Scroll the WCI social media channels, and you’ll see the same tax questions about disability insurance on repeat.

- “If I wait until December to deduct my disability insurance premiums, can I skip the write-off if I had a claim that year, so my benefits won’t be taxed?”

- “I’m a PLLC practice owner. Can I write off my DI premiums, and if I do, will the benefits be taxable?”

- “My employer pays for DI. Are those premiums pre-tax or after-tax, and does that change how my benefits are taxed?”

- “HR says the premium shows up as taxable income on my W-2. Does that make my benefits tax-free?”

All great questions, and they all point to one simple truth: Uncle Sam will get his piece of the pie eventually. And mixing employer pay, pre-tax payroll, and personal policies without a plan is how surprise tax bills happen.

In this post, we’ll keep it plain. We’ll break down the premium payment setups (employer vs. individual, pre-tax vs. after-tax, W-2 “imputed income”) and show how each one could impact the tax status of disability checks. Then, we’ll cover potential situations, split funding, mid-year changes, and what to expect at tax time, so if sickness or injury occurs and work becomes complicated, the IRS doesn’t add insult to injury.

Each situation can be unique, so it’s best to consult a tax professional.

How Disability Benefits Actually Get Triggered

Before anyone worries about how the IRS treats disability benefits, they need to secure coverage first, either an individual disability insurance policy or a group long-term disability plan through an employer. Once coverage is in place, the policy language determines when checks start. It does that through its definition of disability. Some policies use stronger “true own occupation” or “specialty own occupation” language, while others use more restrictive “modified” or “transitional” own occupation definitions that limit benefits if the insured earns income elsewhere.

Many policies also add features like partial or residual benefits for loss of income/time/duties; presumptive disability for severe loss of sight, speech, hearing, or limbs; catastrophic (CAT) riders for inability to perform basic daily activities; and small non-disabling injury benefits. The bottom line is simple: the policy’s definition of “disabled” controls when benefits pay and when they don’t.

Premium Payments Decide If Your Benefit Is Taxed

Whoever pays the premium and whether it’s paid pre-tax or after-tax decides your tax fate. If the premium is paid pre-tax, then the benefit will be taxable. On the flip side, paying with after-tax dollars will result in tax-free benefits at disability claim time. And no, you can’t “flip a switch in December” to change it after the fact. Learn this one rule, and you won’t be surprised.

More information here:

People Aren’t Buying Disability Insurance, But They Should

Disability Insurance Misconceptions: Common Assumptions Physicians Can’t Afford to Make

Disability Insurance Taxation: Employer-Sponsored vs. Individual Policies

Are Employer-Sponsored Long-Term Disability Payments Taxed?

Whether someone works at a hospital, clinic, school, tech company, or any other employer, the basic tax rule is simple:

- If the premium is paid with pre-tax dollars (employer-paid or through a Section 125 cafeteria plan), the benefits are usually taxable when they pay out.

- If the premium is paid with after-tax dollars, the benefits are usually tax-free.

It gets trickier when the cost is split. Maybe the employer pays part of the long-term disability (LTD) premium, and the employee pays the rest with after-tax dollars. In that case, only the employer-paid portion of the benefit is taxable, and the part the employee paid with after-tax money is tax-free. Same idea with a voluntary buy-up: the base layer the employer pays is taxable, while the extra coverage the employee buys with after-tax dollars is generally tax-free.

Some employer tax options:

- If the employer pays the whole premium with pre-tax dollars, the benefit is fully taxable.

- If the employee pays the whole premium with after-tax dollars, the benefit is generally tax-free.

- If the employer pays the premium but reports it as taxable income on the W-2, it’s basically treated like the employee paid it with after-tax dollars, so the benefits are usually tax-free.

But many larger employers don’t offer any choice at all. The plan may be set up so the employer pays the premium on a pre-tax basis and never imputes it as income, which locks employees into taxable benefits if they go on claim. HR and payroll decide this structure, and employees often just have to live with it. That’s why it’s so important to layer individual disability insurance on top of group coverage, especially when group disability benefits would be taxed.

The pattern is simple: pre-tax in = taxable out; after-tax in = usually tax-free out.

