Sometimes, investing hobbyists like myself, especially after a decade or more of investing, assume everybody knows the basics of investing. Occasionally, I am starkly reminded that this is not the case. I refer to these somewhat egregious errors as “violating Investing 101.” Today, I'd like to go on record about what I think everyone should have learned in Investing 101.

Don't Buy Investments You Don't Understand

This one seems so obvious when you say it like that, but it is an incredibly common thing that people do.

“I didn't know that investment could do that.”

“I didn't know there was a surrender fee.”

“I didn't really understand how that worked.”

“I didn't understand the tax consequences of that investment.”

Every day, I run into somebody who has purchased something they didn't understand, and it isn't always whole life insurance.

Limit Speculation with Your Investments

Investments that don't generate income are speculative, and they should make up a very limited, if any at all, part of your portfolio. The classic speculative investment is empty land. You know, a real estate investment that doesn't provide any income and actually has expenses, like insurance and property taxes. Gold, Bitcoin, and Beanie Babies are also speculative.

If you want to put some small part of your portfolio (<10%) into stuff like that, that's probably fine. But I don't put any of my portfolio into speculation. That's serious money I carved out of my income and didn't spend. I'm not going to just play with it. I've got hobbies that are way more fun than that.

More information here:- Should Doctors Consider Angel Investing? The Other 5% of Your Money

- The Emotions Behind Short-Term Trading: The Other 5% of Your Money

Higher Investment Risk Is a Necessary But Not Sufficient Condition for Higher Returns

You have probably heard the old adage that higher risk = higher returns. While there may be a correlation there, it isn't always true. Some risk isn't compensated. Plenty of risky investments have low, zero, or even negative expected returns. Don't buy those. Think roulette. It's high risk, right? There must be a high return, right? No. The expected return is negative on roulette. That's why it's in a casino. Casinos don't have games with positive expected returns.

Diversify Your Investment Portfolio

Another obvious one, right? But people don't diversify. I had someone complain a few years ago that their $100,000 crowdfunded hard-money loan was in foreclosure. That's a known risk of hard-money loans, and some percentage of them will go into foreclosure. But crowdfunding sites generally only require you to invest $2,000-$5,000 into debt investments. Why would someone put $100,000 into a single one? I guess if you had $3 million in crowdfunded hard-money loans, then maybe it's not a big deal. But if you only had $100,000-$200,000? To put 50%-100% of your investment into a single security? You just failed Investing 101.

It's so easy to buy all the stocks in the world at a cost of four basis points a year. There's no reason to have a portfolio consisting of a handful of stocks. We call that uncompensated risk, and nobody is going to pay you for it.

Think about two schools of investing. One is to not put all your eggs in one basket. The other is to put all your eggs in one basket and watch that basket very closely. But watching it closely means you need to be on the board of the company. The person in charge of whether your investment is successful should probably have been a guest at your dinner table if you're investing more than 10% of your portfolio in that company. I've got more than 10% of my net worth tied up in WCI, LLC. Is that risky? Sure. Am I watching that investment closely? More closely than anyone else in the world. That's the sort of watching you need to be doing to bear concentrated risk, and even then, it might not be a good idea.

Invest When You Get the Money

Timing the market is hard. It's so hard that I'm confident far more money has been lost trying to time it than has been made successfully timing it. Obviously, buying low and selling high is ideal. But it's incredibly hard. The next best thing—buying all the time—is very easy. Successful investors buy all the time. You earn money at your job, you carve out a portion of it to invest, and you invest it. Right then. If you happened to buy high? No big deal. Because you did the same thing last month, last year, and the last decade. And you'll do the same thing next month, next year, and next decade.

Eventually, you'll have bought both low and high, and in the long run, you'll be rich. Time in the market matters more than timing the market. Some people advocate a “Dollar-Cost Average” (DCA) approach to investing a lump sum. But guess what? Every day you leave your money invested, it is just like you lump-summed in that day. So you might as well just invest any lump sum you happen to have right now. If you're nervous to put your lump sum in the market all at once, how is that any different from the day after you finish your one-month, six-month, or one-year carefully calculated DCA process? It isn't. Just invest.

More information here:- I Have $150,000; Should I Be Nervous About Lump Sum Investing It When the Stock Market Is at an All-Time High?

- What to Do with a $900,000 Lump Sum of Money

If You Must, Be a Contrarian

Some people just can't put it on autopilot; they can't resist timing the market. Well, if you must time the market, try to do the opposite of what the crowd is doing. Don't buy something right after it went up 1,800% in the last year. Don't sell something because it just went down 75%. Do the opposite. It won't feel right, but in the end, it's far more likely to be right.

