A perennial question that exists in the financial literature and blogs is at what age is best to begin Social Security benefits. There are diametrically differing opinions on this topic. Two financial bloggers whom I respect, Dr. Jim Dahle and Dave Ramsey, have opposing perspectives on this issue; Jim states that one should wait until age 70, and Dave says that you should begin benefits at age 62. Based on the mathematics of the problem, who is correct?

In my opinion, there are only three absolutes regarding when to begin Social Security benefits:

- If you are under Full Retirement Age (“FRA”) (67 years for those born 1960 or later) and still working above the earnings limit ($24,480 in 2026), do not begin Social Security benefits—they will be clawed back.

- If you are afflicted with a terminal or chronic illness that will decrease your life expectancy, take Social Security benefits as soon as possible.

- If your Social Security benefit and your savings will not meet your expenses in retirement, you need to continue working and delay your Social Security benefit if you are under age 70.

Beyond these basic tenets, whether it is mathematically beneficial to take Social Security benefits earlier or later depends on the assumptions that you make regarding inflation, taxes, and stock market returns.

What About the Math?

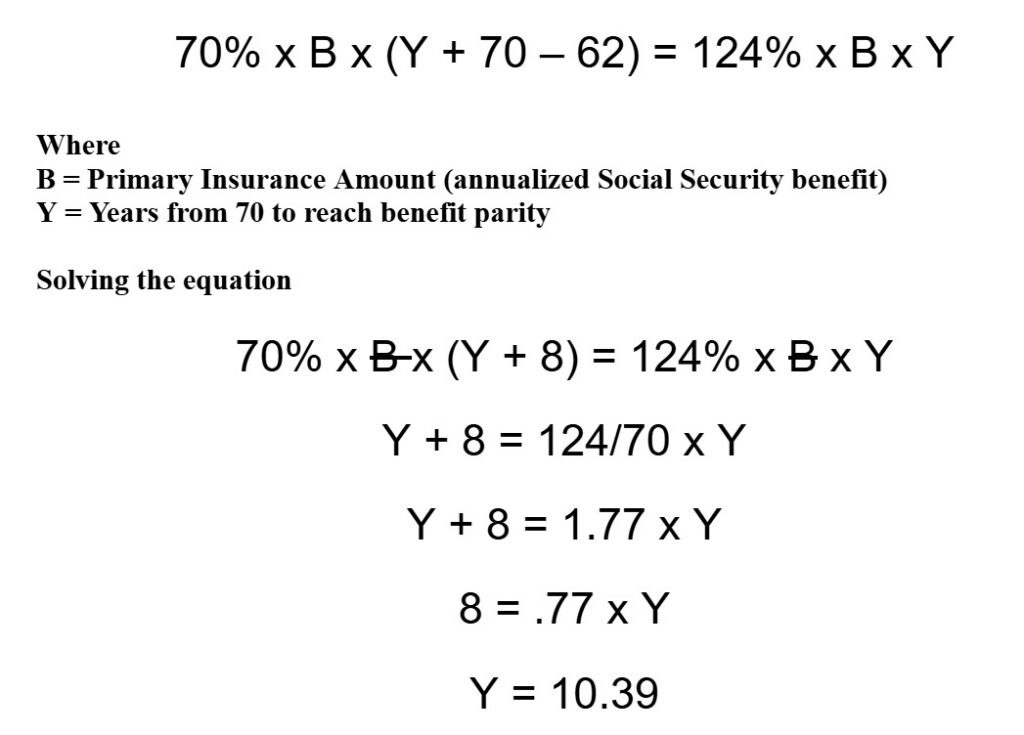

In its simplest form, the benefit equivalency between beginning Social Security benefits at 62 or 70 is represented by the following equation:

