Each year, we do a survey of the WCI community. The main reason we do so is to get the feedback (especially negative feedback) we need to serve you as well as we possibly can. That feedback is so valuable that we are willing to bribe you to give it to us. We do that by giving away free WCI products and swag to respondents. (You've already been contacted if you won.)

But we also do that by offering to share the aggregated data with you in a blog post each year. Most people LOVE to anonymously compare themselves to others, and WCIers are no different. Ready? Let's get into the data.

My 2 Questions

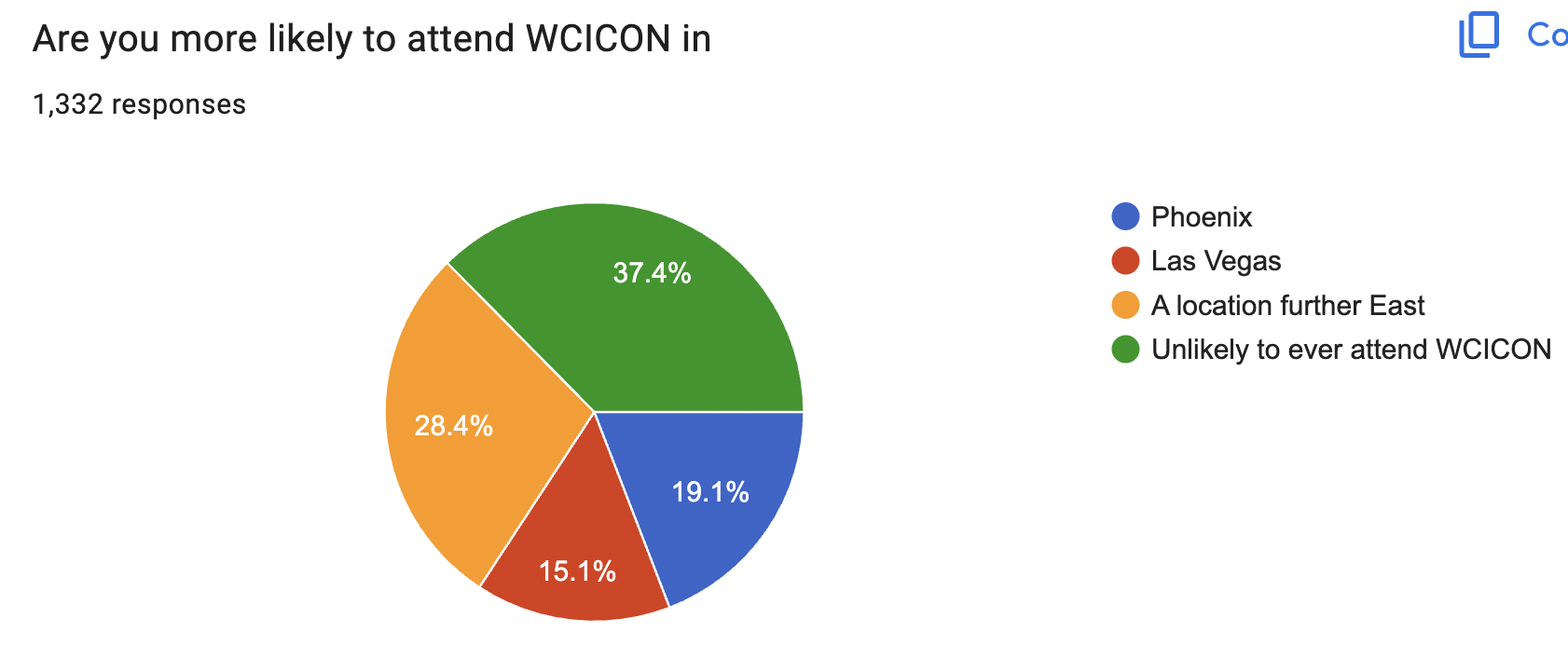

I asked the staff to include two questions on the survey that I really wanted to know about. Let's start with those. The first was a dilemma we've debated back and forth here at WCI about our annual conference, WCICON. I'm convinced that while everybody says they hate Las Vegas, they all kind of secretly like it. Plus, it's a very easy and relatively inexpensive airport to get in and out of due to all the direct flights. I've hypothesized that more of you will actually come to a WCICON in Las Vegas than somewhere else out west, like Phoenix. But now, when we debate things like Las Vegas vs. Phoenix in the future for WCICON, we actually know what you think anonymously about Vegas.

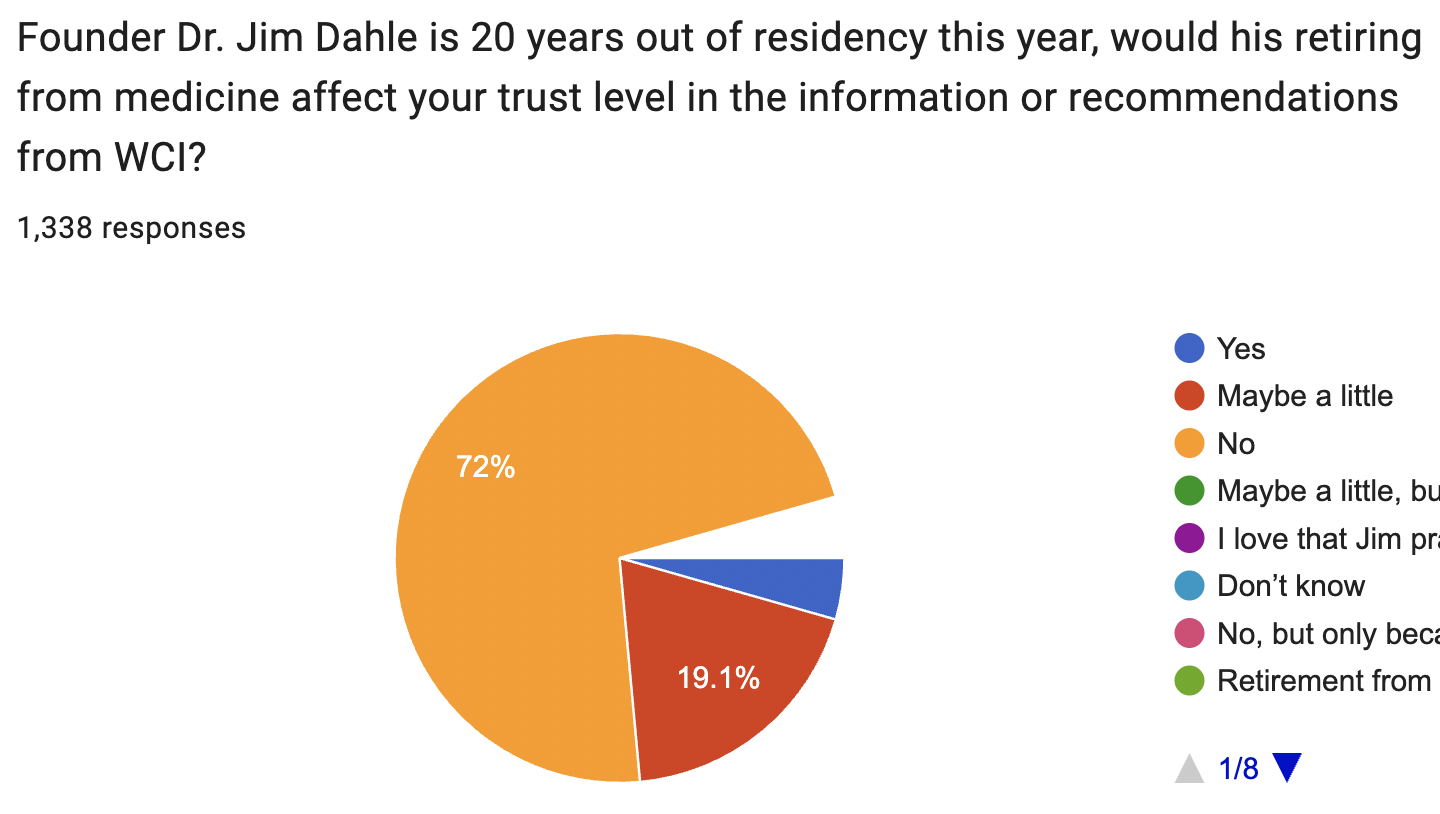

The second question is one I think about all the time as I deal with my daily existential crisis of what I'm going to do with the rest of my life. I've wondered whether my retiring completely from medicine would affect WCI in any way.

It's nice to know that if I were no longer “in the trenches” with you, it wouldn't impact WCI too much. That response will keep me from asking the follow-up question on next year's survey of whether I should drop EM or WCI when I'm ready to cut back to one part-time job. We're pretty sure we know what that answer would be! After taking this survey, one of my partners asked if I was going to retire anytime soon. The answer is still no, but I've seen that decision get made pretty suddenly by some of my partners over the years. I guess you never know, but I am getting ready to board-certify again next year. Fun!

The WCI Community

We know that those who answer these surveys are not exactly representative of the entire WCI community (selection bias, anyone?), but the survey did say that about 40% of respondents had never taken it before. At any rate, here's how you describe yourselves:

You're from all over the country (98.8% US). The big slices there are California, Texas, New York, North Carolina, Ohio, Florida, Illinois, and Minnesota.

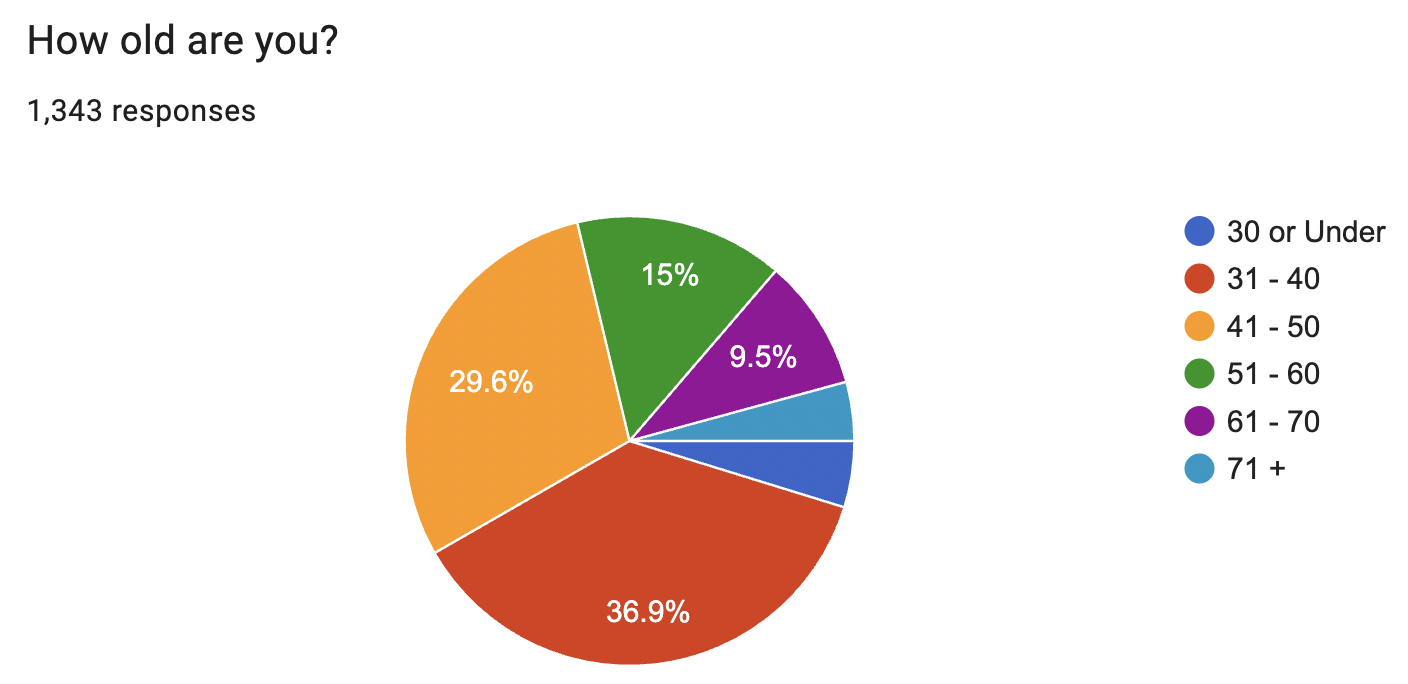

You're mostly my age (50) and younger, but there are plenty of late career and even retirees in the community.