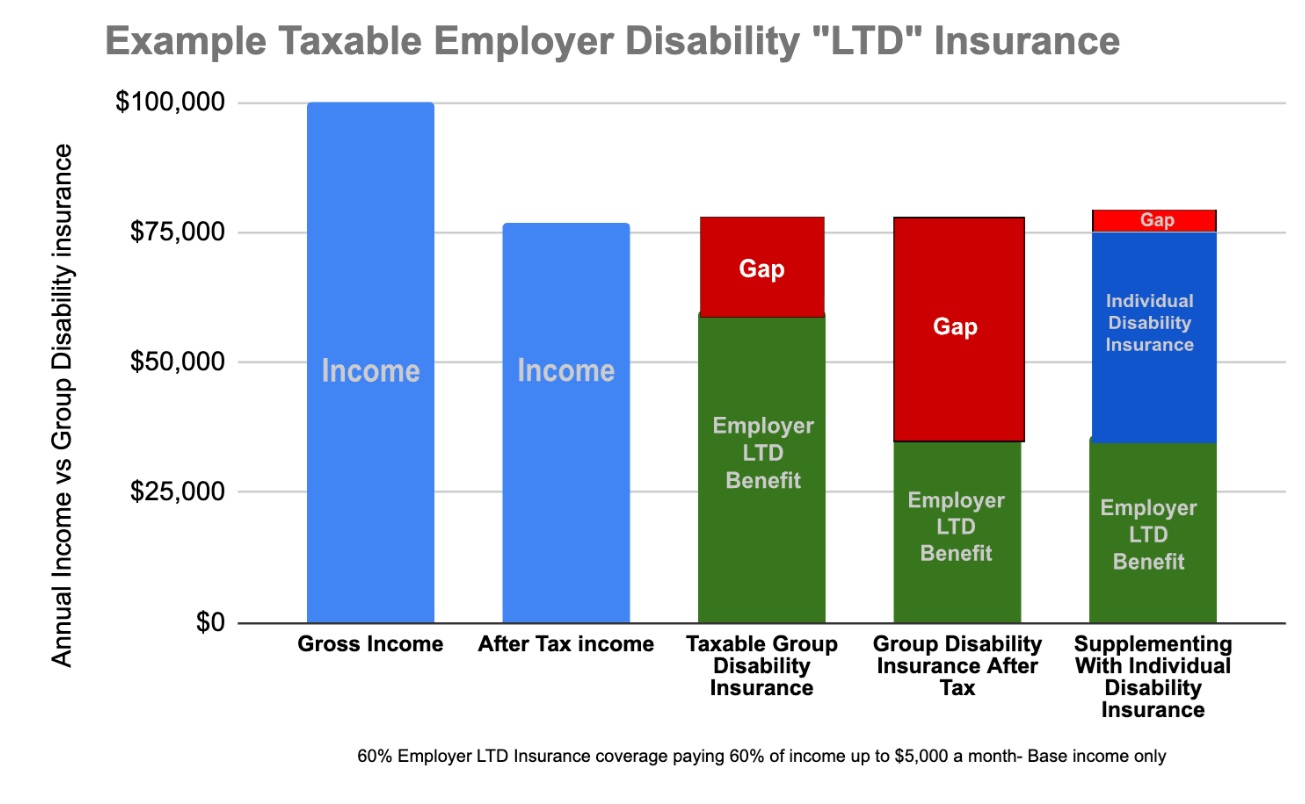

The chart above shows how taxable group LTD benefits actually pay out and the gap that appears once taxes hit. It’s a good reminder why many people choose to supplement group LTD with individual disability coverage to avoid that drop in take-home benefits.

Are Individual Disability Insurance Payments Taxed?

Individual disability insurance is a personally owned policy you buy directly from an agent. The White Coat Investor has a list of recommended insurance agents who write individual disability insurance for the WCI community. Unlike a group disability plan provided by an employer, an individual policy stays with you no matter where you work. It typically has stronger own occupation protections, and it is fully under your control.

Because you pay the premiums with after-tax dollars and you can’t deduct individual DI premiums, the IRS treats the benefits as tax-free in almost every situation. That’s why most physicians and high-income earners prefer individual coverage: stronger definitions, portable protection, and no tax hit on the benefit.