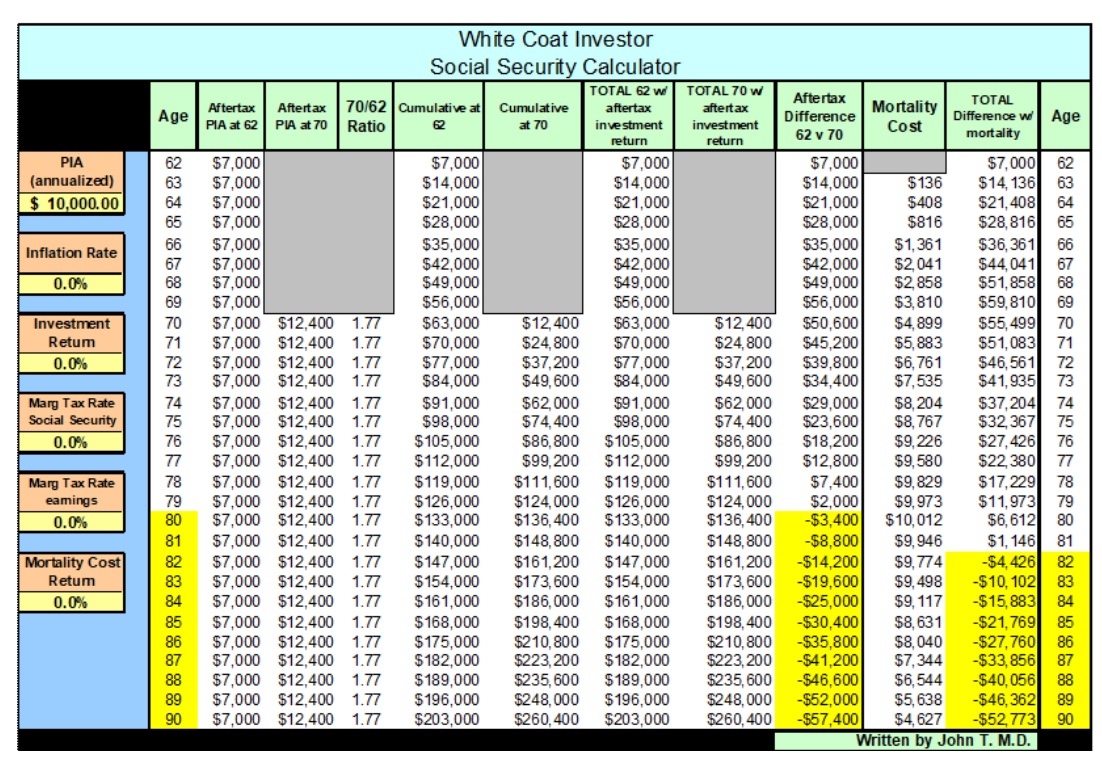

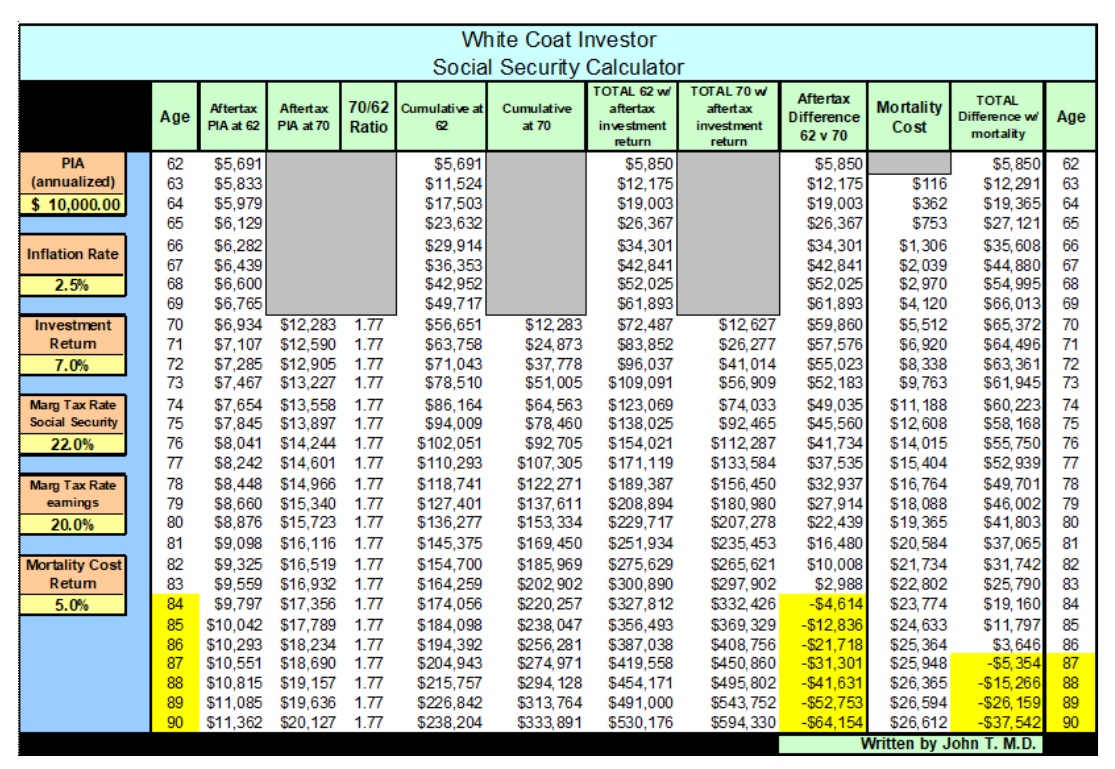

Parity between beginning Social Security benefits at 62 or 70 is reached at age 80.39 years. This is reflected in the table below. (Note that the amount of PIA benefit (the primary insurance amount) is listed at $10,000 for simplicity—the gross amount does not affect the parity calculation.)