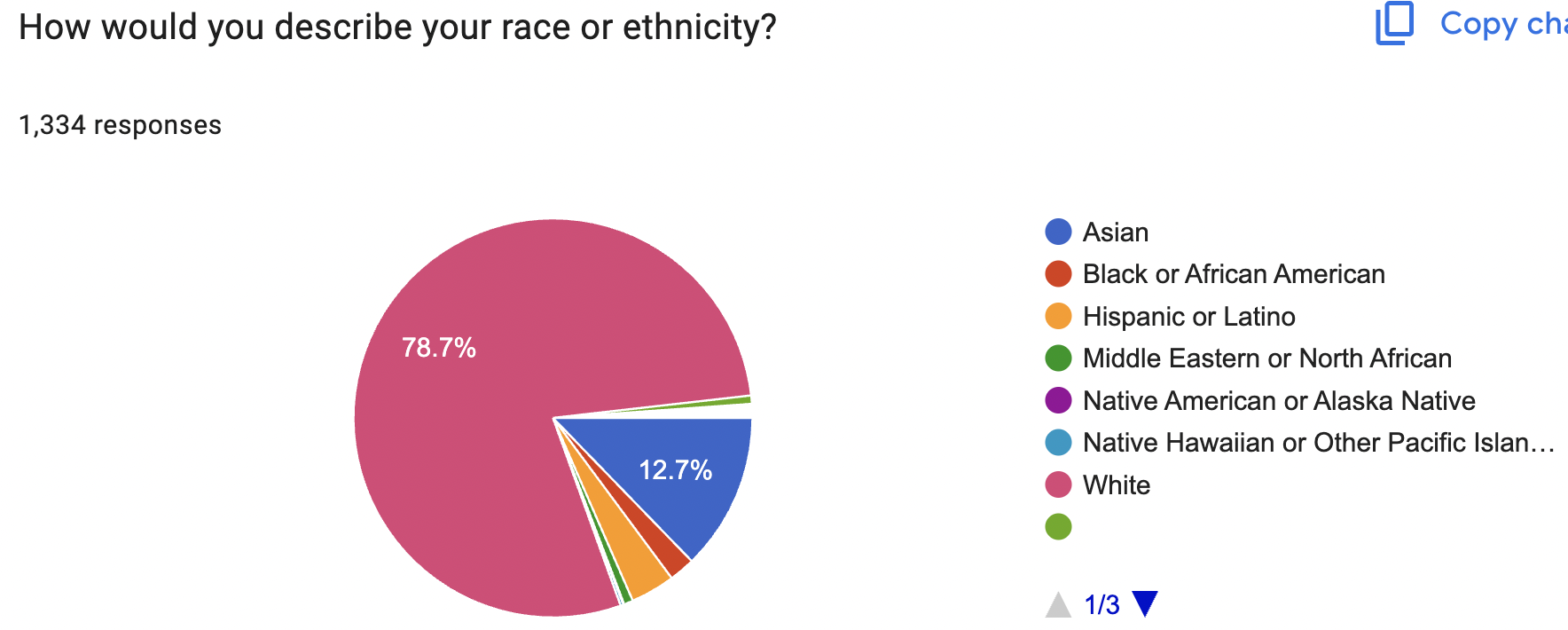

You're white (and Asian),

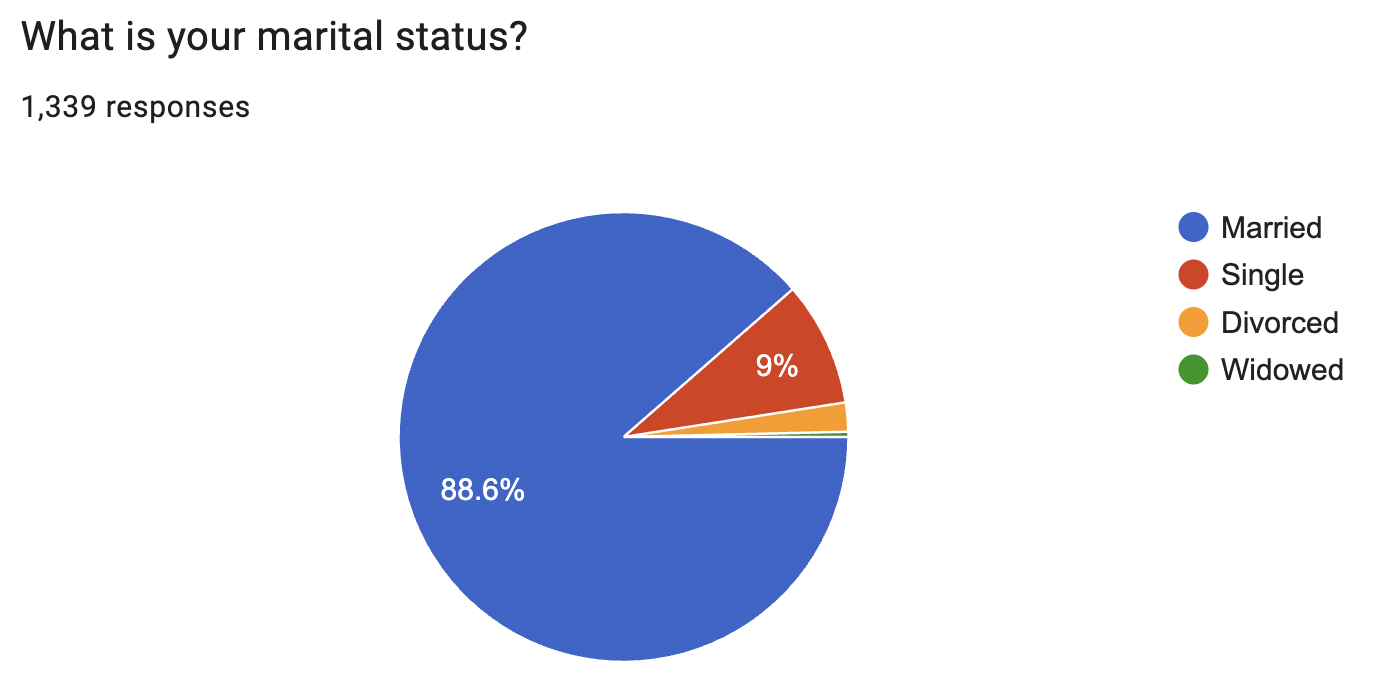

overwhelmingly married (shockingly so),

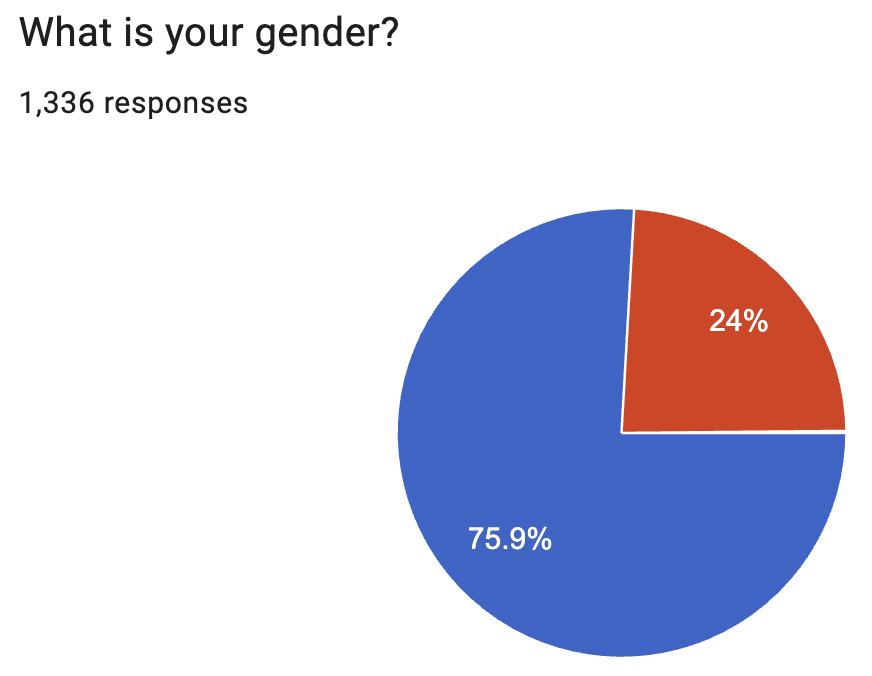

and male (despite our best efforts with columnists, guest posts, and the Financially Empowered Women group). With now >50% of medical school classes being female, we're hopeful this will continue to equalize over time. The conference attendees sure don't look like that, but this survey did. The WCI staff might be majority women, but the audience is apparently not even close.

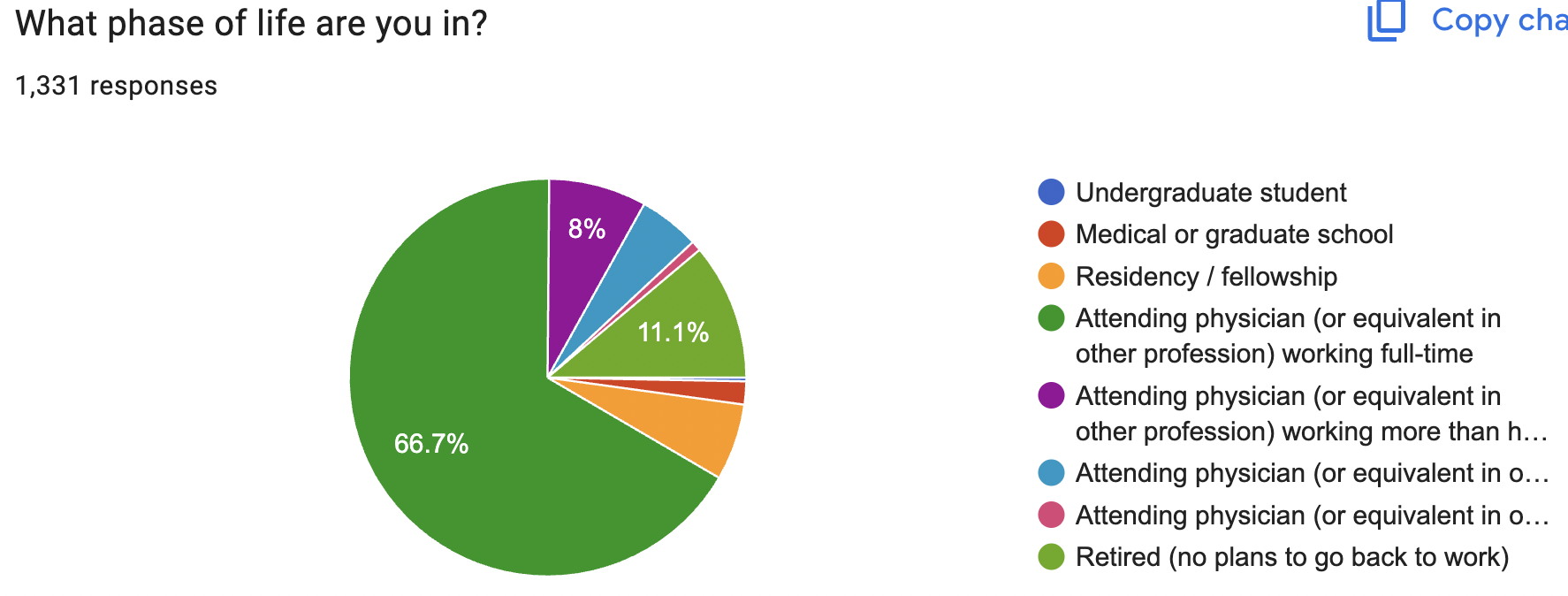

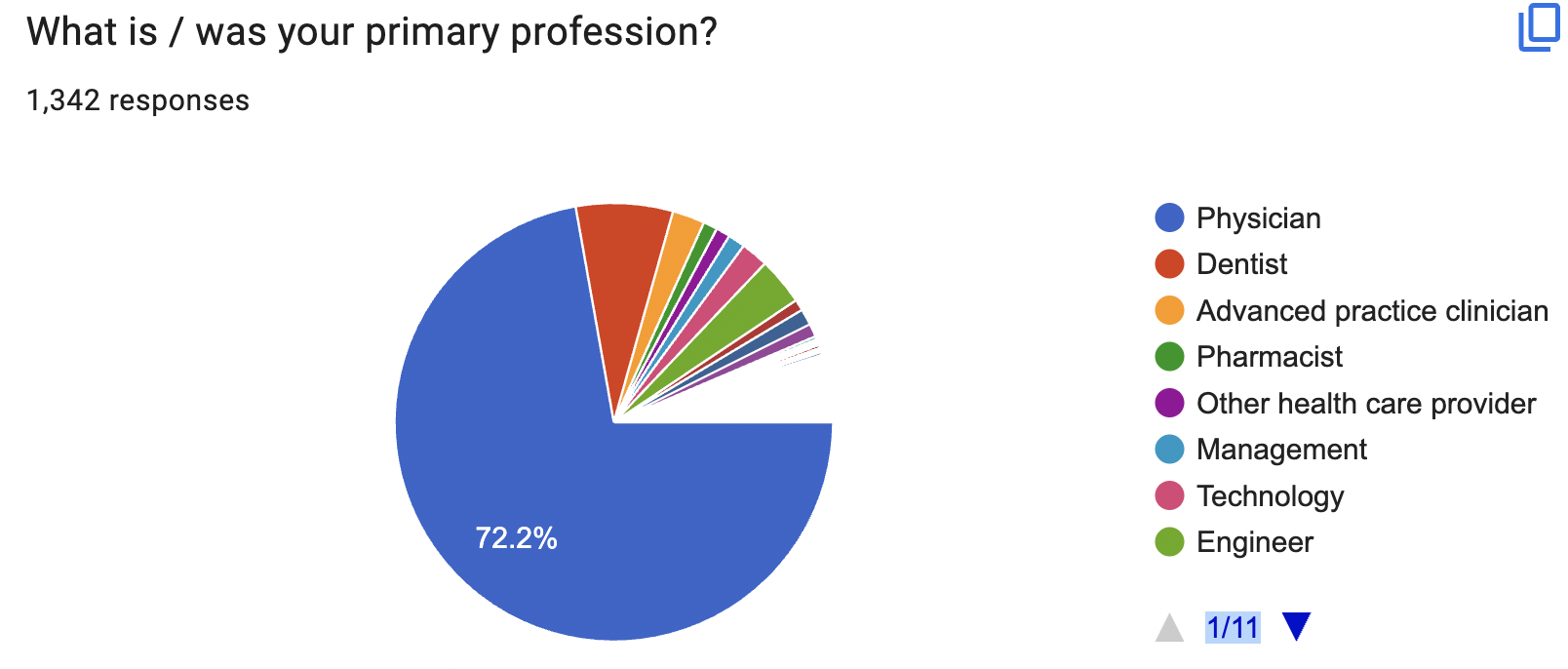

You're mostly attending level physicians (or the equivalent in other professions). Trainees were not the #2 category, though. Retirees were. And in fact, that number went up from 8% of our audience to 11%. Congratulations to that 3%, most of whom presumably retired in the last year.

You're still mostly docs (physicians and dentists), but there are 11 pages of other professions represented in the community. Engineers actually took the #3 spot this year, ahead of APCs.

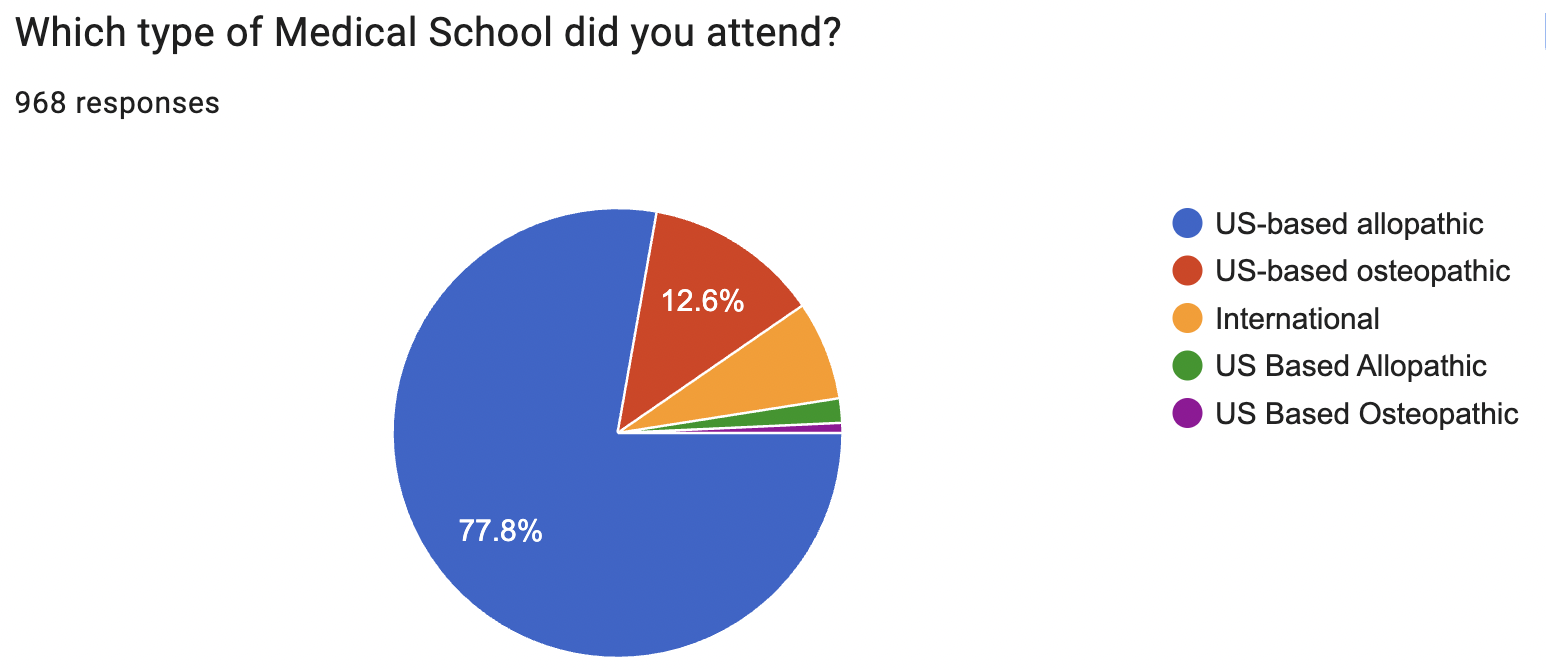

The physicians are mostly MDs, but with plenty of DOs and IMGs. Not sure how we duplicated possible responses on this one.

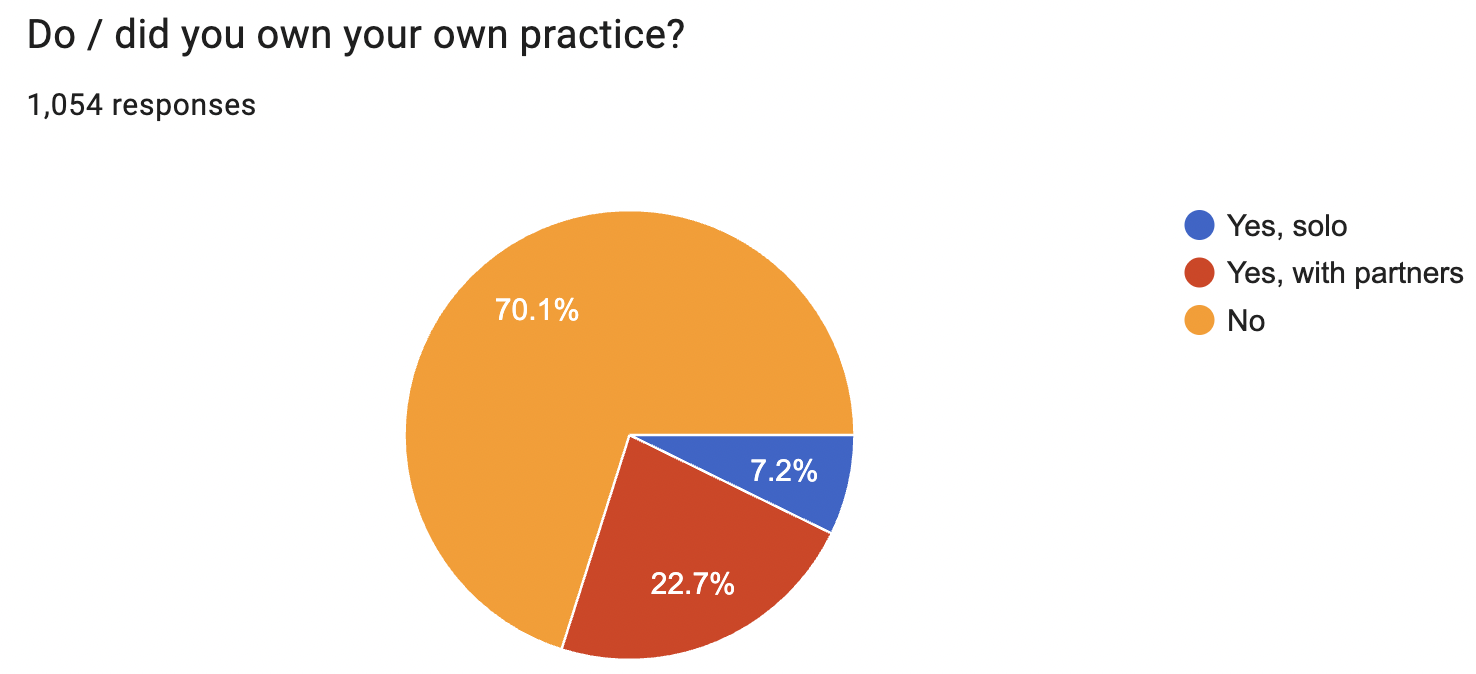

Most are employees.

