If you’re a high-income professional with significant income beyond W-2 wages, you likely need to make estimated tax payments during the year. The US tax system is pay-as-you-go, and the IRS expects you to remit your tax liability throughout the year—not just by April 15. Here are the due dates for all four quarters of the financial year:

Q1: April 15

Q2: June 15

Q3: September 15

Q4: January 15 (of the following year)

(or the next business day if the 15th falls on a weekend or holiday)

This means that even if you pay your entire safe harbor amount by the due date of your return, you could be assessed a penalty for underpayment of estimated taxes if your estimated payments were backloaded for that tax year. This penalty is essentially the amount of interest (calculated daily) between when the expected estimated payment was due and when it was actually paid. This penalty is essentially interest, calculated daily, at the IRS underpayment rate, which is currently 7% but changes quarterly.

The penalty is calculated within your tax return on Form 2210, which then flows into the “Amount You Owe” section of Form 1040. Importantly, this does not reduce the tax you owe—it only reduces the interest-based penalty for when the tax was paid.

How Are Quarterly Estimated Tax Penalties Calculated?

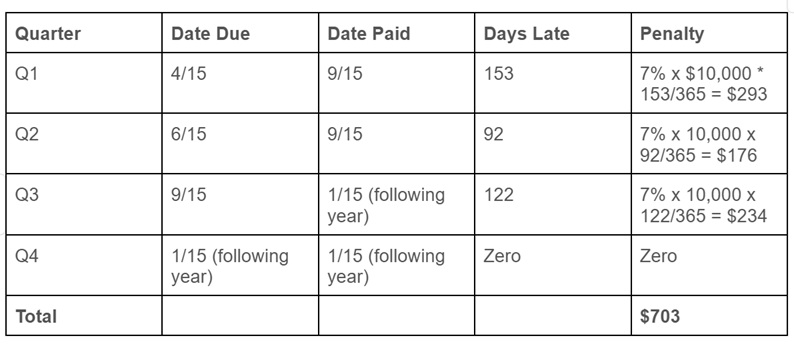

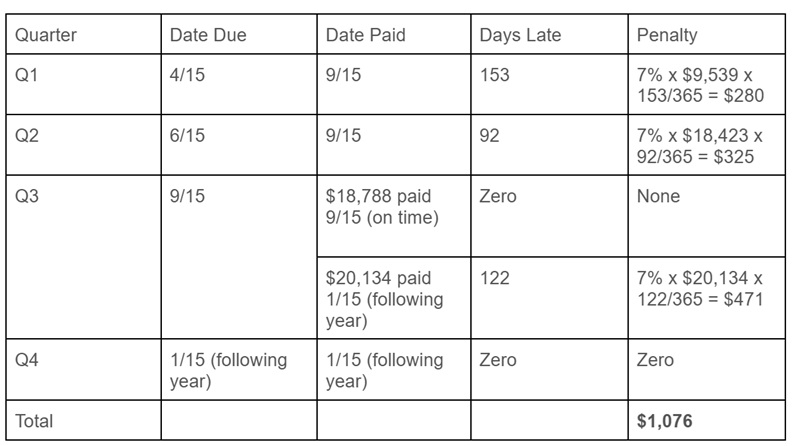

I’ve included a table that shows how the penalty is calculated. In this scenario, the taxpayer has an estimated payment obligation of $40,000 based on their safe harbor (the minimum amount of taxes that someone needs to pay or withhold during the year to not have a penalty for underpayment) or $10,000 per quarter. Let’s imagine that this taxpayer switched from W-2 to 1099 at the beginning of the year, and they were unaware of the estimated payment requirements. As a result, they missed their Q1 and Q2 payments. To make up for this, they paid $20,000 on September 15 and $20,000 on January 15th. How much is the penalty?

Here is how the penalty is calculated:

Assumptions

- Calendar-year taxpayer

- No withholding

- Safe harbor based on prior year's tax

Note that the penalty is calculated for each expected payment in sequential order (the payment on September 15 is first used to “catch up” for the amounts due from Q1 and Q2 before it is applied to Q3). As this example illustrates, it’s unlikely that this penalty will make or break you, but it is still worth avoiding if possible.