However, this is not a fair representation of true parity. This calculation does not take into account the effects of inflation, investment return on saved benefits, taxes on Social Security benefits and investment returns, and the cost of death risk in the 62-70 age period.

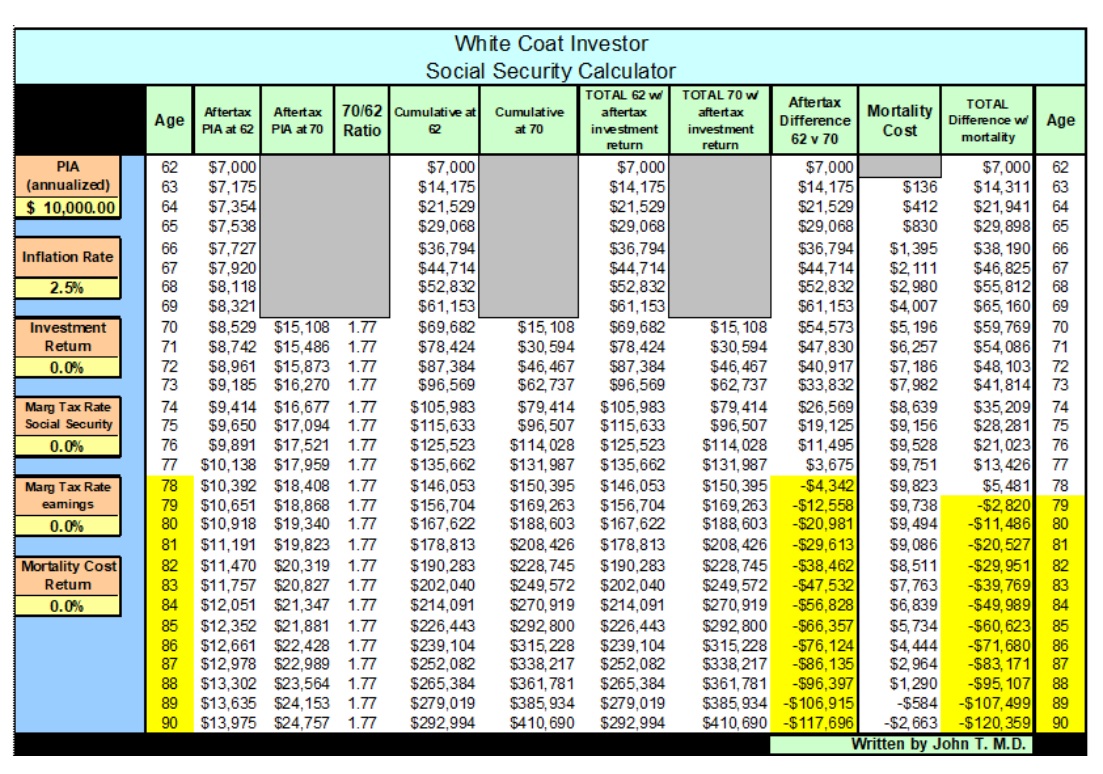

What If We Add Inflation of 2.5%?

Here's what we'd see.

