One of my favorite unsung investment asset classes is real estate debt. While one can invest in this in publicly traded investments, those investments tend to adopt equity like volatility (i.e., high) and yields (i.e., low). So, I actually prefer to invest in this asset class on the private side. I end up with stock-like returns with ridiculously low volatility compared to other investments. Let me give you some real-life examples from my own investments:

Fund #1

- 2021:8.5%

- 2022: 10.1%

- 2023:9.2%

- 2024: 9.6%

- 2025: 8.4%

Fund #2

- 2022: 11.7%

- 2023: 11.3%

- 2024: 10.6%

- 2025: 10.6%

Fund #3

- 2024: 9.6%

- 2025 (through September): 7.8%

The funds' own track records are much longer, but they basically look the same as the experience we've had with them over the last few years. We've been investing in real estate debt since 2017, and the returns have pretty much always looked this way:

- 2017 (last half): 6.7%

- 2018: 9.1%

- 2019: 15.8%

- 2020: 7.6%

- 2021: 7.7%

- 2022: 9.5%

- 2023: 9.1%

- 2024: 9.9%

- 2025: 9.8%

Unless you're just trying to knock the ball out of the park, that's a really attractive return profile—annualized returns of 9.6% with a lowest annual return of 7.6%. All three of these funds use a little bit of leverage, but they basically just invest in short-term (6-18 month) loans to developers backed by real estate in first lien position. It could be argued that these are lower-risk investments than stocks and even corporate bonds.

What's the catch? Well, there are several. The three funds above require accredited investor status, and they have $100,000-$500,000 minimum investments. That's out of reach for many WCIers who want a diversified portfolio. They're also private investments, so they offer less than daily liquidity (although it's usually only a few months). There's also the potential for scams, and they're more hassle to do due diligence on and buy and sell.

However, the real downside of this asset class has nothing to do with all that. To get these stock-like returns with short-term bond-like volatility, you end up with a terribly tax-inefficient investment. Basically, the whole return is paid out every year and is taxed at ordinary income tax rates. Now, those selling these investments like to call them tax-efficient because the 199A deduction basically makes it so that 20% of the return is tax-free. But that is nothing compared to the tax-efficiency you get with a stock index fund or an equity real estate investment.

Among the asset classes in which we invest, this is clearly the top candidate to be placed into a retirement account where it can grow in a tax-protected way. Tax-protected growth will make a bigger difference with this asset class than any other we own. So far, we have managed to get two of the three funds into a retirement account, with the other (Fund #1) held in our taxable account.

But then things started to get even more complicated.

Private Investments in Retirement Accounts

Anyone who has ever tried to put a private investment into a retirement account knows what I'm talking about. Go ahead. Try to buy one of these funds in your 401(k) or 457(b) and let me know how it goes. It's just not possible in most employer retirement accounts. People end up trying it with an IRA (traditional or Roth). But they usually can't pull it off with a typical cookie-cutter IRA from Vanguard, Fidelity, or Schwab. They end up going to a company offering “self-directed” or “checkbook” IRAs. These are the same accounts that people use to invest in gold or Bitcoin when all their retirement money is in retirement accounts. Not only do you have to manage another account, but there are usually some additional fees.

More information here:- Comparing Private Real Estate Lending Funds

- 5 Bad Arguments Against Private Real Estate Syndications

Unrelated Business Income Tax

A tax known as Unrelated Business Income Tax (UBIT) is assessed on Unrelated Business Taxable Income (UBTI). One type of UBIT applies to leveraged real estate investments inside retirement accounts. Basically, despite the fact that the investment is in a retirement account, you (or rather the retirement plan) have to pay some tax on it every year. And UBIT is charged at trust tax rates, which are notoriously high.

One well-known exception to UBIT occurs when you place the real estate investment into a 401(k) instead of an IRA. Few people can actually put private investments into 401(k)s, but if you can, you get out of paying UBIT, thanks to an exception noted in IRC 514(c)9. We can, because we set up the WCI 401(k) (aka the world's best 401(k)), so these sorts of investments are allowed. We incorporated lots of other cool features into it, like Mega Backdoor Roth IRA contributions, too. So far, so good.

Our Recent Issues

Fund #3 above sent us a notice last September 27.