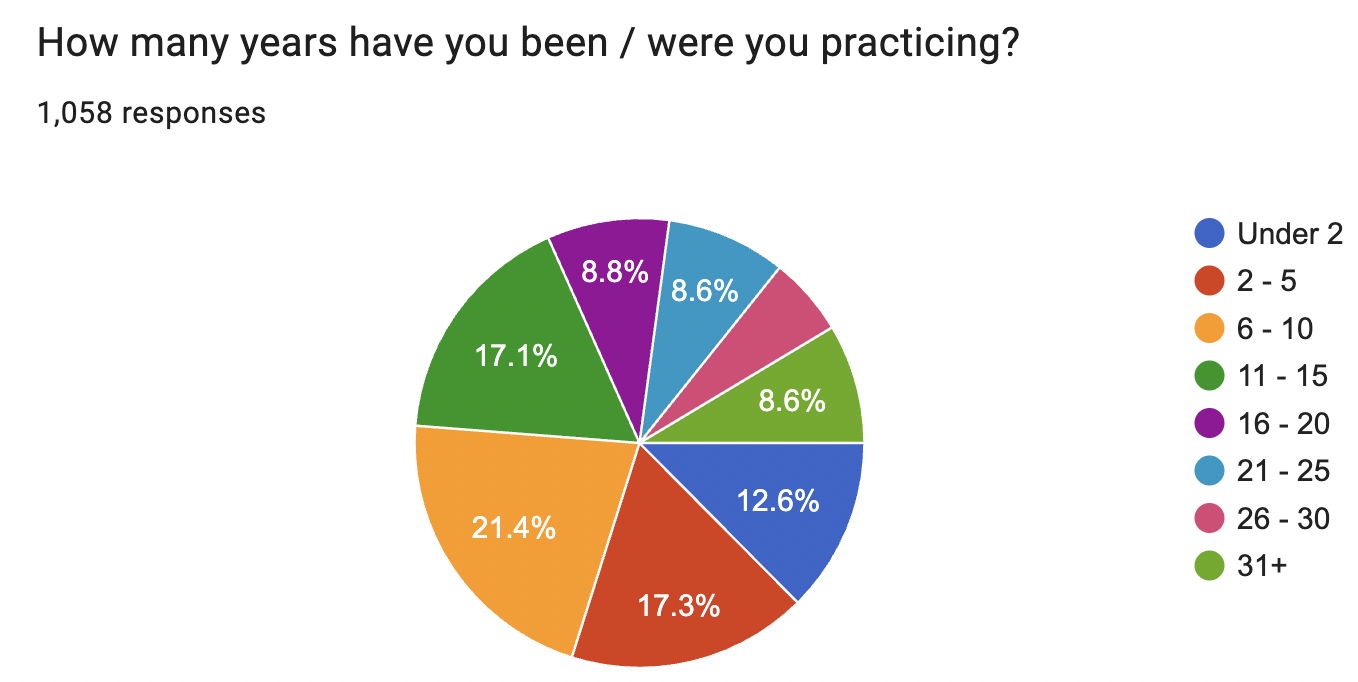

And I've been practicing for longer than most of you. Maybe I should start saving for retirement.

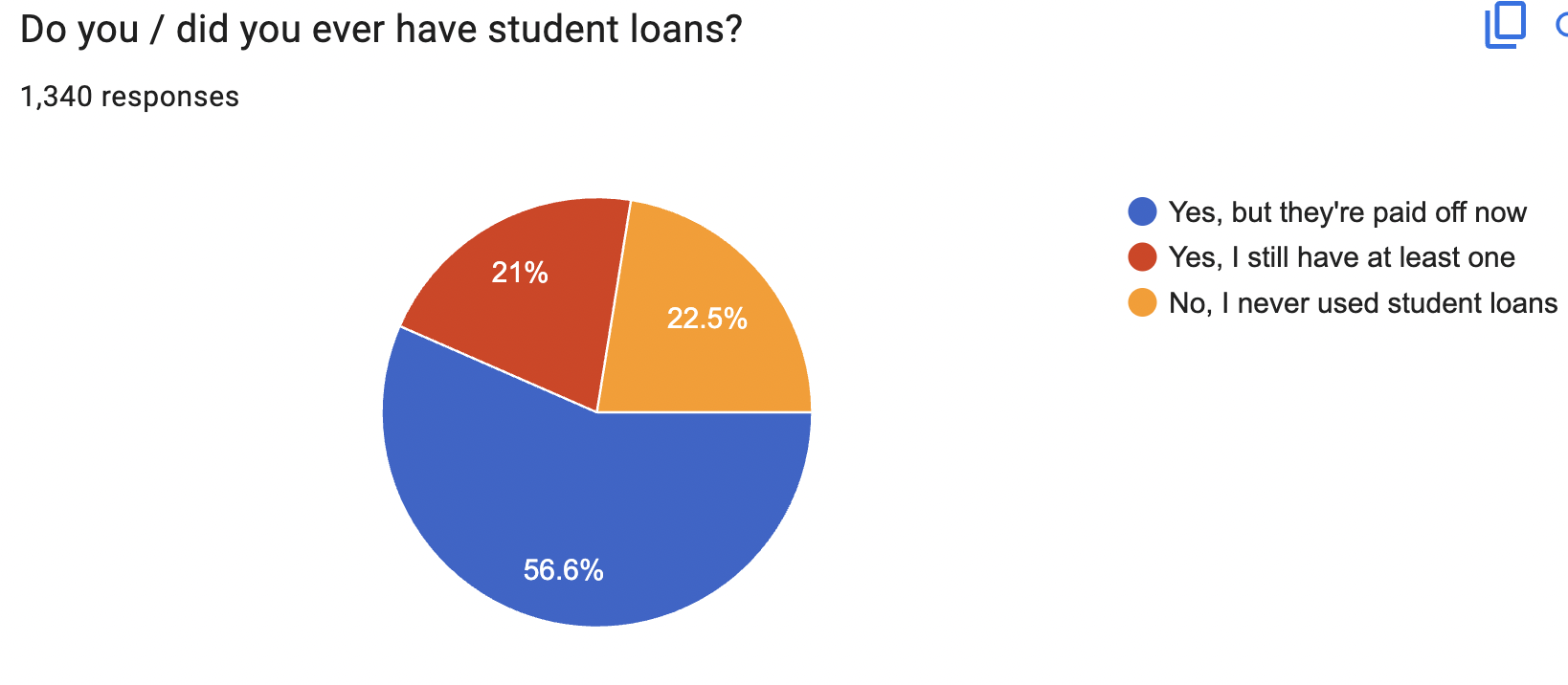

Some of you still have student loans, and this next chart brings joy to my heart:

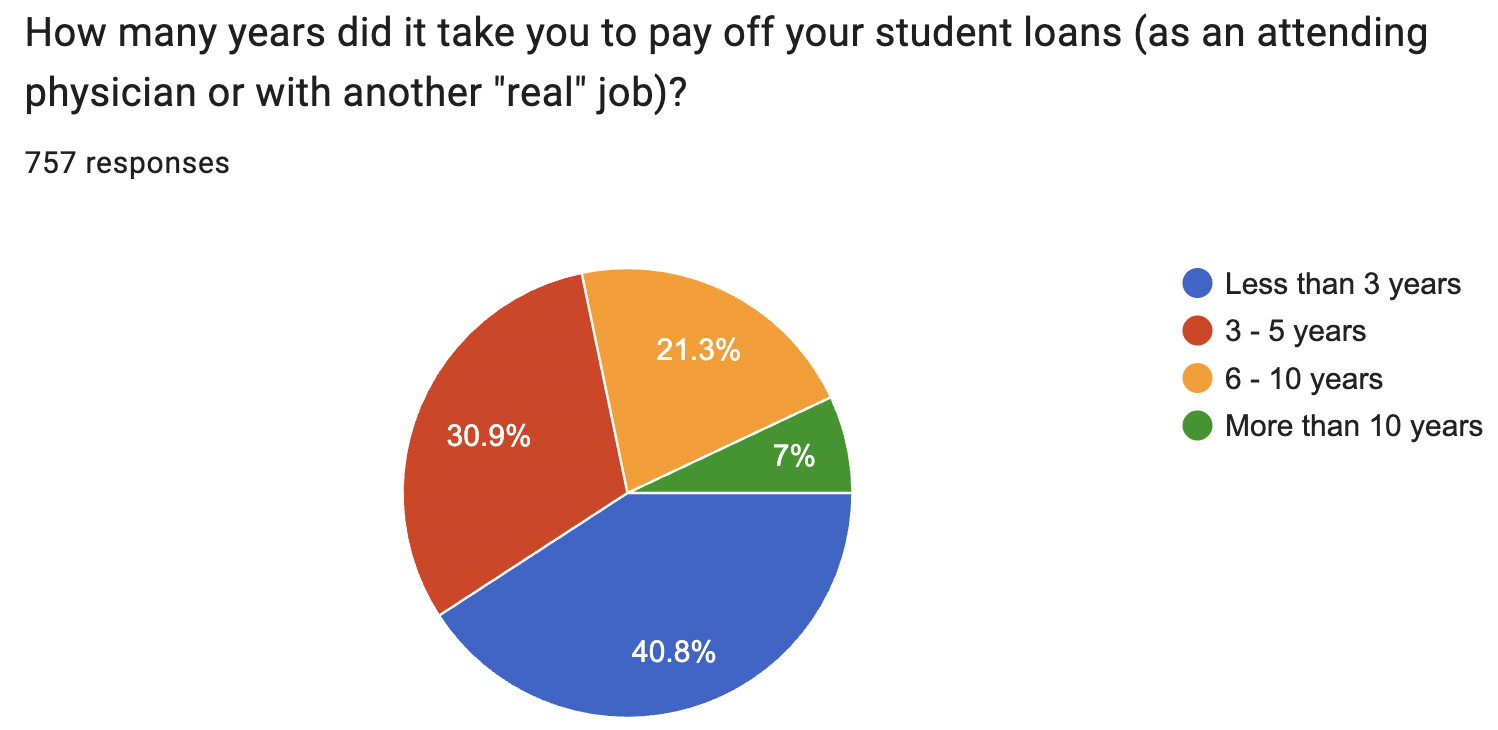

I'm so proud of all of you. Seventy-two percent knocked them out in less than five years, and 93% in less than 10 years. Well done!

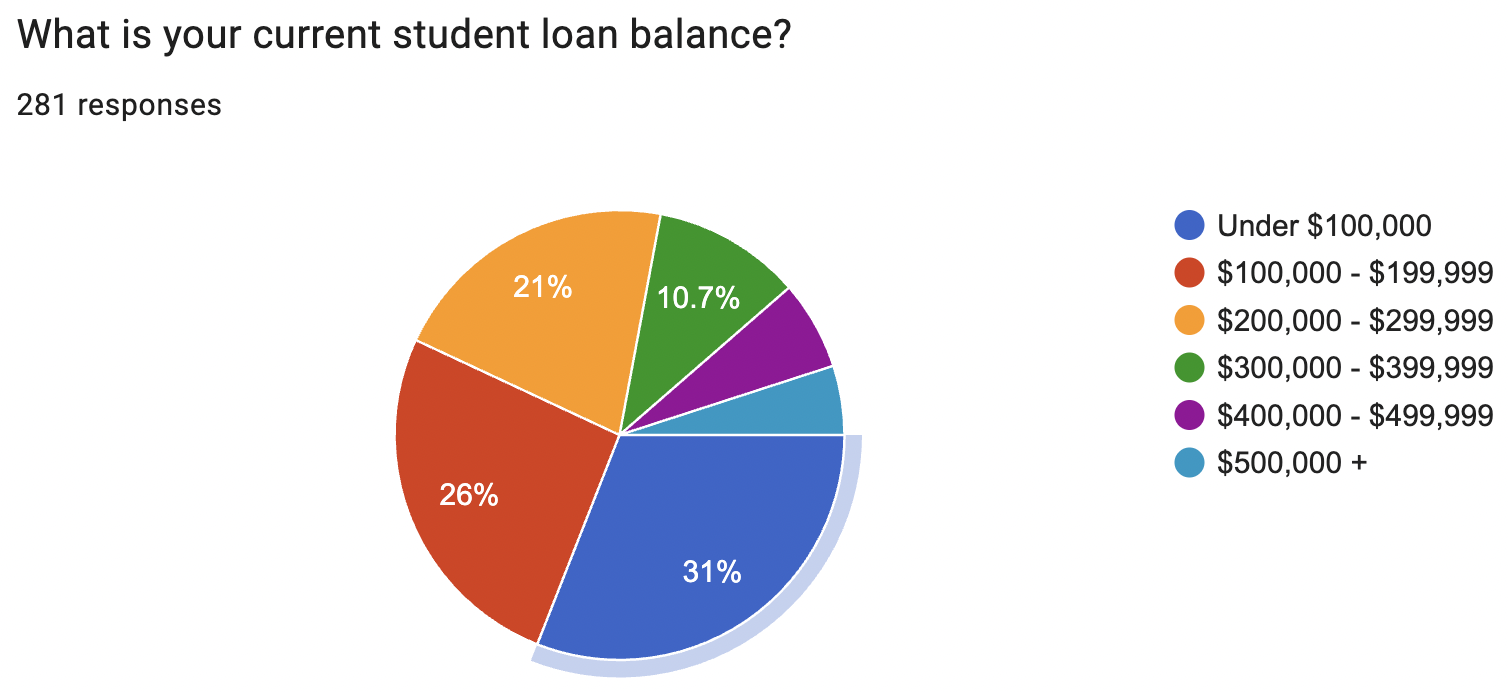

And most of those who do still have loans owe significantly less than the average physician's salary.

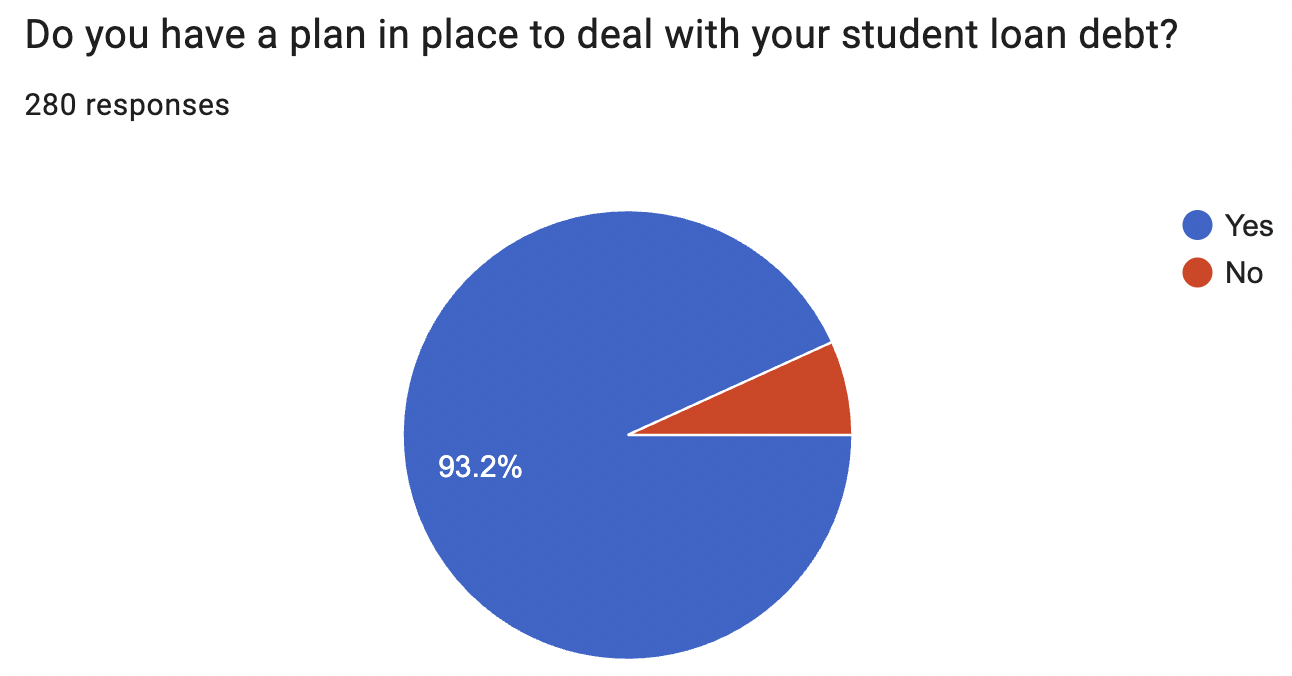

I'm trying to decide if this is a reflection of the good work being done at Student Loan Advice or if it's about to go out of business.

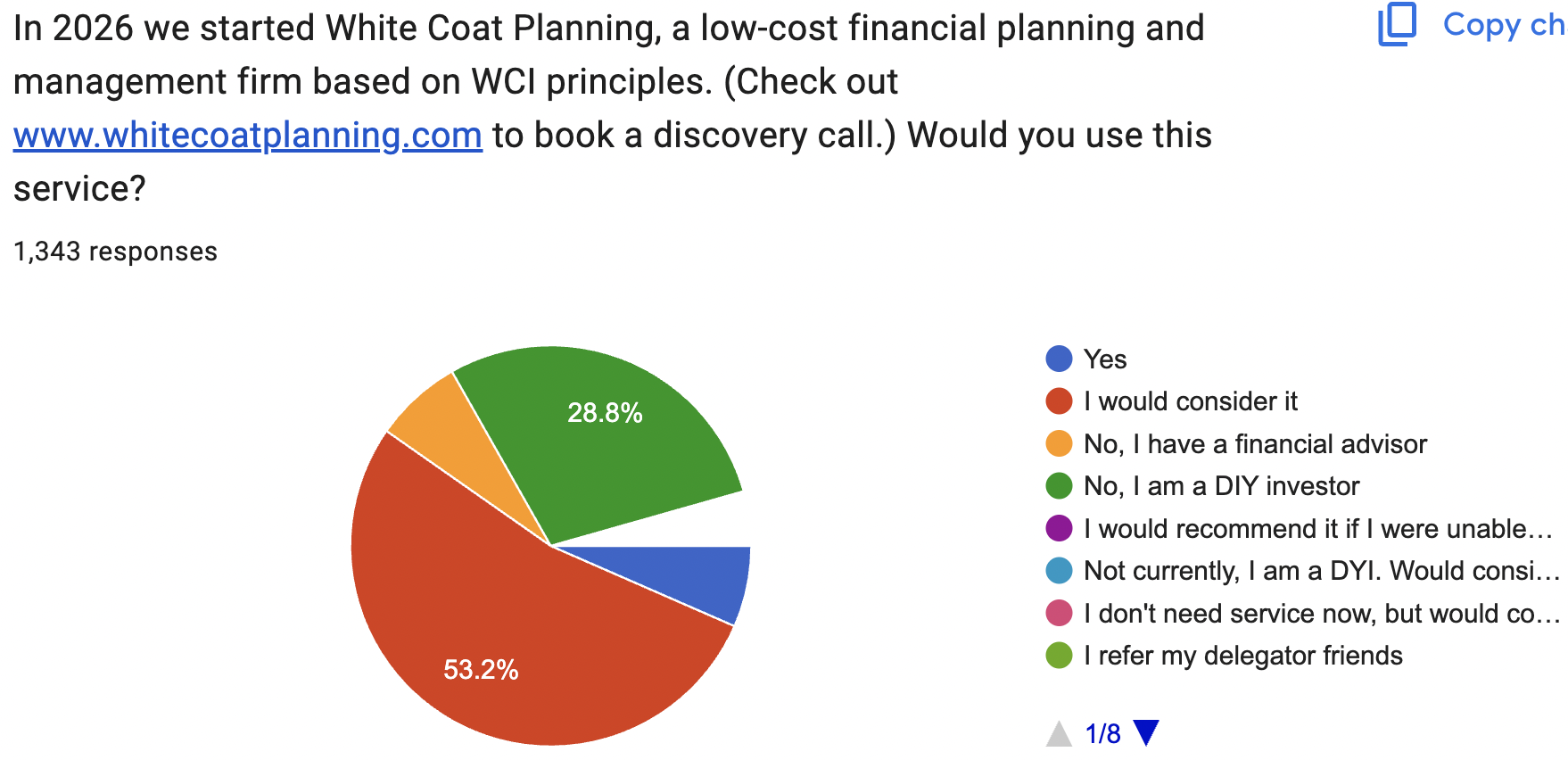

Looks like White Coat Planning will have plenty of work to do, though. Or at least there are lots of people in our audience who would really benefit from buying the Fire Your Financial Advisor course.

