Due mostly to financial illiteracy, too many doctors actually think half of their money goes to taxes. Sometimes that's just because, as employees, they lump everything coming out of their paycheck (taxes, retirement account contributions, health insurance) into the term “taxes.” Sometimes it's because they're having WAY TOO MUCH money withheld from their paychecks and get massive tax refunds every year. But most commonly, it's simply because they don't understand the difference between marginal and effective tax rates.

Let's talk about the differences today.

What Is a Marginal Tax Rate?

Your marginal tax rate is the percentage of the next dollar you earn that goes to taxes. If you earn one more dollar and 45 cents of it goes to taxes, your marginal tax rate is 45%. While it's not exactly the same due to phaseouts and other quirks in the tax code, you can think of this as your tax bracket. This tax rate can be very high. A very high earner in California would pay 37% federal, 12.3% state, 2.9% in Medicare tax, and 0.9% in Additional Medicare tax. That's 53.1%, over half of whatever they earn! While it'd be a little unusual for a doc to have a 50%+ marginal income tax rate, it is possible. Much more common is something in the 24%-40% range.

What Is an Effective Tax Rate?

An effective tax rate is simply every dollar paid in taxes divided by every dollar earned in gross income. If you make $300,000 and you pay $50,000 in taxes, your effective tax rate is $50,000/$300,000 = 16.7%. Tax software will sometimes make some sort of effective tax rate calculation, but it often doesn't use your true gross income as the denominator. Typical physician effective tax rates are in the 15%-33% range when you add in federal income tax; state income tax; and payroll taxes like Social Security, Medicare, and Additional Medicare tax.

More information here:

You Should Do Your Own Taxes at Least Once – Here’s How I Do Mine

How Do Rich People Avoid Taxes?

Calculating Tax Rate

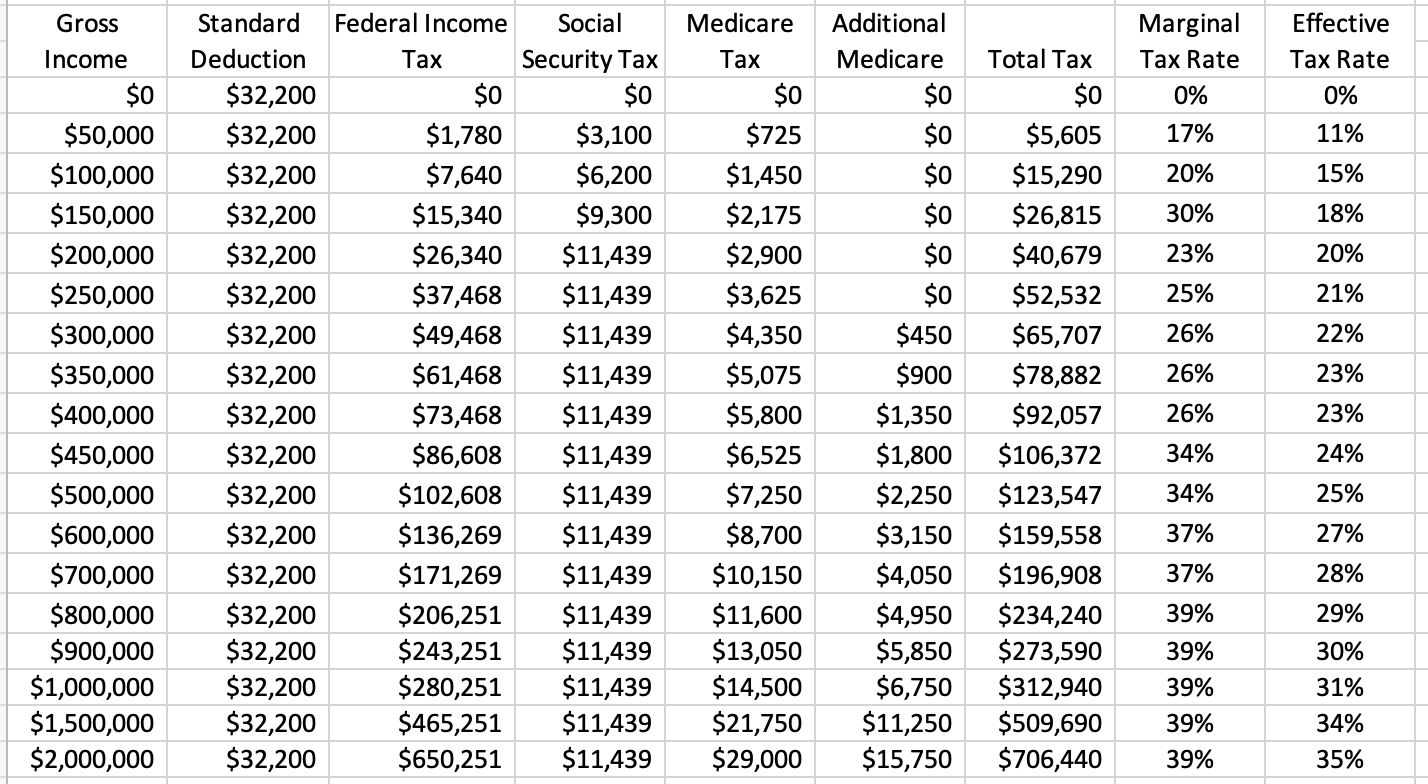

Let's make a chart illustrating this point. The chart won't be perfect. I'm going to ignore a bunch of phaseouts and things like that. We'll assume a married couple with one earner taking the standard deduction for 2026 and use 2026 tax brackets just to keep things simple. We'll also ignore state income tax since it is so variable. And we'll ignore credits like the Earned Income Tax Credit and Child Tax Credit that can actually give low earners a negative effective tax rate. We'll ignore the employer half of payroll taxes, too.

This obviously doesn't apply exactly to very many individuals. Most people live in a state with state income tax, which increases both the marginal and effective tax rates. Many high earners itemize, which would lower the effective tax rate. A two-earner couple would have higher payroll taxes, and a single person would move into higher tax brackets at lower incomes. We're also ignoring things like tax-deferred retirement accounts and HSA contributions. We're ignoring lots of phaseouts and credits. We're also ignoring any sort of investment income, which is usually taxed at a much lower rate.

But it's sufficiently accurate to illustrate my point. Here are the takeaways:

- At most typical physician incomes, the effective tax rate is in the 20%-27% range plus state taxes.

- At most typical physician incomes, the gap between marginal and effective tax rates is 3%-10%, decreasing with income.

- You would need a lot of earned income to actually pay half your earnings in taxes in any state. Even in California and if you only took the standard deduction, it would require over $721,000 in gross earned income before your marginal tax rate hits 50%, and it would take millions before your effective tax rate gets there.

I calculate our marginal and effective tax rates every year, and I think you should, too. Our marginal tax rate is 37% + 4.5% + 1.45% + 0.9% = 43.85%. Our effective tax rate for the last half-decade or so has been between 31%-34%. Given that our income is significantly higher than most physician incomes, I'm amazed at how many docs have higher effective tax rates than we do. You might want to consider living your financial lives a little bit differently.

Consider the following:

- Build a family

- Start a business

- Max out retirement accounts

- Max out an HSA

- Move to a lower tax state

- Give more to charity

- Invest tax-efficiently

- Retire

Do most of those “IRS-approved” activities, and you should get your effective tax rate into the 20s or at least the low 30s.