One of the main ways that investors make money is through capital gains. Understanding how capital gains are taxed is really important in order to maximize the tax efficiency of your investments.

Here's what you should know about the differences between short-term and long-term capital gains.

What Are Capital Gains?

Capital gains are simply the increase in value of an investment between the time you bought it and the time you sell it. The IRS does not recognize the existence of inflation in this regard, so even if your entire increase in value is just inflation, you will still be taxed on the increase.

What Is Basis?

Basis is the amount you paid for an asset. Capital gains are the amount above and beyond your basis. If an investment loses money, capital losses are the difference between your basis and the value at the time of the sale of the investment.

The Difference Between Short-Term and Long-Term Capital Gains

A short-term capital gain is simply the capital gain on something you have owned for one year or less. Once you have owned it for more than one year, your capital gains are considered by the IRS to be “long-term” and are, thus, eligible for a reduced tax rate. This lower rate is presumably to encourage long-term investing and to discourage a speculative, short-term mindset while investing.

More information here:What Is Capital Gains Tax?

If you bought a single share of stock for $100, your basis is $100. If it then increased in value to $110, your capital gain would be $10. You owe taxes on that $10 when you sell. That tax is called the capital gains tax.

How Does Capital Gains Tax Work?

A taxpayer reports their capital gains on Schedule D of Form 1040. There are separate sections for short-term capital gains/losses and long-term capital gains/losses. For most of us, tax software does all the calculating, but just like with taxes on earned income, one simply multiplies the amount of the gain by their capital gains tax rate.

What Is My Capital Gains Tax Rate?

Two sets of tax brackets are used to calculate the amount of tax due on capital gains. The first is the short-term capital gains tax brackets, which are precisely equal to the ordinary income tax brackets. These brackets are used for any investment that you owned for one year or less. The second set is the long-term capital gains tax brackets, which are precisely equal to the qualified dividend tax bracket.

The first thing you need to do when determining your capital gains tax rate is to figure out if your gain is short-term or long-term. Next, determine how much other taxable income you have. That income “fills up” the lower brackets so they are no longer available for your capital gains. Then, look at the tax bracket charts below to determine your capital gains tax rate.

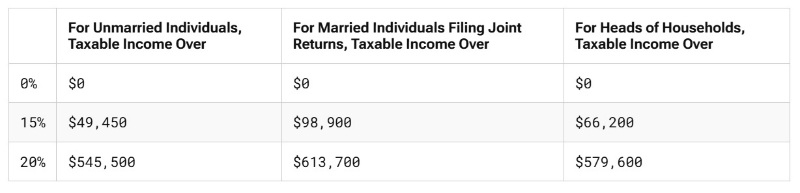

Long-Term Capital Gains Tax Rates

These are the tax rates at which you will pay taxes on long-term capital gains [2026 — visit our annual numbers page to get the most up-to-date figures], via the Tax Foundation.

Remember, those amounts are taxable income, not total income or even Adjusted Gross Income. As you can see, low earners may pay $0 in long-term capital gains. In fact, a married couple could have more than the median American household income (about $83,000 per year in 2024) and still pay 0% in long-term capital gains. However, most of those reading The White Coat Investor will find themselves in the 15% or even 20% long-term capital gains tax brackets.

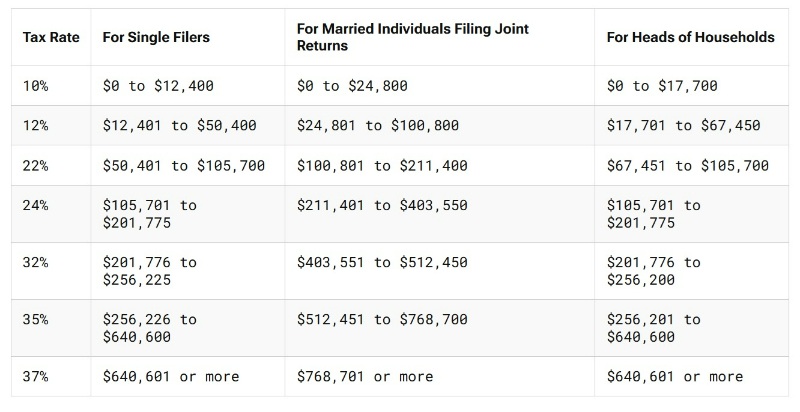

Short-Term Capital Gains Tax Rates

These are the rates at which you will pay on short-term capital gains for 2026 (that will be due in April 2027).

Note that they are precisely the same as your ordinary earned income. Even low earners are likely to pay taxes on their short-term capital gains since there is no 0% bracket. At a married taxable income of $500,000, long-term capital gains would be taxed at just 15% while short-term capital gains would be taxed at 32%, more than twice the rate.

