Those of you who have been following the blog for years know that I make changes to my portfolio quite infrequently. However, one change I have made was to add a risky fixed-income asset class called Peer-to-Peer Loans two years ago. I added it to provide diversification and to boost returns (especially given the very low fixed income returns available in our current low-interest-rate environment). I figure if you're going to chase yield, you might as well go big. That said, this is an asset class with serious downsides. You're loaning money to people based on a promise and a signature, no collateral. Your only recourse if they default is to ruin their credit score. You also are quite dependent on one firm (or a couple of firms) to not go out of business. If Lending Club or Prosper fails, it's going to be ugly. Also, this asset class is somewhat illiquid due to a secondary market with serious issues, although by using the Sacramento method you can at least get out of good loans relatively easily. Perhaps most importantly, investing in this asset class can be very time-consuming, although there are ways to reduce that hassle factor.

I haven't written about my investment in Peer-to-Peer Loans for about a year, but it's still going just as well as ever. One development that has really affected me is that Lending Club stopped allowing you to sell loans where payments were late or pending. That changed my strategy a bit. Up until that point, I hadn't had a default yet (since I sold loans off for 20-80% of their value while they were late but before they defaulted). So now I have a lot more late loans and a few defaults. That's okay, it doesn't seem to affect my returns much. Some of them go back to paying off their loans and some don't, but since I was selling the late ones at such a big discount, it's about the same result in the end. I did finally get my investment up to 5% of my portfolio, primarily in a Roth IRA at Lending Club.

Now, let's talk about how I've done.

My Experimental Lending Club Account

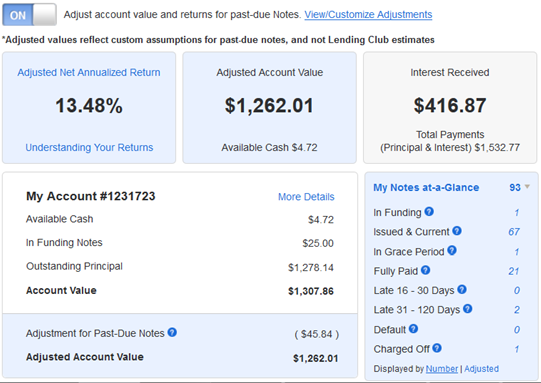

My oldest account is a $1000 Lending Club taxable account I opened in November 2011. I haven't added any money to it at all. My initial investments were on the conservative end of the scale, but after a year or so I began investing it just like my Lending Club Roth IRA- aggressively in the riskier loans that generally had higher returns. Here's what the account looks like:

You can see a few things from this account. First, since you can't invest less than $25, this account has always had some significant cash drag since Lending Club pays 0% on cash. Second, although there were originally just 40 notes, I have had a total of 93 (and I don't believe that counts the few that I sold while they were late). The average note size is obviously now less than $25 each. I have had one of these “charged off.” I bought it in March 2013, they made 11 payments, and then that was it. So I didn't lose the whole investment, but I did lose over 80% of my principal on it. The 2 late notes also made payments for about a year before they stopped paying. Meanwhile, 21 people have paid off their loans completely, many far ahead of time, for better or worse. You'll also notice that I have an “adjusted account value.” This is a relatively new development from Lending Club that lets me reduce the value of late loans. I have it set so grace period loans are discounted 20%, 15-30 day late loans are discounted 50%, loans > 31 days late are discounted 95%, and charged off loans are discounted 100%. It's a more accurate way to look at the account value in my opinion.

You can see a few things from this account. First, since you can't invest less than $25, this account has always had some significant cash drag since Lending Club pays 0% on cash. Second, although there were originally just 40 notes, I have had a total of 93 (and I don't believe that counts the few that I sold while they were late). The average note size is obviously now less than $25 each. I have had one of these “charged off.” I bought it in March 2013, they made 11 payments, and then that was it. So I didn't lose the whole investment, but I did lose over 80% of my principal on it. The 2 late notes also made payments for about a year before they stopped paying. Meanwhile, 21 people have paid off their loans completely, many far ahead of time, for better or worse. You'll also notice that I have an “adjusted account value.” This is a relatively new development from Lending Club that lets me reduce the value of late loans. I have it set so grace period loans are discounted 20%, 15-30 day late loans are discounted 50%, loans > 31 days late are discounted 95%, and charged off loans are discounted 100%. It's a more accurate way to look at the account value in my opinion.

My overall XIRRed return for this account is an annualized 10.4%. Not too bad, and worth the risk IMHO.

