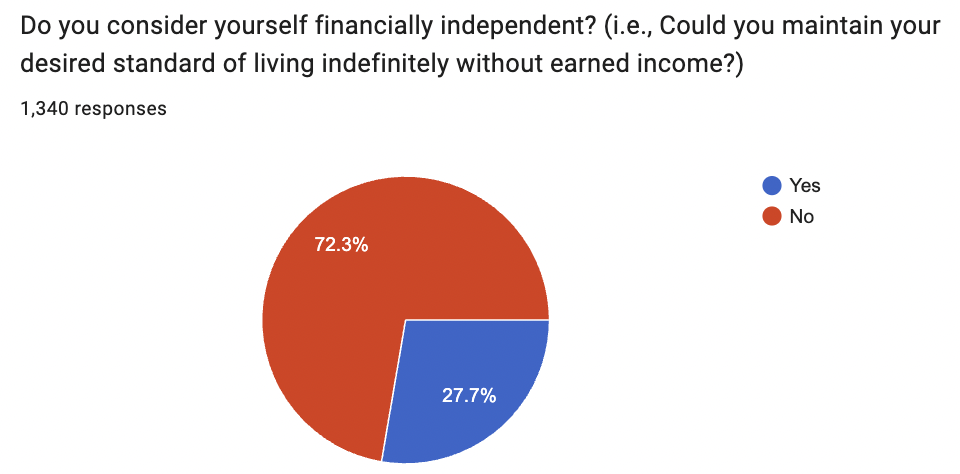

When it comes to FIRE (Financial Independence Retire Early), most people want FI but only some of them want RE. Results from the 2026 WCI Survey were illuminating:

Twenty-eight percent of WCIers are financially independent (up from 22% last year, by the way), but . . .

. . . only 11% (up from 8% last year) of you are retired. That leaves 17% of you in my shoes—financially independent but still working. This post is for you. (The rest of you can either read with anticipation of hitting FI someday or, if you're retired, just sit back and shake your head at us for still working.)

The First Thing That Happens (You Spend More)

The first thing that happens to most people who hit FI but don't hate their jobs is that they wonder if they could actually use some more money. Their spending usually goes up. When setting an FI number as a young accumulator, most people aim for a minimum number, i.e., an amount that they could be “happy” and “never run out of money” if they spend like they do now. But when you hit FI and don't hate your job, you start looking around. You wonder what it would be like to fly first class. You wonder what it would be like to get a new car every few years. You wonder what it would be like to give a little more each year to your favorite charity, send your kid to a more expensive college, renovate the house, buy a second house, or vacation a little more.

In short, your FI number goes up because your desired spending goes up—$1.5 million becomes $2 million, $3 million becomes $5 million, and $5 million becomes $8 million in short order. Be prepared for this and recognize that “it's OK, because I still like what I do and I'm not ready to retire.” You can still tell people you're FI, and you are. But recognize the difference between “Happy FI” and “I seriously can't think of anything else to spend money on that would make me any happier FI.” Let's call that “Truly FI.”

More information here:- 8 Things to Do with Financial Independence Besides Retire Early

- Financial Independence Is Not the Holy Grail

Why Do Truly FI People Still Work?

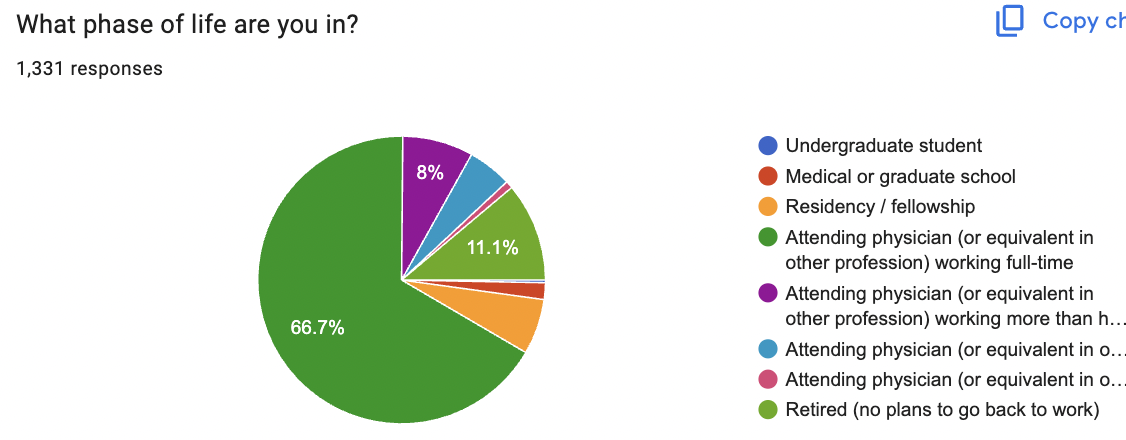

Let's assume you're now truly FI, but again, you still see work as an important part of your life. There are plenty of reasons for this, and I suspect that more than one of these reasons applies to each member of that 14% of FI WCIers who still work.

