Most disability insurance also includes “riders” or additions to the policy usually accompanied by an additional premium. These riders have different names at different companies, but the gist is the same and the devil is always in the details, so pay attention to them. Each rider comes with a cost that varies by policy, so check with your independent agent to obtain individualized pricing for you that can be used to compare one policy to another. Remember when faced with the decision of whether to purchase these riders that the advice you receive from your disability insurance agent isn't unbiased. Their incentive is to sell you as much benefit as possible and as many riders as possible. Each will increase the cost (and value) of your policy, and thus the size of their commission. So it is best that you get some unbiased information about the value of each of these.

Which Disability Insurance Riders Do Physicians Need?

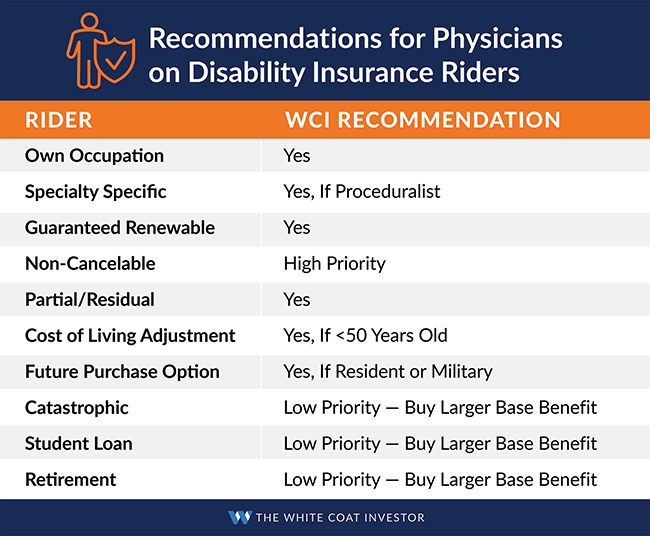

Partial and Residual Disability Rider

A partial disability rider pays if you can still work part of the time or you can still earn some money. This benefit is usually triggered by a drop in income secondary to an illness or accident.

A residual disability rider covers you as you gradually recover from a disability. It allows you to get some financial assistance to make up for the lost income. A residual rider will allow you to receive partial benefits if you endure a 15%-20% or more loss of earnings. This percentage is specific to each insurance provider, so make sure to ask your advisor for full details.

Keep in mind, the “basic” residual disability riders will state that you must lose at least 20% of your income and time or duties in order to qualify for partial disability. Others, such as “enhanced” residual, will state you must lose at least 15% of income to qualify.

Who Should Consider a Residual Disability Rider?

This rider should be purchased by everyone. It covers not only a partial disability but also provides a partial benefit as you recover from your disability. Be aware that the rider with each company is slightly different. Some are better than others, and the better ones usually cost more. You will generally get what you pay for in this regard.

Inflation Protection

This rider indexes your benefit to inflation, usually starting one year after you become disabled. This is a particularly important rider if you are disabled at a young age, so I recommend it for anyone buying a policy in their 20s-40s. If you are already 55 and the policy is only going to pay until you are 65, you can probably skip this rider.

Future Purchase Option

The Future Purchase Option (FPO) rider allows you to buy a larger benefit at a later date without any pesky questions about your health or hobbies. If you are in a position (such as a resident) where you cannot afford as much as you need, purchase this rider.

There are different future increase riders named Future Increase Option (FIO), Benefit Update (BU), Benefit Purchase Rider (BPR), and Benefit Increase Rider (BIR).

Future Increase Option (FIO)

The Future Increase Option Rider will be the most flexible of the future increase riders. You will be allowed to increase at any policy date in the future. You are never forced to increase coverage. Due to the flexibility, this rider comes at an additional cost within the plans. Ameritas, Guardian, and MassMutual are the companies that will have this rider.

Benefit Update (BU), Benefit Purchase (BPR), and Benefit Increase Riders (BIR)

These riders all work the same way. You are allowed one increase at the end of each third year. At the end of the third year, you will need to provide income documentation and request an increase. If you qualify for an increase based on income and other long-term disability coverage, you would need to accept at least 50% of the increase amount you qualify for in order to renew your rider for the following three years. It’s a continuous 3-year cycle where you will need to request an increase to renew the rider. If you do not request an increase at any third year period or you do not increase by at least 50% of what you qualify for, you will lose the future increase rider forever. If you lose the rider, you will need to undergo additional medical underwriting only if you wish to further increase the benefit in the future.

Who Should Consider a FPO Rider?

I think it is worthwhile if you are a resident, a fellow, or a young attending anticipating a large increase in income soon. Otherwise, I'd just buy a larger policy initially and skip the FPO. It's usually only good for ~10 years anyway. For the same price as the FPO, you could have a 10% larger policy. The main benefit is that you save the hassle of buying a whole new policy and you don't have to prove insurability again. You really don't get it any cheaper than you otherwise could later (assuming you're still insurable).