Maybe next year we should just do a survey of new WCIers.

Thank you for telling your friends about WCI. That “referral” is probably worth millions to your friend, just like it was to you.

The Finances of WCIers

OK, now for the part you've all been waiting for. Let's find out how you compare to everyone else who answered the survey.

Your spouse probably works.

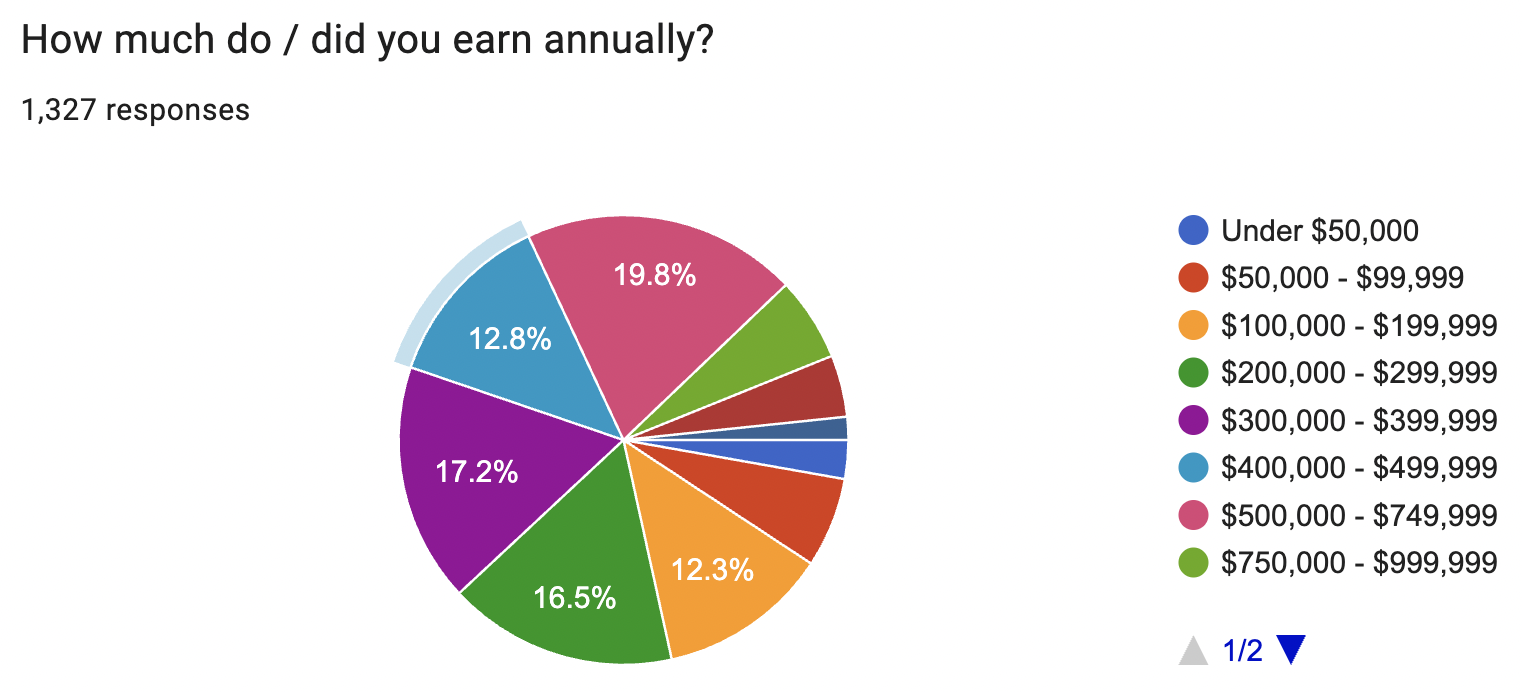

Your income is all over the place. Wherever you fall, you have company here. Especially in the $200,000-$750,000 range.

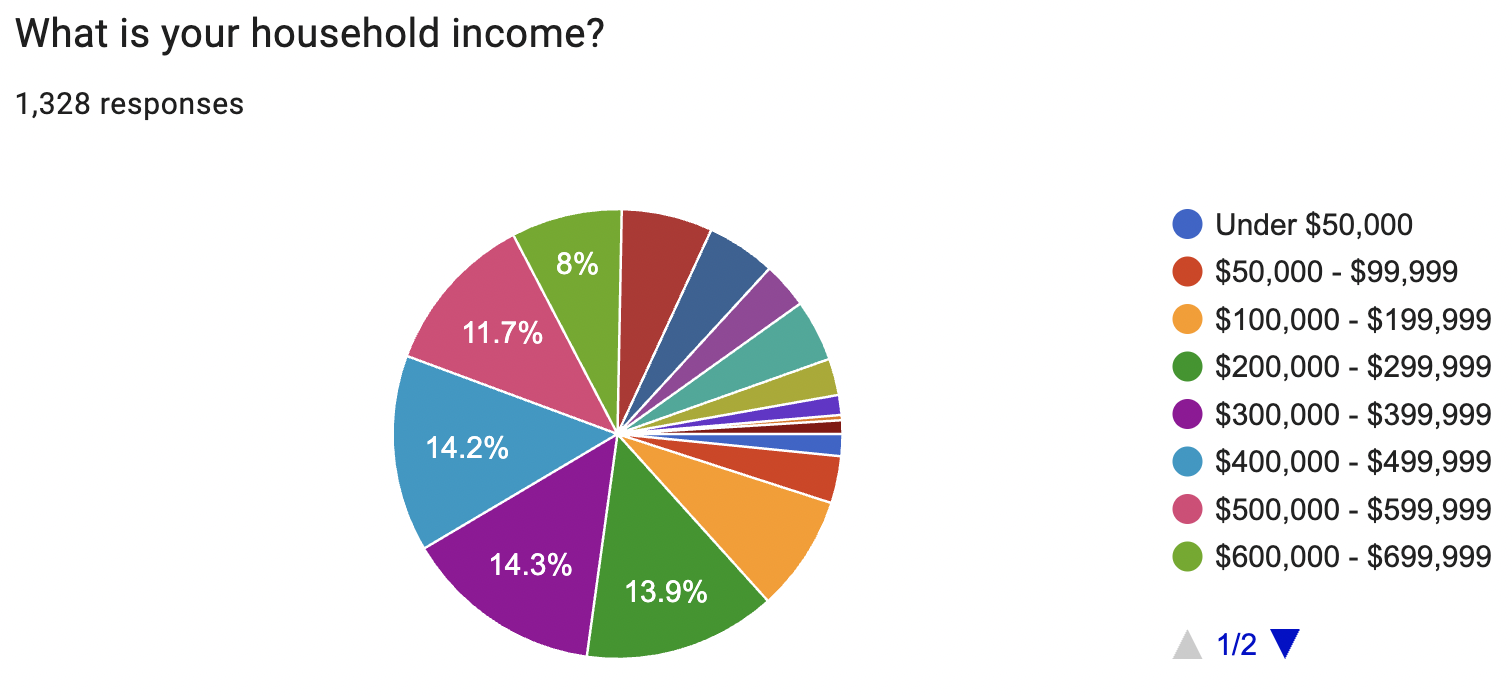

The income looks even better when you include your spouse. Almost 3/4 of you are making at least $300,000, and almost 10% of you are over a million.

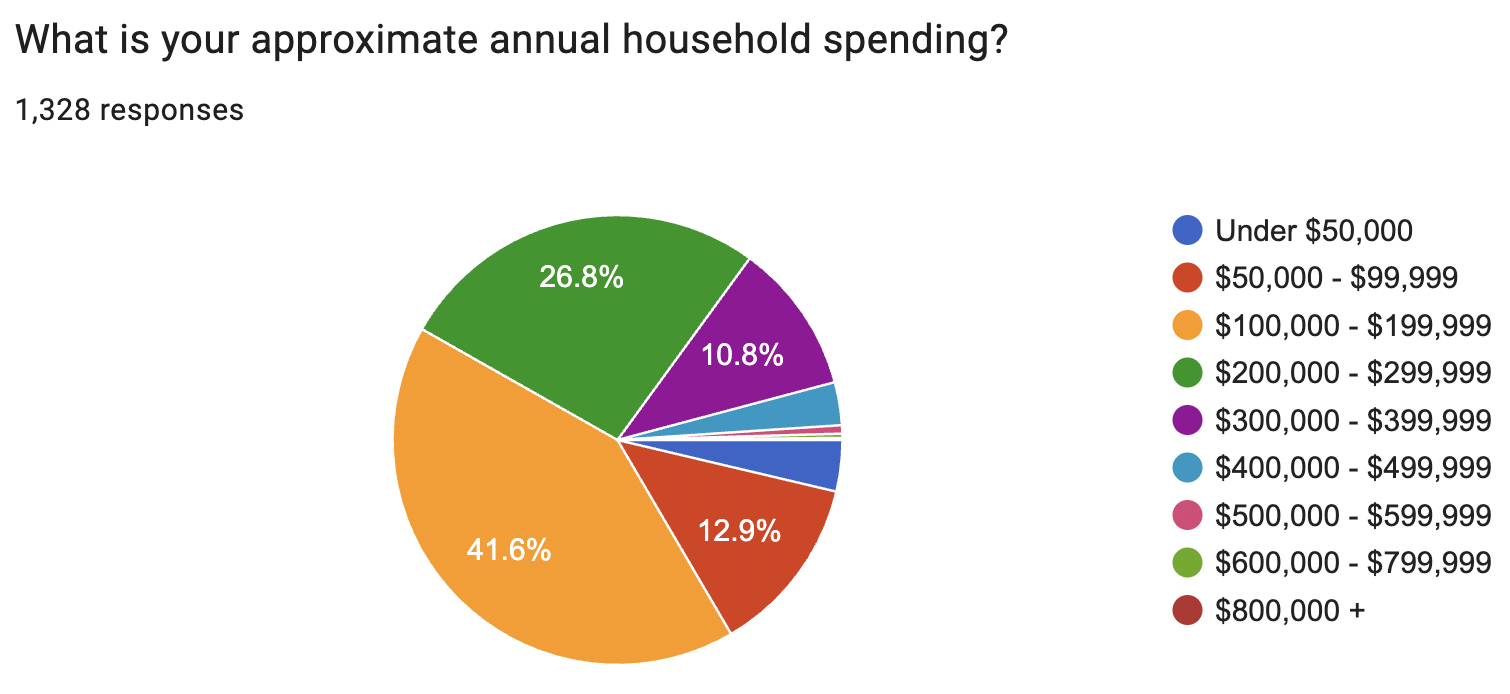

But like good WCIers, you don't spend that much. We're apparently real spendthrifts here in the Dahle household, outspending the vast majority despite not having payments. Only 1% spend more than $500,000, and about 5% spend more than $400,000.

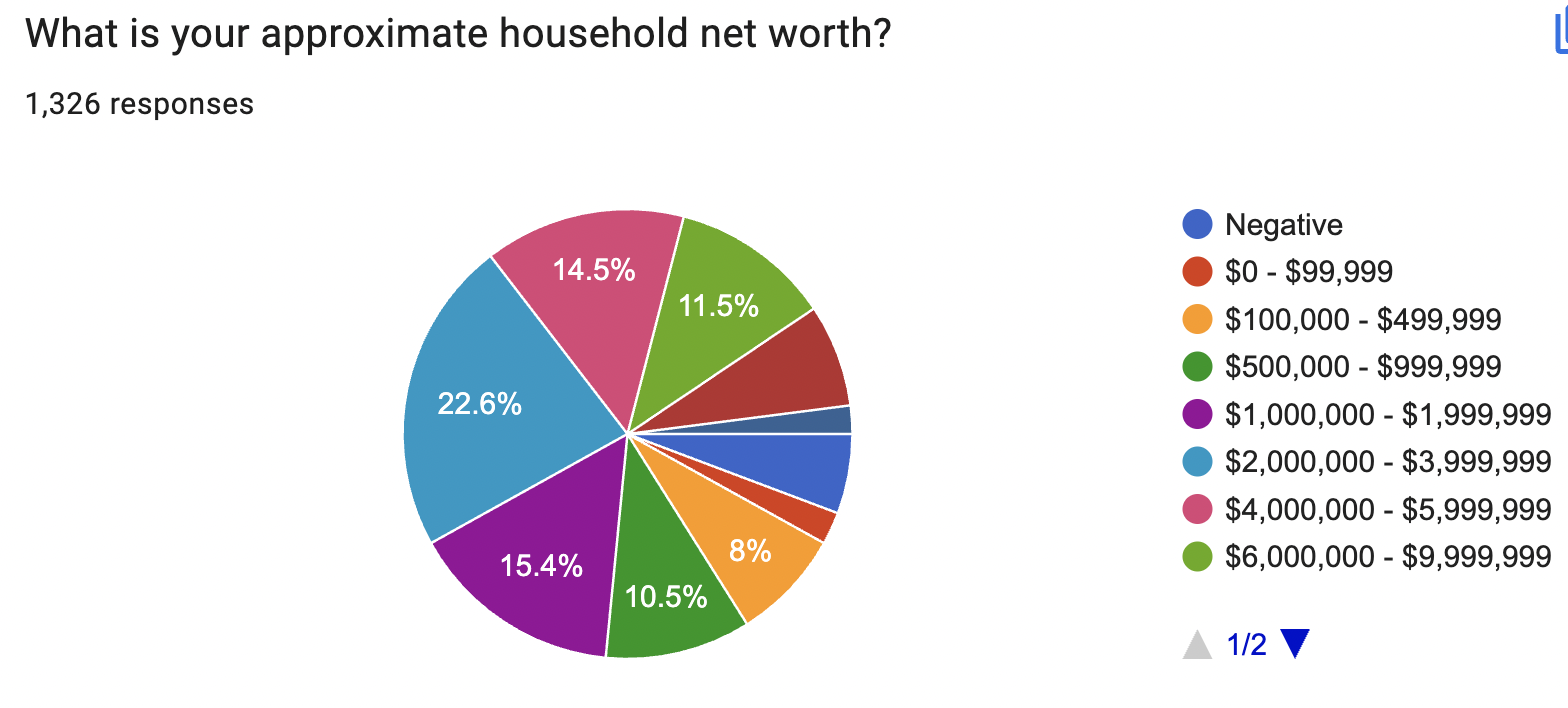

Given your incomes and your savings rates, I guess we shouldn't be surprised that your net worth numbers do not look very similar to those of most doctors. Almost 3/4 of you are millionaires, and more than half of you are multimillionaires. Ten percent of you are decamillionaires, and 2% are multidecamillionaires. It takes a lot of money to be in the 1% around here. One of the few places on Earth where the mere millionaires feel poor, I guess.

