I get asked lots of questions about specific investments. Mostly, the question is asking me to look into my crystal ball and tell them what will provide the best return over their investment period. Aside from the fact that I'm not licensed to recommend specific investments (or paid to do so; even for our real estate sponsors, we only introduce, not recommend), the main issue here is that my crystal ball is usually about as cloudy as that of the person asking the question.

However, I get this particular version of the question often enough that it seemed worth a blog post.

“I practice in an academic setting and, like many of us at academic institutions, I have access to TIAA’s Real Estate Account. I have not been able to find any high-quality reviews of this account to help decide if it is worth investing in, and I was wondering if your team would be up for writing an article about it to provide us with your insight. Some questions that come to mind are whether it is a good investment compared to other direct real estate investing opportunities, if TIAA is considered competitive as an investing institution in the real estate world, and if the benefits of being able to invest in it in a 403(b) outweigh the tax benefits real estate investments offer investors in taxable accounts.”

The TIAA Real Estate Fund (QREARX)

I have known about the TIAA Real Estate Account (fund) for decades, although I admit I don't follow it particularly closely, as it has never been accessible to me as an investment. TIAA-CREF provides a lot of 403(b)s across the country to academics, teachers, and others, and it is generally considered one of the better retirement account providers—or at least it was a decade or two ago before investing became pretty much free with the advent of sub-10 basis point index funds from providers like Vanguard, Fidelity, Blackrock, and more.

The draw of the TIAA fund is that it provides DIRECT investments into real estate, rather than just buying shares of publicly traded REITs. That means there is one less layer between you and the actual investment. Presumably, that would reduce costs and reduce volatility and correlation with the overall stock market, like other direct real estate investments. Of course, one can very reasonably argue that the volatility of private real estate isn't reduced; it's just hidden due to assets not being marked to market regularly. Presumably, QREARX does have to mark to market more regularly than most direct investments, given its high liquidity.

Past Performance

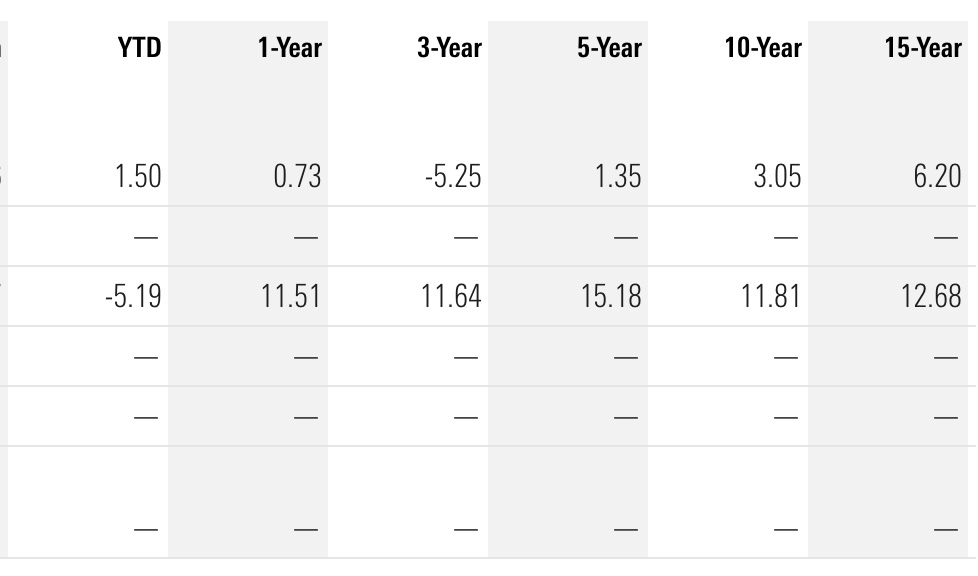

When I first learned about this fund two decades ago, I heard people speak positively about it and assumed it was pretty good, but then I forgot about it because I never had a 403(b) with access to it. Imagine my surprise when I looked it up and learned that maybe it wasn't all that awesome. Take a look at this chart from Morningstar accessed in May 2025.

The top line is fund performance, and the third line is the performance of its category. See what I mean? Ten-year returns of 3% and even 15-year returns of 6% are pretty hard to get excited about. Real estate hasn't done as well as US large cap tech stocks over the last 15 years, but it hasn't been a bad asset class in which to invest. Let's compare it to my preferred publicly traded real estate investment, the Vanguard Real Estate Index fund (VNQ). This fund/ETF owns all the equity Real Estate Investment Trusts (REITs) traded on US markets.

