In the first of the Lord of the Rings movies, Aragorn asks Frodo, “Are you frightened?”

Frodo responds, “Yes.”

Aragorn replies, “Not nearly frightened enough; I know what hunts you.”

Now, Frodo was hunted by nine funky disembodied “ringwraithes,” which aren't exactly a huge problem when it comes to the finances of physicians. However, there are six things that physicians should be frightened about and actively work to avoid.

#1 Burnout

Burnout is the single biggest threat to physician finances. If you become unable to work at age 45 due to severe burnout, that could cost you plenty of money. That's 20 years x $400,000 per year = $8 million. A more accurate figure, taking off 1/4 of that for taxes and applying 20 years of compound interest at 5%, is

=FV(5%,20,-300000,0) = $9.9 million

That's a heck of a financial risk.

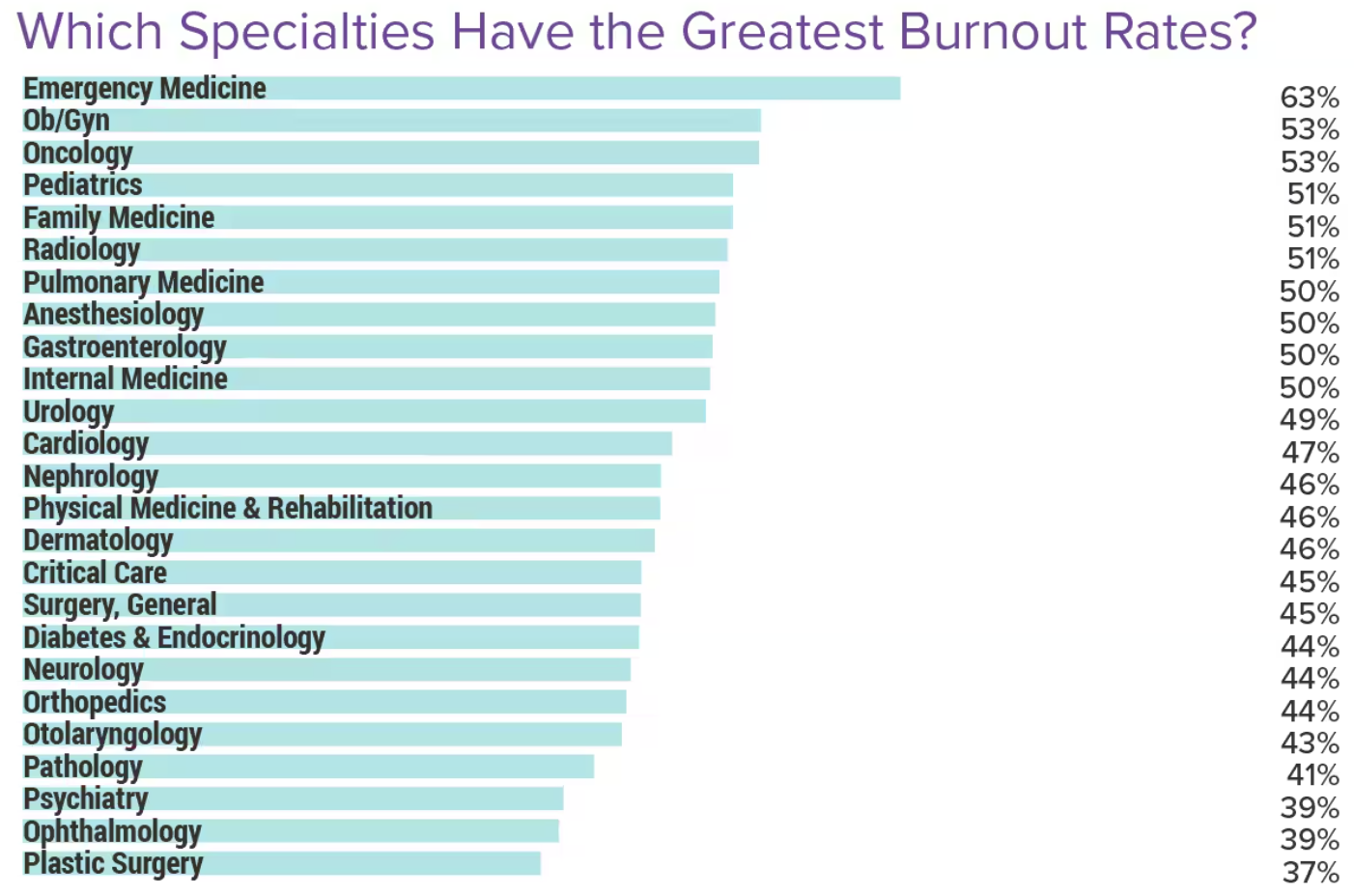

Check out any survey about burnout that you've ever seen. Here's one from the 2024 Medscape Physician Burnout and Depression Report.

Though the burnout numbers seem to be slightly declining now, my specialty of emergency medicine, as usual, is the big winner. If you think you're not going to deal with burnout in EM, well, in the words of Clint Eastwood, “Do you feel lucky?” Given that the most effective burnout technique I know of is to just work less, you'd probably better plan your financial life such that you can cut back to half-time by age 50.

Speaking of working less, the first question I ask a doc suffering from burnout is, “Have you considered cutting back to full-time?” Most chuckle and admit to working more than 40 hours a week. It's pretty amazing how much better all of your life feels when you work 40 hours instead of 60. That's 20 more hours a week, a half-time job, you can spend doing those things that reduce burnout. You know, like sleeping, exercising, pursuing your favorite hobbies, spending time with the people you care about most, or even just vegging out and recovering from a hard day on a challenging job.

Naturally, the downside of this technique usually is lower pay. Lots of other things that also fall into the category of “cutting back” are dropping night, evening, weekend, or holiday shifts; taking less call; or seeing fewer of certain types of patients or doing certain types of procedures. Lower pay, but a better life. And truthfully, it's actually more pay because you can stay in the game longer. Better to be paid for 30 years as a pediatrician than 10 years as a back surgeon, especially when you factor in the lower tax rate, additional Social Security contributions, and more time for compound interest to work its magic.