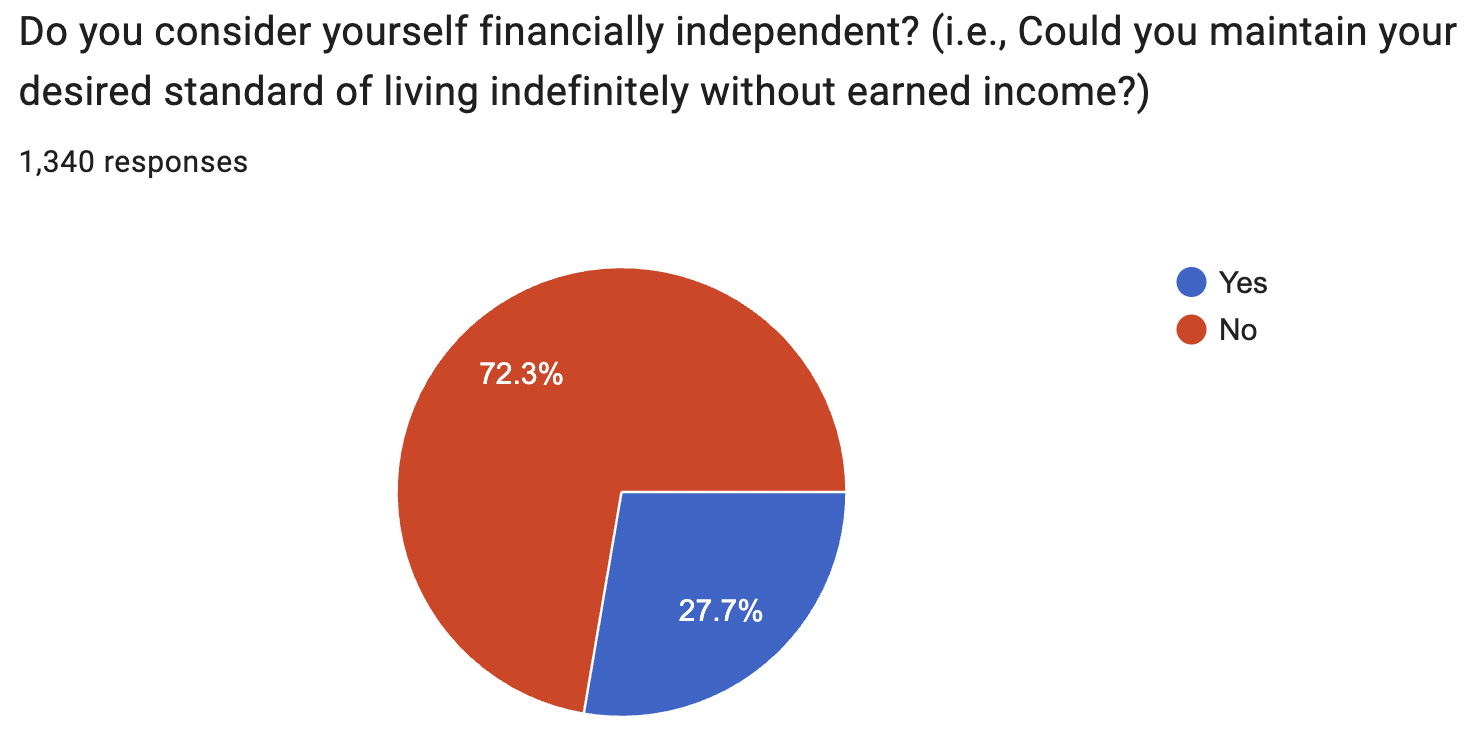

I can't quite reconcile this one with the prior charts above. If more than half of you spend less than $200,000 per year and more than 1/3 of you have $4 million+, why are only 1/4 of you financially independent? You do know how the whole FI thing works, right? Maybe we need more blog posts on that. Or maybe you all just have a big chunk of your money sitting in big, expensive doctor houses and boats or something. Perhaps we should ask about investable assets next year instead of net worth. At any rate, I'm also thrilled about this chart, because last year only 22% of you were FI, and now 28% are.

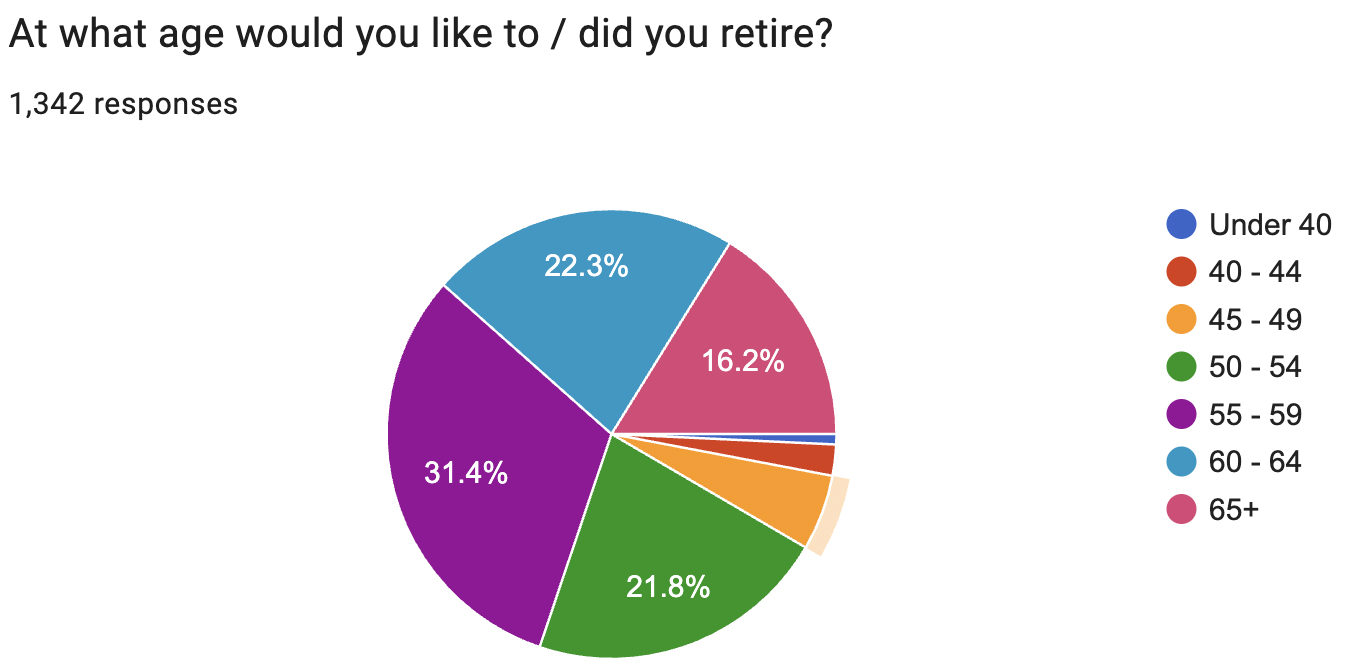

I guess it's OK if you're not FI yet, though, since most of you would like to work until at least 55, and few want to retire in their 40s.

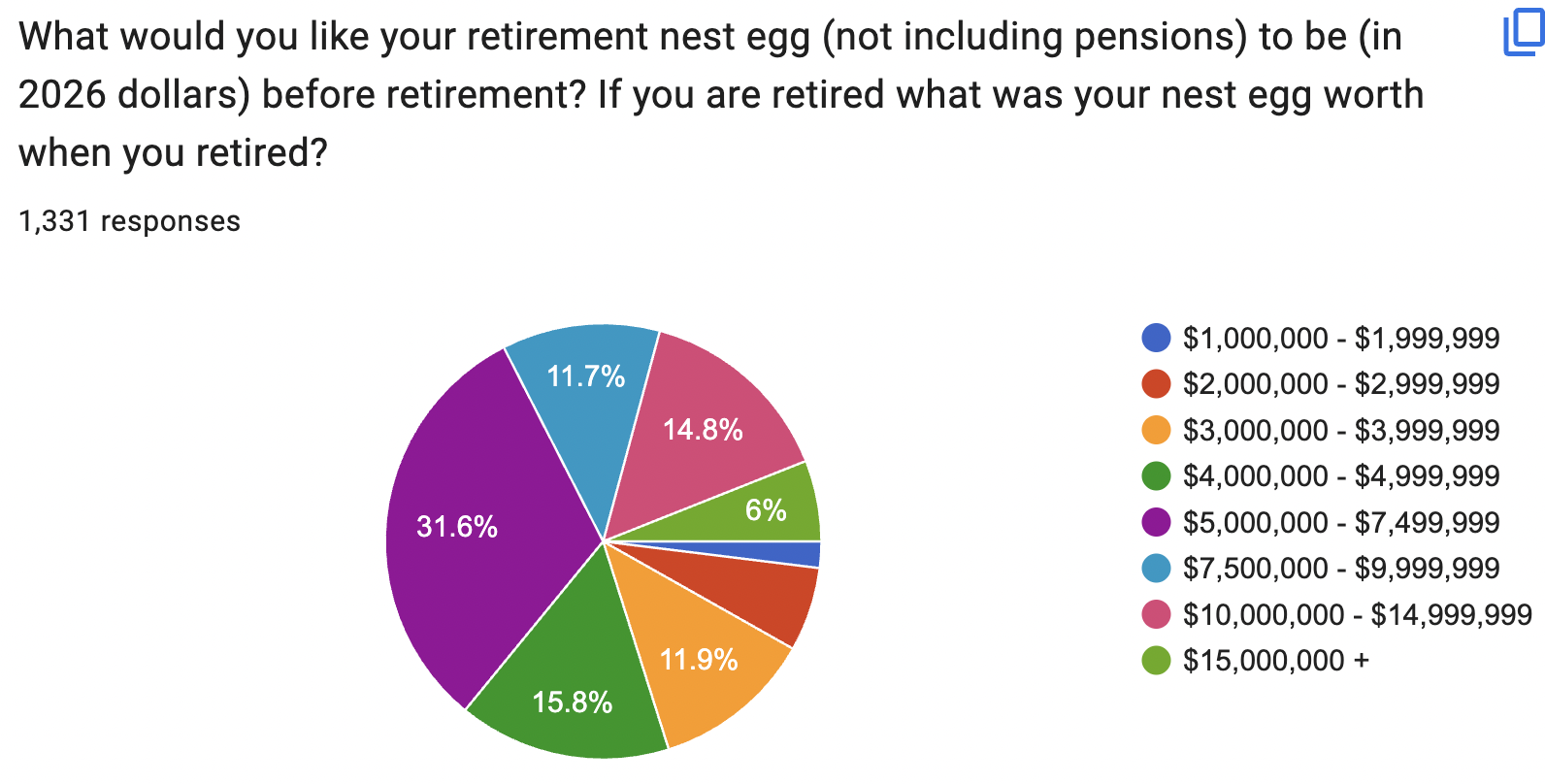

Here's another one that's hard to reconcile with your reported spending. You spend less than $200,000 a year, but you think you need at least $10 million? That's a sub-2% withdrawal rate. You certainly won't run out of money using that. Can I be your heir? I find it interesting that very few of you think $2 million-$3 million is enough, given that's how much most retiring doctors have.

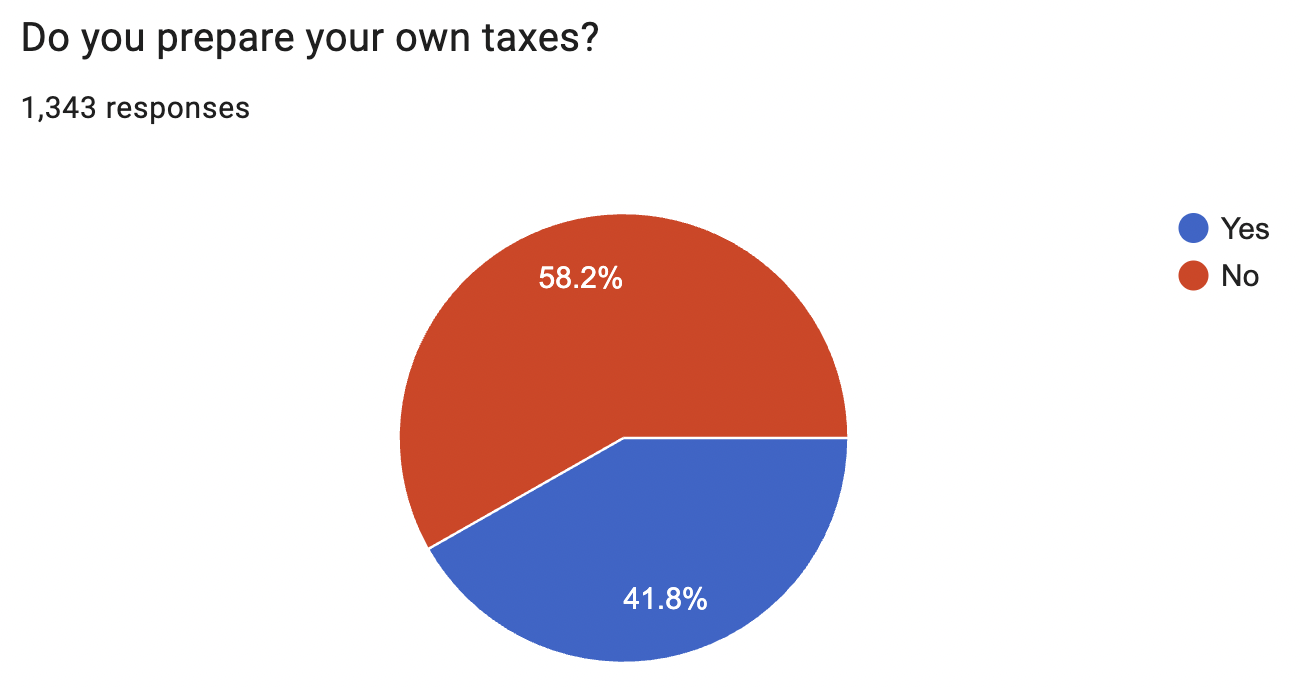

Feeling guilty about hiring out your taxes? Don't.

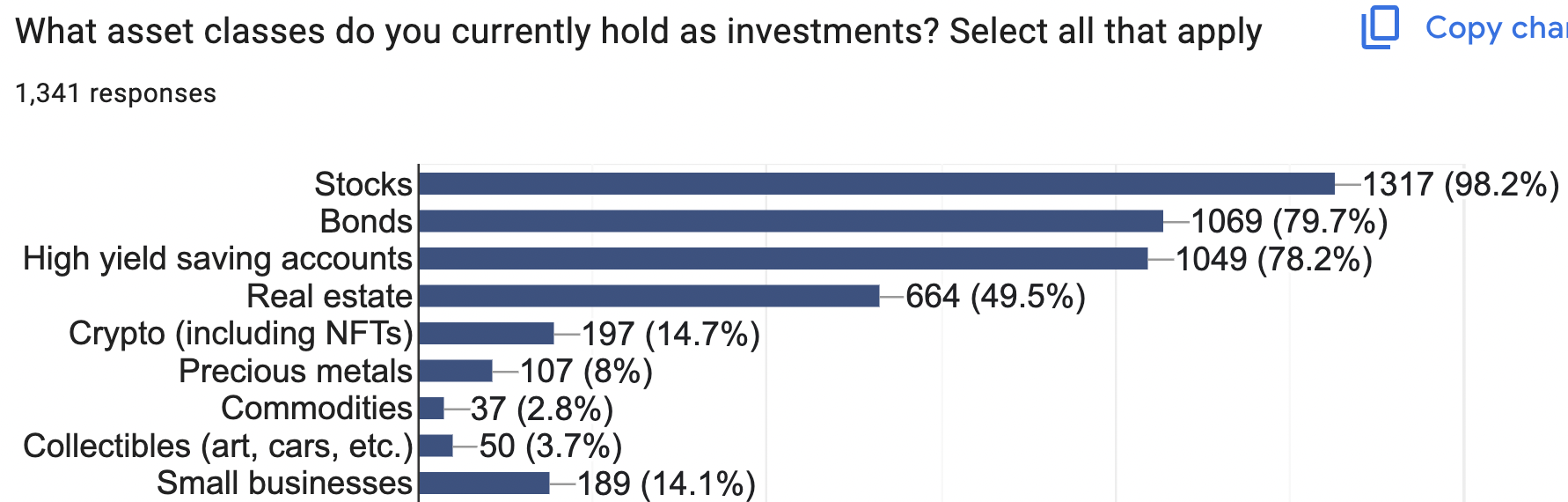

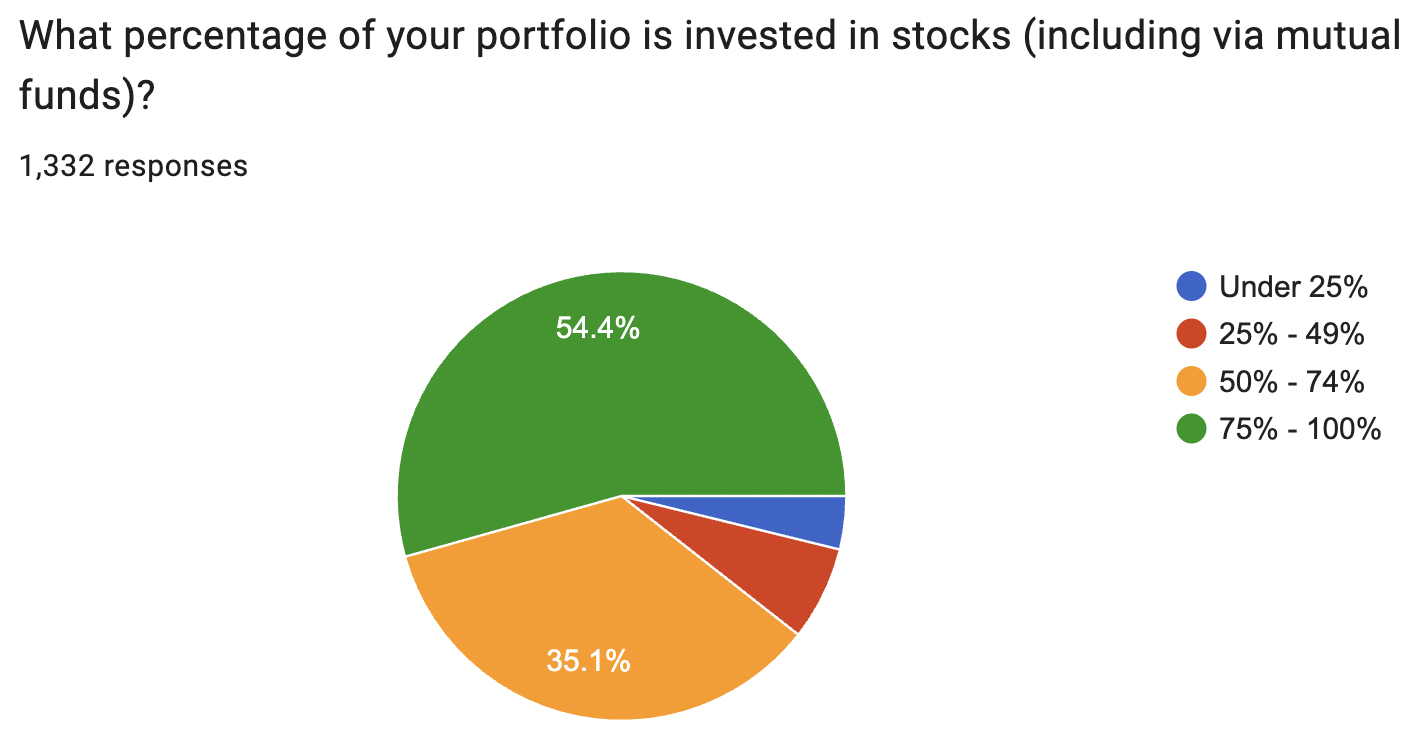

Ninety-eight percent of you invest in stocks, 80% of you invest in bonds, and 50% of you invest in real estate. Would you 100% stock folks please stop giving the rest of us a hard time? YOU'RE the minority here. But now at least WCIers can see why we have lots of content about real estate and even crypto on the site.