“Fund #3 recently reached the 25% threshold for retirement plan assets, which triggers ERISA’s ‘plan asset' rules. Based on guidance from our legal counsel, our current regulatory framework does not permit us to manage Title I ERISA retirement plans within this fund. While we can continue to accept investments from traditional and Roth IRAs, we are unable to accommodate assets from 401(k)s, SEP-IRAs, SIMPLE IRAs, Keogh plans, and similar ERISA-covered accounts.

Unfortunately, this means we are required to redeem all Title I ERISA retirement assets from the fund, including your investment through the WCI 401(K) Plan. We plan to process these redemptions next Friday, September 26.”

I sincerely apologize for the inconvenience, but this step is necessary to remain compliant with ERISA regulations. Please let me know if you have any questions. Again, we are planning on processing your redemption on Friday, September 26, proceeds will be deposited to your Fidelity account.”

Uhhh . . . what? Apparently, ERISA is not OK with more than 25% of a fund being funded with ERISA assets. News to me. Especially since that's really where a savvy investor WANTS to hold these assets. So, with just a few days' notice, our investment was returned and was sitting in cash in one of our 401(k)s. Our choices were to reinvest in that fund using IRA dollars (not ERISA assets) or taxable dollars, drop that fund company altogether, or invest in a different fund at that company.

I kind of liked the idea of having three funds for diversification. But we've been investing with all three of these fund managers for many years (even more than the numbers above would indicate), and we decided we could live with just two of them. We dropped that company and simplified our finances a little bit. In order to maintain our 5% allocation to real estate debt, we decided to take that retirement account money and invest it into Fund #1, which we already owned in our taxable account.

While doing the paperwork to make the investment, I was informed of the following.

“Please be aware that tax deferred investments are subject to UBTI. The Fund has a tax exemption with the IRS, but the tax code says that to the extent that the Fund generates income through debt (in this case our Line of Credit with our Bank) that percentage is taxable even if you are invested through a Tax Deferred/Exempt investment. Each year the UBTI percentage will be reported in a footnote on the Schedule K-1 along with the applicable income amounts. If the amount of UBTI earned by your investment exceeds $1,000 in a given tax year, the Form 990T must be filed and applicable taxes paid. Custodians (such as Fidelity) are the ones that file and pay these taxes on your behalf. Please speak with your custodian or see the IRS website for more information regarding these tax regulations.

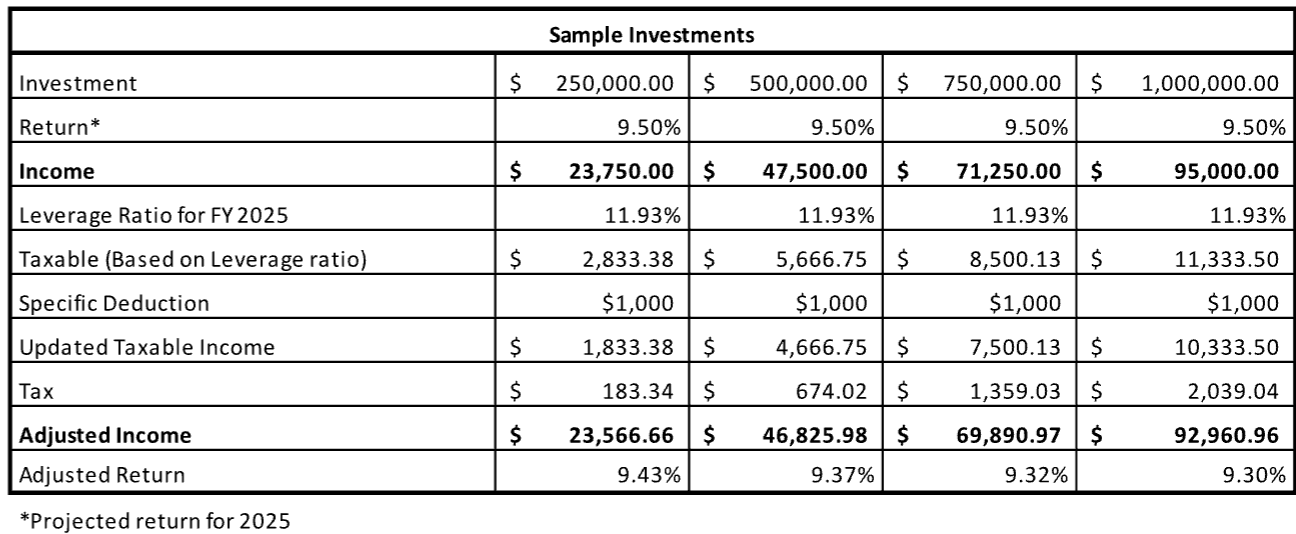

The tax paid is typically very small in comparison to your investment. For example, if you invest $250,000 the projected tax would be $183.34. See attached for more information. Please let us know if you have any questions.”

