By Dr. Hamik Martirosyan, Guest Writer

By Dr. Hamik Martirosyan, Guest WriterIncorporating this feature of markets in the construction of your portfolio may help to improve results. However, we have to be cautious so that this strategy does not morph into market timing. Instead, we should use it as a tool to supplement your investment plan.

In his book, Mastering the Market Cycle, Howard Marks discusses the cyclical nature of markets and how to utilize this tendency to position your portfolio for outperformance. He provides valuable insights which might be helpful to us white coat investors.

Nature of Cycles

Cyclicality is a constant feature of the markets. History shows markets fluctuate between greed and fear, optimism and pessimism, risk-tolerant and risk-averse, overpriced and bargain-priced, etc.

Cycling from one extreme to the opposite is a given. It is impossible for prices to increase to infinity, and conversely, it is unlikely that all asset values will go to zero. They must reverse course and progress in the opposite direction.

Just as important as the inevitability of cycles is the unpredictability of cycles. We know that cycles will happen, but we do not know:

- When it will happen (time)

- How rapidly it will happen (rapidity)

- How severe the reversal will be in the opposite direction (scale)

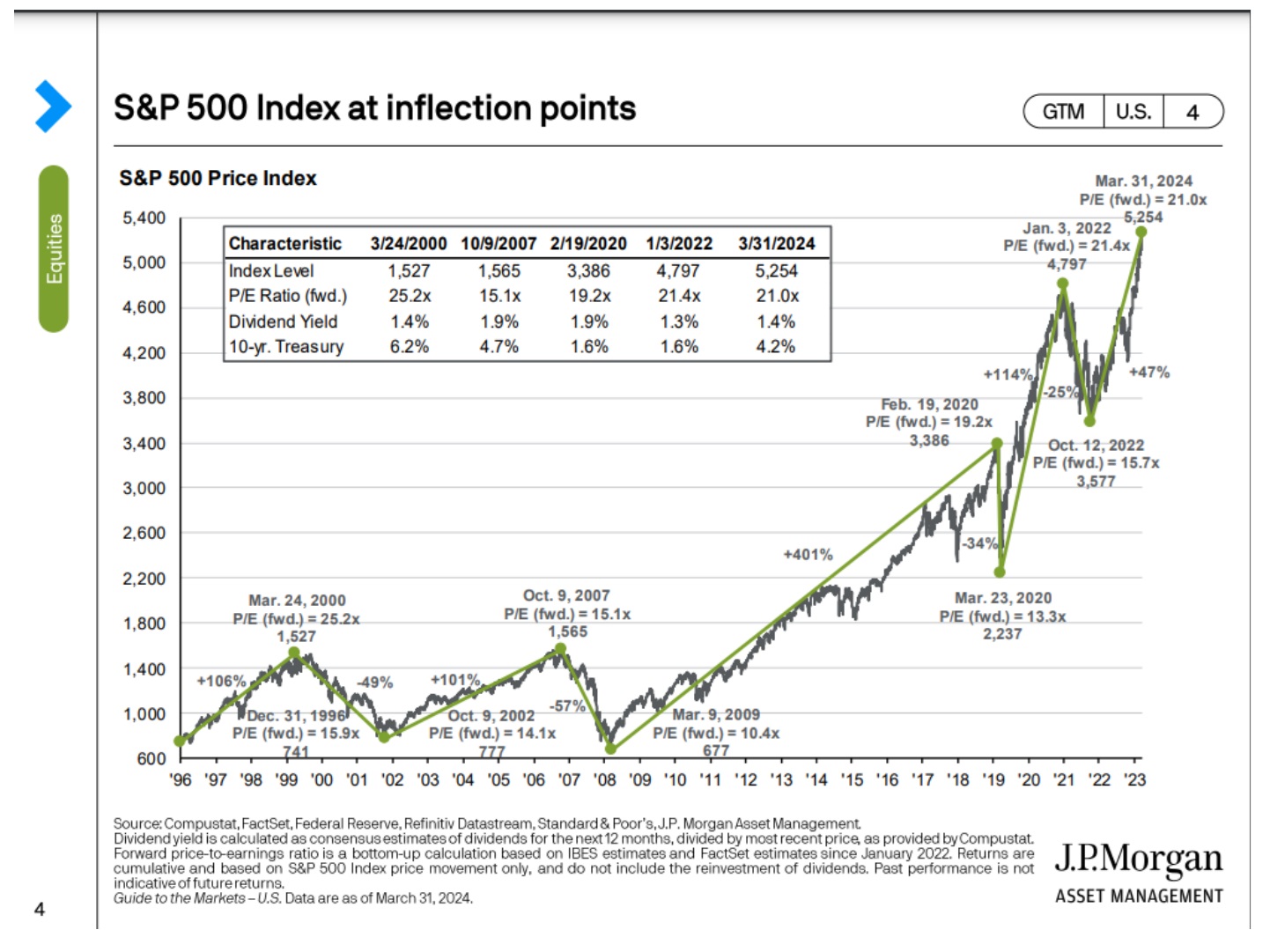

As a result, utilizing the cycle dynamics may not be as simple as it may seem. Putting these components together shows market return cycles as you would see for the S&P 500, for example.

The cyclicality of S&P 500 prices, via the JP Morgan Guide to the Markets

Cycles are self-correcting, and they do not necessarily rely on exogenous factors. The factors responsible for one portion of a cycle will sow the seeds for the next portion. Success will sow the seeds for failure and vice versa. Optimism will sow the seeds for pessimism and vice versa. Overpriced valuations will lock in lower future returns and future disappointment, eventually leading to bargain-priced valuations.