That 1.5% lower per year (15-year returns of 7.73% vs. 6.20%) isn't as bad as I expected, but it's still a substantial underperformance. It looks even worse over the last five years with an underperformance of 6.5% a year. It really makes you wonder what has been happening at QREARX in the last five years. Like private real estate investments, QREARX isn't marked to market as quickly as VNQ. I'm not surprised to see the delay in the poor returns, just as we saw with MANY private real estate investments that had rough years in 2023 and 2024, especially when compared to the overall stock market.

QREARX

VNQ

What Is the TIAA Real Estate Account Actually Doing?

If you read its documents, you can learn a lot about how an account/fund/annuity/whatever actually operates. Let me quote from it:

“The Real Estate Account is designed as an option for retirement and tax-deferred savings plans for employees of non-profit and governmental institutions.

Investment Objective: The Real Estate Account seeks to generate favorable total returns primarily through the rental income and appreciation of a diversified portfolio of directly held, private real estate investments and real estate-related investments, while offering investors guaranteed, daily liquidity.

Investment Strategy: Real Estate-Related Investments. The Account intends to have between 75% and 85% of its net assets invested directly in real estate or real estate-related investments with the goal of producing favorable long-term returns primarily through rental income and appreciation. These investments may consist of:

- Direct ownership interests in domestic and foreign real estate;

- Direct ownership of real estate through interests in joint ventures; or

- Indirect interests in real estate through real estate-related securities, such as:

- Private real estate limited partnerships and limited liability companies (collectively, “real estate funds”);

- Real estate operating businesses;

- Investments in equity or debt securities of domestic and foreign companies whose operations involve real estate (i.e., that primarily own, develop, or manage real estate) which may not be real estate investment trusts (“REITs”);

- Domestic or foreign loans, including conventional commercial mortgage loans, participating mortgage loans, secured domestic and foreign (including UK) mezzanine loans, subordinated loans, and collateralized mortgage obligations, including commercial mortgage-backed securities (“CMBS”), collateralized mortgage obligations (“CMOs”), and other similar investments; and

- Public and/or privately placed, domestic and foreign, registered and unregistered equity investments in REITs, which investments may consist of registered or unregistered common or preferred stock interests.

The Account’s principal strategy is to purchase direct ownership interests in income-producing real estate, including the four primary sectors of office, industrial, retail, and multi-family, and alternative real estate sectors (defined as real estate outside of the four primary sectors noted above). In addition, the Account is authorized to hold up to 25% of its net assets in liquid real estate-related securities, including publicly traded REITs and CMBS. Management intends that the Account will not hold more than 10% of net assets in such securities on a long-term basis. As of December 31, 2024, the Account did not hold any publicly traded REITs or CMBS.”

The document also notes that 15%-25% of the fund's money can be invested in liquid securities like Treasury bonds and money market funds.

More information here:

How to Start Investing in Real Estate

The Tax-Advantaged Income from Our Passive Real Estate Investments

What Are the Pros of Investing in QREARX?

I'm sure plenty of people love investing in QREARX. It has $22.6 billion in it. Let's consider what they probably like.

#1 Easily Invested in with a Retirement Account

The first pro of QREARX is that it provides you with a way to invest in real estate in your TIAA-CREF 403(b). You'll enjoy some tax efficiency from having your real estate investment in a retirement account. And if a huge chunk of your money is in this account, it may be the only way to have a substantial real estate investment in your portfolio.

#2 Less Volatility (Less Money in Publicly Traded REITs)

The second pro of QREARX is that it allows you to invest more directly in real estate than via a REIT mutual fund, such as VNQ. That likely results in less volatility. Of course, that works both ways. In 2021, VNQ was up 41%, but QREARX was only up 18%. On the downside, VNQ dropped 26% in 2022, and QREARX only dropped 17% across 2023-2024. All else equal, lower volatility is good.

#3 Liquidity

QREARX provides daily liquidity, like a typical mutual fund. That's very different from most direct real estate investments, which are generally private and offer much less liquidity. However, it does limit you to transacting once a quarter (presumably to prevent market timing) on the day of your choice.

#4 Stability

This account has only been around since 1995, but frankly, that's an eternity in the private real estate space. Few syndicators and private fund managers have been in business anywhere near that long (blog sponsor MLG is a notable exception). And TIAA itself has been around for more than a century (1918). Like investing in VNQ, you don't have to spend a lot of time worrying about being the victim of a scam here or TIAA going bankrupt. That's often not the case in the private real estate world.