- Lifestyle inflation (sometimes you just have to try first class or bottle service or NetJets or a new pontoon boat or whatever to see if it makes you any happier).

- Legacy goals (“generational wealth” or charitable goals).

- You've tried not working and didn't like it.

- You're happier when you do at least some work.

- A large part of your net worth is tied up in an illiquid business that has not yet been sold.

- Work provides you with a sense of purpose.

- Work provides structure to your day.

- Someone else's income, health, or happiness depends on you working.

- You just need to get out of the house every now and then.

- Your work is more fulfilling and does more good for the world than the volunteer work you've looked at or done before.

- Work isn't keeping you from doing anything else you want to do.

- Anxiety still makes you worry about running out of money.

- Seeing your investment balances fall provokes anxiety after decades of watching them rise.

- It is so easy to make a lot of money that it seems a shame not to do so.

- Additional income/wealth allows you to support more people that you don't HAVE to support but would like to.

- Making more money is an enjoyable game for you, where score is kept with net worth.

- Pure inertia. It takes effort to change.

- You feel like you're better at your job than your patients' alternatives.

- Maintain connections with a network of medical professionals just as you are about to start to require their services.

- Ignorance. You don't actually know you are FI.

- Religious beliefs regarding the importance or virtue of work.

- Role modeling for children (You don't want them to see you not working or they will think they should not work).

- Worry that you do not have anything to retire to.

- Difficult or challenging relationship at home that work helps you to avoid.

- Back-loaded golden handcuffs (pension?) of some kind that you cannot stand to throw away.

- Worry about retirement leading to mental decline.

If you can think of any more, mention them in the comments, and I'll add them to the list.

What Should You Do with Your Investments?

As you become wealthier, more investments become available to you. That doesn't mean you have to invest in them. I assure you that you can put $10 million into VTI just as easily as you can put $1 million or $100,00o or $10,000 into it. It works just the same. But you can at least consider investments that require you to have accredited investor, qualified client, or qualified purchaser status. These are generally private but passive investments in real estate, oil/gas, or private equity.

Some people change their asset allocation to something more conservative. They figure, “Why keep playing the game when I've already won it?” They don't see a reason to take a bunch of risk to make money they don't need to buy stuff they don't want to impress people they don't even care about. Their need to take risk has decreased. Others note their increased ability to take risk. “I can go 100% stock because even if my stock drops 80% in value, I'm still OK.” Others take a set amount of money off the table, such as $2 million or $5 million or whatever, and dump that into very safe investments, and then they take on more risk with whatever is left.

We could never decide how our lower need to take risk interacted with our increased ability to take risk, and we figured 20% of our portfolio in safe investments (as we've always had) was a reasonable amount. So, we just kept the same asset allocation we had before we were FI.

What Should You Do with Your Earnings?

One of the fun things about being FI and still working is that every year you've got a big chunk of change (your earned income), and you can do whatever you want with it. You can spend it frivolously, although it's probably best to spend it on one-time expenses so you don't increase your FI number (25 times or so your annual spending) anymore. You can become ridiculously generous by giving it away to family, friends, charities, political parties, or whoever you like. You can sock it away for future generations or just to see the number on your computer screen get bigger so you can die the richest investor in the graveyard, too. It's really up to you.

Just be aware that continuing to work absolutely will increase your tax bill, so you'd best be OK with that. Some people, FI or not, become so frustrated with paying taxes that they (mistakenly) set a goal to lower their tax bill rather than increase the amount left after paying taxes.

I would submit that the right answer to this question is probably a combination of the above. Spend some, give some, put some away to spend or give later, and be happy to have to pay a bunch of it in taxes.

How Should Work Change?