Catastrophic Disability

This rider pays out an even larger benefit if you are REALLY disabled, usually defined as not being able to do two or more activities of daily living such as dressing, bathing, toileting, or feeding yourself. This is supposed to cover the cost of an in-home assistant (think CNA) to help you with those activities.

Who Should Consider Buying a Catastrophic Disability Rider?

Unless you are already up against the maximum amount you can purchase, I think you are probably better off just buying a larger primary benefit instead of this rider. Some advisors disagree, arguing that a catastrophic disability rider is relatively inexpensive since an expense of perhaps $1,000 per year could add an extra $8,000-$10,000 in monthly benefit. As you decide what to do, just know that there is some controversy about this rider. Obviously, the agent gets paid more to sell you a policy with as many bells and whistles as possible, so they cannot provide a completely unbiased opinion on questions like this. You will just have to decide.

Retirement Benefit

This rider, in the event of disability, causes the insurance company to put some money into some type of retirement vehicle for you in addition to paying your monthly benefit. Unfortunately, these are generally high-expense, insurance-based investing products and not the best way to save for retirement. You are better off purchasing a larger primary benefit with the money that would have gone toward this rider. Just don't forget you need to continue to save for retirement using your disability benefit money since the policy will only pay to age 65, or you will be living only on your Social Security benefits.

Who Should Consider Buying the Retirement Benefit Rider?

Since the investment options the company is likely to use are generally poor compared to what is available on the open market, I recommend you skip this rider. Of course, you need to make sure the benefit you have purchased is sufficiently large that you can not only live on it, but also save for retirement on it, since the policy will only pay until you are in your mid-60s. If you wish you could buy more disability coverage than they will sell you, this is one area where you can get a little bit more.

Cost of Living Rider (COLA)

The Cost of Living Adjustment Rider (COLA), which is optional, is designed to help your disability insurance benefits keep pace with inflation. COLAs generally adjust your policy's monthly benefit annually, based on a fixed percentage or tied to the Consumer Price Index (CPI), after you have been disabled for 12 months. These adjustments apply to both total and residual disabilities and can be based on a simple or compound basis. Although expensive, this rider can provide significant increases to your monthly benefit if you are disabled early in your career.

COLA Rider vs. Additional Disability Coverage

My general rule is that the younger you are and the fewer assets you have (and thus the longer you have until you become financially independent and can drop the policy), the more important the COLA rider is for you to include as part of your policy. However, if you are not opting for the maximum amount of coverage that you qualify for based upon your earned income, you should consider removing the COLA rider and using the dollars you would have allocated to the COLA rider to purchase a larger monthly benefit. Remember, the COLA rider will not increase your monthly benefit until you have been disabled for 12 months. Therefore, if you are not disabled for a long-term period and have been paying the premiums for the COLA Rider, you may not realize as much of an economic benefit from the rider.

Who Should Consider Buying a COLA Rider?

I think this rider is mandatory in the first half of your career. However, since most policies only pay until age 65 or 67, I do not see much reason for someone in their 50s or 60s to be paying for it.

Non-Cancelable and Guaranteed Renewable Rider

If your policy is not non-cancelable and guaranteed renewable, you'll need to buy a rider to get these important features. It's important to understand these terms.

- Conditionally Renewable – This means the company gets to decide what the conditions will be for you to renew your policy, and at what price. You DO NOT want a policy that is conditionally renewable. In fact, it would be unusual for a salesman to even try to sell you one.

- Guaranteed Renewable – This means the company can change your premium, so long as they change it for everyone in your state, your policy year, or your occupational class. But they must renew the policy at some price.

- Non-Cancelable and Guaranteed Renewable – This means the company cannot change anything about the policy—not the premiums, not the monthly benefits, and not the policy benefits up until age 65 (or whatever the specified age in the policy is). Even if you change occupation to something in a more risky class with a lower income, the benefit will remain in place at the same price.

Who Should Consider Buying a Non-Cancelable and Guaranteed Renewable Rider?

I recommend against buying any policy that isn't guaranteed renewable. I like it to be non-cancelable too, but you can make a decent argument for a policy that is just guaranteed renewable if it saves you a significant amount in premiums. It might be better to just spend that money on a larger base benefit.

Knowing which riders to buy and which riders to skip is an important part of the process of purchasing disability insurance. In my opinion, some riders—like a guaranteed renewable and a residual disability—are must-haves. Others, like a conditionally renewable rider, you should avoid buying. And others can be good purchases depending on when you actually buy them and how early you are in your career. But always be cautious: The disability insurance salesperson makes more money every time you say yes to a disability rider. Before you hand over that extra money for a rider, make sure that it's actually something that could be valuable if you ever have to use it.

What disability insurance riders do you have? Are there any you regret purchasing?

The White Coat Investor may receive compensation from White Coat Insurance Services, LLC; licensed in all states including MA and DC; CA license #6009217; NY license #1758759 (exp. 6/2027); Registered address: 10610 S. Jordan Gateway, #200 South Jordan, UT 84095. This does not affect the cost or coverage of insurance.