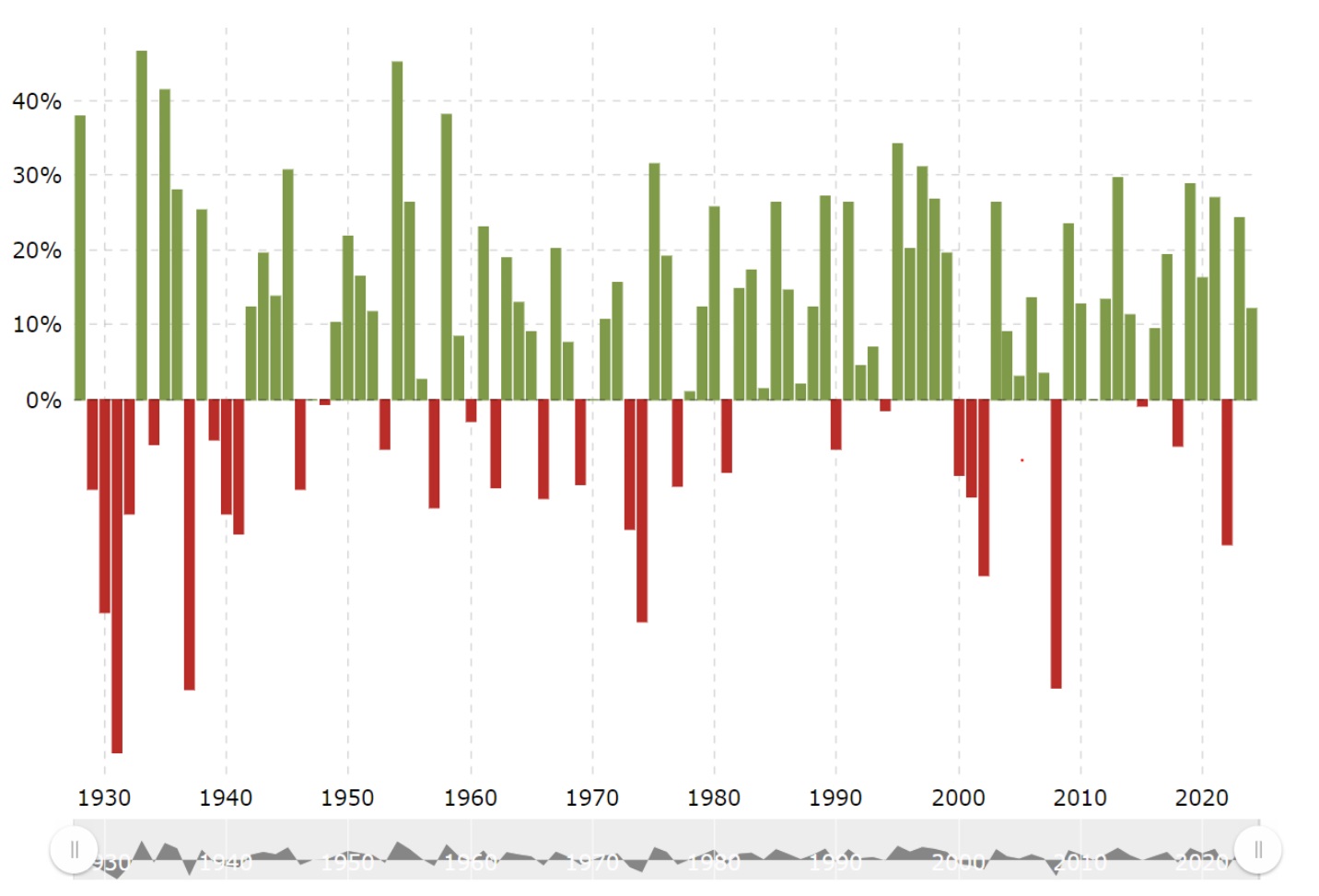

Cycles spend more time at the extremes and less time in the middle/average. Just like a pendulum has the highest velocity at the midpoint and spends the least amount of time there, the forces leading to cycle turnovers peak around the midpoint and cause rapid swings rather than stability at the center. The S&P 500 average annual return since inception has been around 10%. The chart below shows its annual return since the 1920s. It is a rare year when the S&P returns are at or close to 10%; most years see significantly higher or lower returns from this average.

Annual S&P 500 returns, via Macrotrends.net

One of the most, if not the most, important factors to cycles is investor behavior and psychology. The cycle is set by investor behavior rather than financial performance. We do not make decisions scientifically, solely based on financial performance. Instead, we are bound by our emotions. People are emotional and inconsistent, not steady and clinical. This is what leads to the cycles.

Different types of cycles, to name a few, include economic, business (profit cycle), investor psychology, risk, credit, and real estate.

More information here:

Optimists Are the Best Investors, Even If the Pessimists Sound Smarter

Stop Playing When You Win the Game

Typical Cycle Roundtrip

Upswing

An investment or strategy will start at an intrinsic value based on investment fundamentals, like revenue, income, and debt ratios. If there is a perceived benefit, there will be net buyers bidding up the price. Its success will elicit more buying, driving up the price even further. In some scenarios, we may see the formation of a bubble in which buying would continue as some may fear