Imagine year-round skiing, efficient public transit, and a chocolate aisle that feels like a public service. This is life in Switzerland. Or perhaps you prefer the Dominican Republic in the Caribbean, with sun, walkable beaches to wiggle your toes in the sand, and a pace of life that makes Monday feel optional. For some physicians, moving abroad represents this long-planned reward. After years of training and delayed gratification, the idea of practicing medicine while enjoying alpine weekends or ocean mornings feels well-earned. What rarely makes the vision board is US tax compliance.

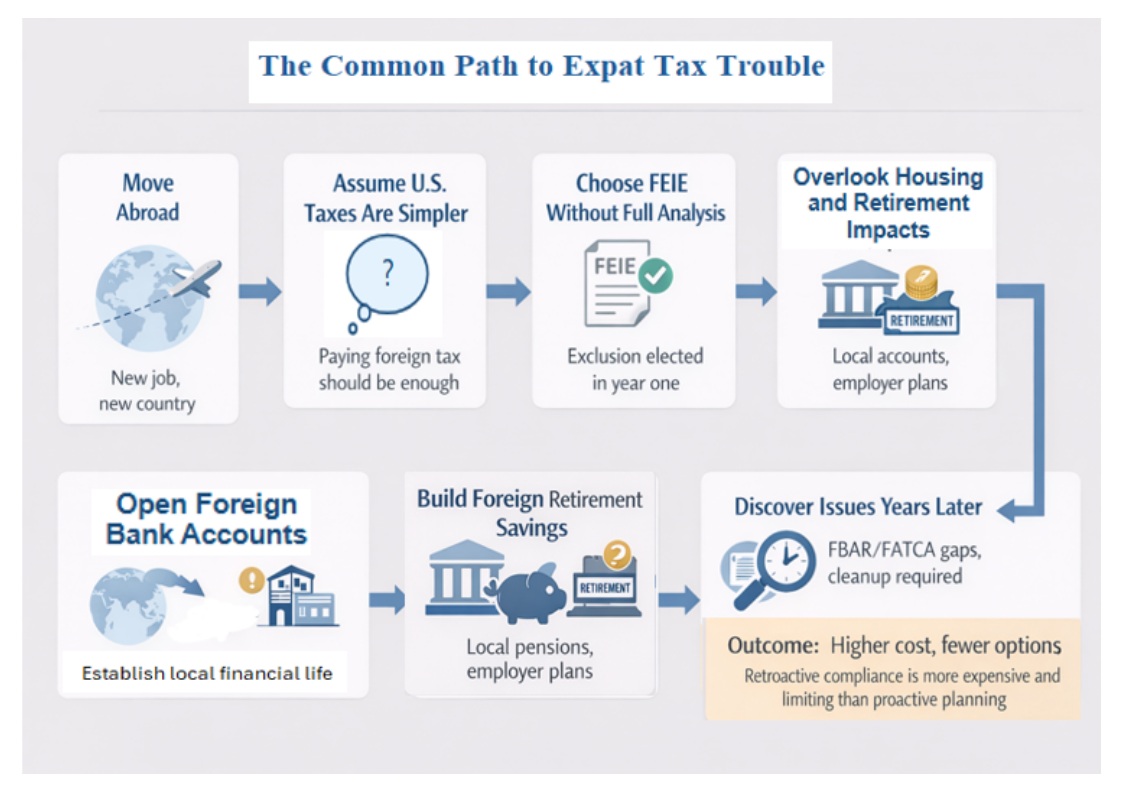

Many physicians assume that once they move overseas, US taxes become simpler. They pay foreign tax, earn foreign income, and live outside the United States. Surely that must reduce IRS involvement.

In reality, living abroad often increases reporting requirements, introduces new classifications, and raises penalty exposure. High-income professionals are especially vulnerable because the rules are unintuitive, widely misunderstood, and significantly more complex.

Why Physician Expats Get This Wrong

Doctors are accustomed to mastering complex systems, but international tax compliance is rarely intuitive. Most expats rely on advice from colleagues, online summaries, or foreign accountants unfamiliar with US reporting. The result is confident decision-making based on incomplete information.

Unlike most countries that tax based on residency, the United States taxes its citizens on worldwide income regardless of where they live—a system shared by only a handful of nations.

