When it comes to personal financial planning, the industry is starting to move towards fixed/flat fee compensation, which is a welcome development for doctors and dentists who are high earners and high net worth (though not necessarily at the same time). When charged for personal financial planning services, asset-based fees are highly unfair towards those with asset levels in excess of $1M and AUM fees can be even more costly for those with retirement plans because many doctors and dentists will accumulate anywhere between $1 and $4 million inside their retirement plans.

Unfortunately, the retirement plan industry has not followed suit and even though the fees are coming down on average, the cost to plan sponsors (and especially for smaller retirement plans) is still significant. Depending on what study one looks at, it is not uncommon to pay total AUM fees of as much as 2%, though the average is probably closer to 1%. However, for plans with $1M or more in assets, this means paying a large fee that increases every year, which is especially true for a group practice plan with multiple partners. Even for a solo practice with over $1M in assets, paying $10k a year for little or no service relative to the cost is not something one wants to do. Many advisors serving the small plans market are rarely acting in an ERISA fiduciary capacity or have experienced managing retirement plans, so paying such high fees is never a good idea, especially for a smaller plan. Larger plans might have smaller AUM fees, but because total assets are often in the tens of millions, the total cost to the plan can be staggering over time. Because most of the money in small practice plans belongs to the owners, they pay the bulk of the fees, and if your plan has AUM fees, you can potentially save a lot of money if you calculate what you are paying in fees, and determine whether you can make changes to the plan to minimize or eliminate completely all AUM fees in favor of fixed/flat fees.

Benchmarking Your Plan’s Fees

There is no easy way to compare and evaluate your plan’s fees which are often a mix of fixed and asset-based fees. How would one go about comparing fees between different service providers to see which one is more cost effective given the services they provide? Your plan might have an advisor, a Third Party Administrator and a record-keeper (usually integrated with a custodian), and your service providers can charge a variety of different fees, including fixed fees, asset-based fees, revenue sharing paid by mutual funds and per participant fees. Some fees can be paid from assets, while other fees are billed directly, so it is often very difficult to estimate the total cost of all of your service providers over time and it is even harder to compare fees charged by different providers side by side.

To make the problem worse, service providers often use ‘funny’ math to discuss their fees. For example, they might say that your 1% AUM fee is actually $X, implying by omission that it is a fixed dollar amount (which it is not, as your AUM fees grow proportional to your asset growth). And when you get a quote from a fixed-fee service provider, the AUM fee service provider might say that your fixed fee is actually Y% AUM which might seem high especially if your plan does not have a lot of assets, and their AUM fee is lower than Y%, thereby implying that a fixed fee is higher than their AUM fee. The problem with this type of comparison is that AUM fees will grow as your assets grow and diminish your portfolio return, while fixed fees are deductible as a business expense, so this type of comparison is disingenuous and wrong, but you often see this type of ‘conversion’ math used even on official plan documents (such as when comparing cost per $1000 for mutual funds in the menu). Instead, we should consider the cost of actual AUM fees rather than ‘converted’ fixed amounts (as this does not provide an accurate picture of the relative magnitude of fees paid over time).

To address the fee comparison issues discussed above, we’ve developed a retirement plan calculator that can be used to analyze the fees of any plan, and compare the fees for different service providers side by side. Below we’ll consider several examples that will explain these differences and why it is important to understand how to properly compare fixed and asset-based fees. Paying fees from your assets diminishes your investment returns, so this has an effect of lowering your portfolio’s growth over time. For high earners, this loss might be as high as $1M or more over several decades, and examples shown below will demonstrate this.

Some plan sponsors choose to pay their service providers outside of the plan using the business cash flow. While this is better than paying directly from your plan assets (because of the business tax deduction one gets when paying service providers directly), this still has significant disadvantages over fixed fees. While you don’t have the AUM fees diminishing your returns anymore, you do have significantly increasing fees nonetheless, so this is still much more costly than paying fixed/flat fees, and this will also be demonstrated by examples below.

Comparing Fixed Fees vs. Asset-Based Fees

Let’s consider several examples that show how to use the cost comparison calculator. While there are drawbacks to using any type of calculators that make static assumptions (such using a fixed rate of return), the main idea here is to compare different scenarios side by side using the same set of assumptions. We are only looking for relative cost difference, rather than absolute numbers, which would not be accurate given how much spread we will get if our assumptions about future returns are wrong. Also please note that the calculator used below is a more advanced version of this cost comparison calculator (with the option of paying AUM fees directly vs. paying AUM fees from assets), so examples 1 through 3 can be replicated using the calculator linked above, while examples 4 and 5 can’t be replicated.