missing out. Continued success will lead to the belief that the investment can only go up and the old rules do not apply. Risk is minimized or ignored even though it is higher since the price being paid locks in lower future returns. Inevitably, since trees don’t grow to the moon, the price will peak, and the reversal will begin.

Downswing

Then, the next part of the cycle—the descent—will start. The catalyst may be a less hospitable economic environment or a black swan event, or it may simply be due to unrealistic expectations set by investors that cannot be achieved or maintained. Net selling will ensue. Prices will fall. Continued selling will feed on itself. No one will want to catch a falling knife. If severe enough, there will be minimal buyers, as most people will be tired of losing capital and will only care about preserving principal. All the negativity will be priced in.

The risk is lowest here when everyone is afraid. At a certain point, the sentiment is too bad to be true, and enterprising investors will jump in and begin the reversal to the upside.

The tech boom and bust of the late 1990s and early 2000s is a good example of a cycle. The euphoria of the tech innovations of the day created a tech bubble. Risk aversiveness was ignored, and fear of missing out was the prevailing emotion. The NASDAQ PE ratio was bid up to 200. Eventually, the unrealistic expectations became apparent as earnings and sales (as some did not even have positive earnings) disappointed. Overpriced valuations became apparent, and the selling began. The bust followed since the boom was not based on any inherent structural fundamentals. During the bust, the NASDAQ PE settled at a low of 10. That's 1/20th of the peak value.

