In my Living Against WCI Advice (AWA) column, I explained why my wife and I want to change the asset allocation for our financial independence (aka retirement) portfolio: my desire for simplicity has become greater than my conviction in the long-term outperformance of small cap value (SCV). Our current asset allocation is 98% stocks and 2% crypto, and our stocks consist of index funds for the following: 60% US total stock market (TSM), 15% US SCV, 20% international TSM, and 5% international SCV. We want to change our allocation of stocks to 75% US TSM and 25% international TSM.

I asked the WCI forum (where you find many live AWA in minor ways) about whether and when I should change my asset allocation. While many members were supportive of my decision, their advice was wide-ranging as to the timing, so I will summarize them here before I share our plan. Just as a written financial plan helps me stay the course, this column will serve as a written transition plan to help us stick with our decision.

Option #1 — Do It Now

One could argue the only thing stopping me from changing our asset allocation is market timing. If I want simplification, à la JL Collins, then I am already willing to sacrifice any extra long-term return. If I agree with BigERN and do not believe in the SCV premium, then I should not be swayed by the short-term outperformance of SCV over TSM so far in 2026.

All our SCV stocks—specifically, Avantis US Small Cap Value ETF (AVUV) and Avantis International Small Cap Value ETF (AVDV)—are in my wife’s and my Roth IRAs, so selling them and buying TSM stocks would not have any tax consequences. But my reservations for choosing this option are twofold.

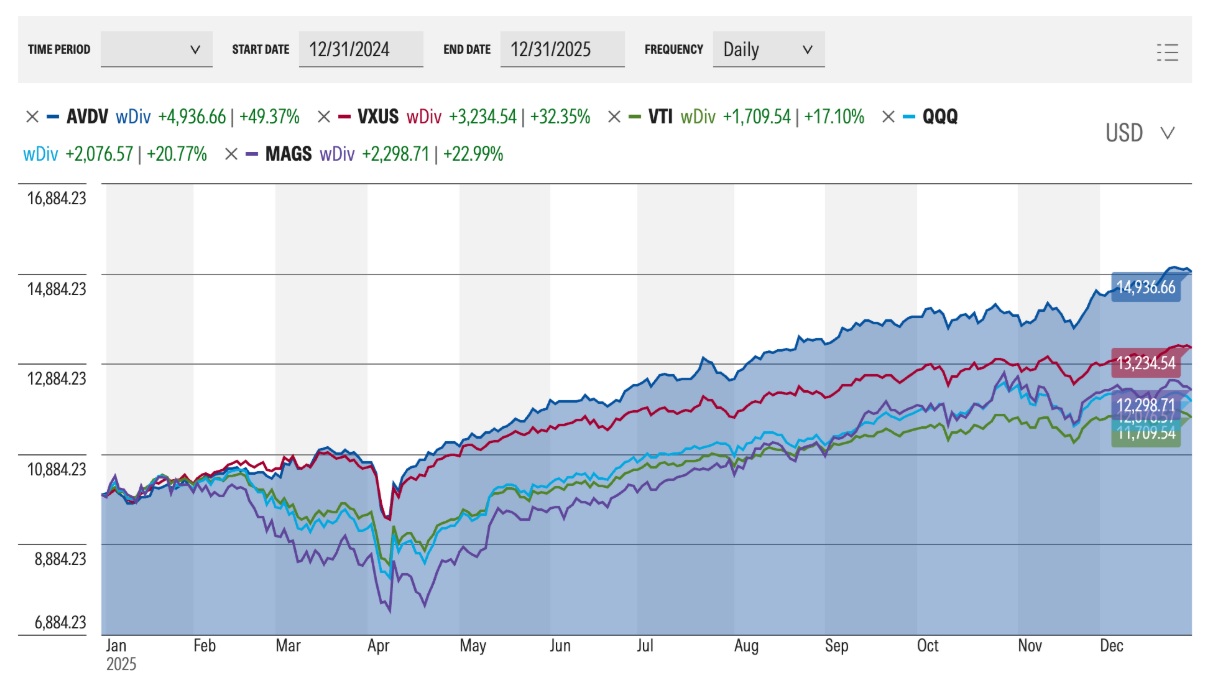

First, BigERN and many other skeptics have focused on US SCV, but international SCV has outperformed international TSM (VTIAX) since the inception of Dimensional Fund Advisors’ international SCV mutual fund (DISVX) in 1996 or the nadir of the Global Financial Crisis.

Second, momentum is a thing: an all-time high tends to beget the next all-time high. Since January 1, 2025, international SCV crushed not only international TSM but also the US TSM (e.g., VTI), NASDAQ 100 (QQQ), and Magnificent 7 stocks (MAGS). Selling AVDV would be a huge bet against momentum. Because of its large outperformance, our allocation to international SCV has increased from 5.04% at the end of 2024 to 7.36% at the end of 2025.