Net Investment Income Tax

But wait, there's more! While you won't have to pay traditional payroll taxes like Social Security and Medicare taxes on capital gains, you will have to pay state income taxes on them in most states. Another tax on the investments of high earners was put into place as part of the Patient Protection and Affordable Care Act (PPACA, aka Obamacare). This tax is called the Net Investment Income Tax. If your Modified Adjusted Gross Income (MAGI) is more than $200,000 ($250,000 Married Filing Jointly), you will owe an additional 3.8% on both your short- and long-term capital gains. This is reported on IRS Form 8960.

In reality, the federal long-term capital gains brackets are 0%, 15%, 18.8%, and 23.8%.

Capital Gains Special Rates and Exceptions

There are not a lot of exceptions to these rules. Perhaps the biggest one is the exception on your residence. If you have lived in a home for at least two of the last five years, you can exclude up to $250,000 ($500,000 married) from capital gains once you sell the home. You can only claim this exception once every two years. You can also add the cost of any improvements and renovations to your basis so it will not be taxed.

On investment properties, depreciation is captured at up to 25%. Only appreciation above and beyond the recapture of depreciation is taxed at long-term capital gains rates. If you do a 1031 exchange to a similar property, you can defer payment of those capital gains, perhaps indefinitely.

Tax losses can also be used to offset capital gains. Some investors deliberately harvest tax losses for this purpose.

Advantages of Long-Term Capital Gains

The main advantage of long-term capital gains is that they are taxed at a lower rate than earned income, short-term capital gains, interest, and non-qualified dividends. However, there are three other significant advantages.

- You do not have to pay until you sell. You can defer paying taxes on gains for decades simply by not selling the investment. You could even avoid paying state income tax on those gains if you move to a tax-free state before selling.

- You do not have to pay Social Security or Medicare tax. These are not due on investment income like capital gains. You have probably read articles and social media posts complaining that the wealthy pay taxes at a lower rate than others. This is primarily because they often live off long-term capital gains instead of earned income.

- The step up in basis resets the basis to the value at the time of death, and neither the estate nor the heirs pays capital gains taxes on any gains that occurred prior to death.

Why Are Long-Term Capital Gains Taxed Less?

Cynics might argue that long-term capital gains are taxed at a lower rate because the wealthy control the levers of government. However, two very good reasons exist to tax long-term capital gains at lower rates than earned income. The first is to encourage investment, a critical aspect of our economy that increases the standard of living for everyone and also provides individual retirement security. The second is to acknowledge that capital gains are paid on every dollar of increased value, even if most of that increase is simply due to inflation and not a real increase.

Imagine a $100,000 investment that earned 5% a year over 20 years while inflation was 3% a year. In reality, that investment is only worth $149,000 on an inflation-adjusted basis, but the investor will owe taxes on a $165,000 gain—15% × $165,000 = $24,750, which is actually more money than 32% × $49,000 = $15,680.

How to Avoid Capital Gains Tax

You can avoid capital gains taxes in six different ways.

#1 Don't Sell

The easiest is to simply not sell the investment. No sale = no tax due.

#2 Use Tax Losses to Offset Gains

Tax-loss harvesting allows you to build up tax losses that can be later used to offset gains to avoid the payment of capital gains taxes.

#3 Live in It

With your principal residence, you can offset $250,000 ($500,000 married) in gains, plus any additional basis you contributed to improving the property.

#4 Exchange It

Unfortunately, this one only works with real estate. If you do a valid 1031 exchange to a similar property, both long-term capital gains and the recapture of depreciation are deferred.

#5 Give It to Charity

One of the best ways to give to charity is to donate appreciated shares you have owned for at least one year. The charity can rapidly liquidate the investment to cash, and neither you nor the charity has to pay long-term capital gains on it. Assuming you are itemizing, you can take the full value of the donation as an itemized deduction, further reducing your tax bill.

#6 Die

When you die, your capital gains are wiped out, thanks to the step up in basis at death. It is as though your heirs purchased the investment themselves on the day of your death.

More information here:- How to Achieve the Zero Tax Bracket in Retirement?

- How to Use Tax Diversification to Reduce Taxes Now AND in Retirement

How Do I Avoid Short-Term Capital Gains?

Simple, just make sure you own the investment for a minimum of 366 days before you sell it.

Can Short-Term Losses Offset Long-Term Gains?

Yes! On Schedule D of Form 1040, all of your short- and long-term gains and losses are totaled up. First, short-term losses offset short-term gains, and then long-term losses offset long-term gains. Any leftover losses of either type can be used against the other type of gains.

Capital gains are a great way to obtain money to live on from your investments. You can minimize the tax hit of this money by ensuring that all of your gains are long-term.

What do you think? What questions do you have about capital gains and their associated taxes?

[This updated post was originally published in 2021.]