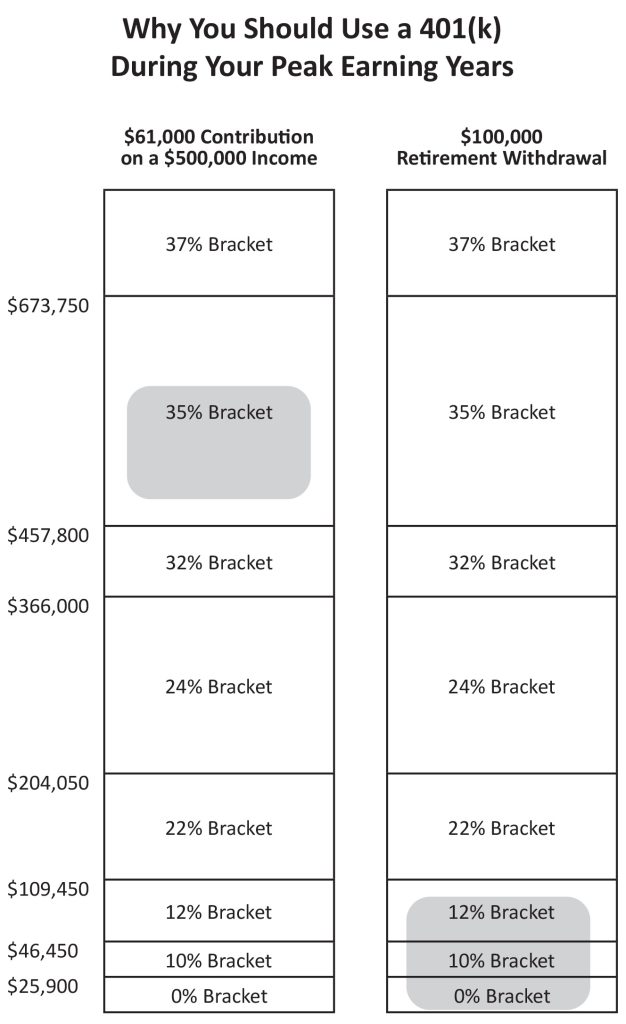

In addition to this effect, for most investors there is an “arbitrage” of tax rates between your peak earnings years and when you pull the money out of the account later. When you put the money into a tax-deferred account, you save taxes at your marginal tax rate. As you pull money out later, you get to use it to fill the brackets. See the chart below to understand how this works:

Using 2022 Tax Brackets

Saving money at 35% and then paying at 0%, 10%, 12%…heck, even 22%, 24%, and 32%, is a winning combination. You can take A LOT of money out of a retirement account in retirement before you're paying 35% on any of it. In a tax-free (i.e., Roth account), you don't get this arbitrage, but at least you get to avoid the tax drag inherent in a taxable account.

So how could an advisor possibly get this wrong? Well, the only way I can think of is that the advisor mistakenly put the same amount of money into a taxable account as an IRA and then ran out the numbers and concluded that because IRA withdrawals are taxed at ordinary income tax rates instead of the lower qualified dividend/long term capital gains rates that one would pay less tax on the taxable account. But the problem is that $10K in an IRA is not the equivalent of $10K in a taxable account. If you are in the 35% tax bracket, $10K in an IRA is the equivalent of $6,500 in a taxable account.

So let's run the numbers. We'll assume a 0.5% tax drag on the taxable account and we'll assume an average 15% tax rate on withdrawal of the IRA. We'll assume an 8% pre-tax return and a contribution of $10K (pre-tax) per year for 30 years.

IRA

= FV(8%,30,-10000) = $1,132,832.11

Then, although this obviously isn't going to happen, let's just take it all out at once at a 15% tax rate. Note that this simplifying assumption makes the taxable account look better than it otherwise would. As noted in Lange's chart above, in reality, the avoidance of tax drag in the distribution phase has an even larger effect than during the accumulation phase.

