While we all hope to remain healthy and injury-free during our prime working years, millions of people become disabled every year. Disability insurance protects doctors and dentists with partial income replacement should we become disabled for any number of reasons. You’ll find various options when choosing disability coverage, such as short-term and long-term disability insurance as well as Guaranteed Standard Issue (GSI) disability insurance.

Dentists and other medical professionals should seriously consider disability insurance if they don’t have ample savings to get them through years without working, perhaps even retirement. Here’s a closer look at how disability insurance works and what you need to know about short-term and long-term disability coverage as a dentist.

What Is Disability Insurance?

Disability insurance is a type of insurance coverage that provides an income if the policyholder is unable to work due to a disability. While some government programs offer a level of disability insurance, financially savvy individuals supplement it with disability insurance from a private insurer to ensure their needs are met.

With disability insurance, you’ll typically pay a monthly premium as long as your policy is active. Should you ever become disabled, either due to injury or illness, disability insurance pays you an amount every month up to policy limits.

You’ll find that disability insurance comes in short-term and long-term versions, and everyone may not need both. But for most employed individuals, including self-employed dentists, long-term disability is an essential financial protection.

Why Do Dentists Need Disability Insurance?

According to the Council for Disability Awareness, 5% of working Americans experience a short-term disability, with almost all unrelated to their work. Of today’s 20-year-olds, 25% will be out of work for at least a year at some point due to a disabling condition before reaching retirement age.

The most common reasons someone becomes disabled include musculoskeletal disorders, injuries, cancer, digestive issues, mental health issues, and circulatory diseases. Taking a tumble on a ski vacation, a bite from a disease-carrying mosquito, a repetitive motion injury, a car accident, a heart attack or stroke, or a cancer diagnosis are all common reasons for someone to become disabled.

The cost of losing your income for a few days or weeks may not significantly impact you and your family, but consider what would happen if you were out of work for three months with no pay. What would you do if you couldn’t work for a year or two? While you hopefully never end up in that situation, there’s always a chance. That’s why disability insurance exists for dentists and doctors.

More information here:

A Pain in the Butt – My Dental Disability Story

How Does Disability Insurance Work?

Disability insurance offers a payment if you become disabled, but understanding how it works can be a bit more complicated. Here’s a closer look at how disability insurance works for dentists and other covered individuals.

Understanding the Definition of Disability

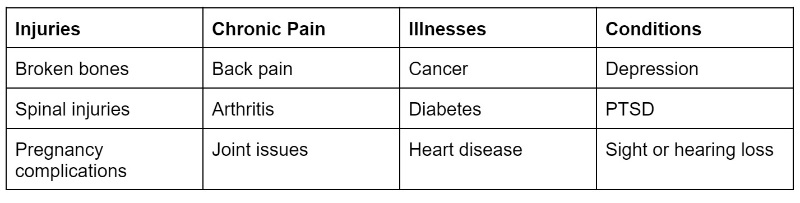

Disability can include a wide range of injuries, illnesses, and chronic conditions. Even pregnancy may be included in some disability coverage. Here’s a list of examples of disabilities covered by the major provider New York Life.

Disabilities can happen at any time, even to people with excellent health. For example, I was bitten by a mosquito in college that gave me West Nile Virus, which led to viral meningitis. I was in bed for a month, and it took about six months to get back to my regular schedule. If that happened today, I would get benefits from my disability insurance to make up for the time I couldn’t work.

What Does Disability Insurance Cover?

Disability insurance is all about income replacement. The amount you would qualify for is set in your policy documents. You can generally pay more for higher payouts if you’re disabled. And while it would be nice if there were a single type of disability coverage that includes everything anyone would need, you need two policies to cover the varying time horizons of a disability.

- Short-term disability coverage typically offers payments for a term of 3-6 months, and there may be a waiting period before coverage begins. For example, you could get coverage for three months after a one-month waiting period. Short-term disability usually covers a significant percentage of your income, perhaps up to 70%.

- Long-term disability coverage typically requires a longer waiting period and offers much longer payment periods. For example, you could have a plan covering five years, 10 years, 20 years, or longer. Shopping around can help you find the right mix of coverage and cost for your finances. Long-term disability often pays 40%-70% of your income.

What Is the Difference Between GSI, Individual, and Group Disability Coverage?