My Experimental Prosper Account

Shortly after opening the Lending Club account, I opened a $500 Taxable Account at Prosper. If you thought there was a lot of cash drag on a $1000 account, you should see a $500 account. I actually had negative returns on this account for quite a while (due to the drag and a few early defaults), but it's gotten better since. Here's what it looks like currently.

Prosper never let me sell late loans, so I never really sold any. At any rate, as you can see, I concentrate on the mid-range notes at Prosper, in the B, C, and D ranges (and especially like people with previous Prosper loans). I've gotten pretty lucky in the few risky (E and HR) loans I've bought. Although I started with 15 loans, I've had a total of 42. 25 loans are current, 3 are late, 9 have been paid in full, and 5 have defaulted. I received anywhere from $1.89 to $8.27 from these $25 notes prior to their default. My XIRRed returns have been:

Prosper never let me sell late loans, so I never really sold any. At any rate, as you can see, I concentrate on the mid-range notes at Prosper, in the B, C, and D ranges (and especially like people with previous Prosper loans). I've gotten pretty lucky in the few risky (E and HR) loans I've bought. Although I started with 15 loans, I've had a total of 42. 25 loans are current, 3 are late, 9 have been paid in full, and 5 have defaulted. I received anywhere from $1.89 to $8.27 from these $25 notes prior to their default. My XIRRed returns have been:

- 2012 (11 months): 4.48%

- 2013: 10.64%

- 2014 (5 months): 3.49%

- Overall: 8.05%

The Main Tax-Protected Account

Since P2P Loans are very tax-inefficient, it's best to invest in them in a tax-protected account. I've gradually rolled Roth IRA money over to Lending Club and invested it in P2P loans, beginning in September 2012 and most recently in April 2014. I would roll over a few thousand, give it time to get invested, and then roll over a few thousand more. It took me essentially a year and a half to get 5% of my portfolio invested. I could have done it faster, but I couldn't have been as picky with which loans I invested in. Here is what this account looks like:

These were initially $25 loans, but I went to $50 loans when loans became more scarce a year ago so it didn't take quite so long to get my money invested. This account has always been invested aggressively. Lending Club claims I'm making 20% on this account. That's not true, it's actually 13.00%. It's interesting that despite this account only being a year and a half old, and that I generally invest in 5 year loans, 10% of the loans I've ever made have been paid in full. Apparently, there are a few intelligent people out there that realize carrying a 20% loan for 5 years is pretty stupid. For the rest of them, I'll continue to take their money. It's hard to tell exactly how many of the loans that I have bought have defaulted, since for the first year I sold all the late ones. But in the last 6 months since they've made it more difficult to sell loans that are about to default (and since I've lost interest in spending time trying to sell these), I've got about a dozen that look like they're going to default.

These were initially $25 loans, but I went to $50 loans when loans became more scarce a year ago so it didn't take quite so long to get my money invested. This account has always been invested aggressively. Lending Club claims I'm making 20% on this account. That's not true, it's actually 13.00%. It's interesting that despite this account only being a year and a half old, and that I generally invest in 5 year loans, 10% of the loans I've ever made have been paid in full. Apparently, there are a few intelligent people out there that realize carrying a 20% loan for 5 years is pretty stupid. For the rest of them, I'll continue to take their money. It's hard to tell exactly how many of the loans that I have bought have defaulted, since for the first year I sold all the late ones. But in the last 6 months since they've made it more difficult to sell loans that are about to default (and since I've lost interest in spending time trying to sell these), I've got about a dozen that look like they're going to default.

Overall Returns

So to summarize my returns:

- Annualized Prosper Return (on a tiny account): 8.05%

- Annualized Lending Club Return (on a tiny account): 10.45%

- Annualized Lending Club Return (on a larger account that has always been invested aggressively:13.00%

- Annualized Lending Club Return (on both accounts): 12.81%

- Overall 2011 Return (6 weeks): 3.22%

- Overall 2012 Return: 12.65%

- Overall 2013 Return: 13.16%

- Overall 2014 Return (5 months): 4.76%

- Annualized Overall P2PL Return: 12.60%

I feel pretty good about these, given that the average returns for Prosper and Lending Club tend to be in the 6-7% range. My active management appears to be adding some value.

Please be sure to limit your investment in this risky asset class. It might be fixed income, but these aren't treasuries and there are some very unique risks in play here. In many ways, the risk is greater than buying equity index funds. I suggest starting with a tiny experimental account before rolling over any serious IRA money to invest. Also look into a way to automate your investing. Without that, it can be a major time hassle. But as you can see, potentially good returns are available and the faster your money grows, the sooner you reach your goals.

What do you think? Do you invest in P2P Loans? Why or why not? Have you been pleased or disappointed with your returns?