$1,132,832.11 * 85% = $962,907.29

Taxable

= FV(7.5%,30,-6500) = $672,096.12

Let's assume a 15% capital gains rate on the gains and again assume you sell it all on the eve of retirement for some bizarre reason, just to keep things equal for comparison sake.

($672,096.12 – ($6500*30)) * 85% +($6500*30) = $600,531.70

As you can see, you end up with over 60% more money by using the retirement account. Even if assumptions are off a bit, this isn't even close. The retirement account is clearly better, all else being equal.

In the minority of situations where this might not be the case (due to reverse arbitrage), the solution is using Roth contributions and conversions, not using a taxable account.

#2 More Money Creates More Flexibility

While it is true that money in a taxable account has more flexibility than an equal amount of money in a retirement account, real flexibility in your life generally comes from having more money. Worst case scenario, you pull the money out of the retirement account and pay taxes and the 10% early withdrawal penalty. As you can see from the example above, you STILL come out ahead using the retirement account. And since that scenario is very unlikely, this is simply a non-issue.

Some people complain that there are assets they can't invest in inside their retirement accounts. Ignoring the fact that most of those investments probably shouldn't be in your portfolio anyway, there are also self-directed IRAs and individual 401(k)s that you can invest in almost anything. Even many standard 401(k)s have brokerage windows that provide immense flexibility in investment choice. But even if you're “stuck” in an employer's 401(k) with unappetizing investments, you likely aren't stuck there long. The average job tenure these days is between 4 and 5 years. If your investing career is 60 years (30 while working and 30 in retirement), being without your favored investment for 5 years doesn't seem like a big deal.

Speaking of flexibility, one place where retirement accounts are more flexible than taxable accounts is when you change investment strategy or need to rebalance. There is no tax cost to doing this in a retirement account, but there is in a taxable account.

#3 Leverage Isn't Worth Skipping a Retirement Account

The third argument was that you can use more leverage outside of retirement accounts. It is true that you can't invest on margin in an IRA or 401(k). You'll need a taxable account to do that. Of course, you probably shouldn't do that, and I hope you don't need to do that to reach your goals. However, it is not true that you cannot use leverage in a retirement account. You certainly can buy a leveraged rental property inside a self-directed IRA, although you would have to pay Unrelated Business Income Tax (UBIT). If you use a self-directed individual 401(k), you don't even have to do that.

Obviously, if you have an investment that is going to make you 30% and you can only buy it in a taxable account, then that sort of return is going to overcome the benefits of a retirement account. But you might be surprised just how much better the investment has to be in order to overcome the tax benefits inherent in a retirement account.

Let's take the numbers from above, just for simplicity's sake. As you'll recall, we assumed 8% pre-tax returns there and ended up with $962K vs. $600K. How much higher would the return on the investment in the taxable account have to be in order for you to finish with $962K? Well, it depends on the tax-efficiency of the investment, but let's assume it is pretty tax-efficient and the tax drag is only 0.5% a year. If that were the case, you would need a pre-tax return of 10.8% instead of 8%.

#4 The Solution to an RMD Trap Is Roth Conversions, Not Skipping Retirement Accounts

First, as I've written before, very few people, including high earners like doctors, will have an “RMD Trap.” It's either a scare tactic used by those with something to sell you or a simple display of ignorance.

Second, if you are one of those few, the solution is not to invest preferentially in a taxable account. It is to do Roth contributions and conversions. Roth IRAs not only do not have Required Minimum Distributions (RMDs), but there is no tax cost to pulling money out of the account anyway.

Third, RMD law seems to keep getting more and more lenient. For example, you no longer have to take RMDs before Age 72 and they were completely waived in 2020.

Concerns about RMDs are NOT a reason to avoid using retirement accounts.

#5 Nobody Is Forced to Retire Later

There are probably lots of people who wait until age 59 1/2 to retire so they don't have to worry at all about the 10% penalty on retirement accounts if you withdraw money prior to age 59 1/2. Just like there are lots of people who wait until they are 65 to retire so they can qualify for Medicare. But neither of these are a requirement to retire. In the case of the “Medicare waiters”, the solution is simply to have enough money to be able to afford to buy health care on your own, at least for those years between retirement and 65 (although as any retiree will tell you, the “free” part of Medicare is not going to cover all your health care needs anyway). In the case of the “Age 59 1/2 waiters”, these early retirees often simply don't understand all the exceptions to the age 59 1/2 rule.