Optimizing for career longevity is the key when it comes to beating burnout. Every time you have a career decision, consider which option will allow you to practice longer, and choose that one. Here are some other ways to learn burnout-busting techniques:

- Attend The Physician Wellness and Financial Literacy Conference (usually about 17 credits of CME)

- Take our Continuing Financial Education 2026 online course (16.5 credits of CME)

- Take our Financial Wellness and Burnout Prevention for Medical Professionals online course (eight credits of CME)

- Hire a physician coach

These are the closest things that exist to “burnout insurance,” and like everything else doctors deal with, it's far better to prevent than treat when it comes to burnout.

More information here:

Biggest Financial Mistakes Doctors Make

How My Burnout Led to Rage That Could’ve Ended My Career

#2 Disability

People debate just how big a risk disability is to your career. The Social Security Administration says 1/4 of people will become disabled before age 65. Whether that risk is 25% or just 10%, the consequences are pretty severe either way. Imagine getting disabled at age 35 and losing the next 30 years of whatever you earn. That's millions of dollars. It's best to buy some disability insurance to cover that. The sooner you buy it, the cheaper it will be, the more benefits you will potentially collect, and the less likely you will be denied for an acquired medical condition.

#3 Death

The death of a breadwinner is just as expensive as disability of the breadwinner. If anyone else also depends on your income, a big fat (seven-figure) term life insurance policy seems appropriate. Which you can buy here.

#4 Divorce

The third of the classic “Big Bad Ds” in personal finance (death, disability, and divorce), this is the only one that can't be insured against. Divorce cuts your assets and your income in half. It's often worse than that, since people blow through money paying attorneys or spending just before the divorce (everything is 50% off!). And expenses after divorce are never cut in half. I have said many times that date night is probably your best asset protection technique.

The only way to be 100% sure to avoid this risk is to never get married, but that's generally bad for your finances as well. The studies are pretty clear that, on average, married people have more money than single people who have more money than divorced people. So, get married, but do it right the first time, and then make that marriage the most important thing in your life. Here is the to-do list for this threat:

- Very careful selection process

- Date night

- Marriage therapy

- Constant improvement and work at marriage

#5 Ignorance

The most common financial mistakes I see people make are just doing the wrong thing because of ignorance. They just don't know that what they're doing is stupid.