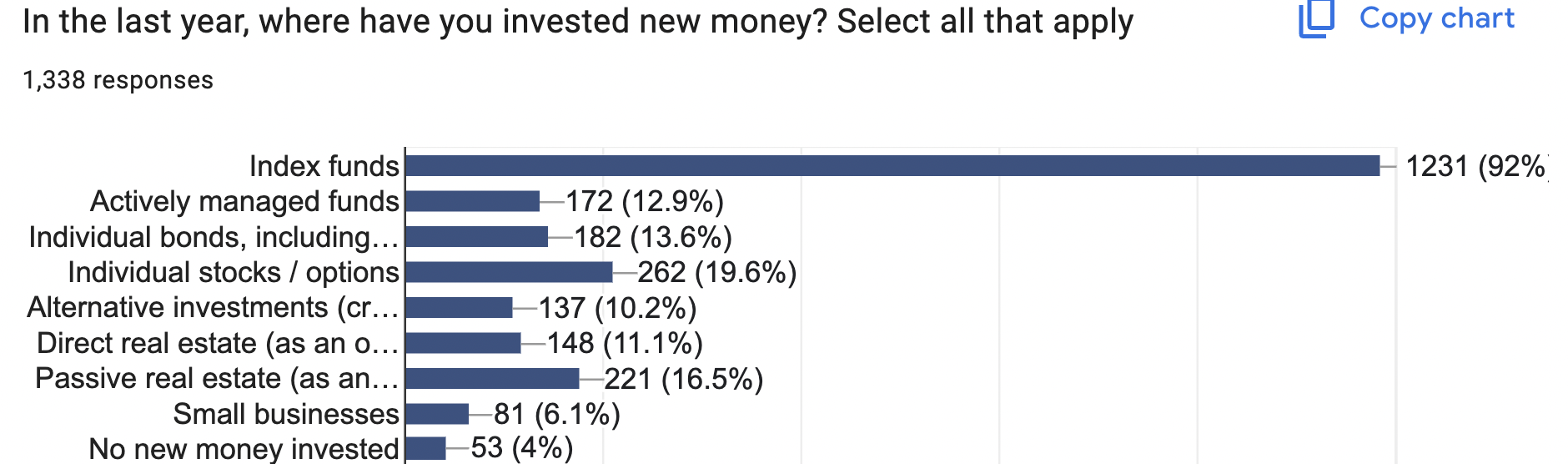

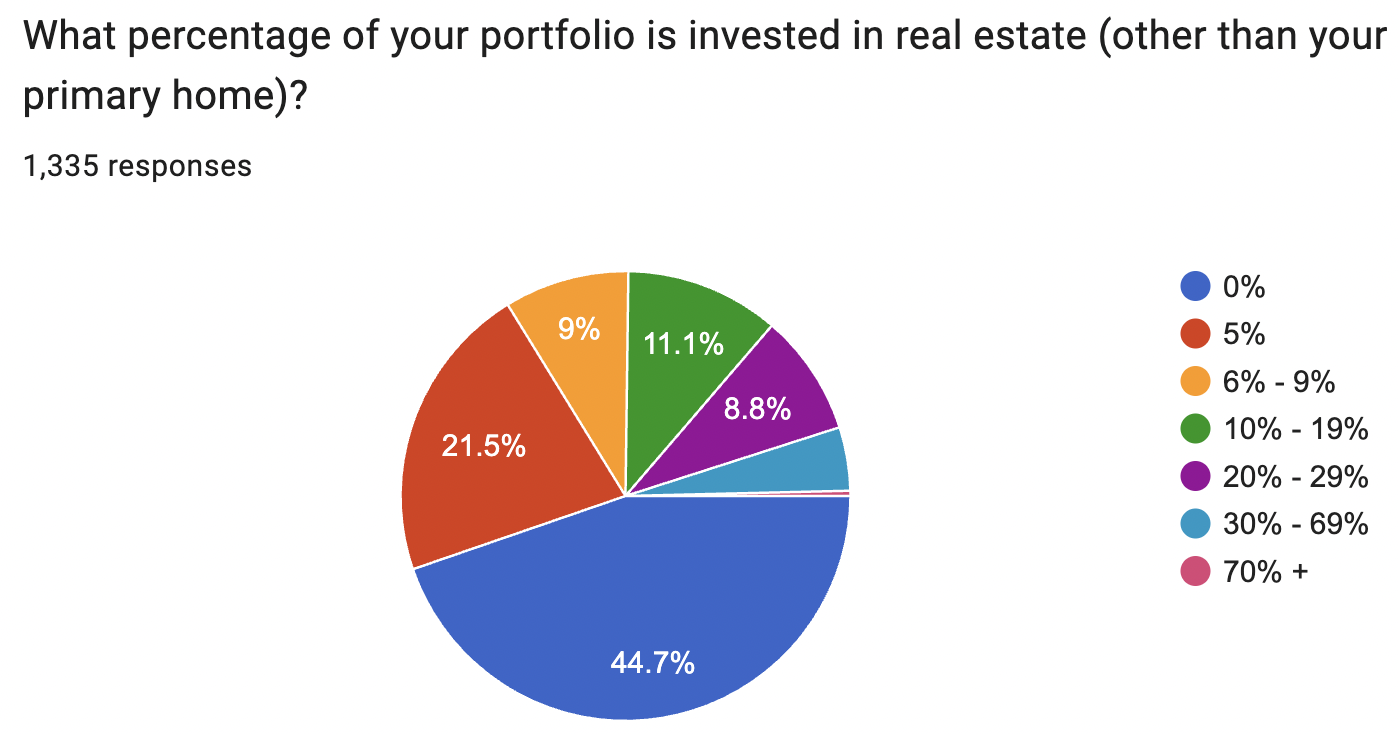

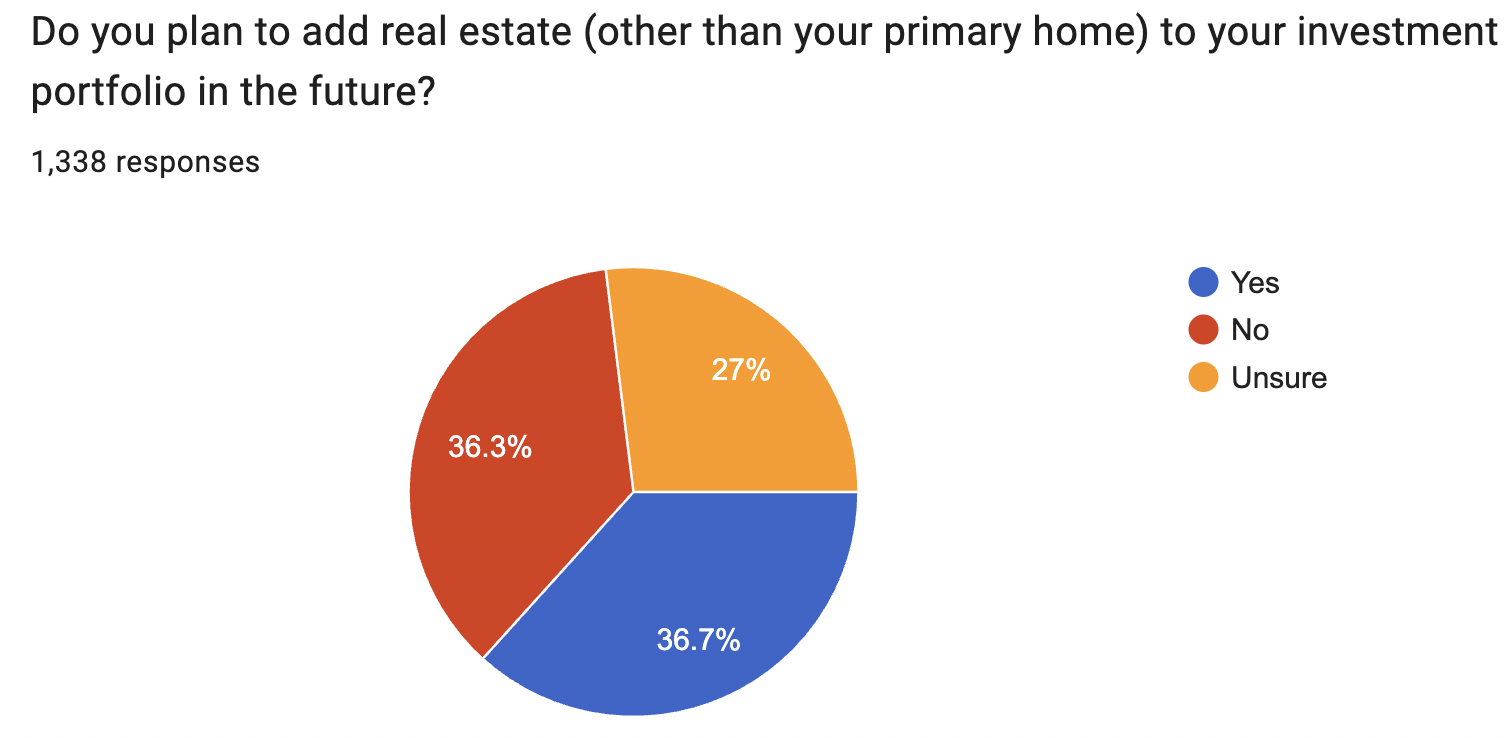

In fact, some of you have a bunch of money invested in real estate.

And a fair number are either planning to add more real estate to their portfolio, or they are at least considering it.

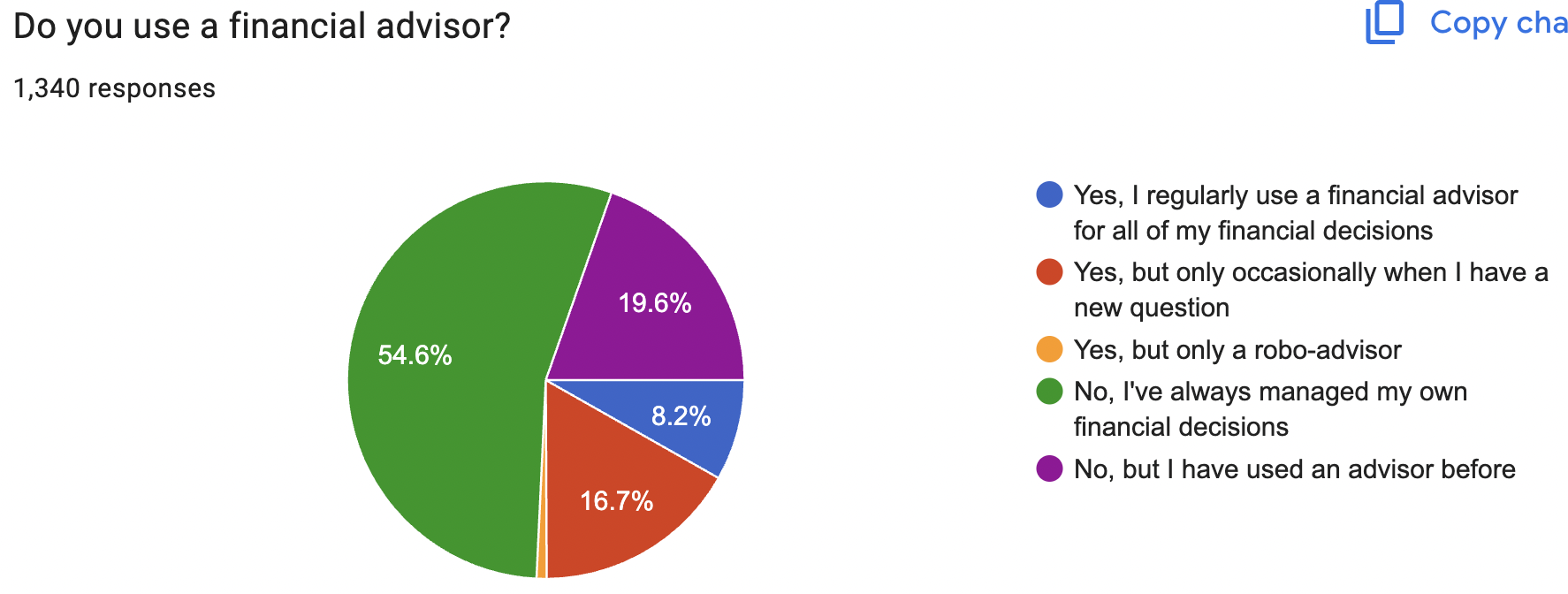

Most WCIers willing to answer this survey are hardcore DIYers. Reportedly, only 8% of you are delegators and 17% are validators.

It's hard to reconcile those percentages with the fact that 53% of you would consider using White Coat Planning. Maybe a lot of you would rather use a financial advisor, but you just can't find one you trust.

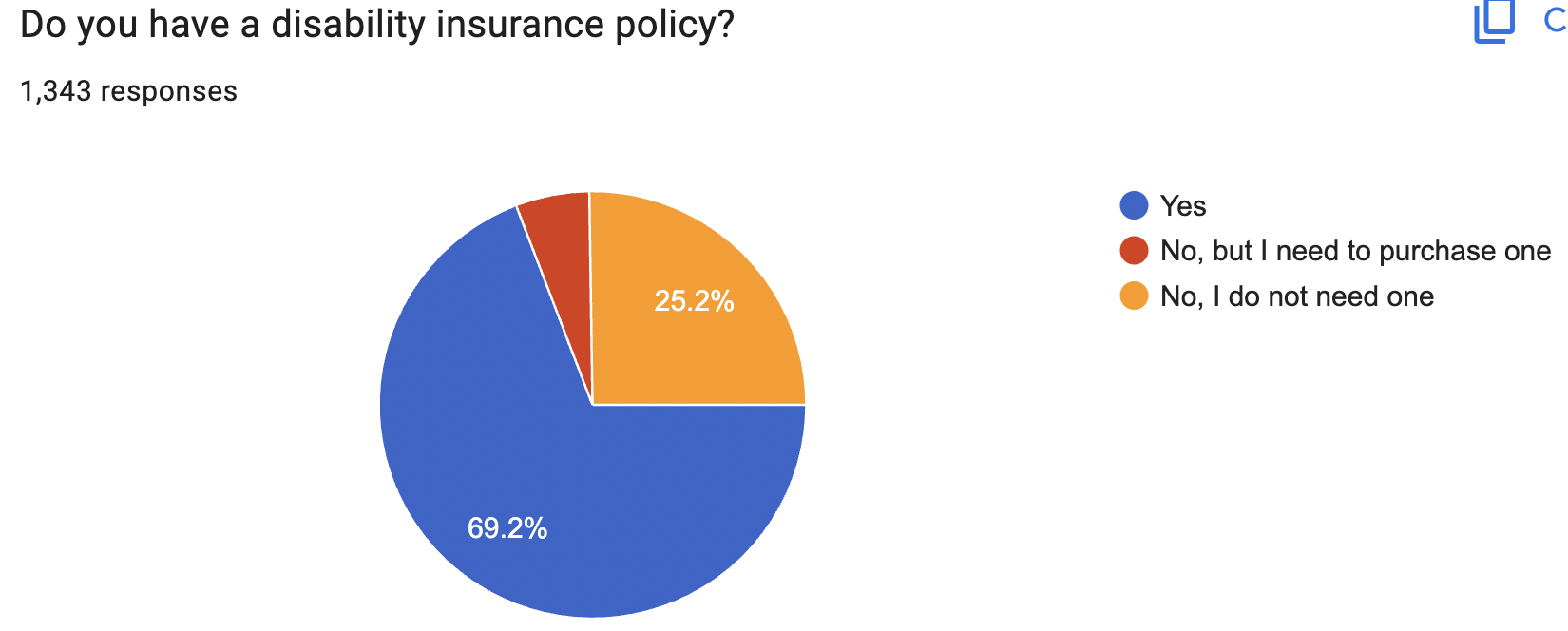

Only 6% of you have not yet purchased a needed disability policy. Bad news for White Coat Insurance. Except for the fact that 30,000 new doctors graduate each year.

