I am often asked about whether or not it is smart to invest in Variable Annuities (VA) and invest after-tax money inside retirement accounts like a non-deductible IRA contribution. The alternative, of course, is to invest in a regular old taxable, non-qualified, brokerage or mutual fund account. It turns out that the answer is “it depends.” Before we get into running the numbers, however, there are a few comments that should be made.

First, with regards to after-tax money in retirement accounts, if you're going to convert that money to Roth (tax-free) money any time soon such as with an annual Backdoor Roth IRA or a Mega Backdoor Roth IRA, that's a good idea.

Second, all of these options are inferior to both tax-free retirement accounts or a tax-deferred retirement account. You don't need to run any numbers to know that. In fact, perhaps the best way to think about a tax-deferred retirement account is to consider it to be two different accounts.

- The first is your account; it is exactly like a Roth (tax-free) account. It grows tax-free and comes out tax-free. Basically, it is sheltered from taxation.

- The second is a “government” or “tax” account. This is simply money that you are investing on behalf of the government and will turn over at the same time you withdraw money from your tax-free account. In most cases, you even get to take a little bit of the government account and move it to your account, making it an even better idea. But the general idea is that this money grows tax-protected and gains are tax-free.

Once you wrap your head around that concept, it's a lot easier to understand what is going on. But don't bother with a taxable account or a Variable Annuity if you haven't maxed out ALL retirement accounts you are eligible for — including individual 401(k)s for side gigs, cash balance plans, HSAs, a personal and spousal Backdoor Roth IRA, etc.

Third, Variable Annuities are an insurance product and it is generally a bad idea to combine investing and insurance. By doing so, you tend to get crummy, expensive insurance and crummy, expensive investments. Insurance companies love to add on bells and whistles so you can't compare apples to apples and you end up with features you don't want or paying too much for features that you do. So in today's post, we're simply going to compare a bare-bones Variable Annuity without any special bells or whistles to a simple taxable account.

Fourth, sometimes it can make sense to use a Variable Annuity for a special situation. For example, some people who are dumping their whole life policies exchange the cash value into a VA to preserve their basis, then let it grow back to the basis in the VA before surrendering the VA tax-free and using the money for other purposes such as investing in a taxable account. That's not what we're talking about today.

Fifth, variable annuities may provide asset protection in your state. You probably don't need that protection, of course. Protection is usually much weaker than that available for retirement accounts and even cash value life insurance.

How Does a Variable Annuity Work?

A variable annuity is simply an insurance policy wrapped around an investment. Like a Roth IRA, you fund it with after-tax money. Like a 401(k), when a VA is surrendered/closed, all gains are fully taxable at your ordinary income tax rate. Unlike retirement accounts, you're basically limited to mutual fund-like sub-accounts and can't invest in real estate or accredited type investments like you could in a self-directed IRA or 401(k). Like a taxable account, your basis (the initial investment) comes out tax-free. Unlike a taxable account, losses are not deductible, there is no tax-loss harvesting, you can't donate it directly to charity to avoid taxes, and your heirs do not get a step-up in basis. If you choose to annuitize the VA, the portion of the annuity payment attributable to basis is tax-free and the rest of the payment is taxable at ordinary income tax rates. In addition, the age 59 1/2 rule applies. Unlike cash value life insurance, you can't borrow against a VA and in a partial withdrawal/surrender situation, the gains come out first instead of the basis.

So basically after-tax money in, tax-protected growth, then gains come out at ordinary income tax rates. In case you're not paying attention, this is MUCH WORSE than the tax treatment of a Roth IRA and a 401(k), somewhat worse than the tax treatment of whole life insurance, and in some ways worse than the tax treatment of a taxable account. The only tax benefit here is that tax-protected growth. The tax treatment is the same as in a non-deductible IRA.

To make matters worse, a VA has additional costs, which can be highly variable, and available investments can be terrible. Companies like Vanguard and TIAA-CREF have generally low costs and some good investments, but even there the higher costs create a drag on returns. For example, take a look at some common Vanguard funds versus the equivalent variable annuity.