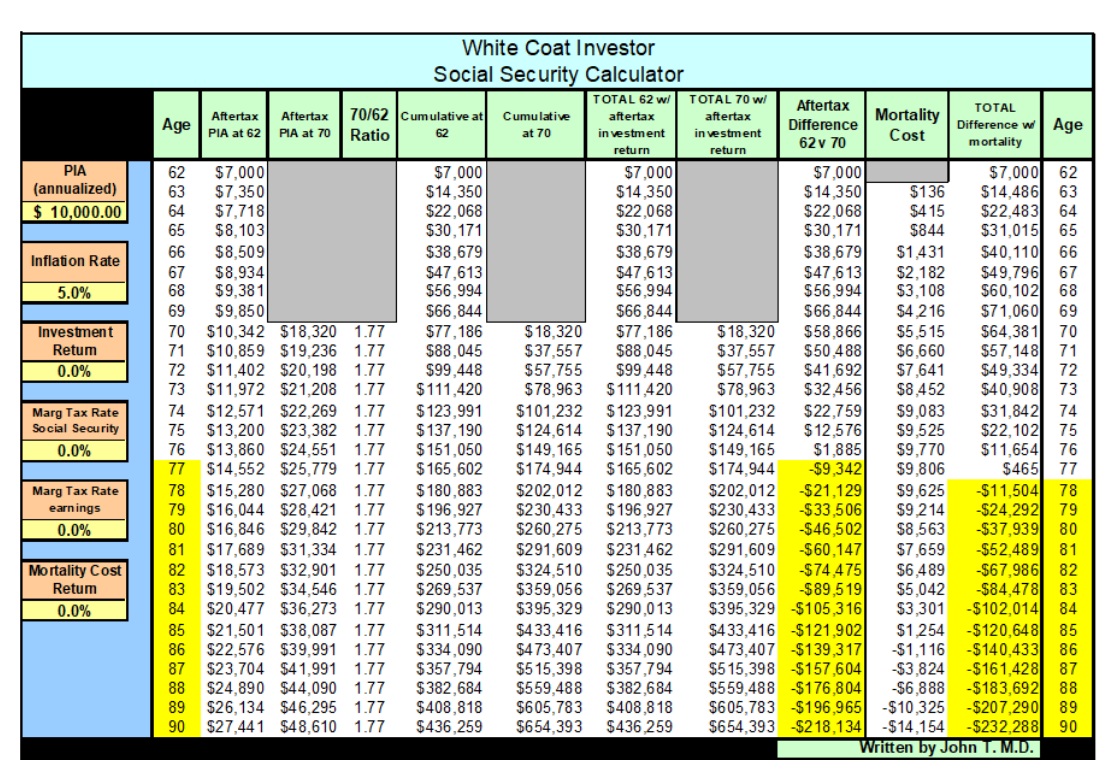

A 2.5% rate of inflation decreases the time to parity by two years to age 78. Note that the ratio of benefits between 70 and 62 never changes. But the absolute difference between the two increases accounts for why higher inflation favors delaying Social Security benefits since they are indexed to the inflation rate. Therefore, a general principle regarding Social Security benefits is that higher inflation favors delaying taking benefits. If you assume a 5% inflation rate, the parity age decreases to 77, as reflected in the table below.

What If We Add an Investment Account for the Benefits?

What does a person who takes Social Security early do with the benefits from 62 to 70? They either spend the money or save the money; however, presumably, the beneficiary is spending less of the saved and invested retirement money if they are receiving and spending the Social Security benefit instead.

For instance, if retirement expenses are $120,000 per year and you can receive a $30,000 annual Social Security benefit at 62, the beneficiary can either withdraw $120,000 from savings each year or take Social Security of $30,000 each year and withdraw $90,000 per year from savings. The result is that you will leave $30,000 more in your investment accounts per year if you take the Social Security benefit.

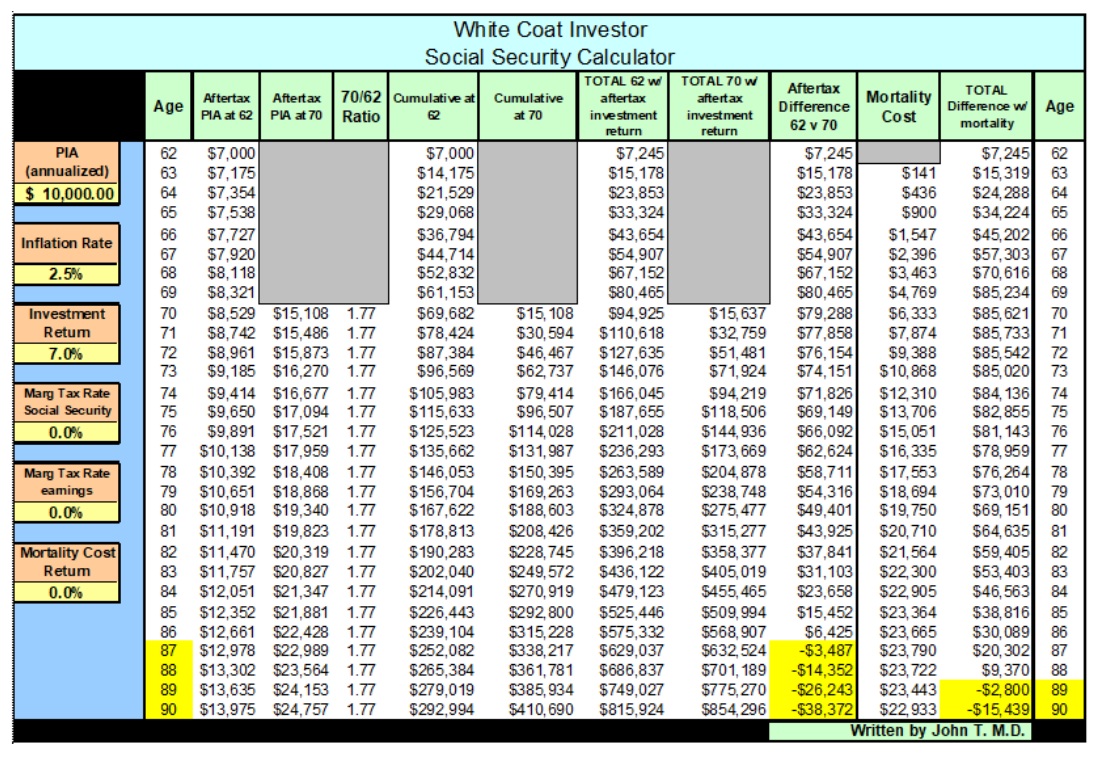

Therefore, when considering parity, we should assume the benefits from 62 to 70 are being invested. What happens to parity with a 2.5% inflation rate and when we add a modest investment return of 7% to benefits?

