Inflation-protected securities often get lumped together. Treasury Inflation Protected Securities (TIPS) and Series I Savings Bonds (I Bonds) are frequently described as interchangeable tools for hedging inflation risk because both are backed by the US Treasury and both are indexed to the same inflation measure. But those surface similarities hide some important differences, including the risks associated with them.

How Did Inflation-Linked Bonds Come About?

The need for inflation-protected bonds became apparent in the 1970s when Treasury investors suffered deeply negative real returns. Inflation averaged roughly 7%-8% per year over the decade, frequently exceeding nominal Treasury yields. Bonds that were considered “safe” actually destroyed purchasing power, and inflation risk was borne almost entirely by bondholders.

The Volcker Federal Reserve ended that inflationary episode in the early 1980s, but it came at the cost of extremely high interest rates, forcing the Treasury to issue debt at historically elevated nominal and real yields. While inflation was brought under control, inflation risk did not disappear, and the government had little incentive to lock in those high real borrowing costs through indexed debt.

Another important obstacle was inflation measurement. Throughout the 1980s and early 1990s, the Consumer Price Index (CPI) was the subject of sustained controversy, with concerns about substitution bias, housing costs, and quality adjustments. Indexing government debt to a disputed statistic would have created political and technical risks. That issue was largely resolved by the Boskin Commission in 1996, which quantified CPI’s upward bias and helped solidify a revised and more credible methodology. By the mid-1990s, CPI-U had become stable and transparent enough to serve as the index for Treasury securities.

By 1997, incentives finally aligned. The Treasury could reduce the inflation risk premium embedded in nominal yields and borrow at known real rates, while institutional investors (especially pension funds and insurers) gained access to long-duration, government-backed real assets.

One sobering observation on the history of both I Bonds and TIPS is that the real returns were higher when they were first introduced than they are today. I Bonds had fixed rates above 3% when they were first introduced; it's a stark contrast to the 0% fixed rate when they were all the rage during the inflation of the COVID pandemic. Likewise, TIPS had real yields around 3%-4% when they were first introduced but had negative real yields around the same time I Bonds had that 0% fixed rate. As of May 2026, new I Bonds have a fixed rate of 0.9%, and TIPS have real yields of 1.25%-2.38% depending on the maturity date.

More information here:The Original Target Audiences for TIPS and I Bonds Differ

TIPS and I Bonds were created for different audiences and purposes. TIPS were first issued as marketable securities designed for institutional investors and bond portfolios, allowing the US Treasury to borrow at real interest rates while giving markets a way to price inflation expectations directly. I Bonds followed in 1998 as a retail savings instrument, intended to protect household savings from inflation without exposing investors to market volatility, reinvestment risk, or complex tax reporting.

Both use CPI-U as their inflation reference, but their structures reflect their distinct goals: TIPS are market instruments, while I Bonds are savings instruments aimed at individual investors.

The Shared Foundation: CPI-U

Both TIPS and I Bonds are indexed to CPI-U (Consumer Price Index for All Urban Consumers), published monthly by the Bureau of Labor Statistics. CPI-U measures price changes for a representative basket of consumer goods and services faced by urban households. Housing is measured using Owners’ Equivalent Rent (OER), and prices within narrow categories use geometric means to account for some level of product substitution (for example, if beef prices increased 20% and chicken prices increased 0%, instead of saying that entire category increased by the arithmetic mean of 10%, the geometric mean of 9.5% is used to account for some level of substitution).

For inflation-protected securities, the Treasury uses the non-seasonally adjusted CPI-U. Seasonal adjustment is helpful for statistical smoothing, but it is subject to annual readjustments, which would complicate its use for securities that might be sold before the applicable adjustment could be made.

The 3-Month Lag for TIPS

Although both TIPS and I Bonds are indexed to CPI-U, they apply that index differently over time. TIPS incorporate an explicit three-month lag when adjusting principal, using an index ratio that interpolates between already-published CPI-U values. This lag is a mechanical feature that allows TIPS to trade daily with precise pricing and settlement; it does not reduce long-term inflation protection, but it can introduce short-term timing differences during periods of rapidly changing inflation.

I Bonds do not use this lag structure. Instead, they apply published CPI-U data directly to calculate a backward-looking six-month inflation rate, which is then compounded internally. Both instruments are necessarily backward-looking, but only TIPS embeds a formal CPI lag.

CPI-U, like any inflation measure, cannot match any individual household’s experience perfectly, but it is a transparent, rule-based index suitable for contracts and securities. When TIPS and I Bonds behave differently, it is not because they use different inflation measures but because they are built differently.