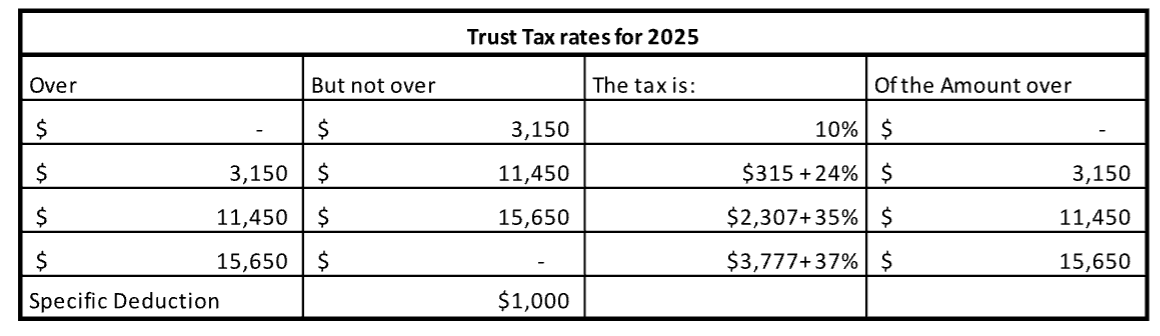

And two nice little charts were provided, one showing trust tax rates . . .

. . . and the other estimating how much UBIT we'd be paying and how much it would lower our returns.

As you can see, it's not a ton of tax, and it would really only lower our returns by something like 0.07%-0.20%. For us, it still makes sense as an investment and still makes sense to put it in a retirement account. Investing in this same fund in taxable reduces our returns by something more like 4.3%.

“But wait,” I said. “I thought UBIT didn't apply in 401(k)s.” I mean, we've been investing in leveraged debt funds through this 401(k) with two other companies for years and never paid UBIT. Fund #3 had its tax expert look into it, and we got this back:

“The biggest hurdle with 514(c)(9) is that it applies strictly to debt-financed real property but does not apply to interest income from mortgages. Also in our case, it would not apply to the dividend income that is coming from the REIT that is subject to the REIT stock which is considered debt-financed property. Note the following from 514(c)(9)(A) and see the yellow highlight : ‘(A)In general Except as provided in subparagraph (B), the term “acquisition indebtedness” does not, for purposes of this section, include indebtedness incurred by a qualified organization in acquiring or improving any real property. For purposes of this paragraph, an interest in a mortgage shall in no event be treated as real property.' So, I would say in a typical debt fund you can still have UBTI as a result of acquisition indebtedness and again the Section 514(c)(9) exception would not apply because it only applies to debt-financed real property.

Basically, the argument was that the 401(k) UBIT exception only applies to equity real estate investments, not debt real estate investments. I thought the argument was very reasonable, but that doesn't mean I'm going to forward it to Fund #2!

More information here:- The 5 Characteristics of My Ideal Private Real Estate Fund

- I Want to Invest in Real Estate, But I Also Want to Be Totally Lazy About It: What Are My Options?

Fund #3 Wasn't Alone

Then I started hearing complaints from WCIers about one of the companies (Fund #2) that partners with WCI to raise money. It seems it's also running into that 25% ERISA issue that Fund #3 had. Fund #2's explanation was much clearer, though. Basically, ERISA laws say that if more than 25% of one of their funds is retirement account money, the entire fund has to be treated as a retirement account, which is apparently a major compliance pain. So, they paused retirement account investments into their funds until the percentage falls back below 25% due to more taxable money being invested into the fund. This was apparently an issue not just for their debt fund, but also for one of their equity funds. I wish Fund #3 had just paused additional distributions rather than telling me they couldn't handle 401(k) money and just sending it all back with little notice. But such is life.

The bottom line is that it is great to get those relatively tax-inefficient real estate debt funds into retirement accounts, but don't be surprised if you run into some issues doing so.

What do you think? Have you invested in real estate inside of retirement accounts? What issues did you run into?