As you can see, the VA wrapper decreases returns by 0.27-0.42% per year.

Bear in mind that some retirement accounts and some brokerage/mutual fund companies also have additional costs which should be added in when making comparisons like these. But since a Vanguard taxable mutual fund account and a Vanguard IRA don't, I'll be ignoring those costs today.

Mutual Funds vs. Variable Annuities

So the comparison here is basically weighing the additional expenses and the additional taxes at surrender of a VA against the benefit of avoiding taxation of dividends and capital gains distributions on a growing investment in a taxable account.

Bear in mind I am completely ignoring the tax benefits of tax-loss harvesting, leaving appreciated shares to heirs for a step-up in basis, or the use of appreciated shares for charitable donations, which makes taxable investing substantially more tax-efficient, especially when you combine the tactics as I do. I am also assuming the very highest tax brackets for both ordinary income (37%) and for capital gains (20%), and for PPACA taxes (3.8%), which is higher than most docs are in now and will be in during retirement. I will also ignore state taxes for the sake of simplicity.

Total Stock Market – A 5-Year Period

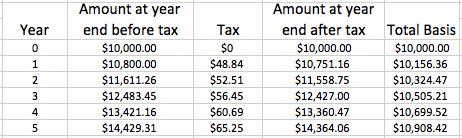

Let's start with a very tax-efficient investment (Total Stock Market) and a very short time period (5 years). Let's assume a return of 8% per year. Current yield on Total Stock Market is 1.90%, almost all of which is taxed at qualified dividend rates and long term capital gains rates. Let's assume I put $10,000 into the mutual fund and $10,000 into the VA. We'll also make the simplifying assumption that the entire distribution is paid at year end, which is obviously not the case but should make little difference.

The TSM Mutual Fund

After five years of growing at 8% and paying taxes along the way, the fund is worth $14,364.

However, now taxes must be paid. Gains are taxed at 23.8%. The initial $10K is not taxed, but neither are the reinvested distributions since they are also part of the basis. The distribution in year one was $205.20, but $48.84 went to the taxman so only $156.36 was invested. Let's add up all the basis.

So you have $14,364.06 with a basis of $10,908.42. So if you sell the entire investment, you will owe 23.8% * ($14,364.06-$10,908.42) = $822.44 in taxes leaving you with $14,364.06 – $822.44 = $13,541.62

The TSM Variable Annuity

The math for the VA is much simpler. It grew at 8% minus the 0.38% tax drag, or 7.62%. After 5 years, you get

= FV(7.62%,5,0,-10000) = $14,436.60.

If you now surrender it, the basis is $10,000, so $4,436.60 is taxable at your ordinary income tax rate plus PPACA tax for a total of 40.8%. Remember this is investment income, not earned income, so you get to pay 3.8% in PPACA tax, not 0.9%.

$14,436.60 – (40.8% * $4,436.60) = $1,810.13

Total after tax = $14,436.60 – $1,810.13 = $12,626.47

That is $13,541.62-$12,626.47 = $915.15 less than you would have in the mutual fund, or about 6.76% less money.

Clearly, with this very tax-efficient asset class and this short 5 year time period, the VA was a dumb idea that cost you money.

Total Stock Market – a 50-Year Period

Now that I've shown my work, let's speed this up a bit. In this section, I'd like to demonstrate the benefit of additional tax protected growth. Instead of holding this investment for 5 years, let's hold it for 50 before liquidating it.

After 50 years, your $10,000 investment in a taxable TSM mutual fund is now worth $373,913, of which $85,752 is basis. So after tax, you have $305,331.

In the VA, your $10,000 investment grew to $393,232, of which $10,000 is basis. So after tax you have $236,874. That's $144,249 or 22.4% less!

What?! That's not even close. How can that be? Well, it turns out with a very tax-efficient investment, you're better off in a taxable account than even a cheap VA, no matter what the time period. And that's ignoring tax-loss harvesting, donations to charity, and the step-up in basis.

