One of the most significant downsides of private real estate deals (and other “alternative” investments) such as private funds and syndications is their illiquidity. While one of the goals in investing in these types of investments is to get paid for taking on that illiquidity, it makes it tough when things aren't going well. In fact, a large percentage of these deals, even those with a solid return afterward, will have a hiccup or two along the way that you will have to ride out. Let me give you a few examples I have encountered with my own personal investments.

Lending Club and Prosper

This one isn't real estate, but I thought it was worth including because it is an illiquid investment, the main subject of this post. I started investing in peer to peer loans in 2012. While yields were insanely high (15-30%), defaults were also substantial so I generally had solid 8-13% returns. I later decided I didn't like the platform risk nor the unsecured nature of the loans (especially when I could get loans with similar returns with real estate collateral in first lien position). So I decided to get out.

Well, the problem was I had a portfolio of 3-5 year loans (technically notes). Lending Club had a mechanism to sell notes on a secondary market, but it turned out to be a fairly thinly traded market. It took me 2 1/2 years to liquidate, despite taking small losses on many of the notes. About the same time, Prosper decided they weren't going to let you sell loans at all. I've still got $22 invested there and will for yet another 15 months. My overall returns were fine, but the opportunity cost and hassle of gradually liquidating and reinvesting an investment is annoying to deal with.

AlphaFlow Decides It Doesn't Like Individual Investors

Something similar happened recently with a company called AlphaFlow. One of the big hassles of investing in real estate debt (usually loaning money to house flippers) via the crowdfunding sites is the need to vet the deals, manage all the cash flow, and diversify the investment. Along comes Alpha Flow, technically an RIA charging 1%, that takes a lump sum from you and spreads it across dozens of loans, reinvesting the earnings as you go. I invested $20K as part of my real estate debt allocation and have been enjoying 7.5% returns after fees.

Well, AlphaFlow has decided it wasn't actually profitable to serve individual investors like me so now they're focusing purely on institutional investors. Basically, they're not reinvesting any of the cash coming out of the notes as they pay their yields and mature. Unfortunately, I've got notes as long as 11 months still in there, so I'll be getting cash in drips and drabs over the next 11 months to reinvest elsewhere. Not the end of the world, but definitely not my favorite way to end an investment. At least it won't take 2 1/2 years this time.

Broadmark Decides to Go Public

Another investment I really liked was a private real estate debt fund run by Broadmark, which lends money to developers in Utah and Colorado. When the 199A deduction came out, they changed their structure from a fund to a REIT. That's probably a good thing for those of us who were investing in a taxable account as 20% of the income was no longer taxable due to the 199A deduction. However, they then decided they wanted to go public. As I write this it is unclear if the proxy vote will clear the path for that or not (I suspect it will) and it is certainly unclear if the market will judge the company to ultimately be worth more or less than its Initial Public Offer (IPO) price.

Certainly, the history of IPOs is not favorable, although it's not entirely clear if the price assigned to me as a fundholder is a good price or not for the shares of the new public company. I suppose the market will let me know within a few months of the IPO. But either way, what I will be left with is an individual stock, something I generally avoid investing in due to uncompensated risk. If I'm going to own a publicly-traded mortgage/debt REIT, I probably ought to buy the iShares index ETF REM. Further updates to come on what we do here and how it turns out, but this is a risk of investing in a private company—it may go public with positive or negative effects on your investment.

[AUTHOR'S NOTE: Update prior to publication: The vote passed. The company did go public and it is up a little bit since then. Interestingly, because I voted against the merger I was given the right (due to WA state law) to sell the stock at the original price until December 20th, essentially a free put. Now I've got to decide whether to sell now for a short-term gain or wait a year. Given my abundance of capital losses from tax loss harvesting, I think I'm inclined to sell sooner rather than later and diversify.]

My Upright Loan (Formerly Fund That Flip)

Before I gradually transitioned from individual deals to funds, I had a few small loans I made on the crowdfunded sites like RealtyShares, PeerStreet, and Upright. To be fair, unlike some investors, I've gotten back every dollar I've invested in those as well as every penny of interest I was owed. Usually on time, sometimes early, and occasionally late.

My last remaining investment, however, was a 1 year, 10%, $5K loan made via Fund that Flip. I am currently 26 months into that 12-month loan and the project is still only 75% complete. To be fair, I am still getting paid that 10% interest (several payments were a little late and I got paid a fee to extend the loan), but if someone really needed their money back in 12 months, the illiquidity of this investment could be a big problem.

Origin Fund III Takes Its Time Calling Capital

I committed $100K to Origin Fund 3. They take their time calling the capital, only investing when they have a good opportunity. I appreciate that (so I can remain fully invested elsewhere rather than having cash sitting around), but many investors may have been surprised to see just how long it took to become fully invested. The fund's first investment was in July 2016. I started investing in October 2017 and here we are in December 2019 and the last of my capital has just been called this week. The investment seems to be doing just fine, but my point in including them here is to discuss the illiquidity with these investments. You make a commitment up front and then you're stuck with it for years—both contributing capital and getting your capital back.

