In your financial life, you should strive to be excellent at five money activities. They are: 1) earning, 2) saving, 3) investing, 4) spending, and 5) giving. Some excel at the first two, but they aren’t as good at spending. Some are great at investing but struggle with giving. Becoming superb at each of them will accelerate your journey to financial success.

For physicians and high income professionals, you can likely do anything you want, but you can’t do everything you want and certainly not all at once. The truth is most doctors spend too much money. Medscape surveys show that 25% of doctors in their 60s aren’t millionaires despite decades with a high income.

A physician cannot choose to pay for an undergraduate education at an expensive institution with loans, get married, have two kids, have a stay-at-home spouse, borrow the entire cost of medical school including living expenses, go into a low-paying pediatric subspecialty, defer the loans during residency and fellowship, and then spend three years at an academic center before becoming a hospital employee at a non-501(c)(3) in order to spend more time with the kids. Meanwhile, they’re buying a fancy physician home in a high cost of living area, get two nice cars on credit, have three more kids during training, put them all in private schools, vacation in Amsterdam, buy a boat, retire early, and choose a high-cost “financial advisor” who sells them lousy investments.

It just cannot be done.

There isn't enough income to cover all those choices. You could possibly do about a third of them and still be financially successful.

The most important aspect at the beginning of your financial journey is determining the right savings rate. If you start in residency (or at least shortly thereafter) putting 20% of your income away toward retirement, you'll never know what you're missing. Maxing out your retirement accounts will provide you with a lifetime of income, a big tax break, and protection of your assets from lawsuits.

Any budget is better than no budget. If you've never done it, just write down every dime you spend for two or three months. That'll show you what your budget is now, whether you know it or not. Then, you can decide if you need to make some changes.

A budget IS a personal thing since it demonstrates where your priorities are. You might not think of it that way, but if your budget DOESN'T reflect your priorities, it's time to make a change. For example, some people may spend more on clothes, transportation, vacations, or their home. Others might direct a large chunk of money toward paying down debt or toward retirement. Still, others may give a lot to charity. Some may even be embarrassed to reveal that they're spending most of what they make—or even more than they make. No wonder no one wants to talk about this.

Enroll in WCI Financial Boot Camp, a FREE educational email series, and learn to convert your high income to wealth

You can unsubscribe anytime using the link at the bottom of any email.

It helps if you think of the process of budgeting not as a constraining, boring process but rather as a plan for financial independence. Tons of marriages break up over financial issues. Budgeting done properly can essentially eliminate relationship fights over money.

