I wrote my column on Why I’m Still Buying Crypto in December 2021 when the price of Bitcoin was in the $40,000s. By the time my column was published in July 2022, it had dipped below $20,000. Many readers ridiculed me, and one WCI forum member (who might not have read the column) described it as a “copium.”

Now, crypto is bigger than ever. Bitcoin was above $90,000 when I wrote this in December 2024, and it surpassed $100,000 only a few days later. If you judge by the title of my columns, you would think that I am about to announce that I am quitting residency and retiring early.

But I am far from “winning the game.” My position in crypto is less than some physicians’ paychecks. In fact, cryptocurrency itself is unlikely to have a significant impact on my journey to financial independence. I can declare that I am winning with crypto because I have followed my financial plan. My 2022 column, at its core, was about doing just that. This column is also about its importance and challenges, with my personal examples of buying and selling crypto.

[AUTHOR'S NOTE: Nowadays, anything can be political. This includes crypto, as the outcome of the 2024 presidential election likely played a role in Bitcoin’s recent price momentum. But I do not mix politics and investing. You shouldn't either!]

My Investment Thesis (or Investment Policy Statement) on Crypto

My investment thesis for crypto has not changed from what I wrote in 2021: “Some smart people will figure out some useful things with crypto, and I do not want my [Fear of Missing Out] FOMO to affect other aspects of my financial plan.” Its first half has not panned out, as seemingly smart people were caught scamming others using crypto. Yet I continued to own crypto through its ups and downs because of the second half of my thesis.

If crypto went to zero, I would have been upset for a day or two (or a week or two) and then moved on because my portfolio’s annualized return has been above my goal of 5% real. Had I sold crypto, I would have been upset for the past year. Visiting The Wall Street Journal website or listening to my favorite financial podcasts would have been painful because they would remind me that everyone else who “HODL'd” crypto is getting rich.

Had I sold crypto, such negative emotions might have overwhelmed me into buying crypto again or taking more risk with individual stocks. Given the remarkable runup in 2024 (Bitcoin's price increased more than 120% for the year), I would have had a decent return if I bought crypto at any point between January and November 2024. The more likely outcome is that I would have anchored on the price at which I sold crypto and waited for a crash.

Ultimately, owning crypto has helped minimize my FOMO. Euphoria about technology stocks and crypto in 2024, just as in 2021, has been like a boiling kettle. I have kept my finger in the water, so I know how quickly the water gets hot and cold and how sensitive I am to the temperature changes. I have genuine respect for those who can tolerate rapid and dramatic changes. Inevitable are my occasional doubts about owning international and small cap value stocks, both of which have underperformed against the US large cap stocks. Yet I am content to be on cruise control with my current asset allocation because I do not want to experience the temperature rollercoaster in order to meet my investing goal.

More information here:

A Neurologist’s Road to Becoming a Bitcoin Maximalist: Why Bitcoin Is Not the Next AOL

My Crypto Allocation and Rebalancing Strategy

In 2022, when I opened a news app and saw that the price of Bitcoin dropped below $20,000, my heart sank a little. But I also remembered my plan for rebalancing. I checked my spreadsheet to see how much more crypto I would need to buy for its allocation to be 2% of my portfolio. Then, I opened my brokerage account to “buy the dip” without thinking (or asking my wife) because (1) it would not impact our cash flow and (2) my wife and I had discussed our plan for crypto during our annual financial review.

My current asset allocation is 98% stocks (all of which are in index funds) and 2% crypto. I settled on 2% because anywhere between 1%-5% seems to be the sweet spot for taking advantage of crypto’s volatility and its relatively weak correlation with stocks compared to the correlation between US and international stocks. The difference between 1% and 2% is negligible in terms of its impact on the overall portfolio, whereas going from 2% to 5% would add a significant amount of risk (and its associated emotions).