Fundamentals could not have changed by a factor of 20 over a few years. The ups and downs were due to investor behavior.

Real Estate Cycles

Commercial Real Estate (CRE) shares the same characteristics as a typical market cycle, but it also has some additional important factors: development time and leverage.

Development Time

Ground-up construction is an important part of the real estate cycle. With buildings, you can't just turn the inventory up or down instantaneously. With how long it takes to build new properties, there is a lead time of 2-3 years. This may exacerbate cycles as the building will be started during boom times and avoided during busts. This may lead to a mismatch with market conditions when the construction is completed 2-3 years later and hits the market, exacerbating prevailing market conditions of the time.

Leverage

Credit is used in CRE, leading to leverage as acquiring real properties requires some debt. The credit cycle has its own characteristics. It is either open or shut, without an in-between. During booms, credit is openly available, even to those with poor capital structures. During busts, lenders stop lending or only lend with onerous terms. This leads to further exacerbation of the prevailing market conditions in both extremes.

We are seeing the current CRE cycle play out. Post-COVID, CRE went on a tear. During late 2020 to early 2022, multiple CRE investments popped up, and equity was easily raised with subscriptions. We started seeing unsustainable rent growths with some places growing at 20%. Some cap rates (valuation ratio for CRE, equal to Net Operating Income/Purchase Price) went down to historically low levels of around 3% (lower means more expensive purchase prices). Since it was so easy to raise money in both the equity and debt markets, poor capital structures were formed, including those with variable financing and high LTVs (loan to value).

Eventually, inflation caused rates to rise and exposed the unrealistic expectations with which investments were made. Variable rates started rising. Rent growth softened as new construction (started 2-3 years ago during the boom) added more supply to the market. This led to increased defaults and capital losses for investors. Cap rates have since increased to 5%. Though going from 3% to 5% does not sound like much, this, if all else is kept equal, would mean a price drop of 40%.

More information here:

The 60+ Worst Mistakes You Can Make in Real Estate Investing

Positioning Your Portfolio in Cycles

Marks recommends positioning your portfolio in cycles by assessing quantitative and qualitative factors of where we stand in the cycle.

Quantitatively, you would assess valuation measures—such as PE and CAPE ratios, capitalization rate (in CRE), and equity risk premium. Marks then gives a list of factors you would qualitatively assess to get a temperature check of how hot or cold the market is. Some include the economy, recent returns, the outlook, access to credit, risk premiums, investor psychology, and investor risk tolerance/aversion. This is not an exact science, but with enough diligence, it will provide utility.

Taken together, this will provide an estimate of where we stand in the cycle and help you decide if you should position in a defensive, offensive, or neutral position.

However, even the best assessment will not guarantee what will happen next. It will only show you the tendency of what may happen. It does not tell us what will happen with certainty. Instead, it tells you which is the most probable next step that will occur. Overpriced valuations can continue to rise temporarily (and vice versa) as markets can remain irrational longer than expected.

Practical Applications and Insights

Despite its utility, assessing the cycle is not a silver bullet. It might only be helpful during the extremes and not helpful during most years. Some examples of utilizing the market cycles are included below. To be clear, I am not advocating for market timing. I do not believe in market timing. The historical data shows that no one can reliably predict future performance.

But understanding the concept of cycles and assessing the market periodically may help you make fewer mistakes. This is done by identifying the extremes and avoiding buying during bubbles and selling low during panics. I think this is the most beneficial aspect of understanding cycles for us retail investors. We are playing a game of amateur tennis in which the winner is not who makes the best shots but who makes the least mistakes. This has hurt me when I have bought cryptocurrency due to the fear of missing out. And it has helped me recently in avoiding buying Tesla at a peak and avoiding buying NVDA currently.