Example 1: Startup Small 401(k) with Profit-Sharing Plan

A question that often arises is whether having an AUM fee is an issue when your plan has no assets. It turns out that the answer is yes, as can be seen from the table below. In the short term, it is true that AUM fees are lower than fixed fees, but over time AUM fees catch up, and after reaching a breakeven point you end up paying significantly more. So everything else being equal, even a plan with no assets can benefit from a flat/fixed fee structure.

Table 1. Startup small 401(k) with profit sharing plan.

Example 2: Existing Small 401(k) with Profit-Sharing Plan

What about an existing plan for a solo owner that already has assets in it? It turns out that the more assets the plan has, the higher the cost of AUM fees, which comes as no surprise, as the table below shows.

Table 2. Existing small 401k with profit sharing plan.

Example 3: Existing Group Practice 401(k) with Profit-Sharing Plan

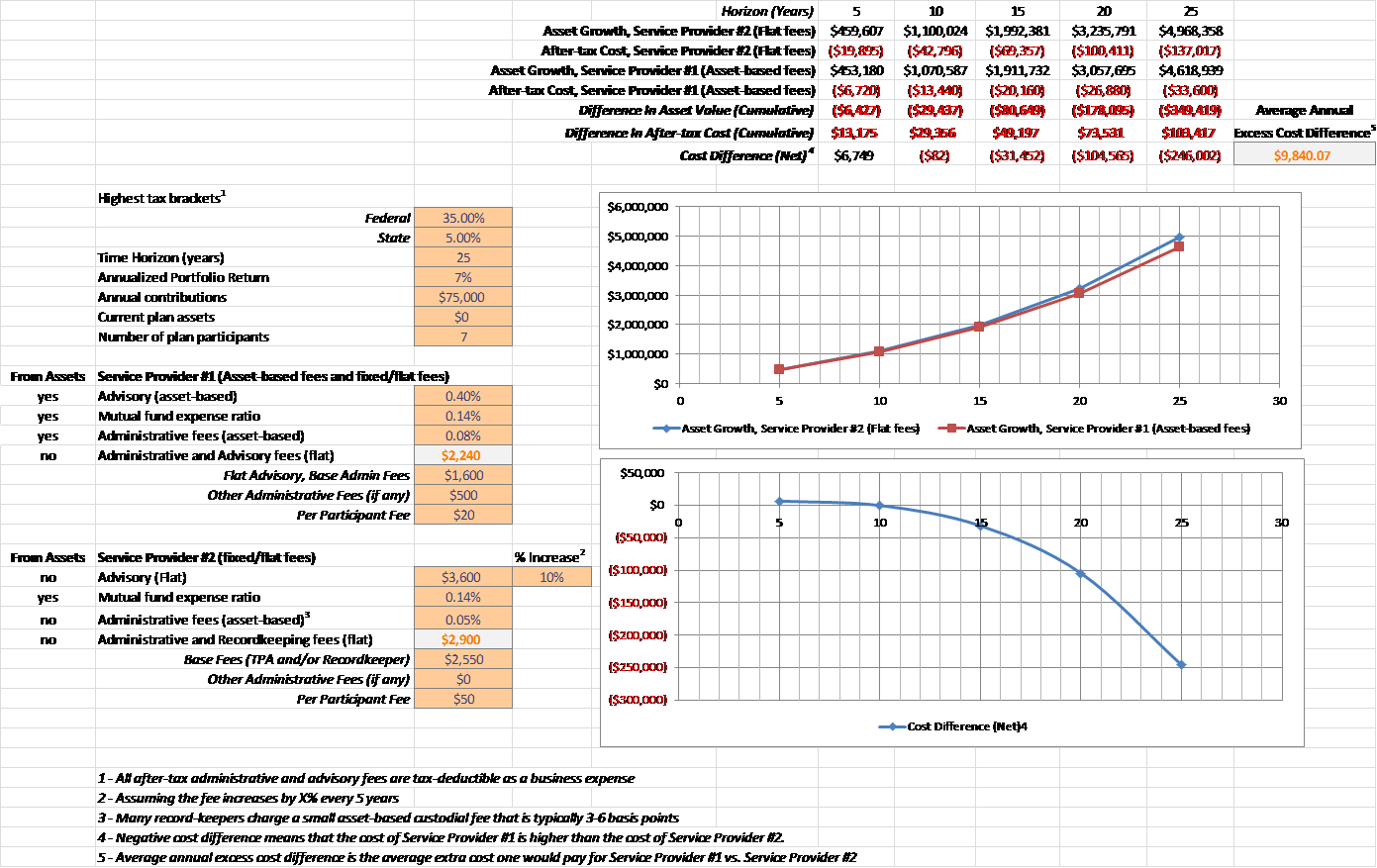

Group practice plans might not have many participants, but they definitely have a lot more assets than a typical plan with the same number of participants. And because most of the money belongs to the partners, the cost of such plans is paid almost exclusively by the partners. Table 3 shows the long term cost of asset-based fees (however modest they might seem on paper).