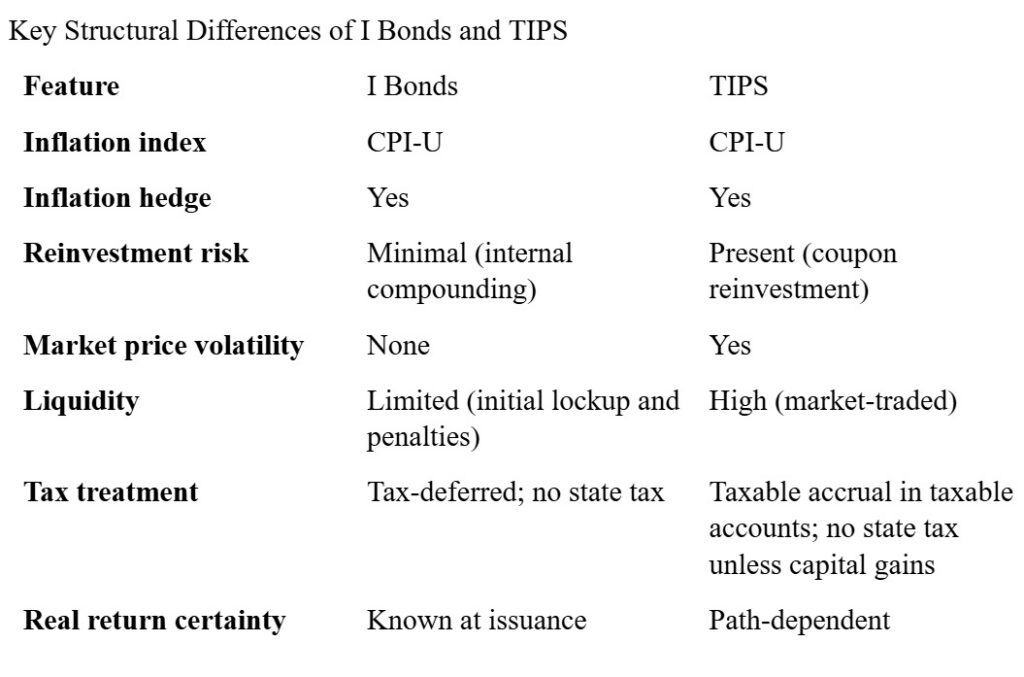

Reinvestment Risk

I Bonds largely eliminate reinvestment risk because both inflation compensation and any fixed real return are capitalized internally. There are no interim cash flows, so the investor does not depend on future interest rates to achieve the promised real return. At the time you purchase an I Bond, you know exactly what the (CPI-U) inflation-adjusted return will be: the fixed real rate of the I Bond.

TIPS, by contrast, distribute part of the inflation compensation through their cash coupons. To compound returns, those coupons must be reinvested at future real yields that cannot be locked in at purchase. Even if a TIPS is held to maturity, its realized real return depends on how those payments are reinvested. Even if they were reinvested in another TIPS, you cannot predict in advance what real rates will be available then.

More information here:Market-Pricing Risk

Market-pricing risk is another key difference between TIPS and I Bonds. I Bonds are not priced by the market; their value is set by the US Treasury. When an investor redeems an I Bond, the payout is known with certainty, and the bond’s value never falls below the original investment. TIPS, by contrast, are traded financial instruments whose prices fluctuate daily based on real interest rates and market conditions. Although TIPS guarantee repayment of inflation-adjusted principal at maturity, they offer no guaranteed price before then. This market-pricing risk can lead to meaningful interim volatility, even when long-term inflation protection remains intact.

Tax Friction

I Bonds benefit from tax deferral: interest compounds internally, and federal tax is owed only when the bond is redeemed. TIPS, by contrast, create annual taxable income in taxable accounts from both coupons and inflation-adjusted principal, even though that principal increase is not received in cash. Both TIPS and I Bonds are exempt from state and local taxes, with the exception that a TIPS bought on the secondary market and later sold could have a capital gain that could be subject to state/local taxes. This ongoing taxation introduces tax friction that can reduce after-tax returns unless TIPS are held in tax-advantaged accounts.

I Bond Purchase and Liquidity Rules

Series I Savings Bonds can only be purchased directly from the US Treasury and cannot be redeemed during the first 12 months after purchase. If they are redeemed before five years, the investor loses the most recent three months of interest as an early-redemption penalty. After five years, I Bonds can be redeemed at any time with no penalty, and interest continues to accrue for up to 30 years from issuance. By contrast, TIPS are marketable securities that can be bought or sold at any time in the secondary market, but their prices fluctuate with changes in real interest rates.

More information here:Possible Portfolio Roles

I Bonds are best viewed as inflation-protected safe assets: useful for emergency funds, near-term purchasing power, and investors who prioritize certainty and tax efficiency. TIPS are better suited for inflation-protected bond allocations, duration management, and portfolios requiring liquidity. Because I Bonds have a yearly investment limit (currently $10,000; in the past, this has been as high as $30,000 and as low as $5,000), an investor needs to accumulate them gradually if they want to have them make up a meaningful portion of their portfolio. There is no limit to the number of TIPS you can buy on the market.

The Bottom Line

TIPS and I Bonds share the same inflation index but deliver inflation protection in fundamentally different ways. I Bonds behave like capitalizing real bonds with minimal reinvestment risk, while TIPS behave like coupon-paying real bonds with reinvestment and market risk. These instruments are not interchangeable competitors but complementary tools, and understanding their structural differences allows inflation protection to be applied intentionally rather than chasing whichever looks more attractive in a given moment.

Do you have inflation-protected bonds in your portfolio? Do you like I Bonds or TIPS better? Why?