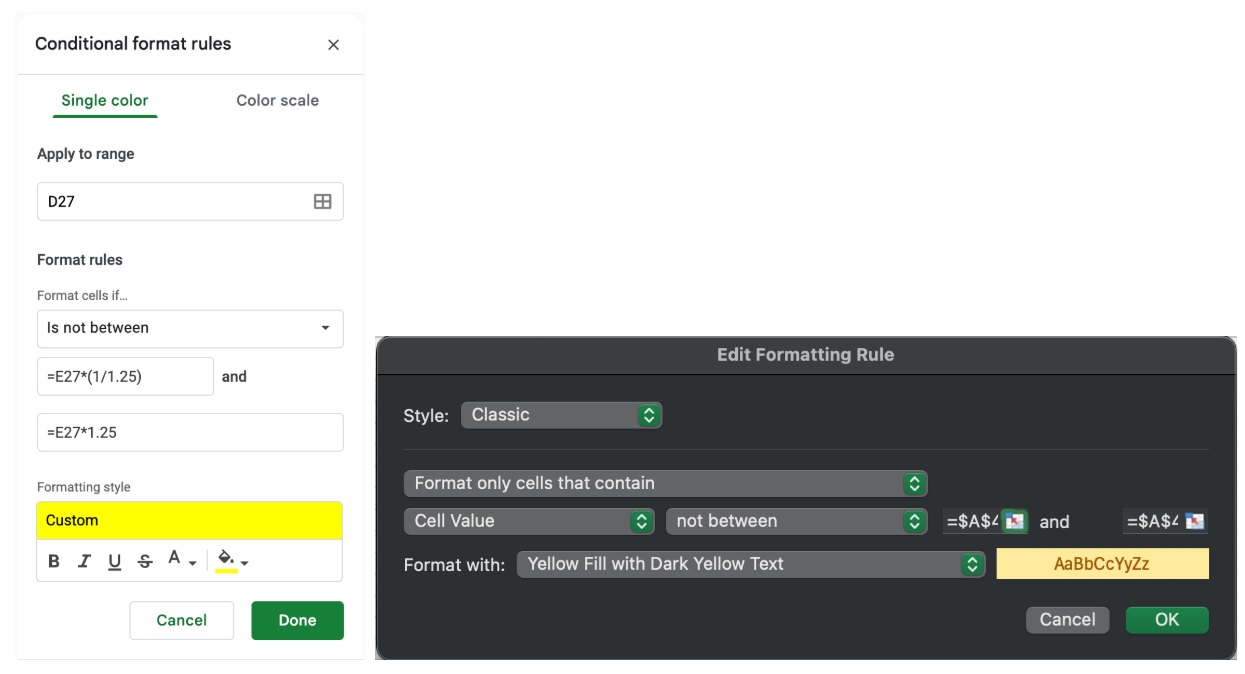

I rebalance stocks every year with new contributions to retirement accounts, but with crypto, I have been more “active.” I buy and sell crypto when the allocation reaches its lower and upper thresholds of 0.8x and 1.25x (that is, 1.6% and 2.5%), respectively. Any gains from selling are used to buy more stocks, whereas I buy crypto with cash from our checking account.

I have the rebalancing plan written down, and I also formatted my spreadsheet so that the cells turn yellow when the asset allocation exceeds the threshold. On Google Sheets and Microsoft Excel (see below), you can use the “conditional formatting” feature to make a cell change colors if the value in the cell is not between the lower and upper limits of your target allocation.

Even with such reminders, I am often reluctant to buy or sell when I own too little or too much crypto. Instead of buying a large lump-sum amount of crypto during its crash in the summer of 2022, my fear that the prices might fall even more led me to buy in only small amounts (below are my receipts). When crypto exceeded 2.5% of my portfolio in the fall of 2024, the price of $100,000 seemed imminent for Bitcoin, so my fear that I would miss out on further gains kept me from selling at $90,000, $95,000, and $98,000. I finally sold the excess crypto only because I started writing this column; I had to practice what I was preaching! Non-automatic investing is hard.

My Crypto’s Annualized Real Return

Calculating the annualized return of crypto specifically (I've previously explained why I do not calculate the returns of other asset classes) has helped me appreciate its volatility and reaffirmed my 2% allocation.

Until 2024, our annualized real return on crypto in our portfolio was negative (see chart below). Crypto lowered our portfolio’s 2022 return by 1.05%, while it improved our 2023 return by 0.88%. From 2021-2023, crypto lowered our portfolio’s overall annualized real return by 0.09%.

In 2024, our real return on crypto was 91% despite selling some Bitcoin for rebalancing (see chart below). Even though our allocation to crypto did not exceed 3% throughout the year, crypto improved our portfolio’s return by 1.29%, and our annualized real return on crypto took a dramatic swing from red to black. From 2021-2024, crypto improved our portfolio’s overall annualized real return by 0.22%.

(The inflation data for 2024 is from November 2023-November 2024.)

Based on our baseline projection of 5% real return for our portfolio, the improvement of 0.22% over a 30-year span would lead to an additional $2,800 for every $10,000. Although my crystal ball with crypto is pitch black, I would be pleasantly shocked if crypto continues to outperform at this rate as it becomes a mature asset class. It is hard to imagine that crypto would go through multiple cycles of volatility like 2022-2023 for 30 years.

However, the only thing I have been right about crypto so far is not selling at its low.

More information here:

Pros and Cons of Cryptocurrency Investing

“Never Interrupt [Compounding] Unnecessarily”

Crypto’s positive impact on my portfolio feels like a bonus because my primary reason for owning crypto is to not interrupt the power of compounding for the 98% portion of my portfolio. Quoting the late Charlie Munger on his first rule of compounding may be ironic because he also called crypto “rat poison.” Still, I hope he would have appreciated my commitment to following that guideline.

My first step in implementing his first rule of “never interrupt[ing compounding] unnecessarily” was creating a financial plan, and I deliberated on why crypto should be a part of it. I have not addressed in this column whether you should buy crypto “now” because I do not know your financial plan, knowledge of financial history, or experience with risk. I can definitively say that the price of Bitcoin should not be the reason. Otherwise, I imagine that crypto will be a rat poison and that you will break the first rule of compounding.

Have you been investing in crypto? Did you see big gains in 2024? Or are you content to watch from the sidelines?