Tilting

Rather than using it as a timing tool, it might be best to tilt your portfolio within the confines of your investment plan during the extreme years. For example, investors commonly use a range for asset allocation. During the COVID selloff when valuations tanked, I tilted my stock allocation to the higher end of my range. And during the end of 2021, when valuations seemed too high, I tilted my portfolio toward the lower range for stocks. At this time, I was not trying to time the market, but I wanted to take some risk off the table since I was progressing toward financial independence faster than I had anticipated. Risk de-escalation is in my investment plan and is based on aging and asset growth. I just accelerated this risk de-escalation as valuations appeared to be rich at the time.

Buying During Downturns

Marks mentions that it is more beneficial to buy when prices are falling and the bottom is unknown rather than during the upswing. Though it may feel like you are trying to catch a falling knife, continued buying will be beneficial in the long run. No one can perfectly time the bottom, and continued buying is important. Those who continued dollar cost averaging during prior bear cycles have been rewarded handsomely. As Dr. William Bernstein has said: if you are young, you should get on your knees and beg for a prolonged, painful recession. Your future self will thank you for it.

Investor Behavior

How investors behave may give you critical information, even though you might not be an expert in the asset class. Marks uses the Global Financial Crisis of 2008 and the subprime market as an example. He was not an expert with CDOs (collateralized debt obligations) and other exotic financial instruments, but based on how investors were behaving, he was led to believe that the US was in a housing bubble. This included home loans being made to people without verifiable income, negative amortization loans, people quitting their jobs to flip houses for a living, and the continued expectations of high price growth in housing.

Study and weigh investor behavior just as much, if not more, than the asset’s strategy and performance, and it will help your decision-making. This has helped me formulate my current plan around cryptocurrency. My decision on buying and selling crypto is based on how investors are behaving toward this asset class rather than the fundamentals of it. This most likely means that I will only buy when it is hated and left for dead. I might miss out on large gains if it succeeds, but I accept that, given its uncertainty and speculative nature. As Warren Buffett has said, “There are no called strikes in investing.” You do not have to pick every successful investment.

More information here:

How to Think About Risk and Why It’s So Hard to Quantify

A Tale of 2 Sponsors: How My Real Estate Investments Have Had Vastly Different Results

The Bottom Line

Cycles are an inherent feature of healthy markets. Investor psychology is perhaps the most important factor in dictating the cycle characteristics. Though cycles are an inherent feature of markets, they are unpredictable in that we don’t know when the tide will turn, how rapidly it will turn, how severe the turn will be, or how long it will last.

Estimating quantitatively and qualitatively where we stand in the cycle may help us tilt our portfolio so that we can achieve improved investment outcomes. This requires time, effort, and skill, and it is not a magic bullet. At a minimum, it may help us make less mistakes at extremes.

[FOUNDER'S NOTE BY DR. JIM DAHLE: One of the reasons we have guest posts at WCI is simply to provide a different perspective than my own, and that is why this post was selected to run. Those who have been reading this blog for many years know that I prefer a static asset allocation approach. It isn't that cycles don't exist or that if you could time the market well it wouldn't be super profitable. It's just that trying to take advantage of these cycles by tinkering with your portfolio in any way is just really hard. So hard that it probably isn't worth trying to do, especially after the costs (time and money) of doing so. Effective, long-term investing is so simple that it is hard to believe it even works. People figure it MUST be possible to add some value to the process by doing something else besides blindly buying, holding, and rebalancing a reasonable, low-cost, broadly diversified static asset allocation of index funds or similar investments.

Nobody wants to be that guy who put a bunch of money into the market in March 2000, July 2008, or February 2020 only to see it dramatically drop in value for a while. It's psychologically painful. But there's a reason all investment approaches are compared to this basic approach of just investing any time you have the money and staying the course with your plan. It's because everybody knows it works. It'll work for you, no matter how many market cycles you have to invest through. Nobody wants to admit tactical asset allocation (allocation changes made due to valuations or thoughts on the market cycle) is market timing, but that is exactly what it is. And a little market timing has the same issues as a lot of market timing—just to a lesser degree.]

Have you studied the market in depth to help you figure out when you should buy and sell? Or do you prefer more of a set-it-and-forget-it philosophy?