Reducing Your Quarterly Estimated Tax Penalties

However, even after the end of the year, you potentially could mitigate this further by completing Form 2210.

Within Form 2210, there are three distinct parts, followed by Schedule AI (which I’ll dive into later). Part I is used to calculate your safe harbor for the tax year. In Part II, you indicate why you are filing Form 2210. Part III contains the actual penalty calculation.

Within Part II, you get several options to choose from to indicate why you are filing the form. The first two describe waivers that are available in limited circumstances (disability or retirement after age 62 with reasonable cause, or underpayment due to a federally declared disaster). The focus of this post is on the next two options, shown here:

By choosing Option C, you are electing to calculate your penalty using the annualized income installment method (AI). This is available for taxpayers whose income varied during the year. Although the IRS, by default, expects you to make equal estimated payments each quarter, this assumes your income tax liability was also incurred evenly throughout the year. The AI method allows for a fair computation of the penalty when there is a mismatch between the standard deadlines and the dates when the tax liability was incurred. It's your way of telling the IRS that you don't want to pay “early” and you have the documentation to support the timing of your income.

This is only likely to be helpful if you received more income (and incurred greater tax liability) later in the year. While it may seem advantageous to eke out a few months of extra interest, I don’t recommend doing this proactively because the benefit isn’t worth the effort of filling out a complicated tax form and maintaining detailed records. A more relevant scenario may be if a doctor has a big cash flow need (i.e., a late solo 401(k) contribution or saving for a home down payment) and has no choice but to defer the estimated payments. If that results in a penalty calculation, you might as well see how much you can reduce it.

More information here:- What Happens If You Miss a Quarterly Estimated Tax Payment?

- How to Pay Estimated Taxes on a Roth Conversion

Calculating the Penalty Using the Annualized Income Installment Method

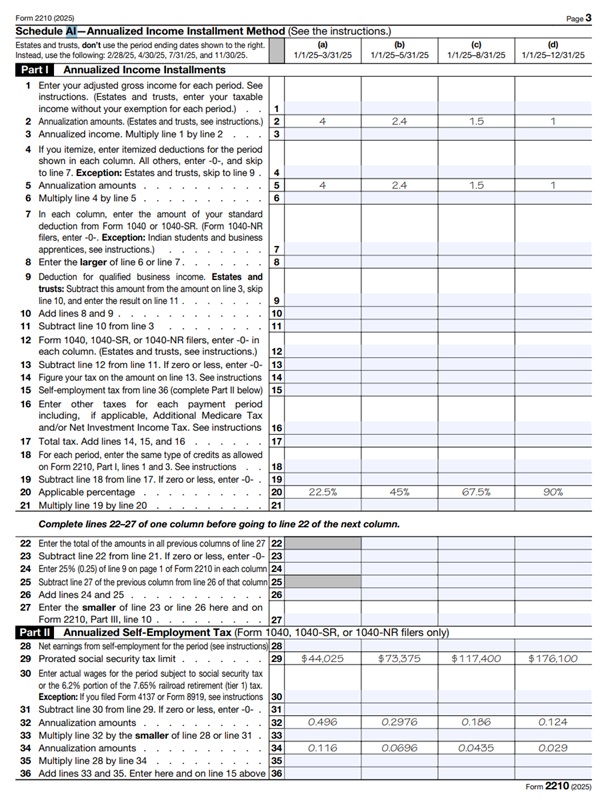

Before exploring a couple of scenarios, let’s take a look at Schedule AI within Form 2210, where this calculation is performed:

As you can see, this schedule can be overwhelming. You must calculate cumulative income through four IRS-defined periods ending on March 31, May 31, August 31, and December 31. This is admittedly the most cumbersome part of Schedule AI, since you can’t just rely on year-end tax reporting forms (W-2, 1099). You need to dig in and locate pay stubs and statements, and you also need to calculate deductions correctly. If preparing tax returns is not your day job, this may be difficult to determine quickly and accurately.