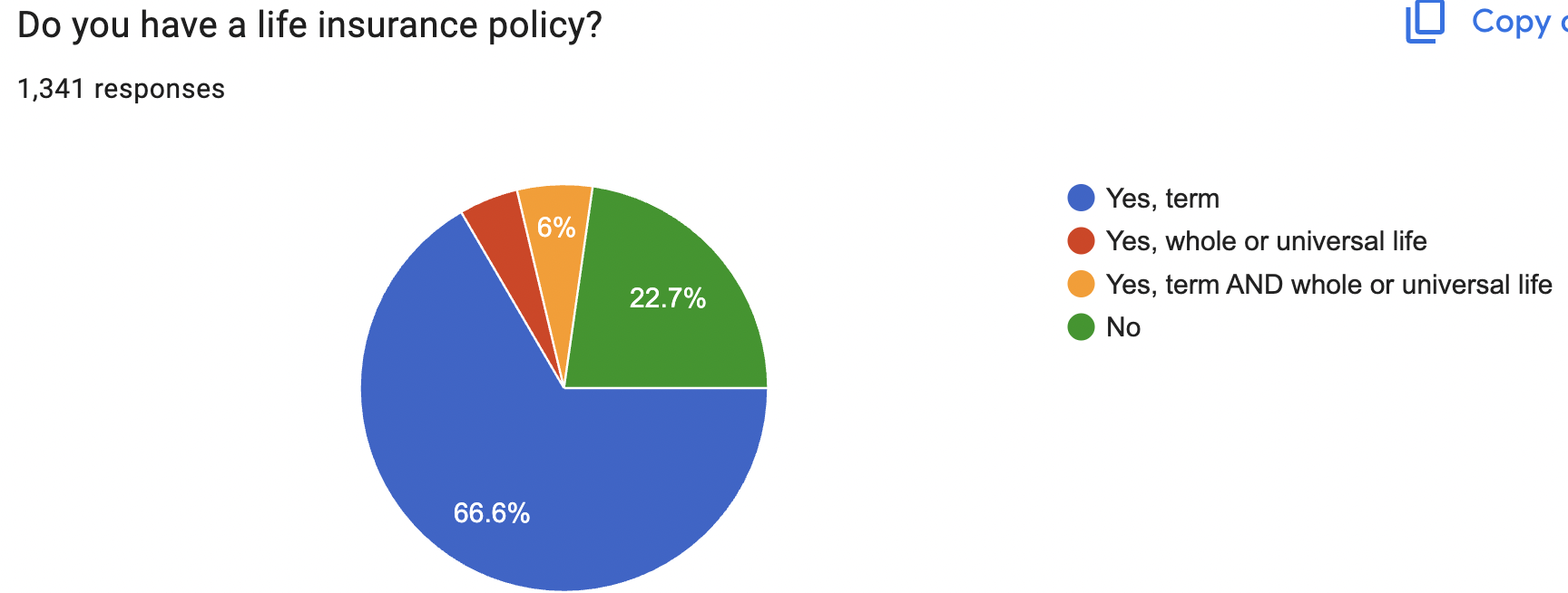

The good news, given that most of you are married, is that the number of you with term life insurance is pretty similar to the number who are not FI.

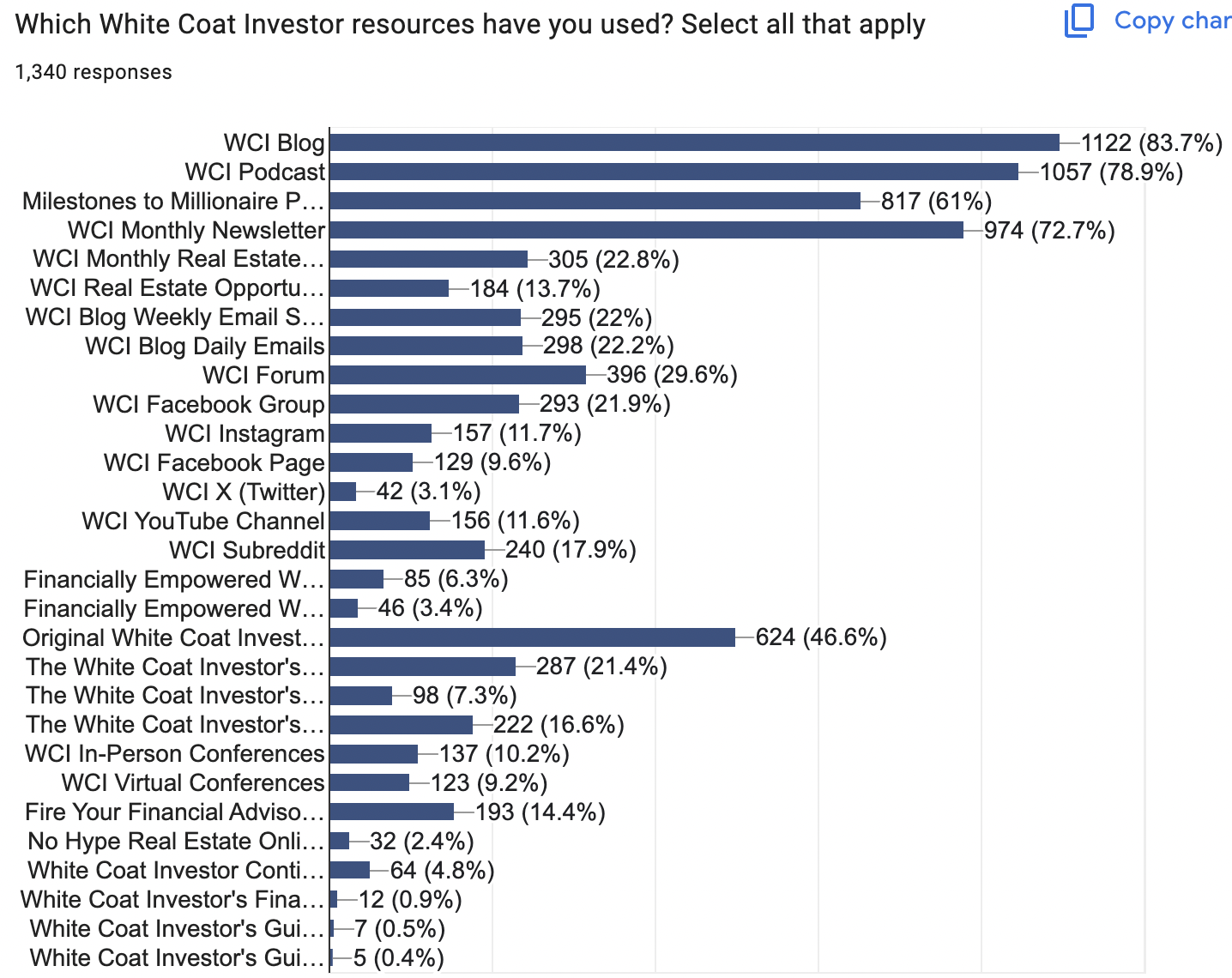

It's always been fascinating to me how many people only consume WCI content via one resource. If I don't mention something in the blog, the podcast, the newsletters, the books, and social media, plenty of people will never learn about it. Interestingly, WCI Forum and Facebook group users are more likely to answer this survey than those using the subreddit, given that Reddit is our largest community.

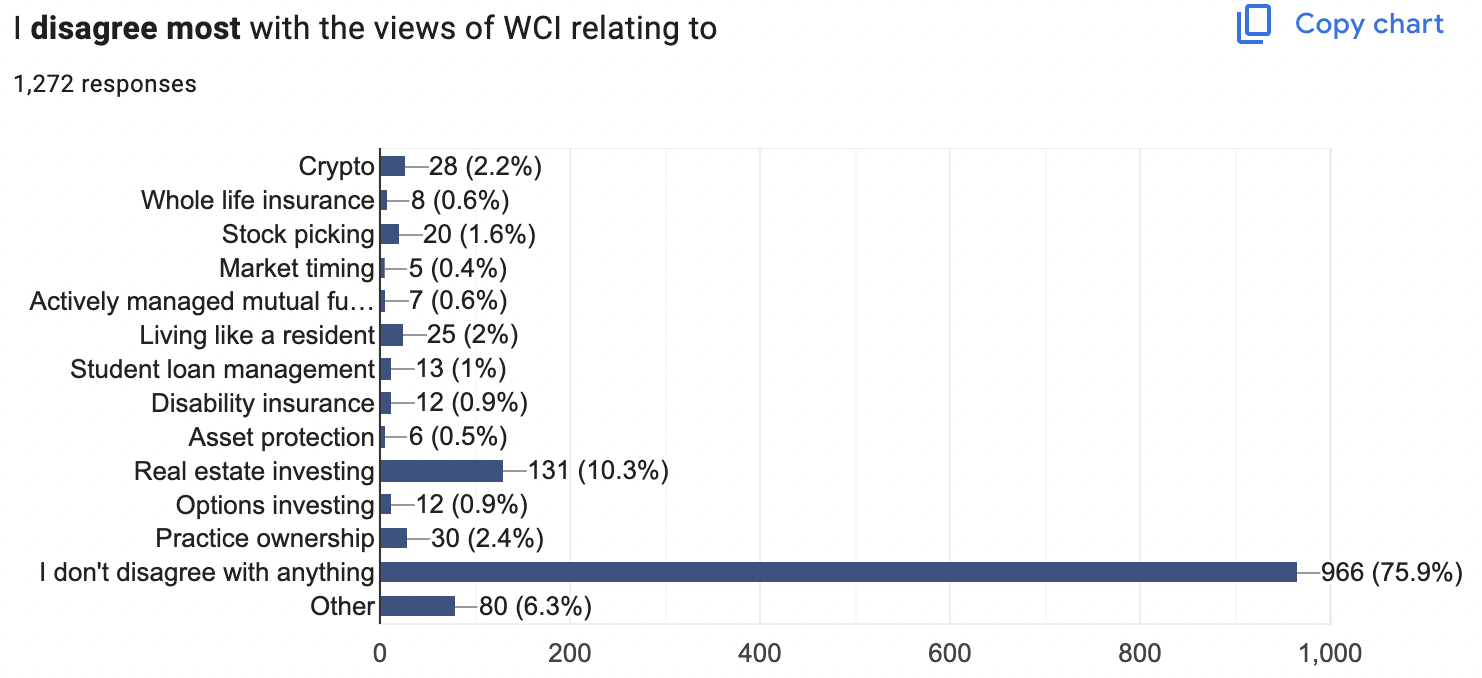

I think this question is pretty fun every year. Real estate investing won again. I'm still not sure why so many people disagree with the concept of “Real estate investing can be valuable but is optional.” I think people just don't like ads, and real estate investments buy more ads than index funds. Apparently, a few of you think I should advocate more for stock picking and whole life and options and Bitcoin and actively managed mutual funds and not living like a resident. Don't hold your breath.

But if you limit it to 5% of your portfolio, don't expect too much criticism from me about your pet asset class. I am curious what it is that six of you don't like about our views on asset protection, though. Send me an email with details if you're one of those.

The Feedback We Value Most (Negative)

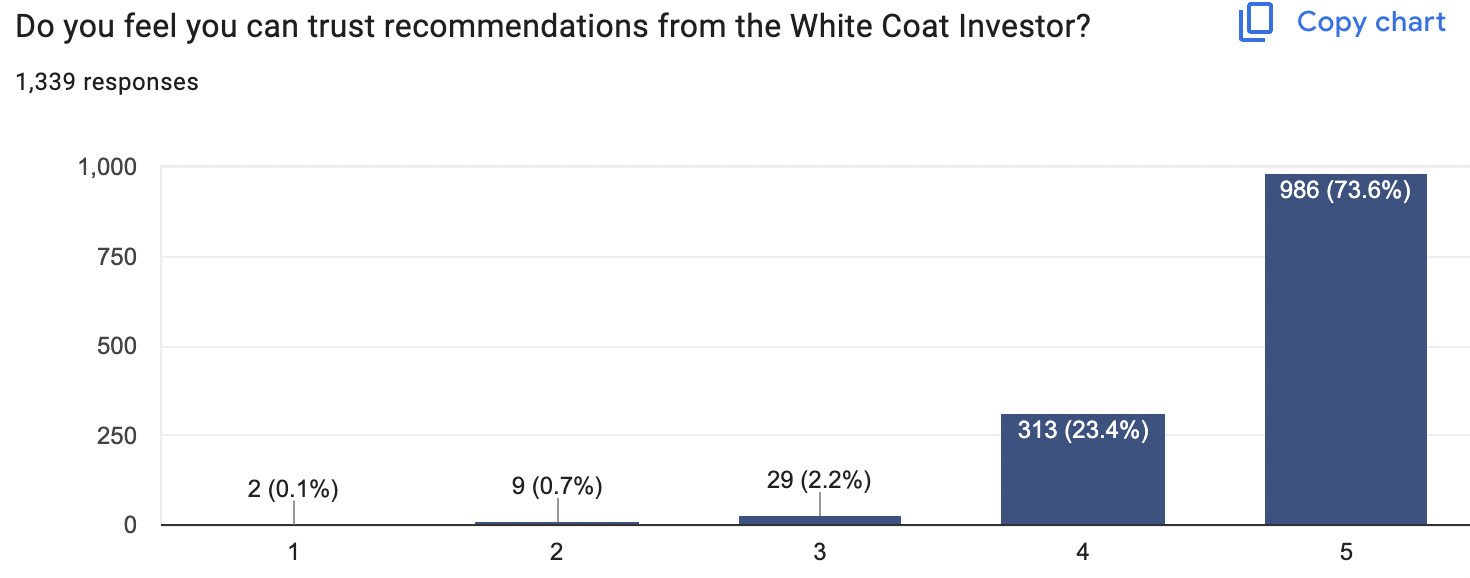

We know our most valuable asset is your trust, and we do all we can to deserve it. We will never do anything purposely to cause you to lose faith in us. I guess we're doing OK, but there's always room for improvement.

I hope the 2-11 of you who were disappointed have or will provide more details privately. Your opinions are particularly important to me.

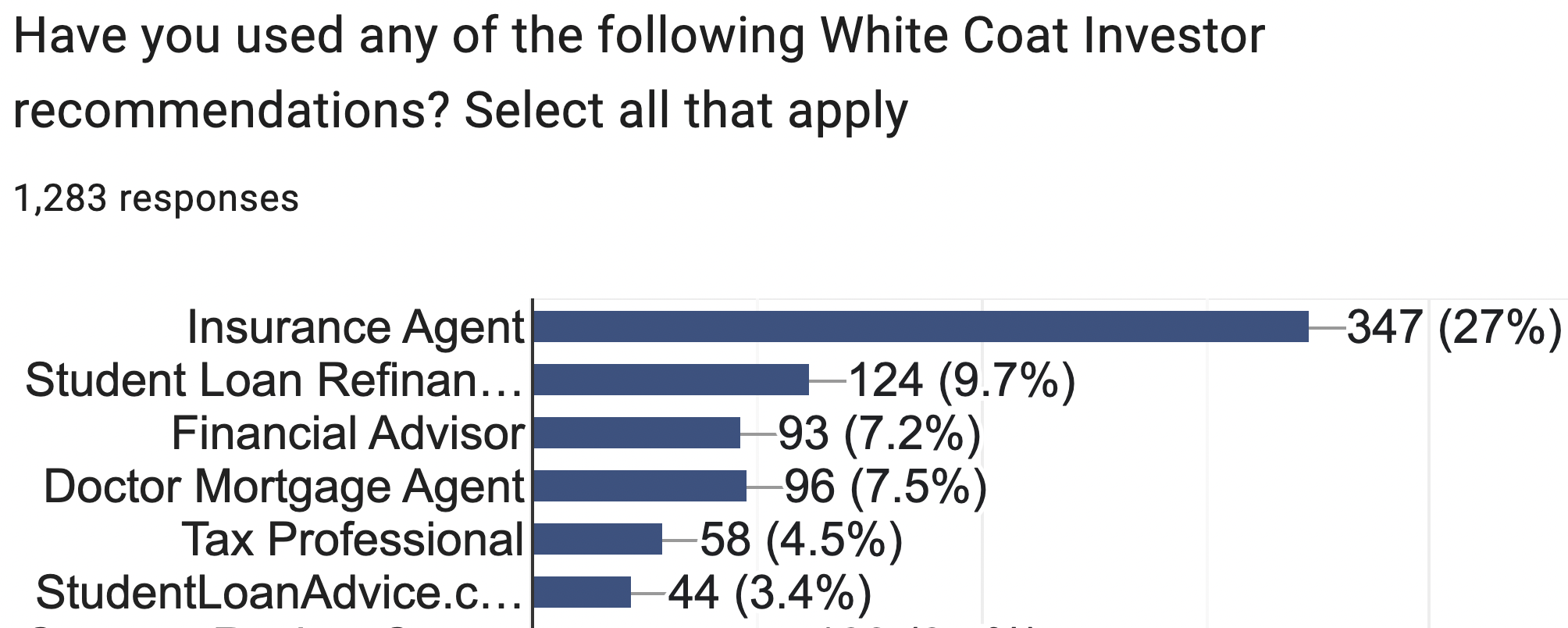

Sorry about the formatting on this one, but I'm thrilled that only 41% of you have never used an advertising partner of ours—whether that is an insurance agent, student loan refinancing, mortgage lender, financial advisor, or just taking a few paid surveys. I love that we can provide all this great content for WCIers free of charge, thanks to these partners.

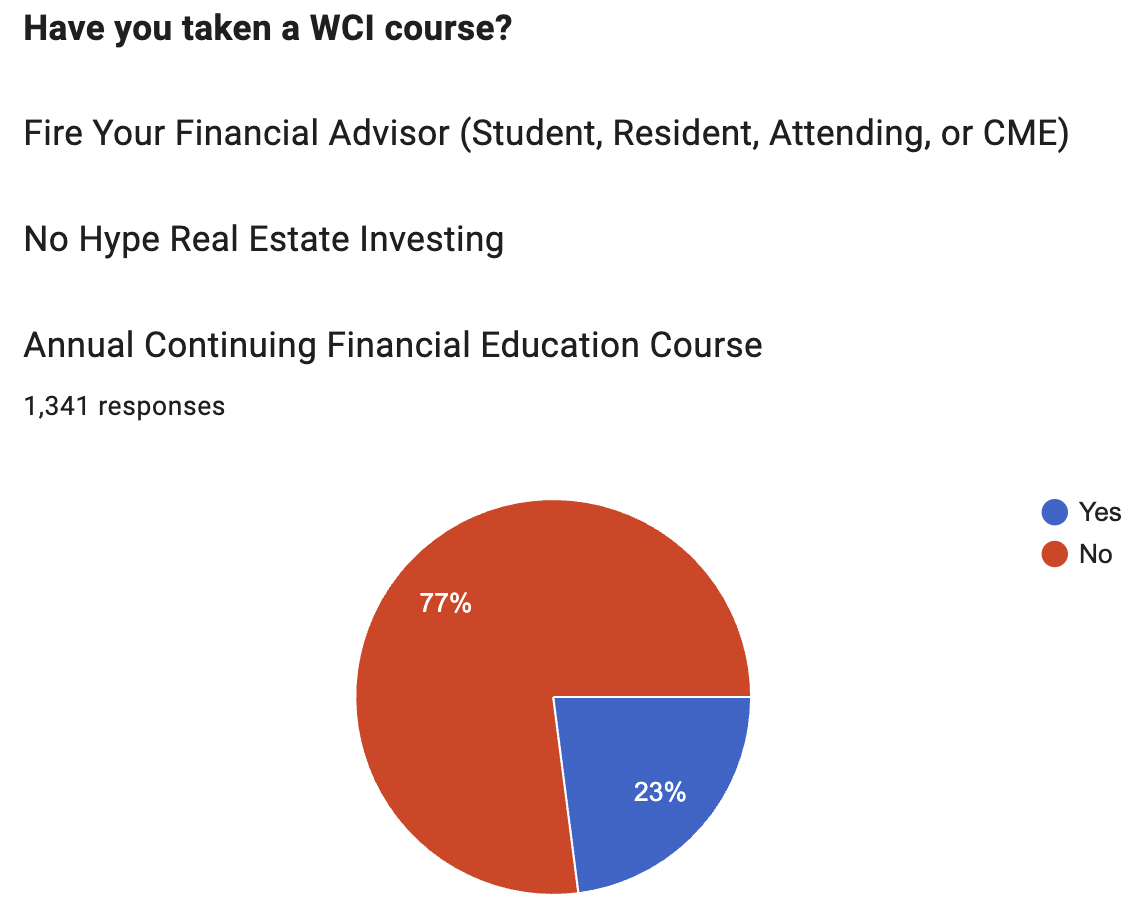

I'm so happy to see this number so high, since those courses represent a ton of work to put together.

