In February I got to go to my third White Coat Investor conference. It is a seriously great conference, and I don’t generally like conferences. I met a lot of cool people that I’m still in touch with, caught up with some friends from past years, ate good food, and picked up good swag. I also got to sit in the “columnists panel” and take questions from the audience. The only downside of the panel was not having enough time to answer everything and having to listen to Dr. Jim Dahle and Josh Katzowitz bicker about Teslas like an old married couple. Some of the things I would have liked to say: 1) Tyler Scott’s “rich life” is travel but mine is working less; 2) No, divorce is not the end of your happiness or your path to financial freedom; and 3) You want to know how we all organize our finances? I'm happy to share.

You might think that someone who had been to three WCICONs (with another coming up in February 2025) would have her finances running like a well-oiled machine. You would be wrong. In my house, we follow the 80/20 rule which says: you spend 20% of your energy doing 80% of any project, and then the last 80% of your energy goes to the last 20% that gets you to perfect. Most of the time you are better off just doing the first 80% of the project and then calling it good. This rule applies nicely to a lot of activities of daily living: laundry and cleaning the garage, for instance (you do 80% of the laundry by not matching socks).

It applies to keeping track of our money, too. If you accept “good enough” as the standard most of the time, you free up a lot of time and energy for activities that demand absolute attention (like surgery) or that are more fun (like skiing). So, turn that perfectionism down a few notches and read about how we keep our finances organized-ish:

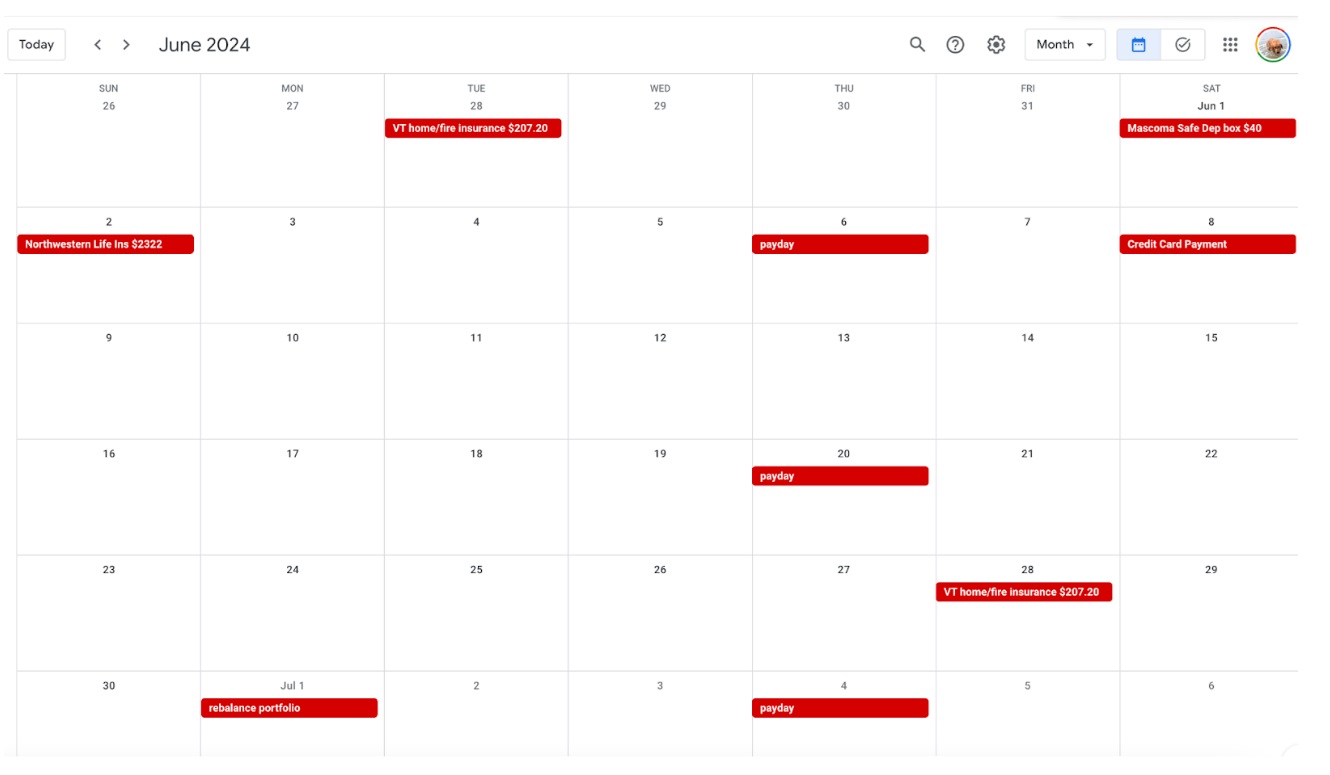

Financial Calendar

All our recurring bills are on auto-pay, but I still like to know when they are going to come out. Plus, there are the bills that can’t be placed on auto-pay (property taxes), routine chores (rebalancing), and the question of whether we get paid this week or next? So, our finances have their own Google calendar (click to enlarge).

Online Aggregator

I’ve used Personal Capital, now called Empower, for a long time. Multiple banks and insurance companies offer similar programs. You link your accounts to the platform and then you can see your overall holdings, performance, etc. It also offers financial planning which I’ve never done.

I use it for the asset allocation feature: it shows a breakdown by cash/stocks/bonds/alternatives, which you can then break down further by large cap stocks, small cap, etc. This is a nice feature, and it saves having to comb through our different accounts to add up all the different holdings. I think of it as a blunt tool because it’s got some shortcomings:

- Sometimes the platform has difficulty linking to one or more accounts, so if you really want to see the up-to-date totals, you have to go and fix the link. I only do that if it’s a major account involved. If it’s just our checking account, I don’t care because I check that manually (and I don’t count that as part of our investments anyway).

- Asset allocations aren’t always accurate. Most of our small cap stock holdings (FSSNX, Fidelity Small Cap Index Fund) are listed in our stock holdings, but some are listed under “Real Estate” and “Cash.” I don’t know how to fix this so if it’s a significant amount (like, tens of thousands of dollars), I add it to my spreadsheet manually. I once tried to create a really clever Excel formula that would capture every holding correctly, but I ended up just getting really annoyed. Now I consider those smaller amounts the last 20% of the accounting that would cost me 80% of my effort—in other words, it's not worth my energy.

Also Empower sends me emails that say things like, “You spent $86,746 less this month than last!” These do not inspire my confidence.