You also need to add up the itemized deductions for each period (primarily state taxes paid, mortgage interest, and charitable contributions).

A good tax software can likely handle the rest.

The simplest scenario, in which the data gathering would take the least amount of time, is for a self-employed taxpayer to maintain accurate and up-to-date records in a spreadsheet or other tracking software (which hopefully is being done anyway). This would allow the taxpayer to quickly compute net income for a particular date range without hunting down other source documents. If their investments are primarily in retirement accounts and they take the standard deduction, it may not take much time at all.

If you are working with a tax professional, ask them how much they will charge you to complete this form, and decide for yourself whether it is worth the time (or expense). Here's a simple (but imperfect) way to decide if it's “worth it.”

- It's probably not worth the trouble unless your penalty is >$1,000.

- Ask your tax preparer upfront how much this form will cost them to prepare. Then, ask them if they'll give you a lower price if you do the manual calculations for each of the four quarters.

- If the price is less than one-third of your penalty, then ask them to complete the form.

Now, let’s walk through an example to show the net impact of completing this schedule.

Example #1 — Annualized Income Installment Method

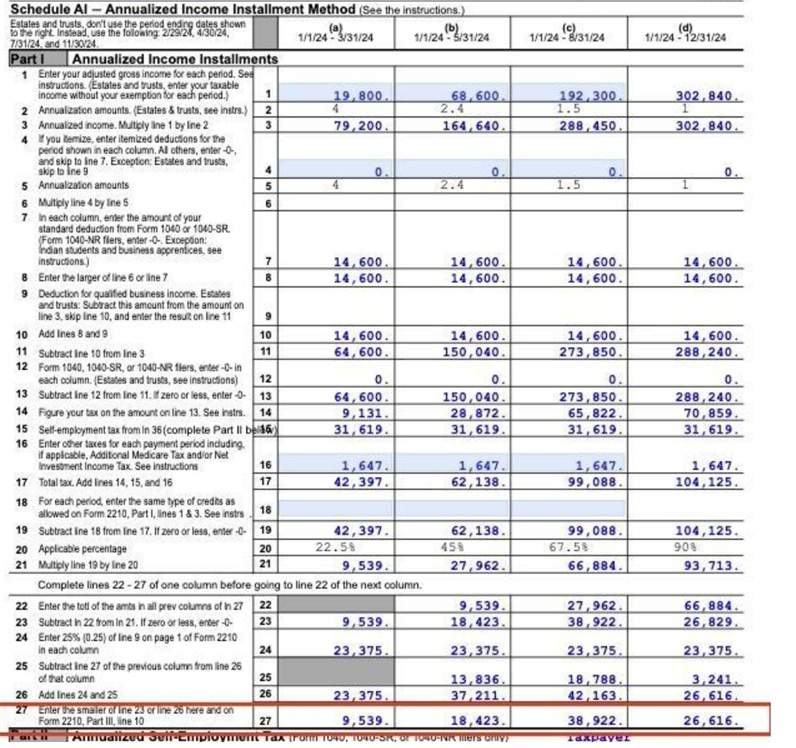

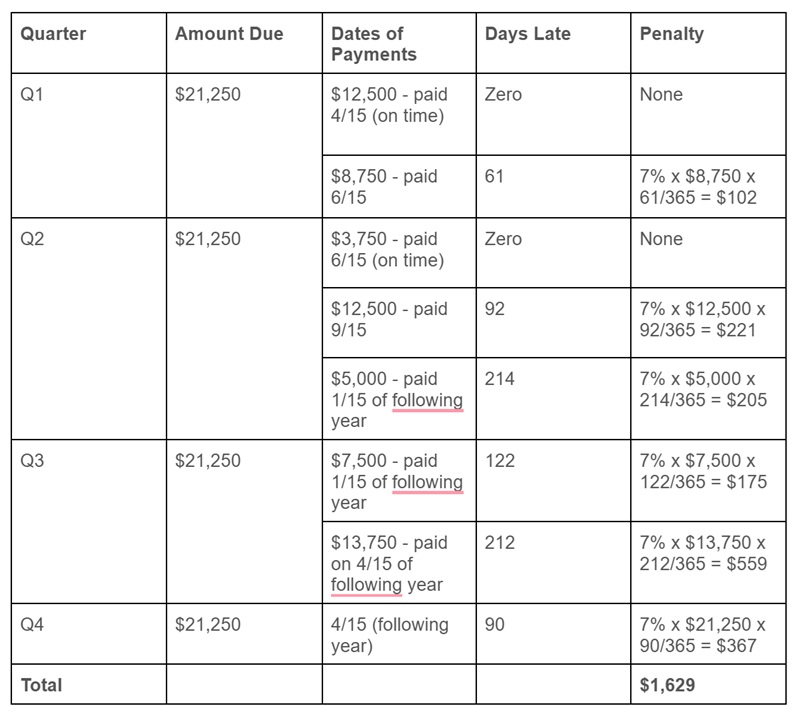

Sarah is a single 1099 physician who took off a lot of time in the first half of the year. Her net Schedule C income was $50,000 in the first quarter (January-March), $50,000 in the second quarter (April-May), $125,000 in the third quarter (June-August), and $175,000 in the fourth quarter (September-December).