Table 3. Existing group practice 401(k) with profit sharing plan.

Example 4: Existing Group Practice 401(k) with Profit-Sharing Plan, with All Asset-Based Fees Paid Directly by the Practice

For the example in Table 3 above, let’s consider what happens when you pay AUM fees directly vs. from plan assets.

Table 4. Existing group practice 401(k) with profit sharing plan, with all asset-based fees paid directly by the practice.

If you had a choice to pay AUM fees, it is always better to pay those from the cash flow because the practice will get a business tax deduction for paying fees directly, and you will not decrease your compounded return. However, as the asset level increases, such fees will grow over time so the cost to the practice will increase constantly, which is less than ideal for planning purposes.

So a rule of thumb for larger plans should be to eliminate as many of their asset-based fees as possible, and to pay the rest after-tax (provided that those fees are relatively low so that the amount is not expected to become a burden). Since most of the money in such plans belongs to the partners, this is the best way to minimize your plan’s cost over time.

Example 5: Comparing a Fixed-Fee Record-Keeper vs. a Record-Keeper with an Asset-Based Custodial Fee

Can you actually get a retirement plan with absolutely no AUM fees (except for low mutual fund expense ratios)? Custodians (such as Matrix, MG Trust, and others) that are integrated with many record-keepers charge a small asset-based custody fee. Record-keepers such as Ascensus don't have AUM fees (because they use their own custodians), but their base fee can be significantly higher, so you'll need to do the analysis to determine the cost difference over time.

Table 5: Comparing a fixed fee record-keeper vs. a record-keeper with an asset-based custodial fee. It is assumed that the asset-based custodial fee is not taken out of assets to minimize cost.

The average annual cost difference for this example is around $17k/year over 20 years, so when the practice has relatively few participants and lots of assets, going with a fixed-fee record-keeper might be a better idea. On the other hand, if the practice has more participants and fewer assets, the benefits of going with a fixed-fee record-keeper are not as pronounced.

Apples to Oranges: Low Fees vs. Low Services

Retirement plan service providers often charge the plan a hefty administration and advisory fee, but the services they actually provide are a lot less than what you can get elsewhere for the same or lower fee. There are also service providers who charge a relatively low fee, but offer no value-added services and advice whatsoever aside from the basic services to keep your plan going on an auto-pilot. There are several articles written on the topic of small practice retirement plan services and what types of services are really necessary and are worth paying for. For larger group practices, it is even more critical to get the right level of services given the complexity of such plans.

Typical Services You Might Be Getting in Your Plan

#1 Advisory Services

Plan level advisory services offered by a broker or non-fiduciary advisor, sometimes by an ERISA 3(21) fiduciary in an advisory role (where the plan sponsor retains full responsibility and liability, and has all decision-making authority).

Usually, this service is provided by advisors who are brokers or representatives of large broker-dealers or advisory firms. Such advisors are typically not retirement plan experts and are not very knowledgeable regarding the issues faced by group practice plans. As representatives of larger firms, they would not be interested in making sure that your plan’s cost is minimized (and they have no incentive to do so because they are getting paid via AUM fees), so they won’t be working in your best interest or looking out for your bottom line. For this reason, it is important to work with your own independent fiduciary under ERISA 3(38) rather than an ERISA 3(21). An ERISA 3(38) fiduciary has discretionary authority to manage your plan’s investments and as long as the philosophy of the ERISA 3(38) fiduciary aligns with that of the plan sponsor, ERISA 3(38) fiduciary can be trusted to manage investments for your plan because of their high fiduciary standards (which includes taking no revenue sharing, 12b1 fees or commissions, something ERISA 3(21) advisrs often accept and which results in higher than necessary costs for the plan).

#2 Participant-Level Advisory Services, Specifically Individualized Participant Advice

Many firms also provide what they call ‘financial planning’, which typically means having a representative offer advice to participants, and the cost of this advice is often added to the overall cost of the plan (which is nearly always an AUM fee). It is very rare that this service delivers any value, and plan sponsors nearly unanimously agree that most plan participants never use this service. If the firm also offers personal financial planning services to retail clients (in addition to servicing retirement plans), this could create a conflict of interest. Employees and representatives of advisory firms offering advice to participants are rarely supervised by the plan sponsor, so it is not known whether their advice is offered in the best interest of plan participants. The plan sponsor in most cases does not even realize that they are responsible for supervising financial representatives offering advice to participants. If a plan sponsor would like to offer personalized advice to plan participants, it is always best to hire an independent specialist firm that provides advice as an ERISA 3(21) to participants only, has no conflicts of interest (such as trying to seer participants into the firm’s retail advisory services), and charges a separate fixed fee. This way you can choose whether to add this service if it fits your plan needs vs. simply paying a higher fee for a service you might not want in the first place.