My Indianapolis Apartment Building

I was going over my investment spreadsheet lately and checked on my Indianapolis Apartment Building ($10K purchased through crowdfunding site RealtyMogul) and noticed that I didn't get a payment in August like I usually do (they've been coming twice a year). And February's payment wasn't anything to write home about either. So I decided I better pay a little more attention to their recent notices and see what's going on. As a reminder, this is a 5-7 year equity, value-add investment in an apartment complex. This month I'm 5 years into it. Well, here's the latest updates. First from the Spring:

It looks like even the pros hire bad property managers sometimes. I've never been a Class B Apartment manager, but apparently 54% retention is pretty typical. Obviously 88% occupancy is a little on the low side. But with income per unit increasing and expenses decreasing, things seem pretty positive. Then I get this in the Fall.

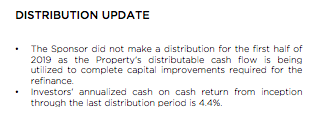

Okay, that sounds good, right? Occupancy up, collections up, rent up, NOI up. But no distribution. What happened?

Ugh. The cash got eaten up again. This property has been a chronic underperformer, at least compared to the proforma. Take a look at the most recent charts (I actually love the format of RealtyMogul's charts, even if I don't like what they're telling me):

My XIRR verifies their cash on cash return of 4.4% annualized. Not quite the 7.3% I expected. Now it's hard to make any final judgments before the round trip, but it seems unlikely that this one will hit the proforma IRR of 15.5%, although I doubt I'll lose money. Stay tuned!

I share this experience to point out that once the decision to invest is made, all you can do is hold on for the ride. When things are going well, that means you're not getting 3 am toilet calls and all you have to do is collect your mailbox money twice a year. When things aren't going well, there's no mailbox money and you wonder how much of your capital you will get back. As was carefully explained in the subscription document:

They really do mean it when they say that.

My Houston Apartment Building

I have a $20K preferred equity position in an apartment building in Houston through Equity Multiple, one of the sponsors at the recent PIMDCON. I bought in almost two years ago and everything was hunky-dory. The plan was to provide investors a 10% preferred return and then another 5% return upon sale in 3 years.

Okay, did you get all that? It was 86% occupied, it was going to be thoroughly renovated and rents raised, and then sold or refinanced in 3 years, paying me off and providing a 10-15% return. So what happened?

Well, all through 2018 I got my monthly payments like clockwork. Then all of a sudden they stopped at the end of 2018. If you read the updates, the occupancy dropped to 75% early in 2018 as renovation proceeded. Then later that year, I get this update:

In case it isn't clear, notices like that are bad when it comes to real estate investing. Now you would think the place was hit by a hurricane, but Hurricane Harvey occurred in August 2017, 4 months before I bought in. But either way, the renovation is not going well. The sponsor may have intended to “advance funds”, but it actually hasn't “advanced funds” in 2019 at all.

This is what I got early in 2019:

While I guess it is good to see EquityMultiple in there mixing it up trying to get me a better return, the fact that they had to is a pretty bad sign. Occupancy dropped from 74% to 59% between Q1 and Q2 (weird that no one wants to live in a construction zone), when this update came out:

Yup. Plenty of cash. We're covering expenses and paying the mortgage. But guess who gets paid after the mortgage? That's right. Me. And there's no cash flow left for me. Payments are now 11 months behind. I'm not nearly as optimistic as Equity Multiple about getting my 10% preferred return out of this, much less that 15%. In fact, I'm starting to worry a bit about my capital too. So I'm using this to demonstrate what a deal going bad looks like. Again, there is absolutely nothing I can do about it but hold on for the ride. No liquidity whatsoever. We'll see what happens in a year.

My Fort Worth Apartment Building

This one was purchased directly via syndicator 37th Parallel. A substantial investment for me at $100K, I'm about 20 months into it. My first three quarterly distributions were $1,243-$1,299, suggesting about a 5% cash on cash return. But the last two were only $671-676. What happened? Well, these are their explanations:

High supply and high property taxes.

High supply and a new manager.

My point of sharing this experience isn't that this is necessarily a bad investment. I certainly don't need this income and am in this one for the long haul hoping for a solid long term return. My point is that real estate income varies. If you were counting on income like this to live off of, you would need to be able to vary your spending accordingly. Once more, it really doesn't matter what the income is or what the explanations for it are. I'm stuck for a decade—good, bad, or ugly. It's very passive at this point, for better or for worse.

A Few Words of Advice

Most who read this will see a cautionary tale. Certainly, I am big on people understanding the risk they are taking with their investments and ensuring those are risks they are capable of handling. And it is only natural to expect the subscription documents to paint a fairly rosy picture of future performance.

But despite the hiccups seen above (even without any sort of general economic or real estate downturn), I still like investing in real estate and plan to do so going forward. Of the 21 private real estate investments I have invested in, 11 have gone round trip (1 equity, 1 preferred equity, and 9 debt). I have received every penny of my principal back AND all expected returns from those 11 investments. The equity investments send me sometimes surprisingly high amounts of depreciation on the K-1s to shelter that income. But once you invest, these investments are totally passive, for better or for worse, and there is no liquidity.

There are other options. In 2019 and really over the last few years, those options did great. On the day I write this in early November, the Vanguard REIT ETF (equity REITs) is up 28.66% year to date (13.08% over the last decade) and the iShares Mortgage REIT Capped ETF (debt REITs) is up 15.44% year to date (8.61% over the last decade), all with daily liquidity. But they are terribly tax-inefficient and certainly subject to the whims of the overall stock market.

The choice is yours really, and truthfully most doctors with a halfway decent savings rate don't need to invest in real estate at all to be successful. But if you choose to go the private route, be prepared to buy and hold, because you won't have any other choice.

What do you think? Does the illiquidity of private real estate deals bother you? Do you think it is worth it?