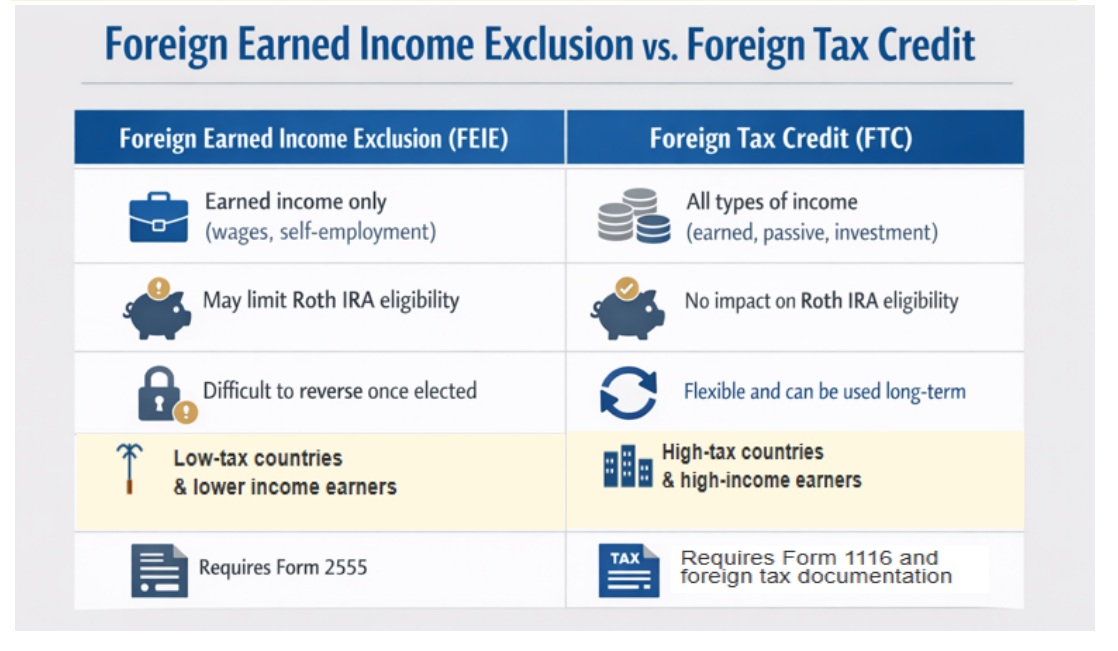

Pitfall #1: Overestimating the Foreign Earned Income Exclusion

The Base Exclusion

The Foreign Earned Income Exclusion (FEIE) allows qualifying US taxpayers living abroad to exclude a portion of earned income from US taxation on IRS Form 2555, subject to strict eligibility rules and an annual cap. The exclusion is not automatic, and it does not apply to investment income or eliminate foreign reporting obligations.

While the FEIE can be valuable in certain situations, it often produces suboptimal results for high-income physicians in high-tax countries, particularly when compared to the Foreign Tax Credit (FTC).

The Housing Exclusion Complication

In addition to the base exclusion, qualifying taxpayers can also claim a Foreign Housing Exclusion or deduction for certain housing costs above a baseline. This benefit has strict limitations, varies by location, and often provides less relief than expected in high-cost cities.

More importantly, the housing exclusion shares the same strategic limitation as the FEIE itself: it may reduce current US income tax while creating long-term disadvantages compared to the Foreign Tax Credit, particularly for high-income physicians.

For example, a physician earning $200,000 in Germany uses the FEIE to exclude $130,000 plus an additional $30,000 through the Foreign Housing Exclusion for high rent costs. Over five years, they lose the ability to contribute $35,000+ to a Roth IRA. As their income rises to $300,000, the FTC would provide better results on their full income, including housing costs offset by foreign taxes paid. But the early FEIE years cannot be undone, and those lost contributions represent permanent opportunity costs.

Why the Foreign Tax Credit Often Wins

For many high-income physicians in high-tax countries, the Foreign Tax Credit often produces better long-term results than the FEIE. Once the exclusion is elected, reversing course can be difficult and costly. This is a strategic decision, not an administrative one.