Since you're now working for non-financial reasons, your primary purpose for working needs to become less and less financial every year. Stop doing stuff you don't like doing, don't see any purpose in doing, or don't want to do for whatever reason. At this point, my health is a bigger priority to me than making more money, so I try not to let work ever get in the way of workouts, eating well, or doctor appointments. At this point, spending time with family or doing things I enjoy is more important to me than making more money, so I try not to let work get in the way of events I want to attend or trips I want to take. Nobody is perfect in this regard, and I even still work my (small) share of weekends and holidays in the ED.

Stop doing procedures you don't like. Stop serving on committees where you don't want to be. Stop working with people with whom you don't want to work. Stop taking call. Stop working nights, weekends, or holidays. Tell the boss what you really think of him or her. The less you care about not having that work anymore, the more freedom you will experience and the happier you are likely to be at work.

More information here:How Do You Know When to Retire?

I wish I knew the answer to this question. I've been struggling with it every year for the last eight years. At times, I dread knowing I'll have to wake up early the next morning to go into the ED, and I wonder, “Why am I doing this?” But by the next afternoon, I'm glad I did. Mostly, I could just use a little more free time because I've packed so much other fun stuff into my life. There are a few other considerations, however.

Leave on Top

We all know a doc who should have retired already. Often, they're still working for financial reasons, but not always. Sometimes it's just inertia. Or they seriously can't find anything else they like to do. Or it's an identity thing. But I think it's probably best to retire BEFORE your skills and knowledge tank. I'm currently practicing medicine at 40% time, or 0.4 FTE. I often caution new grads not to work part-time for a while, although I think it's a great option after two, five, or 10 years, once your skills have solidified.

But how long can one work at half-time, quarter-time, or less and still be a competent doctor? I don't know, but I worry that after some period of time (five, 10, 20 years?), patients may deserve better. Someone doing 0.25 FTE is just not going to be as good as someone doing 1.0 FTE for the last 10 years. Our group decided long ago that the minimum number of shifts for a partner is six a month, and I'm into my sixth year doing just that. As much as I like it, I want to make sure I punch out before hurting anyone.

Identity

Most of us spent more than a decade learning and training to become a doctor. It's a big part of who we are. Leaving medicine means giving that up. That means new identities must become at least as important as the old ones. Yes, you'll always be a doctor, even if you're no longer practicing.

Paycheck Addiction

Some people are addicted to income. Whether it's people who “never spend principal,” dividend-focused investors, or people who just have an easier time spending a paycheck, it's very real. But you have to get over it if you want to retire.

Social Acceptance

It's socially acceptable to retire in your 50s. Not so much in your 40s. Go ahead, try it. Tell people you're retired and check out the look they give you. Not working in your 40s = unemployed, not retired, no matter how much money you have.

Sell the Business

Sometimes retiring is harder than it looks. Imagine half (or more) of your net worth is tied up in a business that is hard to sell. Or it simply would sell at such a low multiple that it seems better to own it until you die. It's not just about flipping off your boss and walking out the door. Now, a major hurdle/barrier to retiring exists that requires plenty of work that you might not even feel like doing.

Don't Leave People You Care About Hanging

Another factor that can affect both business owners and employees is that other people may depend on you still working for their livelihood. Perhaps if you retire, your MA gets fired. Or perhaps you have more than a dozen people working for you, like we do here at WCI. Those aren't the only people depending on your work either. Clients or patients matter. I've run into many doctors (often very subspecialized or in rural locations) who have told me they would retire but they just can't abandon their patients and look themselves in the mirror.

What Is Your Purpose in Life?

There's more to life than just recreation. Being good is one thing, but you should probably also be good for something. All work and no play isn't a recipe for a happy life, but neither is all play and no work. How many hours a week of video games, TV, golf, or beer-brewing can you really handle without feeling worthless? When I look around at what I do as a volunteer, it seems like my paid work is doing the world a whole lot more good. It's like people who tell me they volunteer at the local food bank. I'm a big fan of the food bank, but I'm pretty sure I'm doing a lot more good donating thousands of dollars there every year than I am passing out the food.

As you can see, I have no idea how to know when it's time to retire. I've asked every one of my retired partners this question over the years. They always tell me they just knew and none of them has yet regretted it. Hopefully, I will “just know” when the time is right as well.

Financial independence is wonderful, but a space often exists between FI and RE. Use it well, and don't be surprised if you wallow in some existential dilemmas like I have.

What do you think? Do you plan to RE as soon as you FI? If not, what do you expect those years to look like? If you are FI and still working, what in this post resonates most with you?