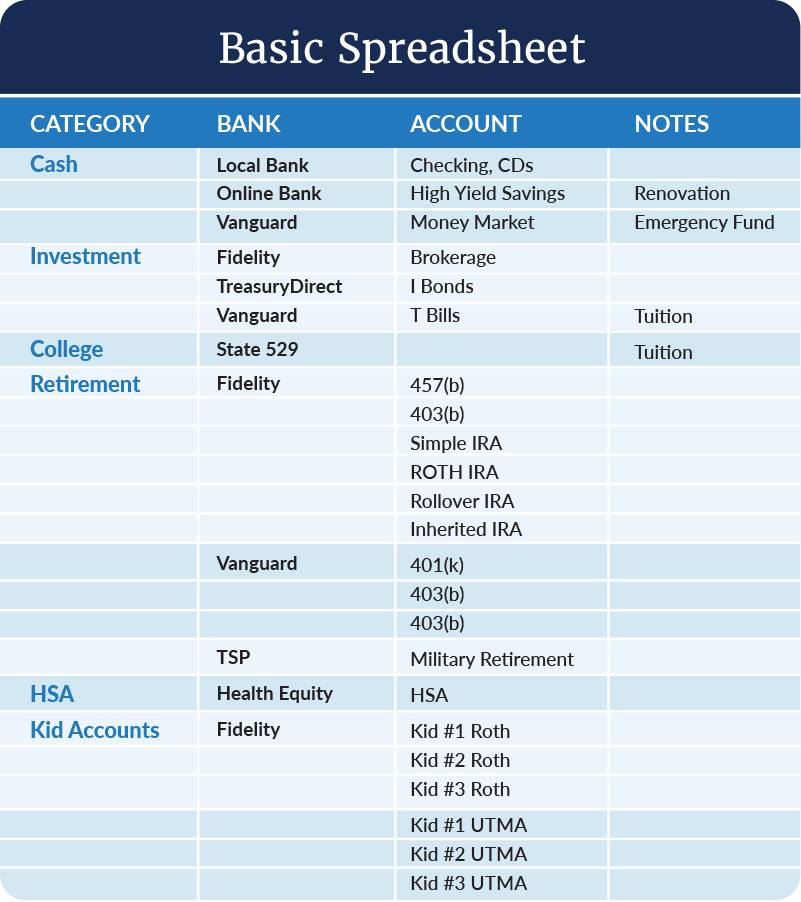

Because of these shortcomings and because the online platform doesn’t let me move categories around, I also use good old-fashioned Excel spreadsheets.

The basic spreadsheet looks like this:

No one tell my kids I rank them in numerical order.

I can rearrange the columns to list them by bank, by purpose, or by however else I want. This makes it easy to keep track of where the money is and where it’s going.

In an ideal world, we would have all our accounts at one local bank (for checking) and one investment bank (for everything else). Instead, we have what you see here: a hodgepodge. We have retirement accounts from a few different employers. We’ve rolled over and combined the ones we can, but for some, we aren’t allowed to (non-governmental 457s) or we haven’t gotten around to yet (TSP).

The logical move would be to transfer all our accounts to Fidelity, but my husband and I both work for an employer that uses Vanguard so we’re keeping those for now. We use an online bank for a high yield savings account. The money will be used in the next six months, more or less, so I’m willing to put up with the hassle of yet another account. When we withdraw the money, we’ll close the account. Some people are willing to have multiple accounts at different banks to get the highest possible rates, but that, to me, is also in the last 20% that would eat up 80% of my effort.

Off-topic but I love our local bank. There is a branch office in the general store a mile from our house. I can do my banking, mail a package, and buy cheddar cheese in bulk all in the same trip. Beat that, Bank of America.

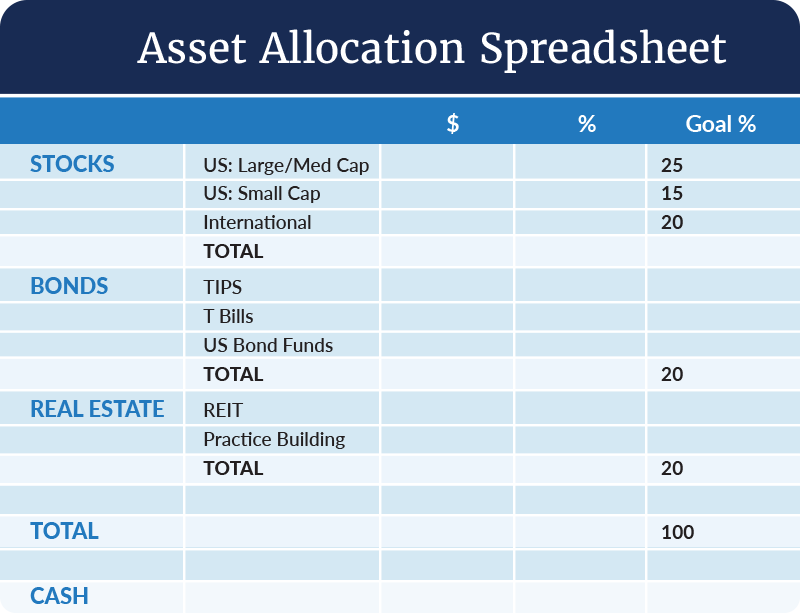

I have another spreadsheet that tracks our actual asset allocation, and it looks like this:

You will notice a few things about this:

- Our asset allocation is 60% stocks/20% bonds/20% real estate. Stocks are broken down further into large/medium cap (25%), small cap (15%), and international (20%). This is a very boring, standard portfolio.

