Being a business owner is risky. That's why, when done well, it generally pays better than being an employee. We have discussed personal disability insurance on this blog many times. It is underappreciated and underpurchased. If you need disability insurance and don't yet own a solid, portable, individual policy, I suggest you meet with a WCI-vetted agent and go over your options.

But that's not what this post is about.

How Would a Disability Affect Your Business?

If you're a physician practice owner with employees, you are not the only one affected in the event of your death or disability. Employees, partners, and the business itself can all be affected. Most business owners recognize the need for a general business liability policy, but too few of them even consider some other important types of insurance. These policies are not nearly as common as individual disability insurance, but they can be very customizable.

More information here:You Need a Plan

You don't necessarily need to buy insurance against every risk that exists. You do need to have a plan of what you and your business are going to do when bad things happen. That's no different than individual disabilities. There are a few options for personal disability that don't involve buying insurance. Consider all of the following:

- Buying individual insurance

- Using an employer-provided insurance policy and hoping you don't need the stronger protections provided by an individual policy

- Relying on your spouse's income and hoping you don't both become disabled

- Relying on your wealthy parents or other benefactors and hoping they still care about you after you become disabled

- Being financially independent yourself

While No. 5 is probably the best option, No. 1 is still top-notch for those early- and mid-career docs who are not yet financially independent.

Now, let's consider each of the risks your business faces.

Death of a Sole Proprietor

What's the plan if that solo practice doc suddenly dies? Typically, the executor(s) will fire sale the business for whatever they can get for it. There are other options, though. The business could own a life insurance policy on the sole proprietor which would provide the funds needed to keep the business going long enough to get a better price for it. Locums docs could be hired, or an orderly transition to a new doc could occur. This could all result in a much better sale price for the heirs and much better patient care.

Term life insurance is probably perfectly adequate for this need, although if a doc is planning to practice into their 70s or 80s, a whole life insurance policy might not be a terrible idea. If the worst doesn't happen, the doc could take ownership of the policy personally and use it to help fund retirement or just leave it as part of their personal estate.

Short-Term Disability of a Sole Proprietor

Imagine you get a big old meningioma. After surgery, you're left with debilitating headaches for months. You can't even manage your household, much less go to work. But if you don't keep paying the rent and your employees, you'll be starting all over after your disability. Your disability insurance will take care of you and your family, but there probably isn't enough income there to also keep the practice afloat. The cash on hand in the business will probably only last a few months, and then you'll be forced to use your personal savings or let the business go.

Is there a solution to this problem from the insurance industry? There sure is. It's called business interruption insurance. It's often bundled into a general business policy, and waiting periods are very short—as little as 48-72 hours. If your business has to close due to a covered reason, this insurance will replace part or all of your revenue. Tree falls on the building? Doctor gets sick? Road in front of the business is closed for construction? Short-term disability? Jury duty? Lengthy malpractice lawsuit requiring you to be away? All could be covered by business interruption insurance. It generally doesn't cover pandemics, floods, earthquakes, or criminal activity. It might not cover utilities either, as the thought is that they'd be shut off if the business closes for a while.

But it does typically cover expenses like these:

- The revenue you'd make if the business was open

- Mortgage or rent payments

- Loan payments

- Taxes

- Payroll

- Benefits

- Relocation costs or rent at a new location

Sometimes, business interruption insurance is distinguished from business overhead insurance. The overhead insurance would be used in the event of the owner's disability, and the interruption insurance would be used for other risks.

Long-Term Disability of a Sole Proprietor

This one is a little bit trickier, because you don't always know in the beginning how long a disability is going to last. Business interruption/overhead insurance typically only pays for 12-24 months, so at some point, one needs to recognize that the doc isn't coming back any time soon and the business needs to be closed or sold.

Death of a Partner

Life becomes more complicated in partnerships. Partners often do not want to be in business with the heirs of their partner. So, partnership agreements often include buy-sell agreements, where the deceased partner's estate is bought out by the still-living partner(s). Again, insurance does not have to be the solution here. My partnership buyout is so small and can be funded over so many years that we would never consider buying life insurance on partners to cover this expense. Plus, there are over 20 partners now to help pay for it.

A buyout of my heirs would just be done using cash flow from the regular business of the partnership. However, in a more valuable partnership with fewer partners, there may not be enough cash. Imagine if you needed millions to buy out your partner's heirs. You probably don't have it, and you may not be able to borrow it. A great solution might be a life insurance policy. Term policies are probably adequate, but whole life insurance policies could be used—especially if partners are planning to work well into their 60s, 70s, or 80s. The policy could be owned by the business or by each of the partners, but the more partners there are, the better it is for the business to own the policies.

Short-Term Disability of a Partner

In a small partnership, even a short-term disability can be a real hardship. A business overhead policy that will cover that partner's share of the overhead seems wise.