When Individual DI Premiums Can Be Deductible

While rare, there are situations where an employer can pay for or reimburse an individual disability policy with pre-tax dollars, usually through a Section 125 cafeteria plan or an executive-benefit arrangement. In that case, the part of the premium paid pre-tax makes that same portion of the benefit taxable, pro rata, just like a group plan.

In the more typical setup, where paying individual DI premiums with after-tax dollars and not deducting them, the benefits are not included in taxable income when they’re paid out.

Are S-Corp, Partnerships, and Sole Prop Disability Premiums Deductible?

For an S-Corp owner who owns more than 2% of the company, the business can deduct the health and accident insurance premiums it pays for that owner, including disability insurance, as long as those premiums are reported on the owner’s W-2 as taxable income. These amounts are not subject to Social Security or Medicare taxes.

In practice, that means the owner is paying the premiums with after-tax dollars, so the disability benefits are usually tax-free if they ever go on claim. For partners and sole proprietors, personal disability insurance premiums are usually not tax-deductible, so they are already paying with after-tax money. The simple rule in all of this is: when premiums are paid with after-tax dollars, disability benefits are typically tax-free when they are paid out. (You should still confirm this with a CPA.)

Timing Your Premiums to Avoid Taxes

At the beginning of this post, one of the questions from a WCI social channel stated, “If I wait until December to deduct my DI premiums, can I skip the write-off if I had a claim that year, so my benefits won’t be taxed?”

It’s important to clear up this misunderstanding about how disability insurance benefits are taxed. The IRS decides whether benefits are taxable based on how the premiums were actually paid—pre-tax or after-tax—over time. If premiums were paid with pre-tax dollars, the benefits are taxable. If premiums were paid with after-tax dollars, the benefits are usually tax-free.

How the 3-Year Look-Back Works for Disability Insurance Taxation

For group disability plans, insurers often use a three-year look-back to figure out what portion of the benefit is taxable when someone has switched between pre-tax and after-tax premium payments. The insurer reviews the last three years of premium payments and taxes the benefit in the same proportion as the percentage of premiums that were paid pre-tax during that period. For example, if one year was pre-tax and two years were after-tax, about one-third of the benefit would be taxable.

For individual disability insurance, the rules are simpler. Most people pay for individual DI with after-tax money, which means the benefit is typically 100% tax-free, and the three-year look-back usually wouldn't apply. A look-back would only come into play if the employer started paying part of the individual policy’s premium with pre-tax dollars or if the premiums were run through a Section 125 cafeteria plan. In those unusual cases, the insurer still has to follow the same IRS principle, and they may use a look-back method to pro-rate the taxable amount. But this situation is rare.

The key point for both group and individual policies is that a person can’t switch how premiums are treated at the last minute to try to change how their benefits will be taxed. The IRS looks at the actual history of premium payments, not the timing of someone’s decision in December. Paying consistently with after-tax dollars is the safest way to keep disability benefits tax-free if a claim ever happens.

More information here:

The Physician’s Guide to the Best Disability Insurance Companies

How Are Disability Business Overhead Expense, Disability Buy-Sell, Key Person, and Business Loan Protection Payments Taxed?

On the business side, disability insurance shows up in a few special forms, and the tax rules follow the same basic pattern you’ve already seen: how the premium is paid usually drives how the benefit is taxed.

Business Overhead Expense (BOE) insurance is meant to keep the lights on if an owner can’t work. It pays the practice’s/business’s monthly bills like rent, staff salaries, and utilities during a disability. BOE premiums are usually deductible to the business as an ordinary expense. The benefits are then taxable to the business, but because the money is used to pay deductible expenses, it often washes out and ends up close to tax-neutral.

Disability Buy-Sell or Buy-Out (DBO) coverage is used to fund a buy-sell agreement when an owner becomes permanently disabled and isn’t coming back. The policy provides money so the healthy owner(s) can buy the disabled partner’s share. DBO premiums are generally not deductible, and the benefits are usually received tax-free when the arrangement is set up correctly. However, capital gains may come into play if the buyout price exceeds the disabled owner’s adjusted tax basis in their ownership interest. That’s why attorneys and CPAs should be involved in drafting the buy-sell and ownership structure.