When shopping around, you may come across multiple types of disability insurance. Here are the three most common that dental professionals should know about:

- Individual Disability Insurance: Individual disability is insurance purchased by an individual directly from an insurance company. You may not get a price as low as a group policy, but you can keep it even if you change employers. You may have to go through a medical review to get this type of coverage.

- Group Disability Insurance: Group disability coverage generally comes as an employee benefit. Employers often cover a portion of the cost, making it more affordable for the insured. However, you lose coverage if you change jobs. A medical review isn’t typically needed for group disability up to a certain limit.

- GSI Disability Insurance: GSI disability insurance is guaranteed without medical underwriting and is generally intended to offer portable coverage if you change jobs. But it is first purchased through an employer group, such as a hospital or healthcare company. Check out our detailed guide to GSI Disability Insurance. Keep in mind, GSI Disability Insurance for Dentists may be hard to come by. It's best to check with one of our vetted insurance agents for doctors and dentist to find options that are right for you.

Should You Use ADA Disability Insurance?

ADA Disability Income Protection Insurance is a plan exclusively for ADA members and is underwritten by Protective, a major insurer. Premiums may be reasonable for many dentists, particularly those with past health issues who may not be able to get individual coverage elsewhere. However, those premiums go up every 5 years and are not guaranteed. In addition, there are other features within the ADA policy that may be lacking that other fully underwritten plans may offer. Features like full mental nervous coverage, recovery benefits that last until retirement age, and coverage that continues even if your billable hours drop below 30 hours a week. All coverages you may be able to obtain by going to an insurance carrier vs. through the ADA plan.

You’re best off shopping around and comparing ADA disability insurance to other options to ensure it’s the most cost-effective coverage for your needs. You may get both individual and ADA coverage to build a strong safety net if you become disabled.

More information here:

People Aren’t Buying Disability Insurance, But They Should

How Much Disability Insurance Coverage Should Dentists Get?

To determine how much disability insurance coverage you need, consider your income, expenses, and savings. There’s no universal answer for everyone, so you need to take the time to understand your financial situation to decide what’s suitable for your household.

For retirement, a common reference point is that investors can take 4% of their investment account value out annually and never run out of money. Look at your available investments, determine how much 4% would offer, and subtract that from your living expenses. You need to cover the remainder with income, and that number could be considered a minimum for long-term disability insurance.

How Much Does Disability Insurance Cost for Dentists?

Individual disability insurance generally costs around 1%-3% of your income for adequate coverage. You’ll pay more as you get older, and certain lifestyle risks can lead to more expensive coverage. If you’re familiar with the factors that go into pricing life insurance, the considerations are similar for disability insurance.

You’ll pay more for riders, which are added features to enhance an insurance policy. For comparison, ADA disability insurance for dentists costs between $46.91-$354.46 per month for plans with a 90-day waiting period.

More information here:

Is Dentistry Worth It? Comparing It to Being a Pediatrician, a Planner, and a Plumber

Which Disability Insurance Riders Should Dentists Add?

Again, there’s no universal answer to which riders a dentist should add when buying disability insurance. Here are a few common riders to consider:

- Non-Cancelable and Guaranteed renewable rider: provides assurance that you can renew your insurance–see what we did there? With this add-on, as long as you pay your premiums, you can keep the coverage as long as you’d like and your premiums won't go up.

- Inflation protection rider: This rider adds cost-of-living adjustments to your policy. Your premium and benefits increase over time with inflation.

- Residual benefits rider: This addition allows you to get a partial disability insurance benefit if you can still work but at a reduced capacity.

Where Can Dentists Buy Disability Insurance?

Dentists can buy disability insurance through their employer, through the program for ADA members, or from an independent insurance agent. We like the benefits of an independent agent, as they can help you shop multiple plans to find the best deal for your unique situation and needs. Check out our listing of vetted insurance agents for doctors to kickstart your search for adequate disability insurance coverage to protect yourself and your family for years to come.

The White Coat Investor is filled with posts like this, whether it’s increasing your financial literacy, showing you the best strategies on your path to financial success, or discussing the topic of mental wellness. To discover just how much The White Coat Investor can help you in your financial journey, start here to read some of our most popular posts and to see everything else WCI has to offer. And make sure to sign up for our newsletters to keep up with our newest content.

The White Coat Investor may receive compensation from White Coat Insurance Services, LLC; licensed in all states including MA and DC; CA license #6009217; NY license #1758759 (exp. 6/2027); Registered address: 10610 S. Jordan Gateway, #200 South Jordan, UT 84095. This does not affect the cost or coverage of insurance.