#3 All-Inclusive (‘Bundled’) Platform That Includes a Third-Party Administration and Record-Keeping Services

For plans set up by medical and dental practices, it is always advisable to hire your own TPA rather than rely on the TPAs that work for the record-keeper.The key differences are as follows:

- Your own TPA works directly for you. Record-keepers have thousands of clients and only a handful of TPAs, so you can’t expect the same level of service from a record-keeper.

- Independent TPAs are specialists in plan design and administration while a record-keeper has fewer resources to provide the higher level of services required by medical/dental plans.

- Independents TPAs are experts in compliance and fixing retirement plan errors, while a record-keeper is not. This is important because you want to make sure that any errors (which occur all the time even with the best oversight) are fixed in a timely fashion to avoid any future problems.

Advisory firms working with bundled platforms usually do not offer advice directly to the plan sponsor, but they charge significant AUM fees for their services nevertheless, so even if there is a bundled ERISA 3(38) ‘advisor’, chances are you will never get to talk to them. A good independent ERISA 3(38) fiduciary can bring significant value to a group plan since they can provide the following services:

- Select a low-cost investment menu

- Build a number of managed portfolios for the staff

- Assist with selection and evaluation of quality service providers that don't charge any AUM fees, including Third Party Administrators, record-keepers and actuaries.

- Assist with any plan-related matters, such as evaluating a Cash Balance plan option for the group, improving existing plan design, and doing all they can to minimize plan sponsor fiduciary liability (such as by converting brokerage-only plans into plans with an investment menu, for example).

While there are so-called ‘low cost’ retirement plan providers (specifically, record-keepers that bundle everything under one roof), when it comes to complex retirement plans (such as group practice plans or 401(k) with profit sharing plans that require more sophisticated designs), saving money on service providers that can add significant value to your plan is not going to help your bottom line.

Takeaways

- AUM fees grow with your assets, and because your plan assets will always grow due to continuous contributions, this is a lucrative source of revenue for the retirement plan service providers. With AUM fees, your expenses will grow as your portfolio grows, even though the level of services provided remains the same, so for that reason, AUM fees are nearly always more costly than fixed/flat fees over several decades.

- A startup plan might not have any assets in the beginning, but AUM fees will increase rapidly as your assets grow, especially if you are maximizing your retirement plan contributions.

- An established plan with significant assets has to make an effort to eliminate most if not all AUM fees from the plan to avoid overpaying for services. This is especially true for group practice plans where most of the assets belong to the partners.

- Paying AUM fees using your business cash flow will definitely save you money over time vs. paying the fees out of your assets, but this still will not avoid the significant disadvantage of having your fees grow over time, so instead of having a fixed fee that’s paid year to year, the business will face an increasing burden of having to pay AUM fees that grow every year from cash flow.

- You should not pay any AUM fees to your service providers. Record-keepers and TPAs should be paid a fixed/flat fee for their services. Record-keepers often have a custodial fee component that is AUM, and this fee should be around 5 bps or less. Your plan advisor should be an ERISA fiduciary (ideally an ERISA 3(38) fiduciary), and they should not be charging any AUM fees for their services. Our retirement plan cost comparison calculator can be used to calculate the fees you are paying in your retirement plan as well as to compare various retirement plan proposals side by side.

- When comparing plan service proposals side by side, there are several things to consider:

- Will you be getting the same service quality from your potential service providers? A lower cost proposal does not mean it is a better one if the service quality is lower as well.

- Are there conflicts of interest that you should be aware of? If you have a bundled service provider, they don’t have to make sure that all of the parts are best/lowest cost for your plan – they are simply selling everything as a bundle, so you need to be aware of this.

- Are there any revenue-sharing arrangements whereby your service providers use specific mutual funds because they are getting reimbursed by these funds? In that case, you will not get the best/lowest cost funds for your plan.

- Are you working with a fiduciary who will work with the plan sponsor to get you the best/lowest cost plan for your practice, or are you working with a service provider who is only selling their own bundled platform?

- Are your service providers taking care of all of your retirement plan needs? Or are they providing only the most rudimentary services to your plan, while your plan can benefit from more sophisticated services?

- How to Run a Successful Retirement Plan for a Medical or Dental Office

- Small Practice Retirement Plans

- The Ideal Retirement Plan for Your Practice

- The Best 401(k) Plan: Pooled or Participant-Directed?

- Cash Balance Plans for Solo and Group Practices

What do you think? Do you agree with Mr. Litovsky's analysis, conclusions, and recommendations?