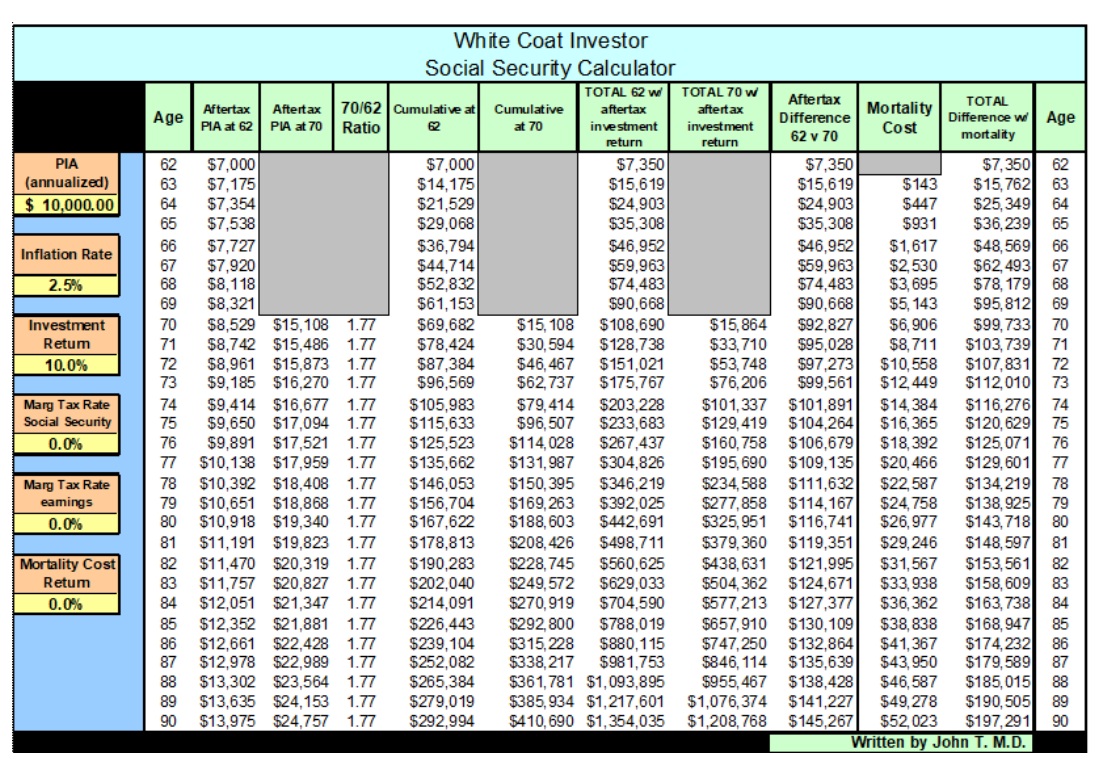

Parity is not achieved until age 87. This is beyond the life expectancy of most people. If we assume a 10% return (see the table below), which is what Dave Ramsey assumes in his advice, parity is never reached. This is why he advises beginning benefits at 62. So, another principle is that if you assume a higher rate of market return on your savings, it is more beneficial to take Social Security early.

What If We Add Taxation?

But this projection is not fair either. Social Security benefits and money saved in a side account may be subject to taxation. Social Security is always considered ordinary income, and for most WCIers, 85% of the benefit would be taxed. The side account taxation is even more complicated, as it may be ordinary income, capital gain income, or a combination of the two. It may be tax-free income in a Roth or tax-deferred income in a regular IRA that you didn’t have to spend because you were getting Social Security benefits. It may be money invested in an index fund that has minimal capital gain distributions and dividend distributions that may be taxed at a 0% rate.

