We recently checked out a fancy retirement software product called Boldin, formerly known as NewRetirement. We felt it met our high standards of quality, and we wanted to bring it to the WCI community as a recommended product.

Naturally, as a for-profit business, we also negotiated an affiliate agreement with them, so if you sign up via the links for their paid (not free) version, we also get paid. It's not a very expensive product, though, so the affiliate payments really aren't all that high. In fact, we put off Boldin for a year or two because it just didn't make business sense for us to promote a product like this at such a low price point. However, it's a really good product, and even if we don't make any money from the partnership, many WCIers are still going to benefit from being introduced to it. All right, I think that's enough conflict of interest disclosure. Let's get into the review.

Boldin: The Best Retirement Calculator Out There

There have been retirement calculators out there for many years. Even Empower, formerly known as Personal Capital, does some of this. Most hardcore DIYers have heard of FIRECalc. MaxiFi (formerly ESPlanner) is also a worthy competitor with some advantages and disadvantages when compared to Boldin. However, I think Boldin is the first one you should check out, and it's certainly the only one you need. The truth is that they're all very cheap, and all of them have some sort of free version to get a taste for them. You could just get them all.

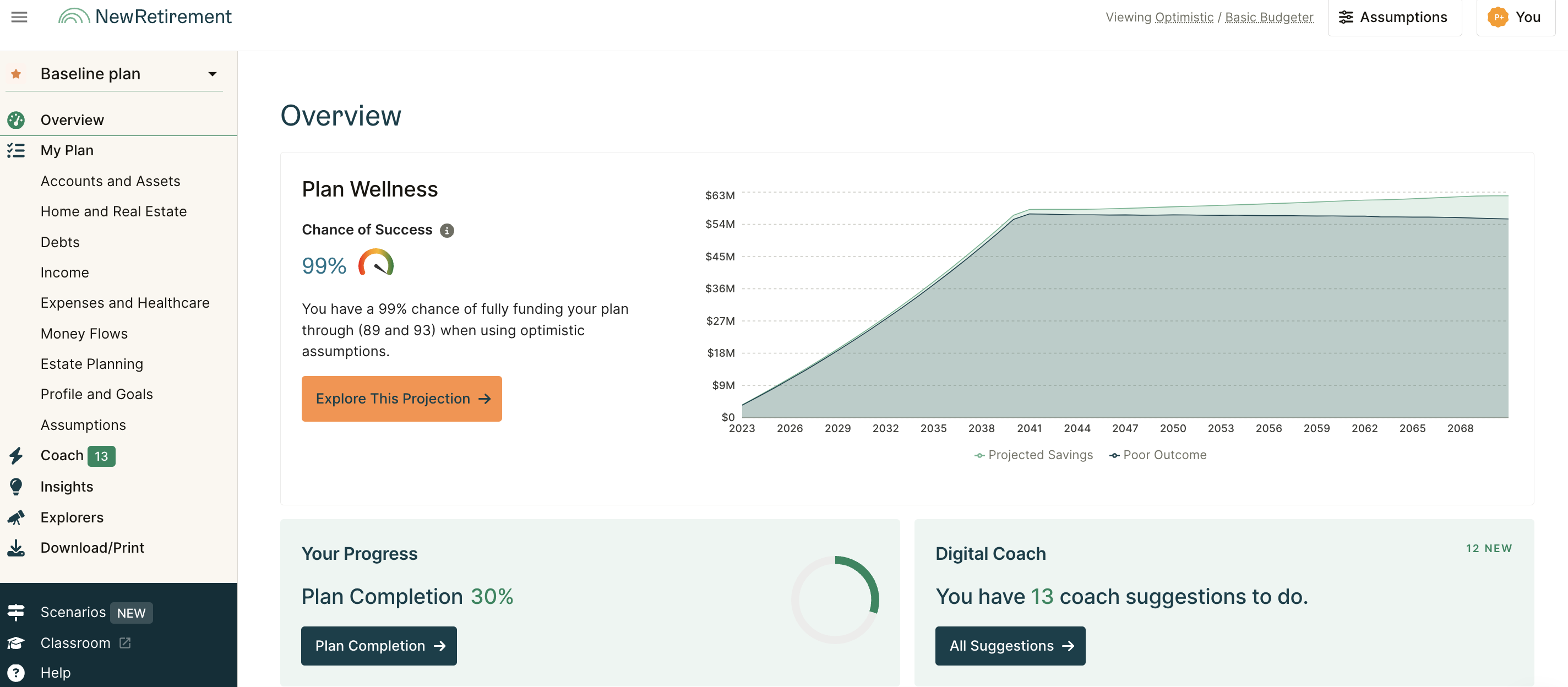

Boldin provides a robust set of information—even just the free version—and it's incredibly easy to get started. In fact, once you sign up (10 seconds), the first thing that's offered is a super fast, friendly way to get started while providing a minimum of information. Within five minutes, I found out that my hypothetical doctor (someone my age with a $340,000 income, a $2 million nest egg, no debt, and spending a little over $15,000 a month) had a 99% chance of retirement success.