- I’ve broken down the bonds into funds bought through our accounts at Fidelity, TIPS bought through TreasuryDirect, and T Bills through Vanguard. I did this so that I remember to get the totals from each of those accounts, but for our asset allocation, all I need is the total amount in all bonds. There are people who have a very carefully considered portfolio of different bonds. I am not one of them.

- “Practice building” in the real estate category refers to the building we bought for my husband’s practice. I listed the down payment, because we just bought it. In the future, if I was trying to calculate our net worth, I would put down what I think it could sell for minus what we owe. I don’t include our home’s value, because we don’t intend to sell it.

- Cash is a separate category, outside the investment total. Some portfolio models use a percent cash allocation, usually something small like 5%. As your portfolio gets bigger, the percentage in cash should get smaller because you want most of your money invested and working for you. I find it easier to just keep about three months worth of expenses in cash rather than a percentage. I include short-term CDs in the “cash” category, but if you are doing longer-term or a CD ladder, you might include them in overall asset allocation.

Setting up this spreadsheet is really easy. Stock Total = (large/medium cap + small cap + international). Portfolio total = (Stock Total + Bond Total +RE Total). Stock % = (Stock Total/Portfolio Total).

We don’t use a budget app, although we used Mint in the past. I’ve heard good things about You Need a Budget. At this point, our ins and outs are pretty stable. We only have one credit card, so if I need to look at our spending, I just pull up the card statements. If we were trying to change our spending patterns, I would definitely use an app, although it requires some diligence in entering transactions as they happen.

More information here:

What to Do with a $900,000 Lump Sum of Money

Password Manager

We just started using this because we got tired of trying to keep straight all the passwords for those many accounts. Then, just when we thought we had them straight, we would have to re-set one, and that would totally upset the apple cart. We use 1Password because it was highly ranked by several online reviews, but there are others. We did the free two-week trial and then signed on for a one-year plan.

Password managers all promise top-notch security. I figure they are safer than most banks (plus everyone knows the Deep State already has all our secrets and the only thing they aren’t tracking at this point is my cheddar cheese consumption). If anything, our digital lives are safer now because we use the password generator feature to make actual secure passwords instead of relying on the same five or six over and over.

File Cabinet

We still have one. We keep paper copies of vehicle titles, birth certificates, and property tax bills. We keep a “taxes” file for each year and put receipts and stuff in there throughout the year. We need to thin out the files, but we haven’t gotten around to it. I’m sure there are people out there who immediately download every form and receipt. One of them should write a column.

More information here:

You Should Invest Like a 50-Year-Old Woman

Living Our Lives in a Dual-Physician Income Household

Areas for Improvement

Besides consolidating bank accounts and weeding out the file cabinet, my husband and I need to start having regular sit-downs to review the numbers. Our problem isn’t that we don’t talk about money enough—it’s that we talk about it too much, in passing, when the need arises or when the mood strikes. We would do better to take Sarah Catherine Gutierrez’s advice from the conference: have scheduled financial meetings with your partner and then don’t talk about money the rest of the time. This is good relationship advice, right up there with “don’t ask questions you don’t want to hear the answer to.”

There you have it: our good-enough-for-us organization system. I hope it helps. I hope the 80/20 rule works as well for you as it does for us. Tell us your system in the comments, or come to next year’s conference and tell us in person. Then, we can all go do something more fun.

What's your organizational system like? Do you feel the need to tweak it, or is it working well for you? Do you also have a general store where you can mail a package and eat some cheese?