Key-person disability insurance protects the business when a critical employee or partner can’t work, someone whose loss would really hurt revenue or operations. The business typically pays the premiums and does not deduct them, which allows the business to receive the disability benefits tax-free when a claim happens. Those tax-free dollars can be used to cover lost income, hire a replacement, or keep the business stable.

Disability business loan protection (or business loan DI) is designed to make sure loan payments continue if the owner is disabled. This could be a practice loan, equipment loan, or business purchase loan. The business usually pays the premiums, and the exact tax treatment (deductible or not, taxable or not) can depend on how the policy and loan are structured. The simple rule still applies: if the business takes a deduction for the premiums, some or all of the benefits may be taxable; if it doesn’t deduct the premiums, benefits are more likely to be tax-free. Because these policies tie into entity structure and loan documents, this is another area where a good CPA and attorney should be part of the setup.

Are SSDI, Workers’ Comp, and Other Disability Payments Taxed?

There are a few other disability-related programs people run into, and their tax rules work differently from regular disability insurance. Social Security Disability Insurance (SSDI) can be taxable depending on a person’s provisional income, which includes things like half of their SSDI benefit and other earned income. High-income households often end up paying tax on part of their SSDI check because they cross the IRS income thresholds.

Workers’ compensation benefits are usually tax-free, because the IRS treats them as payments for workplace injuries. The only exception is when a person also receives SSDI—sometimes SSDI is reduced (offset) because of workers’ comp, but the tax-free treatment of workers’ comp itself doesn’t change.

For state income taxes, most states follow the same tax rules the IRS uses for disability benefits, but not all of them do. A few states have their own rules about what’s taxable and what’s not, so people should always check their specific state’s tax guidance.

Disability Insurance Tax Examples

The best way to understand disability insurance taxation is to show examples.

Individual DI paid after-tax: A physician pays their individual disability policy with after-tax dollars. They receive a $10,000 per month benefit, and the full $10,000 is tax-free.

Employer LTD paid pre-tax: The hospital pays for the physician’s LTD through payroll on a pre-tax basis. When a claim happens, the $10,000 per month benefit is fully taxable as regular income. Their actual take-home will be lower depending on their effective tax rate.

50/50 split premium: An employer and employee split the LTD premium evenly, with the employer deducting its portion and the employee paying with after-tax payroll dollars. A $10,000 per month benefit becomes $5,000 taxable and $5,000 tax-free, because taxes follow the percentage of pre-tax vs. after-tax premium dollars.

S-Corp owner (>2% shareholder): The S-Corp pays the DI premium and reports it on the owner’s W-2 as taxable income (not subject to FICA). Because this is treated as after-tax, a $10,000 per month benefit is tax-free when paid.

BOE (Business Overhead Expense) policy: A BOE policy pays $20,000 per month to cover business expenses like rent and staff salaries while the owner is disabled. The benefit is taxable to the business, but those dollars are used to pay deductible business expenses, making the whole thing effectively tax-neutral.

The Bottom Line

Disability insurance taxation really comes down to one simple rule: how the premium is paid decides how the benefit is taxed. Pre-tax premiums usually lead to taxable benefits, while after-tax premiums usually lead to tax-free benefits. The best move for most people is to pay for personal DI with after-tax dollars, know exactly how employer LTD is funded, understand how any business disability coverage is paid for, and have a CPA make sure the paperwork matches the plan.

Set it up correctly now so you don’t get hit with tax surprises later.

[AUTHOR'S NOTE: This is general education, not tax advice. Verify entity-specific treatment with a CPA; rules can vary by state and by plan document.]

Have you ever received disability insurance benefits? Were they taxed, or was it tax-free? Are you currently paying DI premiums with after-tax dollars, or are you on a group disability policy?

The White Coat Investor may receive compensation from White Coat Insurance Services, LLC; licensed in all states including MA and DC; CA license #6009217; NY license #1758759 (exp. 6/2027); Registered address: 10610 S. Jordan Gateway, #200 South Jordan, UT 84095. This does not affect the cost or coverage of insurance.