Our recent post providing a to-do list of what you should do in the first year of your baby's life was so popular on social media that we decided to make a similar list for first-year medical students. Here are the financial tasks that first-year professional students need to be doing. You may not need to do all of them to be successful, but you probably should do most of them.

#1 Read The White Coat Investor's Guide for Students

Your lifelong quest for financial literacy should start today, and this WCI book was written just for you. It discusses all of the financial issues that affect medical students. Why not start there?

#2 Volunteer to Be Your Class's WCI Champion

Is the book too expensive? How would you like a free one? How about a free one for you and each of your classmates? How about a little WCI swag to go with it? All you have to do is volunteer (between about October and March) to pass out the books, and we'll get them shipped off ASAP to a “WCI Champion” in every first-year class.

#3 Get Your Federal Student Loans

Seventy-three percent of medical students pay for school with student loans. The first $50,000 you borrow each year should be federal student loans if at all possible, so they are later eligible for Income Driven Repayment (IDR) programs and Public Service Loan Forgiveness (PSLF). You can apply here.

More information here:#4 Get Your Private Student Loans

Need to borrow more than $50,000 per year? You're not alone. If you apply through the links on the WCI website for private student loans, we'll throw in the student version of our flagship online Fire Your Financial Advisor course for free. Some of the lenders will give you some cash back, too. We work hard to make sure the best deals available from private lenders are those we advertise. If you know of a better deal, please send it our way, and we'll try to get it added to the list.

† Bonus may include cash rebates and value of free course. Student loan borrowers who use the WCI links will be enrolled in The White Coat Investor’s flagship course, Fire Your Financial Advisor: STUDENT for free ($99 value). Borrowers may still receive the amazing cash rebates that WCI has negotiated with lenders. Offer valid for loan applications submitted from May 1, 2026 through October 31, 2026. Free course must be claimed within 90 days of first loan disbursement. To claim free course enrollment, visit https://www.whitecoatinvestor.com/loanbonus.

#5 Take Fire Your Financial Advisor

Don't need student loans, so you don't qualify for the free Fire Your Financial Advisor course? Then buy it. It's only $99, and you can upgrade it to the resident course later. Which can be upgraded to the attending course after that. And if you don't like it, it comes with a one-week, no questions asked, 100% money back guarantee. But you probably won't return it, because it's the best course out there to teach docs how to manage money.

#6 Get a Roommate

As much as we'd like to help you get private student loans, you should take out as little as possible. One of the best ways to do so is to cut your housing expenses in half. Or in thirds. Or quarters.

#7 Send Your Partner to Work

Your spouse might not think it's too cool that you get a roommate. But they could possibly get a job instead, which is even better.

#8 Consider a Job

Some medical students do a little part-time work. Can you handle it while balancing school and the rest of your life? If you can, it can also help reduce how much you borrow.

#9 Apply for the WCI Scholarship

Too much work? Maybe just write a 1,000-word essay for the WCI Scholarship every summer. We give out $50,000+ spread across 10 cash awards each year. Didn't win your first year? You've got three more chances. Keep your eyes open for other scholarships, too. There are a lot fewer than for undergrads, but there are more than zero.

More information here:- 8 Pieces of Financial Advice for Pre-Meds and Medical Students

- Should Medical Students Buy Disability Insurance?