- Oh, I should buy insurance for that?

- Oh, I need to save 20% for retirement for my whole career?

- Oh, there is an evidence-based way to invest properly?

- Oh, that's how my retirement accounts work?

- Oh, I can still contribute to a Roth IRA despite having a high income?

- Oh, I should have bought term life instead of this whole life?

- Oh, my second home isn't really an investment at all?

- Oh, you don't change investments based on what is happening in the news?

- Oh, I should have titled this property differently?

- Oh, I need a will?

Financial literacy is incredibly valuable when combined with the high income of most who read this site. That first good financial book you read is literally worth millions of dollars over the course of your life. We're here to help with this one. Try these techniques:

- Read the blog.

- Listen to the podcast.

- Read some good books.

- Put a written financial plan in place.

- Take the Fire Your Financial Advisor online course.

#6 Bad Financial Behavior

Financial literacy doesn't actually save you from everything. You still need some financial discipline. The combination of financial literacy and financial discipline in our world is so rare that if you have both, it's like having a superpower. You look at all the muggles around you and sometimes just shake your head, wondering how someone could live like that. Discipline is what keeps you from spending all your money (and more), raiding your emergency fund for trivial things, carrying credit card debt, buying cars on credit because you lack the patience to save up for three more months, becoming house poor, buying high/selling low, and more.

- Build your financial muscles early on.

- Learn to spend deliberately on what you value most.

- Be generally frugal and selectively extravagant.

- Follow your written investing plan, especially in a bear market.

More information here:

Best Investment Portfolios — 150+ Portfolios Better Than Yours

What Is Not a Threat to Your Finances?

Not everything is a big threat to your finances, despite how often they get discussed and debated around here. Here are some examples:

Picking the Wrong Investments

Your asset allocation doesn't actually matter that much. Funded adequately, anything reasonable will likely get you to your goals. Even if you choose actively managed mutual funds or you pick your own diversified portfolio of individual stocks, you'll probably still get where you're going—even if you arrive a little late.

Spending Some Money Along the Way

If you're reading this blog, you're far more likely to struggle with spending money appropriately than saving it. The goal isn't to be the richest doctor in the graveyard but to find the proper balance of your limited resources. That includes time, health, money, and motivation. Save some, spend some, give some, and (most of all) build a wonderful, full life.

Whether You Pay Off Debt or Invest

Both paying off debt and investing provide you with a return and build your net worth. It really doesn't matter all that much which one you do first. If the decision isn't obvious, it doesn't matter much.

Tax-Deferred or Roth

You know what else is choosing between good and better? That classic, endless argument you have with yourself about whether to do a Roth conversion or make a Roth contribution. If the right choice isn't obvious, it really doesn't matter all that much.

Driving a New Car or a Used Car

This one is a big deal for the average American but not for doctors making $200,000-$800,000 a year. It's not financially wise to churn brand new cars every three years (much less lease them), but it probably won't sink a doctor ship.

Whether You Use an Advisor

It's also possible to be successful whether you choose to be your own financial planner and asset manager or hire someone who offers good advice at a fair price. If you're going to DIY, you need to make sure you do it right, and if you hire an advisor, you do need to make sure you're getting good advice (the advice should sound like what you read on this blog) for a fair price ($7,500-$15,000 per year).

Take Social Security Early or Not

The right move for most is that the high earner, if reasonably healthy, delays Social Security until age 70. But it isn't the end of the world if you take it at 67 or even 62.

Avoiding IRMAA, Getting ACA Subsidies, Getting Your Kid into the Right College

We could run a blog post every day of the year about the things that just don't matter all that much. Be careful trying to optimize too much in your life. With all that optimizing you're doing, be sure not to forget to enjoy the ride. All of us are only here for a few more years, and your hearse won't have a trailer hitch.

What do you think? What are the biggest threats to your finances and why? What threats don't matter to you?

The White Coat Investor may receive compensation from White Coat Insurance Services, LLC; licensed in all states including MA and DC; CA license #6009217; NY license #1758759 (exp. 6/2027); Registered address: 10610 S. Jordan Gateway, #200 South Jordan, UT 84095. This does not affect the cost or coverage of insurance.