#5 Easy Taxes

This investment is in your 403(b), so there is zero tax preparation required for it. That's definitely NOT the case for a portfolio of syndications or funds sending you multi-state K-1s or having to file multiple Schedule Es each year for your direct real estate investments.

#6 Very Passive

VNQ is just as passive as QREARX, and many private funds are similarly passive, at least after the initial due diligence. But lots of real estate takes a whole lot more work than that.

What Are the Cons of Investing in QREARX?

Like any investment, there are pros AND cons. QREARX is no different. But the cons depend on your comparison. You have to invest in SOMETHING. Although all real estate is optional, it seemed most reasonable to compare it to the other real estate investments typically used by white coat investors rather than stocks, bonds, or some other asset class. These include public REITs via something like VNQ, passive private syndications and funds similar to those on our real estate sponsor list, and truly direct ownership of income-producing rental property (aka landlording) like we teach in our No Hype Real Estate Investment online course.

#1 More Expensive Than VNQ

Investing in VNQ, like most Vanguard index funds, is awfully close to free. The expense ratio is 0.13%. That's not the 0-5 basis points you see on a total stock market fund these days, but it's still a whole lot closer to free than most funds charge. On the other hand, QREARX charges more or less the classic “1% a year.” In fact, it's slightly more at 1.015% a year. Those fees/expenses have to come from your returns. There is no other place to take them from.

Fee comparison with private passive investments is a lot more challenging. At first glance, they seem a lot higher—often something like 1% plus 20% of returns above 8% or so. But you have to keep in mind that some of those fees are often going to the expenses of running the investment itself. Those expenses aren't included in the ER of VNQ. It's not entirely clear how operating expenses show up with QREARX. Some private investments (like the DLP funds) don't charge you any fees until you've received your preferred return. QREARX isn't offering anything like that.

#2 Unexciting Returns

I'm not sure how else to describe the last decade or two of returns for the TIAA Real Estate Account. They're obviously lower than those provided by the even more liquid and significantly cheaper VNQ. They also seem to be quite a bit lower than the returns offered by most passive private real estate investments. Let's compare a somewhat similar investment, the DLP Housing Fund. This fund isn't as liquid, although it does offer more liquidity (annual redemptions) than most private real estate investments. It is, like QREARX, evergreen—also unlike most real estate investments. How has it been doing the last few years? Let's take a look.

Unfortunately, Morningstar doesn't make a nice little graph every day for private real estate investments, but I carefully track my own returns in all of these investments. I invested $250,000 in this fund in June 2021 and have an annualized return from then until the end of April 2025 of 13% a year. By year, the returns look like this:

- 2021 (Jun-Dec): 6.69%

- 2022: 18.93%

- 2023: 12.57%

- 2024: 9.97%

- 2025 (Jan-Apr): 4.68%

Needless to say, 13% is way better than whatever QREARX has done over that time period—perhaps by as much as 11%-12% a year. They're both actively managed real estate funds and past performance doesn't necessarily indicate future performance, but you do have to ask yourself how much you trust the QREARX manager to do better after an underperformance like that.

Even if I had just gone with VNQ, I'd be significantly ahead of QREARX.

I could have taken less risk, too, and done better. Real estate debt funds have performed just fine over the last five years. We own three of them (including the DLP Lending Fund), and our returns for that asset class are a very stable 9.56% per year since we started investing in it in 2017.

Now, not every private real estate turned in better performance than QREARX, but most of mine did. While it's not necessarily an indicator of future performance, low returns may be my biggest con about the TIAA Real Estate Account.

#3 Unavailability

QREARX may be available to you. But it's not available to me or most white coat investors—at least not without changing jobs or at least opening an IRA with TIAA-CREF. You can probably only put as much money in it as you have in your TIAA 403(b). Unlike a private equity real estate investment, you can't put it in a taxable account and enjoy passive income sheltered by depreciation. And if you use your 403(b) space for real estate, that means you can't put something else (bonds?) in there.

More information here:

How the IRS Treats You as a Real Estate Investor

The 60+ Worst Mistakes You Can Make in Real Estate Investing

The Bottom Line

While I find the concept of a liquid direct real estate investment available to non-accredited investors in their employer-provided retirement accounts very interesting, it's hard for me to get over the additional expenses and lower returns seen with QREARX. And if you're really interested in putting in some time and effort into real estate investing, you're probably not going to end up in this fund.

What do you think? Do you invest in the TIAA Real Estate Account? Why or why not? What do you like/dislike about it?