Don't Catch a Falling Knife

While we're on that subject, remember that just because something went down a whole bunch, that doesn't mean it will go back up any time soon, and vice versa. There is a certain amount of momentum in investing, but it's awfully hard to get it right. See the above section about “investing when you get the money.” It's wonderful to own a good investment, but the difference between a good investment and a bad investment is often just the price you pay for it. Would you like to buy a nice property with a great tenant that has a net operating income of $8,000 per year? Sure, if it costs $100,000 but not so much if it costs $300,000.

Past Performance Does Not Guarantee Future Performance

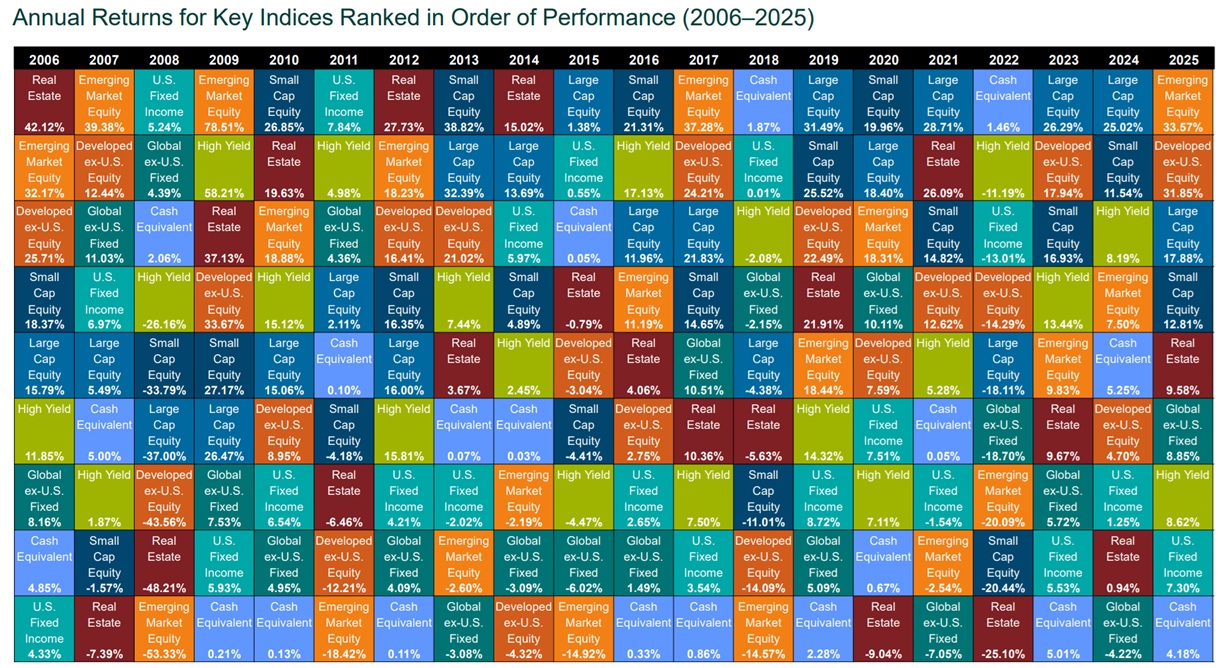

Your natural tendency as a human being is to look at what did well in the past and buy it. When it comes to picking stocks, mutual funds, or asset classes, that is usually a recipe for underperformance. This is such a truism that mutual funds are required by law to put it in their paperwork. In fact, there is a phenomenon often called “mean reversion,” which suggests that asset classes that have done poorly in the recent past are likely to do better in the near future. You can really see that at play with this chart, called the Callan Periodic Table of Investment Returns.

Spend a second with this, because it's important (you can click on the image to expand it). Basically, each color is an asset class represented by a given market index. Notice that how it did one year really has nothing to do with how it did the next year compared to other asset classes. Some asset classes are riskier than others. For example, the orange one is emerging market stocks, like companies in China and India. Note how it is often the top performer or the biggest loser (or sometimes, stuck in the exact middle).

The point is that you don't know what asset class is going to be on top next year, so buy them all. In a reasonable portfolio, every asset class will have its day in the sun and its night in the doghouse. But switching from one to another chasing performance is a good way to spend most nights in the doghouse.

Better Have a Good Reason Not to Use an Index Fund

The data supporting the use of passive investments, like low-cost index funds, instead of actively managed funds in the publicly traded stock and bond markets is so strong that you'd better have a darn good reason to choose an actively managed one. Good reasons include things like, “There is no index fund in this asset class” or “My 401(k) doesn't offer index funds,” not “I found an actively managed fund with a track record of beating the index fund for five years straight.” That happens just by chance and probably won't repeat.