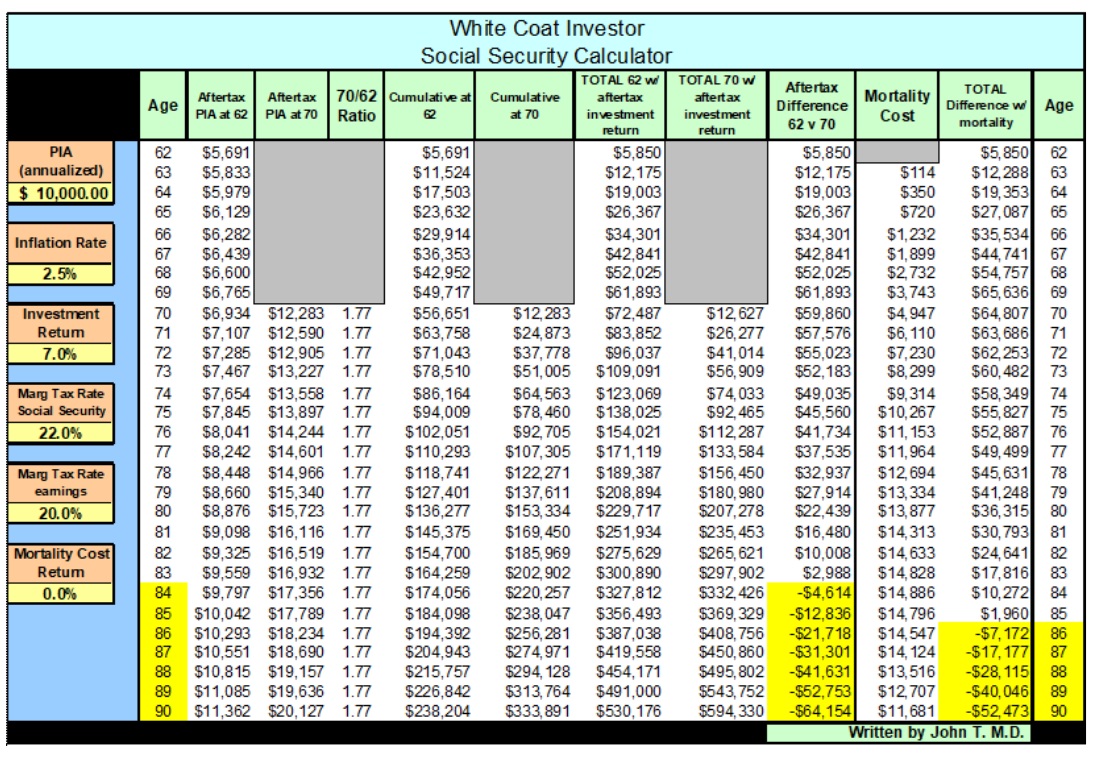

Let’s assume a marginal tax rate of 22% and an average earnings tax rate of 20%.

The higher the tax rate on earnings, the shorter the time that is required to achieve parity. In this case, parity is achieved at age 84 instead of 87. Not surprisingly, a higher rate of taxation on your savings favors taking Social Security later rather than earlier.

More information here:- Social Security Is Not Going Away (But You Might Have to Adjust Your Plans)

- A Change of Plans About When I Took Social Security (and the Bureaucratic Frustrations That Followed)

Mortality Risk?

To achieve true parity, however, we must also consider the mortality risk—the risk that the person who delays Social Security benefits to 70 will die before achieving parity. For instance, if the beneficiary in the above chart died at 63, they would have lost $5,850 in after-tax benefits. That difference is the mortality risk, and it increases every year until at least age 70. This principle is true even when considering survivor benefits, which we will discuss later.

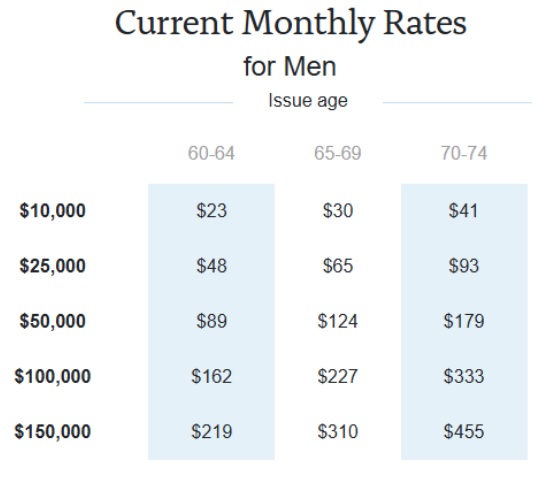

The math, admittedly, gets fuzzy at this point as I am not an actuary. So, I went online and got quotes for 15-year term life insurance from New York Life. The quote was a 10-year term life for a 62-year-old non-smoking, otherwise healthy male. (Getting this quote was quite a sacrifice, as I am now being inundated with emails and phone calls from agents trying to sell me life insurance.)