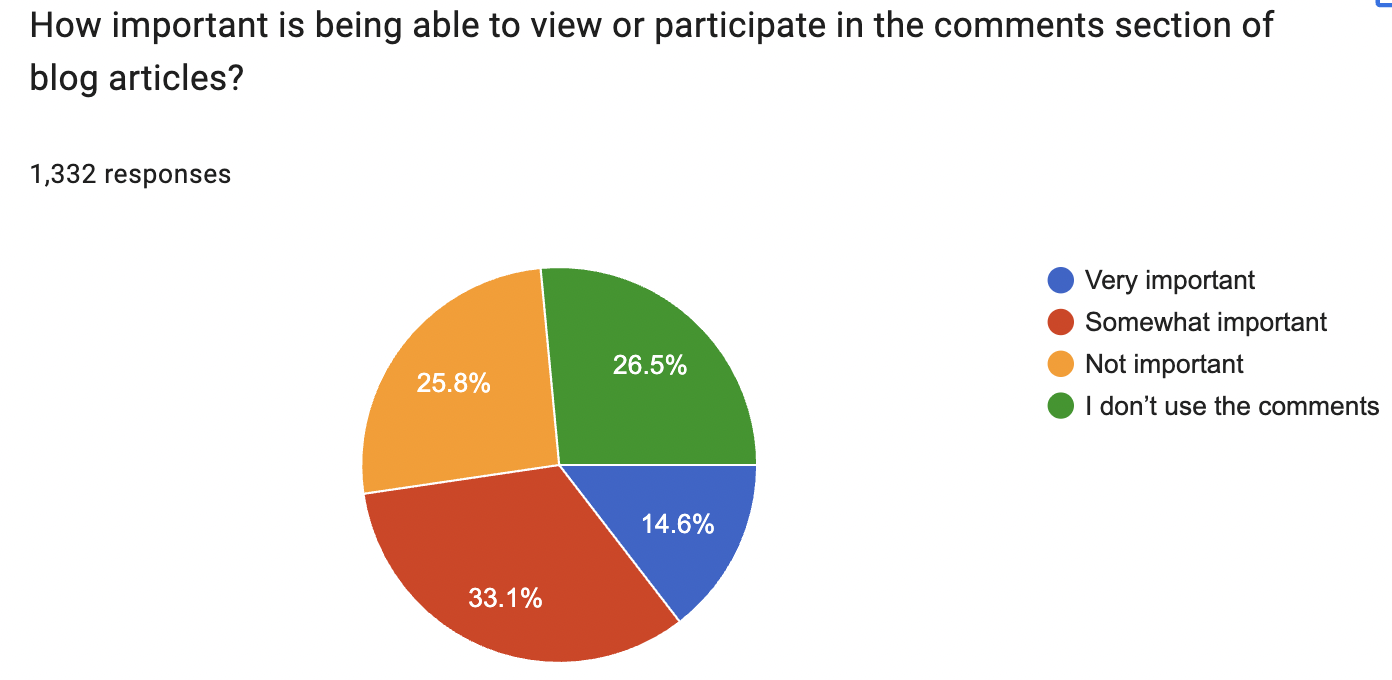

Sometimes we consider turning off the blog comments. Bad idea, I guess, since some of you really like them.

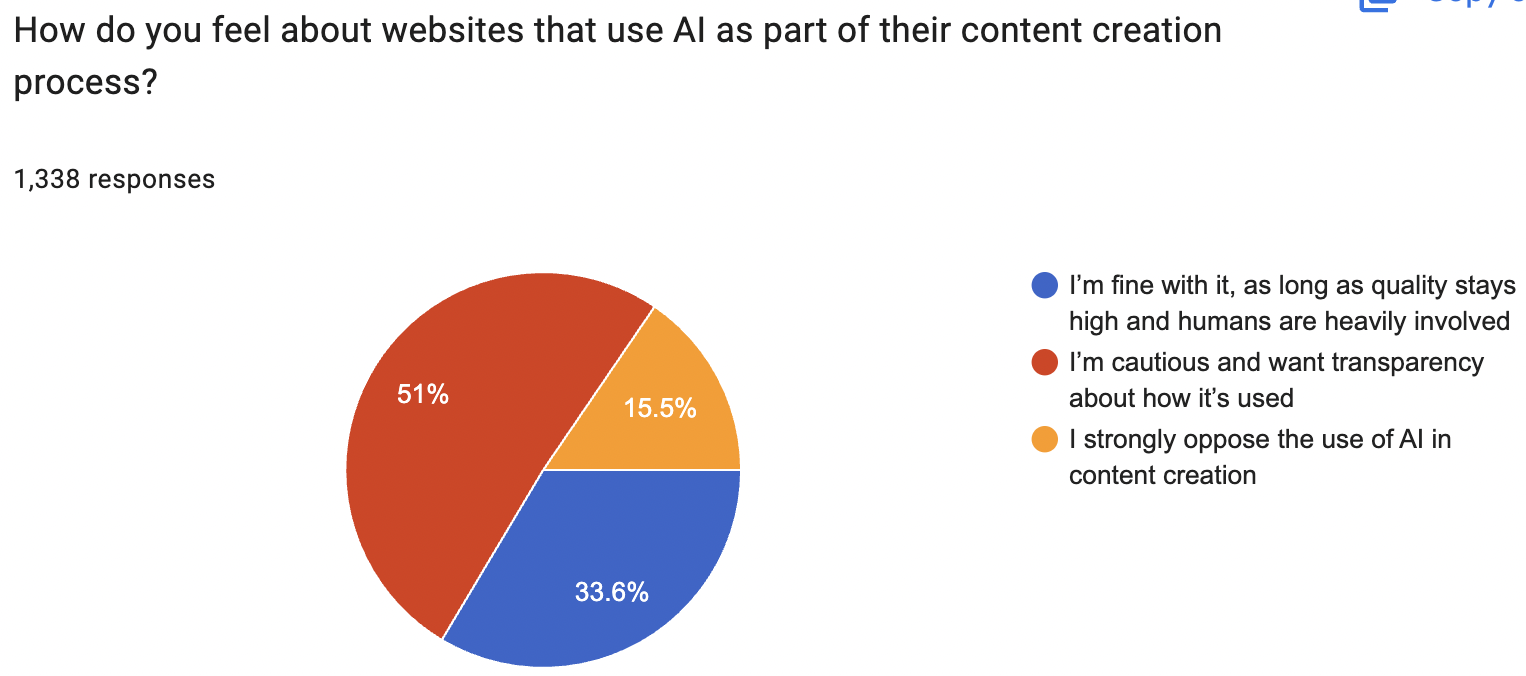

This is another great piece of feedback to have as we weigh if and how AI gets used around here.

We asked what topics you would like to see covered in the future. There were lots of useful responses. Here are some that made me chuckle:

“Jim's net worth updates, I liked seeing those.”

You mean like that book that was published in 2014? That net worth update? I'm pretty sure that was the last time I published my net worth.

“Looking back, I think specialty selection for medical students is CRITICAL. And not emphasized nearly enough. I just don’t think there are any experts out there with good, evidence backed data on fit.”

Average salary data is readily found and provided on WCI, but I'm not aware of any evidence-backed data on fit out there. If you are, please send it our way.

“Cutting edge investment forecasts.”

Let me peer into my cloudy crystal ball.

We also asked about your biggest financial worry. Provided answers included: none, taxes, Trump, student loans, inflation, retirement/decumulation, burnout, asset protection, buying a house, overspending, scarcity mindset, spouse indifferent to finance, frustration about just having to follow the plan for years, market volatility, and teaching finance to kids.

We asked what financial mistake you most wish you could help others avoid. The most common answer, by far, was overspending, as it should be. There were several pages of answers (906 total), and only one or so per page was something besides overspending. There's a lesson there.

We asked how we could better serve you. The most common answer was “there's nothing more you can do,” but we did have many requests ranging from “quit using the term APC” to “don't quit” to “be nicer to California” to “fewer ads” to “more politics” to something a bit more heartbreaking like:

“Never stop saying thank you for all that you do. I’m an ICU doctor, often you're the [oomph] I need to walk in the hospital doors.”

And lest we forget that WCIer incomes are all over the place, there was this:

“Jim often claims people complain that too many people he interviews are ‘million dollar a year earnings' who ‘haven't made any financial mistakes.' As someone who fits the profile of very high earner, high saver, VVHCOL area, I wish there was more content for ‘very high earner problems.'”

and this:

“Sometimes episodes cater to super wealthy.”

and this:

“I appreciate the diversity of docs you have come on. Please show more people in New England, no matter the income.”

and this:

“Feature docs that make more mistakes, too many over achievers!”

It's hard to have every post and every podcast episode applicable to every person, I suppose.

My favorite response was “A WCI Video game.” I wouldn't hold your breath.

We asked how WCI had made a difference in your life. Then we cried as we read your answers like these:

“I’m so grateful to Jim and the team. I felt hopeless about my finances and I didn’t know where to start. Talking to the ‘doctor' financial advisors felt like going into a crooked mechanic. After I heard about WCI and heard the first podcast, I nearly cried when Jim said, ‘Keep your head up and shoulders back—you’ve got this.' I felt like I finally found an honest financial guide who knew what I was going through.”

“Massive impact. We have a financial plan, I cut down to working less than full time in a job I love. As people who grew up with no financial education/bad advice from parents, WCI has been instrumental in our success.”

“Hugely. WCI has helped me avoid the big mistakes in financial adulthood. I’ve negotiated my pay. I am informed about insurance and pay a fair price for the insurance products I choose to purchase. I didn’t buy too much house even in a HCOL area. I have followed an automated, low cost, broadly diversified investment strategy, and have pocketed and compounded the difference in fees that I would have otherwise paid to an advisor. I have informed myself of relevant tax reduction strategies and made consistent use of all retirement accounts, from 403(b) to Backdoor Roth to 457(b) to HSA to taxable. All of this is on auto pilot now. I feel confident giving financial advice in my workplace, including to medical residents.”

“I owe my financial success to WCI. I cannot thank you all enough. You are doing amazing and valuable work!”

“It helped brainwash me into financial responsibility and stability.”

“It has dramatically improved my financial well being and my career longevity. I used to feel trapped and woke up every morning thinking how can I get out of this mess? After getting myself into a more optimized position, I have been able to work more on my own terms, say ‘no' to things that I do not want, and contribute in a capacity that aligns with my goals. This has dramatically prolonged my career and improved my outlook on being a doctor.”

“Set me on the path to where I am currently financially independent within 10 years from a nasty divorce with a negative 850,000 net worth (now low eight-figure net worth).”

“Followed since early residency. Followed the advice. Early paying off loans, lived like a fellow even in early attending. But I had a million net worth at 40. I can work as much or as little as I want. My kids can do whatever activities they want and my wife can stay home.”

“Gamer changer. I went from around $200,000 net worth to > $1.8 million in 3-4 years after starting WCI, as a general pediatrician.”

“Completely changed my entire financial future since residency. I attribute more to WCI than any other resource in terms of my financial life and many non financial topics. I am grateful to have found him so early in my financial life. I am a better husband, father, physician because of what I've learned. Jim Dahle literally ‘walks on water' in my eyes and I'm an official convert from ‘Boglehead' to “Dahlehead' if there's such a thing.”

“I believe WCI has added seven figures to my net worth in 10 years.”

“I owe a lot to Jim and WCI. I am a multi-millionaire because of him and his teachings.”

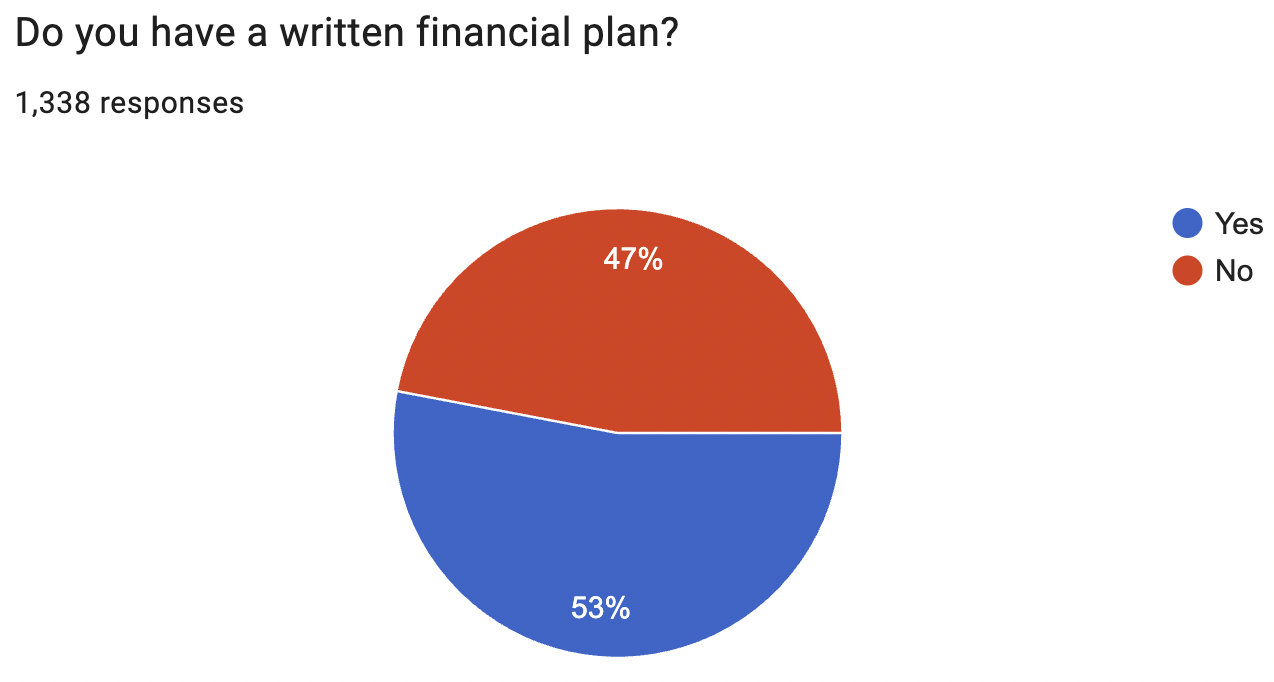

“My financial life is 1,000x better because of WCI. I went from zero financial knowledge in med school to being confident and knowledgeable about my finances. I also have peace of mind knowing that I have a written financial plan. I am eternally grateful to Dr. Dahle and his team!”

“It changed everything. I grew up with no financial literacy. My only lesson was don’t do what my parents did which is live above your means and take on debt for things you don’t need. I’ve always been frugal but more so savings not investing. Thanks to WCI, we have a financial plan and an estate plan designed for our family’s ideal future. Without WCI, I would’ve had no idea about financial independence or know that it is possible.”

“It has brought some peace. I don’t know anyone who has taken out as many loans as I will be, and the anxiety keeps me up some nights. Hearing that other people paid it off while still being comfortable is reassuring.”

“WCI has impacted my life tremendously and I will forever be grateful. Dr. Dahle and his excellent team are so relatable, knowledgable, and are a fantastic resource in all things finance. More importantly, you don't feel alone when you navigate the scary waters of finance because you realize that there are a lot of other people out there just like you or better yet, have gone through what you are experiencing and you can learn from them. I love the fact that the WCI community are supportive of each other. Thank you Dr. Dahle and the WCI team. I appreciate everything that you have done for me and my family!!”

“I’m on track to be financially independent in my early 50s thanks to WCI. Knowing my financial life is essentially on autopilot using WCI principles means I can maximize time with my spouse and young children and relish these experiences without stress.”

“It has made a huge impact on my life. I am in academic medicine and make a lot less than my colleagues. I would have never started investing and been in the financial situation I am in now if it was not for WCI. I took the Fire Your Financial Advisor course in 2020 and it was life changing. I am also grateful that I just by chance chose a fee based planner in 2016 that helped us make smart decisions and introduced us to WCI.”

“Hopefully, there is a succession plan. Dr. Dahle may not want to be as involved as he is forever but his mission has to go on.”

Thank you so much to all of you for your kind words and your constructive feedback. We will use it to continue to improve what was started sitting in a recliner 16 years ago with a 7-year-old (now married), a 4-year-old (now in college), and a 2-year-old (one year from high school graduation) sitting on my lap. It's been a wild ride these last 15 years. Thanks for riding along.

What do you think? What are your favorite and least favorite things about WCI?