Some consider 10% to be the minimum allocation for meaningful diversification and dismiss the significance of our 5% allocation to international SCV. But except for crypto, I do not think anyone has run the numbers to know the real answer. Many portfolios in the growing list of 150+ portfolio examples allocate 5% or less to an asset class. David Swenson, the legendary chief investment officer at Yale, wrote in his book Unconventional Success: “Diversification requires that individual asset-class allocations rise to a level sufficient to have an impact on the portfolio, with each asset class accounting for at least 5%-10% of assets.”

Even if its 2026 outperformance is much less than that of 2025 (as any WCI reader knows, my crystal ball is cloudy), we would not want to miss out on such significant gains by choosing option #1. If I were not going to sell our international SCV stocks all at once, I did not want to sell our US SCV stocks either. As luck would have it, both the US and international SCV have outperformed their TSM counterparts year-to-date by the end of June 2026.

More information here:- Why the Small Value Tilt Works: A Psychological Perspective on a Persistent Premium

- Value Tilt — Don’t Give Up on Your Small-Cap Value Strategy

Option #2 — Don’t Sell SCV and Stop Buying SCV

This option would be a psychological hedge against SCV outperforming their TSM counterparts for the next 20-30 years. While our asset allocation on paper would exclude the US and international SCV, I would still hold on to our existing AVUV and AVDV shares. By not buying any more AVUV or AVDV, their actual allocation would eventually become insignificant.

This seemed like the worst idea. Unless I stop using our current brokerage firm, I cannot ignore them when I check our accounts online, and I do not want reminders of what I could have or should have done. Also, I do not want such a significant discrepancy (that is, beyond a few percentage points) between my paper asset allocation and actual asset allocation.

Option #3 — Wait Until I Sign My First Attending Contract

I am anticipating additional hassle with maintaining our current asset allocation when I become an attending. My attending salary will allow us to significantly increase our contributions to defined contribution plans (DCPs), such as a 401(k). Yet most DCPs my wife and I have had do not have my preferred SCV investments such as AVUV or DFA’s mutual fund. We might have to maximize the “asset location” of SCV in other retirement accounts and even hold SCV in a taxable account.

My fear might be unfounded. Before I sell off SCV, I might want to wait and see the available investment options within the DCP of my new job. As a psychiatry resident, the barrier to self-employment or ownership is low, as I can start my own private practice or join a partnership. This would allow me to contribute to a solo 401(k) in which I have the flexibility to buy AVUV and AVDV.

The timing of Option #3 aligns most closely with what I first had in mind. But my decision to change my asset allocation is not solely contingent on the degree of hassle that I would experience as I buy and sell stocks across multiple accounts. This decision also reflects what my wife would be willing to do if she were on her own.

More information here:Our Transition Plan

I will sell all of our SCV holdings on the first business day of 2028, January 3. The main reason is my obsessive-compulsive personality. Although I will likely start my attending job between July and December of 2027, I keep track of our savings rate and annual real return by calendar year. By implementing our new asset allocation in 2028, our money-weighted annual real return for 2027 will reflect the whole year of holding AVUV and AVDV and not include the randomness of when I sell them. Moreover, because I contribute a lump sum to our Roth IRAs on the first business day of the year, I can buy the US and international TSM index funds with both existing and new funds at the same time.

I anticipate that our allocation of stocks will remain as 75% US TSM and 25% international TSM for the foreseeable future because it hits the sweet spot of simplicity and global diversification. On paper, the “two-fund approach” is not as simple as owning a single fund (e.g., VT), but many DCPs do not have a total world stock market index fund. The static allocation does not reflect the current market-cap weights, but I do not want to bother tracking the actual weights.

We will add bonds to prepare for Sequence of Returns Risk as we get closer to retirement. We do not know when that will be, but we have a tentative written plan. Even then, I like that our international TSM allocation will be a multiple of five as we decrease our ratio of stocks to bonds from 100:0 (25%) to 80:20 (20%) or 60:40 (15%).

‘Personal Finance Is More Personal Than Finance'

Some might criticize our decision to change our asset allocation as if everyone’s financial plan should be immutable. But our decision is based on market history and self-reflection about our willingness to take risk and sacrifice simplicity. I even have receipts supporting our financial discipline.

I have heard the above saying over and over again because it proves to be true in so many personal finance decisions. I suspect that many WCIers similarly want to change their asset allocation because of life circumstances rather than fear or envy. A written transition plan can help them implement the change and reassure their skeptics, including themselves.

If you were about to become an attending, would you change your asset allocation? Is a small cap value tilt still a good play? What other options are there?