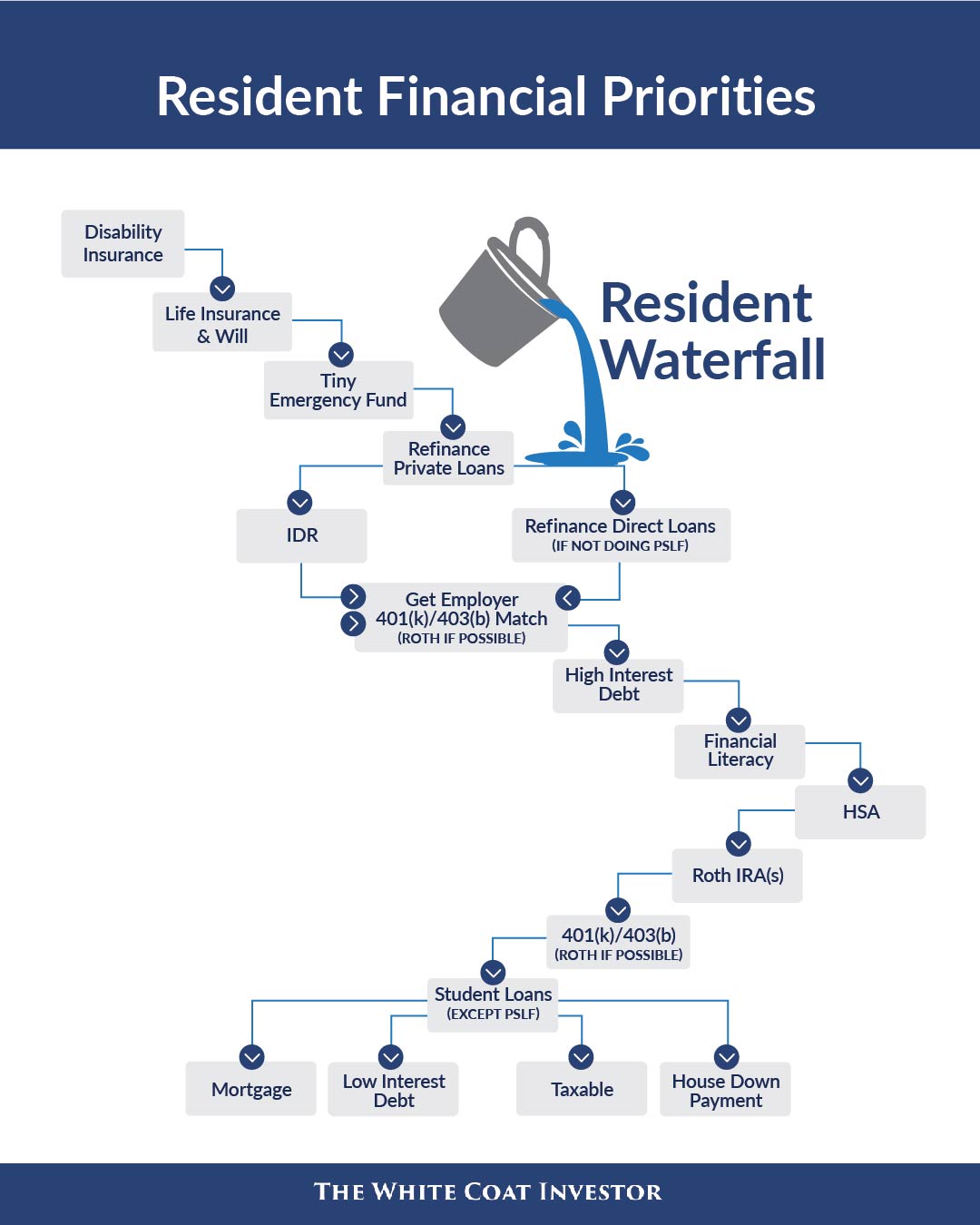

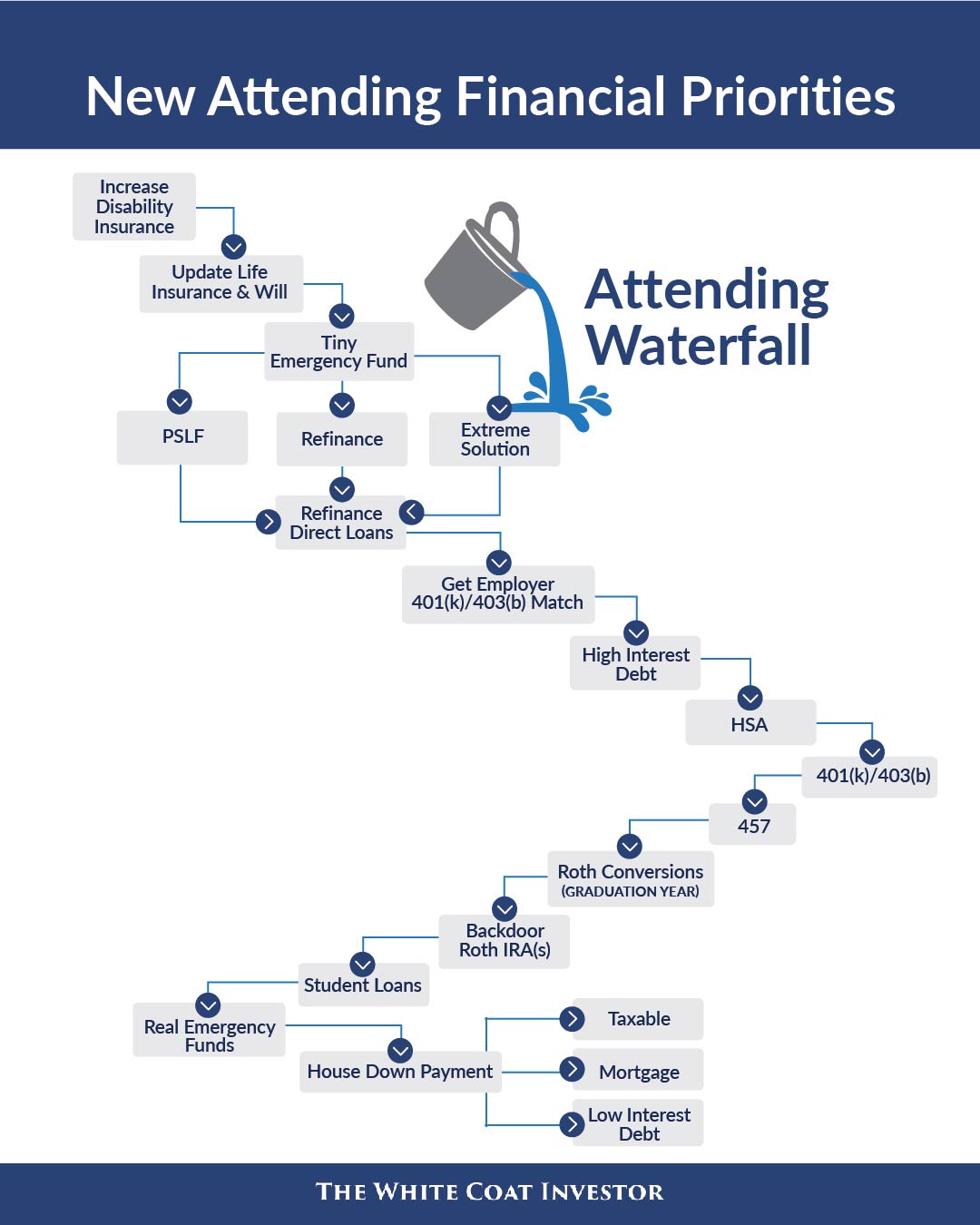

Doctors love this kind of thing—a list that tells them exactly what to do with their money. Reality is a little more complicated than just a list, and a hardcore hobbyist can usually pick a few nits with any list. But they're still pretty useful as a rule of thumb.

Medical school may not have taught you about money, but we will.

We will never sell your information. Modify your preferences or unsubscribe at any time.

Get ready to take control of your financial life. You can do this, and we can help.

We won't sell your information. Modify your preferences or unsubscribe at any time.