Eliminating the VA Costs (Investing in a Non-Deductible IRA)

But what if you eliminate the costs of the VA. Let's say you are investing in a Total Stock Market Fund inside a non-deductible IRA. Is that worth it? I mean, you will probably get some asset protection there and perhaps you can do a Roth conversion of those dollars down the road, but we're just talking from a tax savings standpoint assuming you are never able to do a Roth conversion.

The 5-Year Comparison

We know TSM in taxable after 5 years is worth $13,542.

Inside an IRA, it would grow at 8% each year and then after 5 years, all gains would be taxed at 40.8%. It grows to $12,778. So no, at 5 years, the non-deductible doesn't make sense. But what about at 50 years?

The 50-Year Comparison

After 50 years, TSM in taxable is worth $305,331.

Inside an IRA, it would grow to be $469,016 before tax and $281,738 after tax. So no, even after 50 years, it doesn't make sense unless you can somehow do a Roth conversion or get into a lower tax bracket at withdrawal. How much lower? Well, at 50 years, your tax bracket would have to be at least 6% lower. At 5 years, it would have to be at least 15% lower.

A Less Tax-Efficient Investment

Let's demonstrate it now for a less tax-efficient investment. We could look at bonds, but it gets kind of tricky because if this high tax bracket investor were going to invest in bonds in taxable, they would use a muni bond fund and we wouldn't be comparing apples to apples. So let's take a look at REITs. Remember REITs are required to pay out at least 90% of their earnings each year as distributions and these are taxed at ordinary income rates. We'll assume 100% is paid out for the sake of simplicity. They are now eligible for the Section 199A deduction, however. So 20% of that distribution is tax-free.

REITs – A 5-Year Period

We'll assume that the REIT mutual fund earns 8% per year pre-tax and the REIT VA earns 7.58% per year.

After 5 years, the mutual fund has grown to $12,873, of which it is ALL basis. (Remember all earnings are paid out and taxes are paid each year on this investment.

After 5 years, the VA has grown to $14,410 before tax and $12,611 after tax.

The taxable account is ahead, but only by $12,873-$12,611= $262, or about 2%.

REITs – A 50-Year Period

After 50 years, the mutual fund has only grown to $124,922. Note how much lower that is than TSM at 50 years ($305,331). This is why it is important to invest in tax-efficient mutual funds in a taxable account, even with the new 199A deduction.

By contrast, the VA has grown to $232,587, or $107,665 (86%) more. Clearly, the advantage of tax-protected growth has overcome the costs of the VA with this tax-inefficient asset class.

The Breakeven

So where is the breakeven? It turns out it is about 13 years. At 13 years, the REIT mutual fund is worth $19,281 and the REIT VA is worth $19,385. Note that without the VA wrapper costs (i.e. in a low-cost non-deductible IRA) the break even is in year one.

What about investments with intermediate tax-efficiency? Some mutual funds are less tax-efficient than TSM but more tax-efficient than REITs. Does it make sense to put those into a VA or a nondeductible IRA? You just have to run the numbers but realize you're going to have to leave it in the VA for decades for it to work out. The more tax-efficient, the longer. Due to the lower costs (and potential conversion) of the IRA, you would need less time there.

The Bottom Line

There are a few conclusions that can be reliably drawn from these calculations.

- First, it does not make sense to buy even a low-cost VA in order to shelter a very tax-efficient asset class from taxation.

- Second, it does not make sense to invest in a tax-efficient asset class inside a non-deductible retirement account unless you expect to be able to do a Roth conversion (and the sooner the better) or have a significantly lower marginal tax rate at withdrawal.

- Third, for a very tax-inefficient investment that you are going to hold for multiple decades, it is probably worth using a low-cost variable annuity.

- Fourth, for a very tax-inefficient investment, it is worth using a no-cost non-deductible IRA for any length of time.

What do you think? Do you use a VA? Why or why not? What about a nondeductible IRA?