First, if the money is in a 401(k) and you separated from the employer, you can often tap it as soon as you are 55.

Second, there are lots of exceptions to the rule that allow you to avoid the penalty—a first house (for you or a family member), disability, death, health expenses, medical insurance/expenses, IRS levy, and higher education expenses.

Third, the biggest exception to the Age 59 1/2 rule is the Substantially Equal Periodic Payments (SEPP) rule. Basically, early retirement is an exception to the Age 59 1/2 rule. Sure, a 55-year-old can only pull out about 2.4% a year without paying the 10% penalty, but that penalty only applies to the amount above 2.4%.

Mostly, however, it simply doesn't make any sense that someone would have enough money in a taxable account to retire early but would not have had more than enough in retirement accounts to have done so, even if they had to pay a bit of a penalty to do so. And the truth of the matter is that most of those FIRE types are saving so much money each year they couldn't stuff it all into retirement accounts anyway and so they end up with a large taxable account they can use first anyway.

People aren't forced to retire later because they used retirement accounts. They are forced to retire later because they didn't save enough money. If anything, the use of a retirement account HELPED them to retire earlier, rather than preventing them from doing so.

Bonus Material

But wait! There's more. I think we've pretty much shown that investing preferentially in a taxable account is a bad idea already. But let's pile on a bit.

Asset Protection

In most states, 401(k) and IRA money receive significant asset protection from creditors. Taxable accounts generally receive none at all.

Estate Planning

You can name beneficiaries for retirement accounts, facilitating inexpensive and simple estate planning. Plus, IRAs and Roth IRAs can be stretched for 10 years by your heirs.

Roth Conversions

You can do Roth conversions in relatively low-income years, allowing YOU to choose when you pay the taxes on the money you earned during your life and at what rate you do so. Can't do that once you passed on a retirement account contribution in favor of a taxable one.

Get Your Match

And of course, make sure you get any possible employer match. That's part of your salary. Skipping that to invest in taxable is truly a colossal mistake.

Exceptions to the Rule

Now, there are always exceptions to any rule of thumb. Let's see if we can think of any to this rule.

#1 Awesome Investments

If you have access to an absolutely awesome investment and there is no way to stick it in a retirement account, it could be worth skipping a retirement account contribution in order to buy it. For example, my investments into my partner blogs like Physician on FIRE, Passive Income MD, and The Physician Philosopher have had spectacular rates of return, but it would not have been practical to buy those in my retirement accounts. If you have investments like that available to you, hopefully you, like me, are saving enough that you'd be able to max out your retirement account and still buy this investment, but if you can't, then that's certainly an exception.

#2 Equity Real Estate

Despite the fact that you can put an equity real estate investment into a self-directed IRA (or better yet, a self-directed individual 401(k)), you may not be dramatically better off by doing so. Most of the income is often sheltered by depreciation, you can't use the property yourself, and if you do exchanges well, you may never end up having that depreciation recaptured. Plus it makes leverage easier to use. Again, like the exception above, hopefully, you can max out your retirement accounts AND still make this investment, but if not, perhaps it could be justified.

#3 Money You Know You'll Need Well Before 59 1/2

If there is money you are going to need to spend in your 30s or even 40s, then the SEPP rule becomes pretty unwieldy. Same thing for short term money, like next year's tax bill or a down payment you'll need in a few years. Keep that out of your retirement accounts (and out of long-term investments for that matter). But again, if you'er retiring super early, you probably have 457s or a sizable taxable account and can wait to tap the retirement accounts.

So there you have it. While there are few absolutes, skipping tax-protected/asset-protected contributions in favor of unprotected, taxable account is usually a mistake.

What do you think? Under what circumstances would you or have you skipped a retirement account contribution to invest elsewhere?