Once you get through the preliminary stuff, you end up on this main screen. This is where the software starts to get really powerful. Of course, you are regularly reminded about what you get if you sign up for the paid version ($12 a month with a free 14-day trial) that you're not getting right now.

Financial Planning Software

I felt like Boldin was so much more than just a calculator, though. It's actually pretty robust financial planning software. The quality of the financial plan it generated was actually far higher than I have seen come from many professional financial advisory firms. When combined with a financial literacy course, such as our Fire Your Financial Advisor course, this could be a powerful tool for someone looking to bridge the gap between hardcore DIY financial planning and paying thousands to a financial advisor.

Features

The calculator starts with all of the features you would expect. While easy to use, it's not a simple calculator. There is a lot that goes into these calculations, which means you have to input a lot of data. The more you put in, the more accurate the projections and figures. Garbage in, garbage out. Some of the data you can put in include:

- Retirement age for you and your partner

- Social Security age for you and your partner (and there's a cool tool to help you optimize this)

- Housing expenses

- Healthcare expenses

- All other expenses

- Current income

- Current assets

- Asset locations (i.e., types of accounts)

- Debts

- Legacy goals

More powerfully, it allows you to change all kinds of assumptions but makes it easy by putting in something so you can get started. So, you start with something reasonable, and then you can change it to see how much your retirement success and income depend on that particular variable. Some of these changeable assumptions include:

- Inflation rate

- Social Security COLA

- Housing appreciation rate

- Medical inflation rate

- Expenses

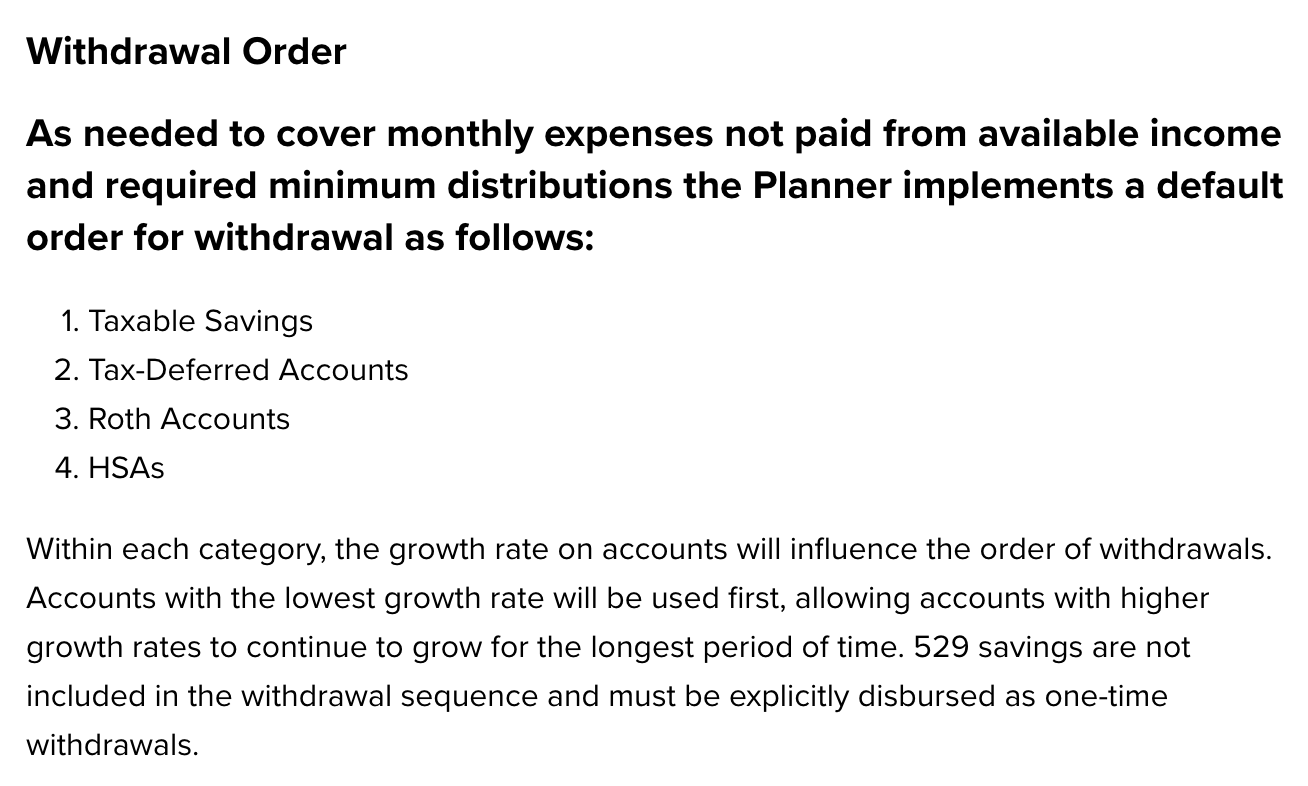

- Withdrawal strategy (three options)

- Tax rates

Perhaps most importantly, almost everything allows you to use “optimistic,” “average,” and “pessimistic” assumptions simply by toggling between them.

The software is not all powerful. While I was impressed it can adjust for the fact that HSAs get taxed differently in California and New Jersey, the software also has some “fixed” assumptions you may or may not agree with. For example,

If you were planning to blend tax-deferred and tax-free withdrawals in retirement, this software can't handle that. That's an awfully nuanced thing, though. If you're thinking about things like that, you probably don't need software like this to help you set up your financial plan.