I took the annual premiums quoted for $100,000, annualized them, and prorated the amount to reflect the after-tax benefit difference in lieu of the full $100,000 benefit. That amount is approximately what it would cost to insure for the loss of the benefit difference prior to age 70 in the event of a premature death.

Looking at that amount in the far right column, parity is not achieved until age 86. If we choose to add a modest investment return of 5% to that amount (money that would not have to be spent to achieve true parity and could be otherwise invested), then parity would come even later at age 87.

Spousal Benefits

In most cases, a lower-earning spouse is entitled to Social Security spousal benefits. It is important to remember that a lower-earning spouse can claim the higher of either his/her personal benefit or 50% of the benefit of the higher-earning spouse at his/her full retirement age. But they can't claim both. The spousal benefit can be requested only if the higher-earning spouse has applied for Social Security benefits. As with a higher-earning spouse’s Social Security benefits, the amount of benefit for a lower-earning spouse depends on the age of the lower-earning spouse at the time benefits begin.

It is important to remember that the amount of spousal benefit is not affected by the age at which the higher-earning spouse elects to start benefits. In addition, the lower-earning spouse does not receive any additional amount for delaying benefits beyond their FRA. Finally, it is important to remember that the lower-earning spouse can receive the higher of 50% of the higher-earning spouse’s FRA amount or their own Social Security benefit, but they cannot receive both.

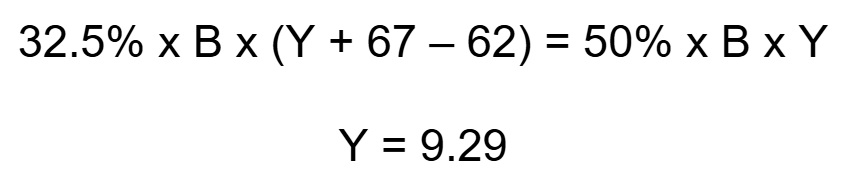

The calculation for parity in this scenario would be represented by the following formula:

In this case, parity between beginning spousal benefits at 62 vs. 67 would be achieved at approximately age 76. This is earlier than parity for the higher-earning spouse, which favors delaying benefits until age 67. As with the other projection, higher inflation favors delaying benefits, and higher market investment returns favor taking benefits early.

If the lower-earning spouse has accrued a Social Security benefit that is greater than 50% of the FRA benefit of the higher-earning spouse, then each spouse would receive their own benefit, and the spousal benefits would not play a role in their decision-making.

Dependent Benefits

Another consideration when deciding on when to take Social Security benefits is whether you have children who are younger than 20 years old. Minor children may be eligible for dependent care Social Security benefits if either spouse has filed for their Social Security benefits. The amount is typically 50% of the filing spouse’s Social Security benefit at FRA (subject to a family maximum depending on the number of children). This can be a significant benefit, and it should be considered when you make your decision.

More information here:Survivor Benefits

If the higher-earning spouse passes away, the lower-earning spouse would be entitled to claim a survivor’s benefit. As with spousal benefits, the amount of benefit depends on the age at which the lower-earning spouse begins their benefits. In addition, the lower-earning spouse can take either the survivor benefit or their own benefit, but not both. Unlike a spousal benefit, however, the amount of a survivor’s benefit is based on the total benefit of the higher-earning spouse. Therefore, if the higher-earning spouse delays benefits until age 70, the survivor’s benefit will be based on that increased amount.

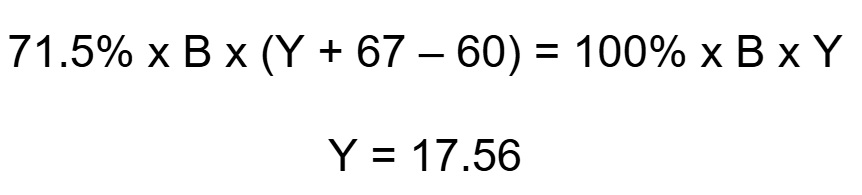

A surviving spouse may begin a benefit at age 60 at 71.5%. If they wait until FRA, the benefit is 100% of the deceased spouse’s benefit. Parity, without considering the effects of market return or inflation, would be achieved at approximately age 84.

Obviously, the death of a spouse is a traumatic experience, and your decisions will likely not be dictated solely by the projected Social Security benefits.

The practical effect of the survivor’s benefit is to extend the higher-earning spouse’s benefits until both married partners pass away. This prolongs the amount of time that they have to achieve parity in Social Security benefits if they delay beginning Social Security until age 70.

One strategy in this regard is for the lower-earning spouse to begin benefits at 62 and the higher-earning spouse to begin benefits at 70. However, the same parity calculations would apply to the higher-earning spouse—the only difference would be the extended time since both partners would have to pass away before the benefit would terminate (unless the lower-earning spouse is below FRA when survivor’s benefits begin).