Long-Term Disability of a Partner

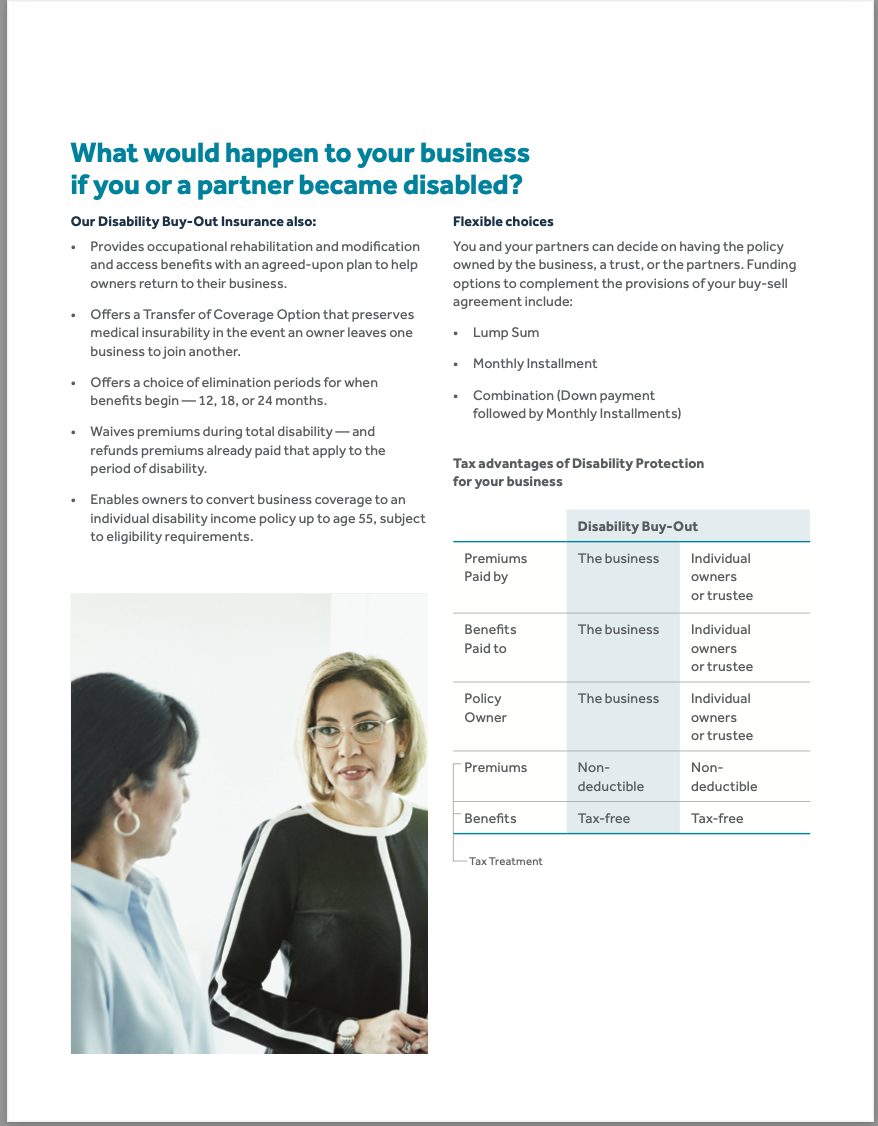

Finally, we arrive at the real point of this post. While you can use life insurance to fund the buyout of a dead partner's heirs, you can't use it to fund the buyout of a permanently disabled partner. Luckily, there is an insurance solution to this problem as well. It's called disability buy-out insurance. Here's a Guardian pamphlet that demonstrates how the marketing for this product looks:

Disability Buy-Out Insurance Pamphlet

Here's the meat from the pamphlet:

These are all customizable, and the benefit payments should match the buy-sell agreement. For example, if the buyout is one lump sum, then the insurance policy should pay one lump sum. These policies typically require permanent disability using a true own occupation definition and, because it can take time to determine if one is truly permanently disabled, they often don't pay for 12-24 months. The buy-sell agreement may need to be modified to match that. For that first 1-2 years, business overhead insurance would need to make the practice whole in the event of the disability of a partner.

Here's a video talking about how these three types of insurance (personal disability, overhead insurance, and disability buy-out insurance) can work together to provide full coverage in the event a doctor becomes disabled:

Should You Buy Disability Buy-Out Insurance?

Here's where the rubber meets the road. Do you actually want to pay for this coverage? As you know from looking at personal disability policies, they're expensive because disability is far more likely than death. The more partners you have, the more likely one of them is to become disabled.

Of course, the more partners you have, the less each partner's share of a buyout of a disabled partner would be. You don't necessarily need insurance, but you do need a plan. Many partnerships, upon making a plan, will appropriately decide that this type of insurance is an important part of that plan. Like most disability insurance policies, premiums are not deductible but the benefits are tax-free. The policies can be owned by the business or “cross-purchased” by the other partners. The first is generally easier, but the second could potentially be more attractive to some people, especially in a small partnership and particularly if the buyout is the responsibility of the individual partners and not the business.

What Does Disability Buy-Out Insurance Cost?

I obtained a quote from Guardian for a $1 million payout 12 months after disability of a healthy 40-year-old non-surgeon partner. Here is what it looked like:

Not cheap. Note how much more expensive this is than a 10-year level premium term life insurance policy for a healthy 40-year-old male ($580 per year for $1 million). You can make it cheaper by pushing out when it pays out to two years,

That would save you about 20%.

More information here:What Does Business Overhead Insurance Cost?

While we're at it, let's look at the cost of a business overhead insurance policy. Same doctor, a maximum of a $300,000 benefit payable over 12 months.

There are alternatives that are both more and less expensive.

Obviously, these quotes are not for you, but they should give you a ballpark sense of what these policies cost. As you can see, buying all of this (personal disability, disability buy-out, and business overhead) is basically the equivalent of buying three different disability insurance policies. You could easily spend $10,000 a year between the three. As insurance becomes more and more expensive, people logically choose to “go bare and hope.”

The death or disability of a practice owner or partner can be a financial catastrophe to the business. Don't buy unnecessary insurance, but insure well against financial catastrophes. If you need help with business overhead insurance or disability buy-out insurance, your first stop should be consulting with one of the agents vetted by the WCI community.

What do you think? Does your practice have a life insurance policy on owners? What about disability insurance? What's your plan if one of your partners gets disabled?