For example, a physician earning $250,000 in Germany or Australia will exceed the exclusion threshold by roughly half their income. In these high-tax jurisdictions, the Foreign Tax Credit typically provides full relief on all income without the complications of splitting income sources or limiting retirement contributions. Additionally, using the FEIE can reduce or eliminate your ability to contribute to a Roth IRA, since the exclusion reduces your earned income for contribution eligibility purposes. The FTC, meanwhile, has no impact on the ability to make Roth IRA contributions.

Why FEIE Limits Roth IRA Contributions

With the exception of a spousal IRA, you must have taxable compensation (earned income) to contribute to a Roth IRA.

Because the FTC doesn't exclude income (it only provides a credit for foreign taxes paid), all income still counts as taxable compensation for Roth IRA contribution purposes. In contrast, income excluded using the FEIE doesn't count toward the taxable compensation requirement for IRA contributions.

Pitfall #2: Assuming Foreign Retirement Accounts Mirror US Plans

Foreign retirement accounts are frequently misclassified.

These may include employer-sponsored pensions, mandatory government systems, or voluntary retirement savings accounts. Treatment varies depending on the country and the applicable tax treaties. Some receive favorable treatment, while others generate current US taxable income, additional reporting, or both.

Consider a Canadian TFSA (Tax-Free Savings Account) or an Australian superannuation fund. What the local government treats as tax-deferred, the IRS may treat as a foreign trust or a taxable investment account—triggering annual reporting on Forms 3520, 3520-A, or 8621, with penalties starting at $10,000 per form.

The primary risk is not taxation alone but incorrect classification that triggers cascading compliance failures.

More information here:- What Doctors Need to Know About Receiving Gifts from Abroad: Tax Traps and Filing Requirements

- Navigating the Minefield of Foreign Investing as a US Expat

Pitfall #3: Treating FBAR and FATCA as Minor Formalities

Foreign account reporting is mandatory, even when no tax is due.

Common errors include omitting dormant accounts, ignoring joint accounts with non-US spouses, and misunderstanding reporting thresholds. Penalties are assessed for missing forms, not unpaid tax.

FBAR penalties can reach $10,000 per violation for non-willful failures or the greater of $100,000 or 50% of the account balance for willful violations. These apply per account per year—meaning a physician with multiple foreign accounts can face significant penalties even when all taxes were paid.

Pitfall #4: Delaying Cleanup Until It Becomes Urgent

Many expats discover compliance issues years later, often during a home purchase, a foreign property sale, a return to the United States, or a change in tax advisor. At that point, correction is still possible, but it requires structured procedures and careful documentation. The IRS Streamlined Filing Compliance Procedures allow eligible taxpayers to come into compliance with reduced penalties, but they require certifying that prior failures were non-willful—a standard that becomes harder to meet the longer that issues remain unaddressed. These programs can eliminate penalties when handled properly, but eligibility matters.

What to Do Next

If you are planning a move abroad, consult a tax advisor with specific US expat expertise before your first day of foreign employment. Decisions made in Year 1—such as choosing between the FEIE and Foreign Tax Credit—can affect your tax position for decades.

If you are already abroad and uncertain about your compliance status, do not wait for a triggering event. A proactive review costs far less than reactive penalty abatement procedures.

More information here:- 5 Financial Considerations for American Doctors Wishing to Live Abroad

- When Everything Clicks into Place: How Foreign Travel Can Make You a Better Doctor

Key Takeaways

- Living abroad increases US tax reporting obligations rather than eliminating them.

- The Foreign Earned Income Exclusion and Foreign Tax Credit involve tradeoffs that often favor the tax credit for high-income physicians in high-tax countries.

- Foreign retirement accounts frequently create US tax and reporting issues when misclassified.

- FBAR and FATCA penalties apply even when no US tax is due.

- Seek advice from a tax professional with specific US expat experience before making irrevocable elections or foreign financial commitments.

The Bottom Line

Living abroad (and feeling the luxury of sand between your toes and eating scrumptious chocolate) does not simplify US taxes. It changes the framework entirely.

For physician expats, the greatest risk is not aggressive planning. It is unexamined assumptions. If you earn income, save, or retire outside the United States, your tax strategy should be intentional, not accidental.

The IRS does not forget expats. It simply waits.

What do you think? If you live or have lived abroad, what kind of tax planning did you do? Despite the tax complexity, is living abroad still worth it for you?