For the purposes of the spousal and survivor’s benefits, I have assumed that a couple’s earnings histories are disparate (higher-earning spouse and lower-earning spouse) and that the individuals were born after 1960. When the earnings histories are similar, the value of the spousal and survivor’s benefits decreases substantially.

Who Was Right?

In the end, was Dave Ramsey or Jim Dahle right regarding when to begin Social Security? In short, they are both right, depending on what assumptions you choose to make.

It is difficult to predict the future, and there are dozens of permutations possible with this model. There are also many nuances with respect to Social Security benefits (disability, disabled child, divorce, etc.) which I have not addressed in the name of brevity. I hope that I have given you some insight into the basic principles of Social Security so that you can develop an innate understanding when you meet with your financial advisor. I have attached the spreadsheet for you to determine what assumptions you want to make. You can enter your assumptions for inflation, market return, etc., and the spreadsheet will automatically highlight where parity occurs.

For me, the choice that I made was to take Social Security benefits at the time that I retired at age 64. My wife, born in 1957, was 66 1/2 years old and received 50% of my benefit. (She had started her personal benefit at 62, and when I retired, she switched to her spousal benefit at 66 1/2.) I do not regret making this decision.

Every WCIer may have different needs and may make different assumptions regarding inflation, taxes, investment returns, and mortality risk. I hope that you find this model useful for your planning.

Please note that this spreadsheet is for illustration of a single individual and does not take into account possible options for married couples. Please consult your financial advisor before making any decisions regarding when to begin your Social Security benefits. The spreadsheet is locked, but you can view the formulas used in the calculations. I tried to be conscientious when I wrote it, but please feel free to let me know if you find any errors.

[FOUNDER'S NOTE BY DR. JIM DAHLE: There are few absolutes when it comes to claiming Social Security, but it's key to understand what they are. The first is that the wealthier you are, the less this matters. If you're retiring with $8 million, it just doesn't matter if you take your Social Security at 62 or 70. This is an optimizer/satisficer thing. Poor people are the folks who would really benefit from delaying Social Security. Unfortunately, they are the ones least likely to be able and willing to do so. Just having the ability to delay Social Security to 70 (i.e., having something else to live on or perhaps still being able to work) is a sign of privilege.

The second absolute is that delaying Social Security is the best annuity available on the market and probably the best fixed-income investment possible. So, if you're buying a SPIA and NOT delaying Social Security, you're making a mistake. And the more bonds, CDs, and cash you have in your portfolio, the better off you are spending it in order to delay your Social Security payments.

The third absolute is that the longer you live, the better off you are delaying Social Security. That's how the math works, but most importantly, that's how the insurance aspect works. If you die in a couple of years, well, that's a bummer, but you didn't get close to running out of money. If you live to be 108, I guarantee you'll be glad you delayed your Social Security. Delaying Social Security is like buying longevity insurance. It pays out if you live a long time, and if you don't, you didn't need it anyway. Think of delaying Social Security like buying a Single Premium Immediate Annuity, where the longer you live, the more you're paid. Interestingly, annuity buyers live longer than those who don't buy them, and I bet Social Security delayers live longer, too. Correlation is not causation, but it's something to think about. That insurance aspect of Social Security has value, more value than the absolute dollars and cents that a calculation would spit out. You might come out ahead investing, but the guarantee has value. It's a bit like whole life insurance that way. Yes, your rate of return is lousy . . . unless you die at 40, and a few life insurance purchasers will. Racecar driver Kyle Busch successfully sued insurance companies for selling him some lousy permanent life insurance policies, but then he died at 41. Maybe his heirs would have come out ahead if he had spent more of his money on life insurance, not less. (Naturally, they would have come out much further ahead if he had spent the same amount of money on big fat, term life policies instead of IULs, which was the reason for the lawsuits).

So yes, the rule of thumb is that, assuming good health, single people and the higher earner in a couple should delay Social Security until 70. But rules of thumb have exceptions, and only you can decide if you are one. Frankly, I hope most WCIers build so much wealth that this question ends up on their “doesn't matter” list.

If you want to get beyond rules of thumb, I would suggest you spend some time with Mike Piper on this subject. He wrote Social Security Made Simple and designed the free Open Social Security software. If you run your numbers through there and it tells you to claim at 67 (or whatever) instead of 70, then I think it's fine to do so. But when I run our numbers through there, I get the expected recommendation that Katie should file at 62 and I should wait until 70. I bet you will, too. Doing that will take you a whole lot less time than trying to DIY the calculations, and I'm confident Mike has spent a whole lot more time on this subject than any of the rest of us.]

What do you think? At what age do you plan to begin Social Security benefits? Is waiting as long as possible the best strategy?