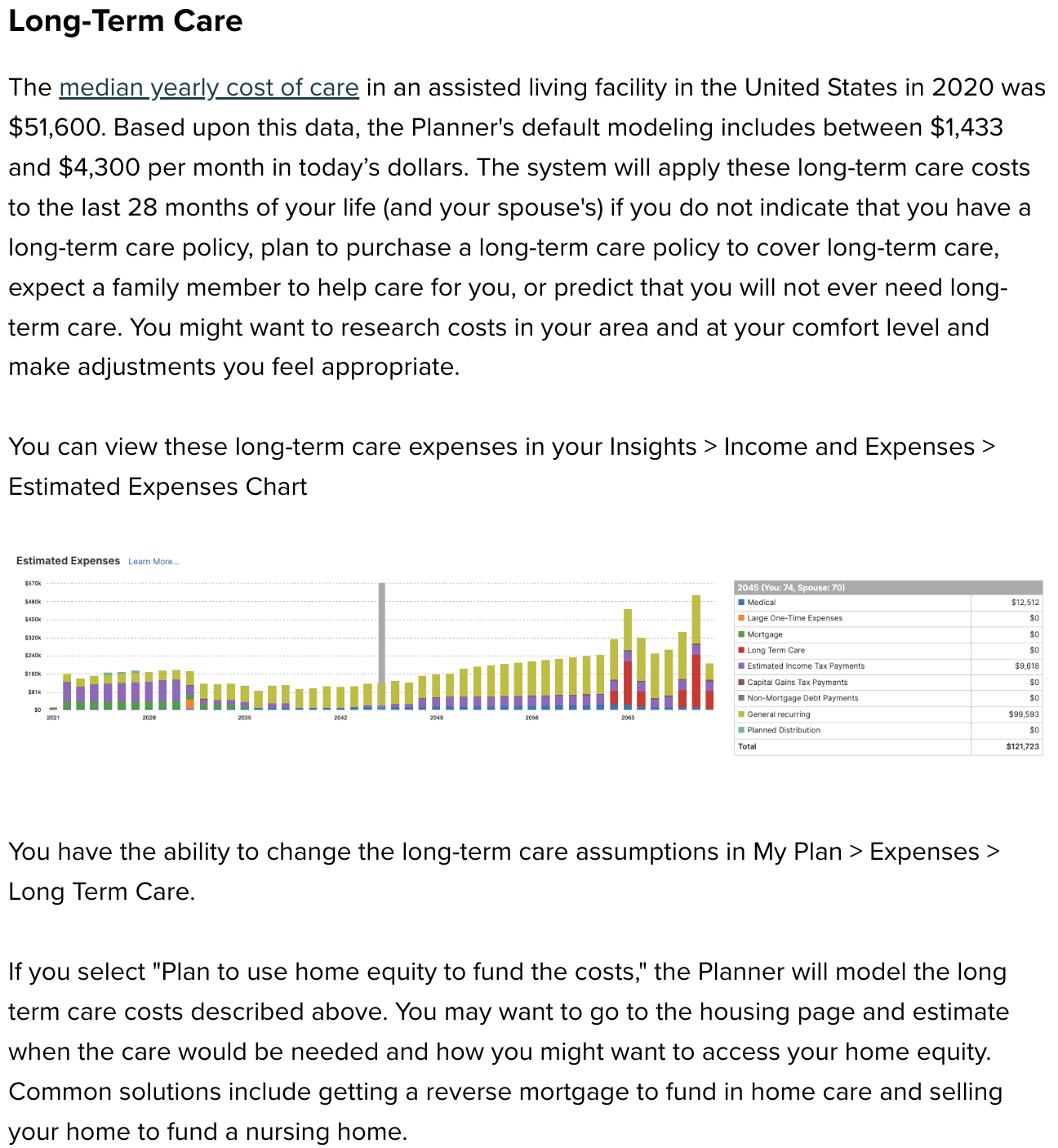

Boldin has also thought about a lot of stuff that you probably haven't. Consider this built-in assumption from a few years ago::

As of Genworth’s 2024 data, Boldin points out that the newest default model includes a phase of $1,966 per month for 12 months, followed by $5,900 per month for 16 months, totaling $117,992 in today’s dollars.

You can pay thousands of dollars for a professional financial plan, and they may not get into anywhere near that level of detail with their assumptions. You can change this one, too. The power of the software is really in the number of assumptions, the flexibility of the assumptions, and the fact that they start with something reasonable there to help you get going.

It also allows you to build a “baseline plan” but then create a number of “scenarios,” essentially variations of the plan to see how they might play out. That might include retiring now instead of later, changing an asset allocation, getting divorced, or just being much more pessimistic about everything.

Digital Coach and Live Help

There are two other features worth mentioning. The first is the digital coach; it's like a little built-in financial planner. This kicks in somewhat even in the free version.

After my five-minute financial plan, the digital coach told me they had 12 suggestions for me. These were the 3/12 I could see with the free version. It very politely informed me that if I really want to do well investing, I should be a passive investor.

There is also an option to get on the phone with a CFP®. While you don't get THAT for $12 a month, it's only $2,800 a year, which is awfully inexpensive financial planning rivaling the very most cost-effective of our recommended advisors. Naturally, that makes me worry a little about the quality of the advice since I haven't vetted the CFPs picking up the phone for Boldin.

There are actually three versions of the product:

- Free version: Basic plan, “what if” scenarios, Monte Carlo analysis, Social Security Explorer, Roth Conversion Explorer

- PlannerPlus ($144 per year): The full planner software for a robust plan, the ability to compare scenarios, access to live Q&A sessions

- Boldin Advisors ($2,800 per year): Get professional help

Here's what else you can get with PlannerPlus:

- Custom retirement withdrawal order

- Enhanced Roth conversion modeling

- Better rate customization for inflation, appreciation, and returns

- Inherited IRA modeling (pre- and post-SECURE Act)

- Financial wellness metrics

- Today vs. future dollars toggle

- Retirement withdrawals report

- Boldin classroom + weekday live classes

- AI-powered help chat

Everyone reading this blog post should go get the free one today, but if you actually need or want financial planning software, the one to get is the $12 per month ($144 per year) PlannerPlus version, and that's not just because that's how WCI gets paid. It's because your time is valuable. If you're actually going to spend the time to use this software to do your financial planning, $144 is nothing. What's an hour of your time worth? Exactly. Get the full version.

Weaknesses

Naturally, no robo advisor or software can really, truly replace an expert. For instance, this software is not doctor specific at all. Its assumptions do not model the typical financial pathway of a doctor. For instance, if you filled it all out as a resident using your resident income, assets, and expenses, the outputs would be practically useless for you because your life will soon dramatically change.

The student loan section is also completely inadequate for someone with $400,000 in student loans who's considering PSLF, and I'll bet dollars to donuts even the $2,800 a year guy on the phone isn't an expert on managing physician student loans.

It also uses as its main output the “chance of success” rather than telling you how much you can spend (“income smoothing”) like at least one of its competitors. That's more of a philosophy thing, though.

The Bottom Line

Like almost anything else with financial planning, you'll get out of this tool just as much as you put into it. If you want a five-minute confirmation that you're doing fine, it'll give you that. If you want to spend hours with and use it to educate you and your partner about many of the ins and outs of financial planning, it will also do that. Modeling scenarios and changing assumptions are its strengths. It is also very useful for tweaking your plan slightly or just updating it every year. Boldin is well worth your time and certainly worth your money.

What do you think? Have you used Boldin? What did you like and not like?