She contributed $24,500 to her solo 401(k) in the first quarter on a pre-tax basis, and she made the remaining solo 401(k) contribution of $47,500 that December. She also contributed $4,400 to her HSA at the beginning of the year. Health insurance premiums of $700 were paid monthly. She received $100 of interest monthly. Finally, she was paid $500 of qualified dividends each quarter from her brokerage investments (in March, June, September, and December). She rents and takes the standard deduction.

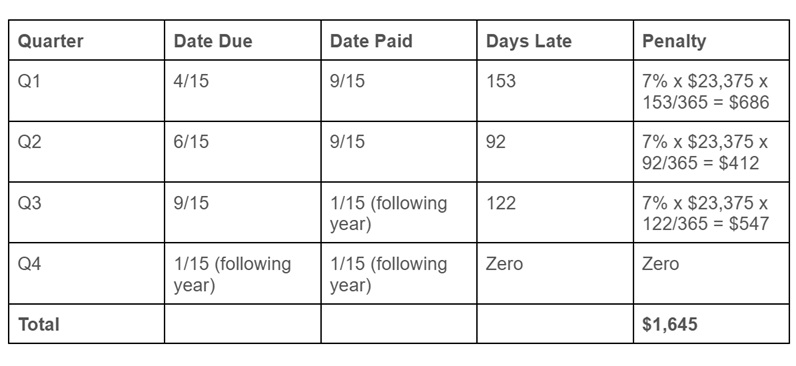

Her previous year’s tax liability was $85,000, and, thus, her safe harbor for estimated payments based on the previous year is $93,500 (let’s assume this is lower than the other safe harbor calculations). The IRS expects a minimum of $23,375 to be paid each quarter. If, instead, she pays $46,750 on September 15 and January 15, her penalty works out to be $1,645.

If she were to complete Schedule AI, this is how it would look.

The numbers to focus on here are in Line 27. They replace the “default” payment of $23,375 per quarter. If you use the numbers from line 27 (7% interest, calculated daily), the underpayment penalty works out to be quite a bit less:

By completing Schedule AI, Sarah saved $569. Even if her tax preparer charged her to complete this form, she likely would come out ahead. Perhaps she could have even completed it on her own quickly enough to justify the time and effort.

More information here:- The 5 Worst Tax Penalties

- Unhappy with Your Tax Audit Results? How to Appeal and Litigate an IRS Tax Audit

Example #2 — Frontloaded Withholding

Now, let’s examine another reason (Option D from earlier) to indicate why you are filing Form 2210. Importantly, unlike with estimated payments, the IRS does not track the dates during the year when taxes were withheld. It is assumed that equal amounts were withheld each quarter (even though the “quarters” are variable in duration). If you actually withheld more earlier in the year, however, your underpayment penalty is likely to be lower if you report the actual amounts withheld for each period.