More information here:Stop Playing When You've Won the Game

Investing is a single-player game. The object of the game is to reach your own investing goals. You don't need to beat the market or your brother-in-law or that guy at the water cooler. Ideally, you take on only enough risk to have the best possible chance to reach your goals and no more. If you receive some good fortune, such as strong returns or an inheritance, it might be smart to dial back the risk a bit.

Careful Adding New Asset Classes to Portfolio

If you're going to add a new asset class, make sure it has good returns and a low correlation with the rest of your portfolio. And make certain it's an intelligent investment on its own, not just when combined with the rest of the portfolio. Beware performance chasing.

I can look at a Boglehead's portfolio and pretty much tell you what year the owner joined that forum. A small value tilt? 2001-2005. A REIT tilt? 2005-2007. Three-fund portfolio? 2009-2015. Good investing books in the late '90s recommended a tech fund. I Bonds, TIPS, momentum funds, fundamental indexing, peer-to-peer loans, cryptocurrencies—they've all had their day in the sun. Don't kid yourself when adding new asset classes; you're probably performance chasing.

Rebalance Every Now and Then

Intermediate investors are fixated on rebalancing. They come up with mantras like, “It isn't buy and hold; it's buy, hold, and rebalance.” Rebalancing doesn't make that much of a difference, and it often hurts portfolio performance. For that reason, academic studies suggest rebalancing every 1-3 years is ideal. But never rebalancing is a rookie mistake. Investing 101 teaches that you should rebalance your portfolio every now and then.

There Are Many Roads to Establishing a Successful Investment Portfolio

I've met thousands of successful investors online and in real life. Not one of them followed the same exact path. What that tells me is that you need to pick something reasonable, fund it adequately, and stick with it. Don't get dogmatic about your own investing method or asset allocation. It's probably not much better than the next guy's portfolio and could be a little worse. The difference between 5% REITs and 10% REITs isn't going to have much of an effect on your retirement date, and no one can predict which allocation will hasten it and which will delay it.

Sometimes You Find a $20 Bill on the Ground; Pick It Up.

There's an old joke about an economist walking with one of his students who points out a $20 bill on the ground. The economist doesn't believe it. Well, every now and then, you actually do find a $20 bill lying on the ground. Pick it up. It won't be there for long.

A few times in your investing life (and more frequently in your business life), you'll run into this sort of situation. At first, you'll think it's a scam, but as you look into it, you'll realize it's almost free money. Take it. Maybe someone wants your house, boat, or car more than you do. Maybe it's a property being sold by a busy heir who doesn't know or care what it's worth. Who knows? But just like there are really bad deals out there, there are really good ones, too.

Stay the Course in Bull and Bear Markets

Beginner investors don't stay the course in a bear market. Intermediate investors don't stay the course in a bull market. Successful investors do both.

Don't Mix Investing and Insurance

Some products are made to be bought, but many are made to be sold. A large quantity of those are sold by insurance companies and their representatives. The agent will tell you it isn't an investment. Believe them, and walk away.

More information here:Use Retirement Investment Accounts

When given the choice, invest preferentially in tax-protected and asset-protected accounts. Hint: that choice is a lot more common than most people realize. An HSA is your best investing account. You can still use a Roth IRA after you start making the big bucks. You can have more than one 401(k). Don't fear the age 59 1/2 rule; there are lots of exceptions to it, including early retirement.

Don't Let the Tax Tail Wag the Investment Dog

Don't be so tax paranoid that you forget the goal isn't to pay the least amount possible in taxes. The goal is actually to have the most after paying them.

Costs Compound Just Like Returns

Cost matters, and it matters a lot, especially over long time periods. Every beginner investor knows about the magic of compound interest. Too few realize it also applies to all their costs. A 1% AUM fee really adds up over the decades.

The Majesty of Simplicity in Your Investment Portfolio

Simple, low-cost portfolios often beat complex, higher-cost portfolios, especially when you add in the cost of your time. Be cautious when adding complexity and cost to your portfolio. Like reaching for something that isn't an index fund, you'd better have a very good reason to do it.

The Investor Matters More Than the Investment

The most important determinant of your investing success is your own behavior. Are you saving enough? Can you stick with your investing plan? Can you limit yourself to a reasonable withdrawal rate in retirement? Can you avoid performance-chasing, greed, and fear? That all matters a whole lot more than a few basis points in fees or extra return.

There you go, Investing 101. Learn it from me or learn it in the school of hard knocks. But eventually, you will learn it.

What do you think? What else belongs in Investing 101?

[This updated post was originally published in 2018.]