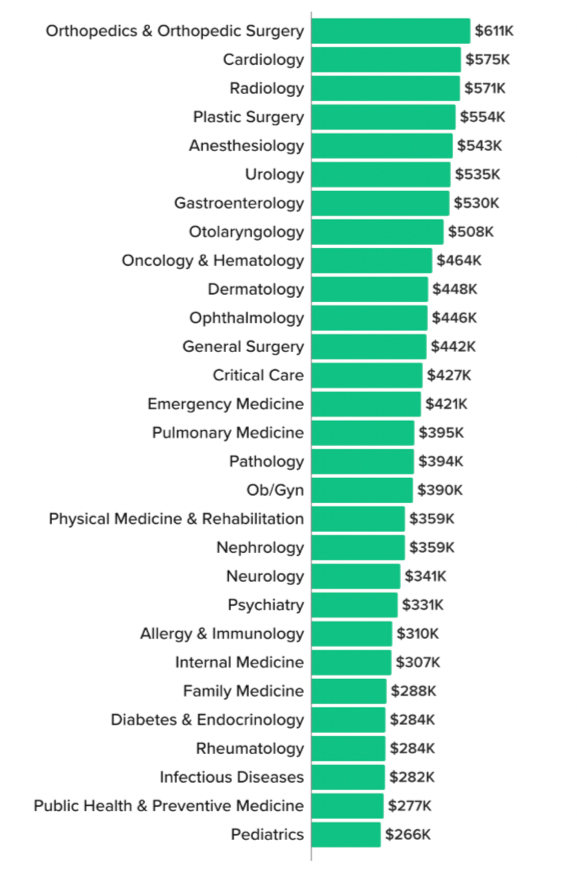

#10 Start Thinking About Specialty Choice

The biggest financial decision you make in medical school is which specialty you will practice the rest of your life. While you don't have to decide as a first year, it is time to start thinking about it. It turns out some doctors get paid way more than others . . .

. . . although the range of pay in every specialty often dwarfs the interspecialty average difference.

While medical students should probably give a little more weight to future lifestyle and income considerations than they typically do at this most idealistic stage of their life, the most important financial consideration for specialty choice is to pick something that you will love to do for a full career. Optimize all career decisions for longevity. You're far better off being a pediatrician for 30 years than spending an extra three years training to be a gastroenterologist and then burning out five years later because you really wanted to be a pediatrician.

#11 Do Roth Conversions

Did you have a prior job/career with a retirement plan? Is any of that money tax-deferred (traditional)? Did you know that you can probably convert it to tax-free (Roth) money during medical school with a very low tax cost and maybe no tax cost at all? Don't miss the opportunity.

#12 Get Health Insurance

Most medical schools require it, but if they don't, buy it anyway. It'll probably be very cheap given your (lack of) income. Take a look at the ACA exchange in your state and see if the school offers a plan. You can consider term life and disability insurance, too, but most docs wait until they start earning as residents before buying that.

#13 Sign Up for Government Benefits

Due to their low income, many medical students, especially married medical students with children, qualify for all kinds of government benefits, including:

- Medicaid

- CHIP

- WIC

- SNAP (food stamps)

If you qualify, you qualify. If you think someone who will have a great future income shouldn't use government benefits, isn't that exactly the point of them: to get people to self-sufficiency without anything bad happening to them? Don't hate the player, hate the game.

#14 Talk to Parents About Money

Twenty-seven percent of medical students graduate debt-free. Most of those have wealthy parents. Most parents can help at least a little, even if you still have to borrow some money. Talk to them about how much they are willing to help. It's probably best if you don't borrow money from them, though. If they can't afford to give it, take a pass. If you can get through school and residency, get a halfway decent full-time job for a few years, and learn to manage money, you can pay off your student loans pretty quickly. And certainly don't let them borrow for your school. If anyone is going to borrow, let it be the student. That way if, heaven forbid, the student dies or is permanently disabled, the loans will go away. If your parents borrow money to pay for your school, at least have them also buy some term life insurance on you in an equal amount.

More information here:- How Much Should You Sacrifice to Pay for Your Child’s Medical School Education?

- Economic Outpatient Care and the Aspiring Millionaire Next Door

#15 Consider Contract Programs

Some of those students who graduate debt-free don't owe any money, but they may owe some time. The military (HPSP), Indian Health Services, National Health Service Corps, National Guard, MD/PhD programs, and others can all offer money for medical school, but it's usually in exchange for a significant commitment of your time. If, however, you want to be a military (or whatever) doctor anyway, you might as well get the money that comes along with that choice.

#16 Tap Your Own Assets

Carefully evaluate your own assets. Do you have any savings or investments? Any 529 money? While I usually don't recommend that people tap their retirement accounts for school, everything else should probably be used before taking out 6%-10% loans. You might have a car, motorcycle, ATV, boat, or something else that you can sell to help pay for school, too. You can even sell your plasma if you want. You could probably get something like $400 a month, and you can even study while donating. This level of frugality probably isn't required just to attend medical school, but the plasma does go to a good cause.

#17 Tax-Gain Harvest

A few medical students might be so wealthy that they can pay for school and have some taxable assets left over. Consider tax-gain harvesting them, updating your basis to reduce your future capital gains taxes. Be aware that many states (including mine) do not have a 0% long term capital gains bracket, like the federal government does.

Being a first-year medical student can be tough, both mentally and financially. Roll your way through this checklist to make sure you don't forget any of the financial tasks needed.

What do you think? What else should be on this list? Was any of this a priority when you were a first-year medical student?