An added benefit is that this is potentially much less cumbersome than calculating the underpayment using Schedule AI. Most likely, you can determine your W-2 withholdings for each quarter by examining the final paystub of each period.

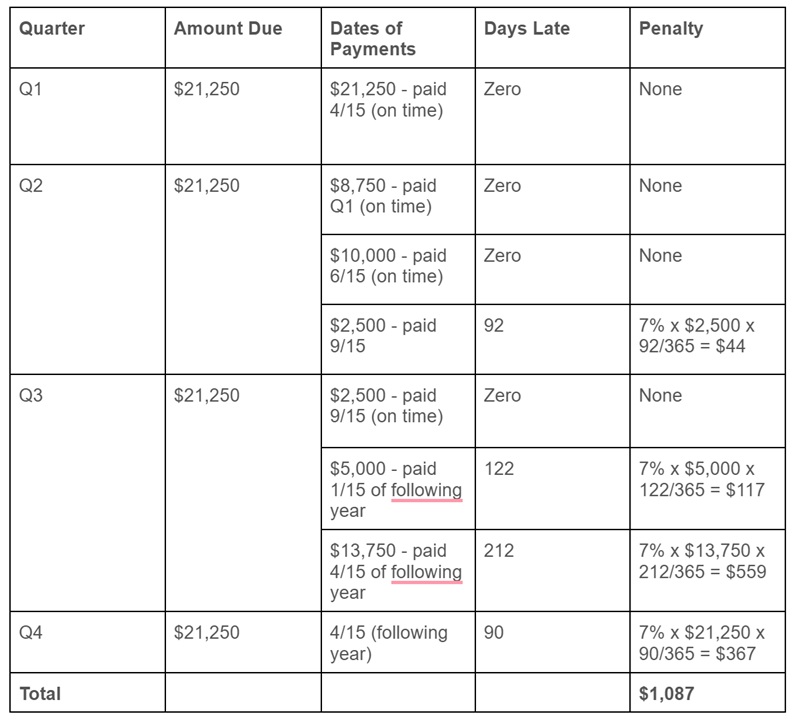

Here is a scenario in which the taxpayer benefits by documenting actual withholding for each quarter. Jeremy is a W-2 physician who earned most of his income in the first half of the year, but unfortunately, he filled out his W-4 incorrectly and underwithheld. His safe harbor is $85,000, but he only withheld $50,000, and he did not make any other estimated payments. As a result, it is assumed that $12,500 is withheld per quarter. When the tax return is initially prepared, the underpayment penalty is computed to be as follows:

If Jeremy goes back and looks at his pay stubs, he sees that $30,000 was withheld in Q1, $10,000 was withheld in Q2, and $5,000 was withheld in both Q3 and Q4.

This changes the penalty calculation as follows:

Similar to the previous example, using the actual withholding amounts in Part III of Form 2210 resulted in more than $500 of savings.

The Bottom Line

Although I understand that not all readers are inclined to crunch the numbers this way, I hope some qualitative observations stand out. These factors suggest that you could possibly reduce your underpayment penalty:

- Your income and tax liability are backloaded toward the end of the year. In this case, you may wish to complete Form 2210 and fill out Schedule AI.

- Your tax withholding is heavily shifted to the beginning of the year. In this case, you may wish to input the actual withholdings in Part II of Form 2210.

- Interest rates are higher. The higher the interest rate, the greater the underpayment penalty and also the larger the potential impact from an alternate calculation.

If one or more of these fact patterns describe you, it would be worth your while to ask your preparer if they will complete Form 2210 for you; or, if you are doing your own taxes, complete an alternate calculation if it is not unacceptably onerous. If you later conclude that the juice isn’t worth the squeeze, you can always just go with the base calculation.

What do you think? Have you ever tried to reduce your tax penalty for not paying enough quarterly estimated payments? Did it work?