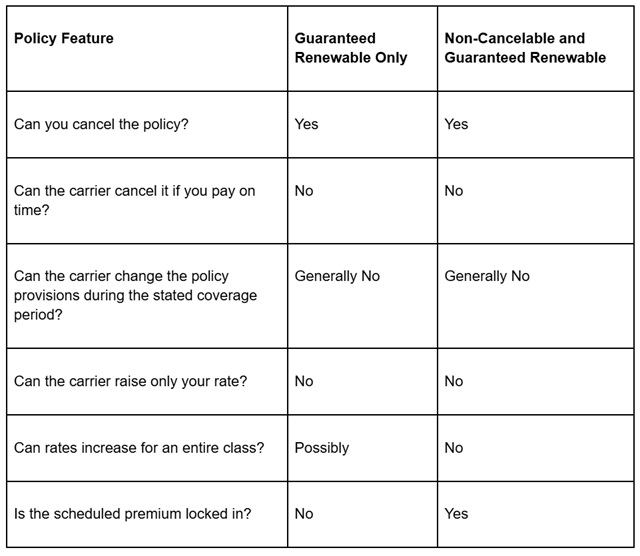

When buying individual disability insurance, you may be purchasing a policy that says the insurance company must keep your coverage in place as long as you pay the premium on time. Many policies include two important protections called guaranteed renewable and non-cancelable. Guaranteed renewable means the company generally cannot cancel your policy, change the policy terms, or raise your rate because your health changes or you file a claim. Non-cancelable adds another layer by locking in the scheduled premium through the stated coverage period, which is often to age 65 or 67.

That long-term protection is one reason individual disability insurance can cost more than people expect. You are not only buying a monthly benefit, but you also have stronger control over whether the policy can change later.

Today, let's talk about whether it's wise to have non-cancelable disability insurance.

What Is a Guaranteed Renewable Only Policy?

A guaranteed renewable only disability insurance policy means the insurance company cannot cancel your coverage as long as you pay the premium on time. It also cannot single you out for a rate increase because your health changes, you switch occupations, or you file a claim. The policy terms are generally locked in during the stated coverage period (typically to age 65 or 67). However, the company may be allowed to raise premiums for an entire class of similar policyholders, subject to the contract and state requirements. For example, the carrier might raise rates for policyholders with the same policy form, occupation class, gender, tobacco status, or state, depending on how the contract defines the class.

With that, the “generally locked in” matters because the policy language controls exactly what is guaranteed to continue. The base policy may be guaranteed renewable through a stated age, while certain riders or options can end earlier. For example, a future increase option may expire at a certain age even though the main disability policy remains in force. This also applies to non-cancelable and guaranteed renewable policies.

Among the major disability insurance carriers discussed here, Ameritas and The Standard currently allow buyers to choose a guaranteed renewable-only policy. Guardian, MassMutual, and Principal generally include both guaranteed renewable and non-cancelable protection in their main policies. Ameritas and The Standard also offer both protections, but they give buyers the option to leave off the non-cancelable provision.

More information here:- Disability Insurance Increase Riders: What’s the Difference?

- People Aren’t Buying Disability Insurance, But They Should

What Is a Non-Cancelable and Guaranteed Renewable Policy?

A non-cancelable and guaranteed renewable policy adds price increase risk protection: the insurance company cannot raise the scheduled premium during the stated coverage period. Put simply, guaranteed renewable protects your right to keep the policy and its terms, while non-cancelable also locks in the price, often to age 65 or 67. Without the non-cancelable provision, your premium could still increase if the carrier raises rates for an entire approved class of similar policyholders.

You can still cancel either type of policy whenever you choose.

Can You Save on Guaranteed Renewable Only Disability Insurance?

I compared Ameritas and The Standard to see whether choosing guaranteed renewable only coverage could save a few bucks while accepting the risk of a future rate increase for an entire class of policyholders. I kept the benefits, waiting period, benefit period, occupation, and riders as close to apples-to-apples as possible.

With Ameritas, the savings were tiny, about 0.2% for the male physician and 0.5% for the female physician. That small gap is partly due to how Ameritas handles mental and nervous condition coverage. Its guaranteed renewable policy already includes a 24-month limit on claims involving mental or nervous conditions, while the non-cancelable version can receive a 10% discount when the same limit is selected. That brings the prices very close together. Before this product change, the guaranteed renewable only option may have cost about 12%-13% less.

With The Standard, the savings were more noticeable at about 10% for both the male and female physicians. The tradeoff is simple: you save money now, but the carrier could possibly raise premiums later for an entire approved class of similar policyholders. These examples are only illustrations, and actual savings depend on the state, gender, occupation class, discounts, riders, and policy design.

Is Non-Cancelable Coverage Worth It?

For most buyers, non-cancelable coverage is worth considering because it removes the risk of a class-wide premium increase during the guaranteed coverage period. With Ameritas, the savings from choosing guaranteed renewable only coverage were so small in the examples above that paying a little more to lock in the premium may be worth considering. With The Standard, the savings were closer to 10%, so choosing guaranteed renewable only coverage may be worth it when looking at price alone. Even then, the extra cost for non-cancelable protection may still be worth it.

Keep in mind—and I’ll reiterate this—disability insurance is about more than cost. The policy provisions and the rules that determine whether and how benefits are paid matter just as much, if not more, than the premium.

More information here:- 17 Physician Disability Insurance Mistakes to Avoid

- The Physician’s Guide to the Best Disability Insurance Companies

What Happens After the Guaranteed Coverage Period Ends?

Many people assume disability insurance automatically ends at age 65 or 67, but that is not always true. Some policies allow coverage to continue after the original end date if the insured is still working and meets the policy’s renewal rules. At that point, the policy may become conditionally renewable (which means it may renew one year at a time), premiums may be based on the insured’s current age, and some riders may end.

For example, MassMutual’s Radius Choice policy may continue after age 65 if the insured is still working and meets the policy requirements. If a disability begins at age 65 or later but before age 75, the maximum benefit period is 24 months, even if the original policy had a benefit period to age 67 or 70. If a disability begins after age 75, the maximum benefit period may be 12 months. Riders and optional benefits may also fall off when the policy becomes conditionally renewable, so the continued coverage may be more limited than it was before.

Guardian and Principal also allow certain policies to continue beyond the original coverage period if the insured is still working and meets their renewal rules. Continuing a policy past age 65 or 67 does not necessarily mean keeping every feature of the original policy, so the renewal terms should be reviewed before relying on that coverage later in life.

Always work with a knowledgeable independent insurance broker who can compare the major carriers and help you find the best fit.

The Bottom Line

The takeaway is simple: guaranteed renewable coverage protects the policyholder’s right to keep the policy, while non-cancelable coverage also protects the price. Locking in the premium is often worth considering, especially when the extra cost is small. However, disability insurance should never be chosen based on price alone. The policy language, definition of disability, exclusions, riders, and rules for getting paid can matter much more than saving a few dollars each month.

Do you have non-cancelable coverage or a guaranteed renewable only disability insurance policy? Does it help ease your mind? Or do you regret buying it? What should a young doctor do?

The White Coat Investor may receive compensation from White Coat Insurance Services, LLC; licensed in all states including MA and DC; CA license #6009217; NY license #1758759 (exp. 6/2027); Registered address: 10610 S. Jordan Gateway, #200 South Jordan, UT 84095. This does not affect the cost or coverage of insurance.