Financial service companies—like mutual fund providers, brokerages, banks, and insurance companies—are always coming up with new products to sell you. While they occasionally develop something that turns out to be very beneficial in the long run (like Exchange Traded Funds or ETFs), most of the “innovations” result in products designed to be sold, not bought.

Frequently, these products play on the natural desire of investors to limit their losses. Investors want free lunches. They want all of the upside with none of the downside. These products never offer that, of course, because it cannot be offered. So, these companies offer products that limit the upside in exchange for limiting the downside. The question then becomes, “Am I giving up too much of the upside to avoid the downside?” In my opinion, the answer is usually yes.

Over the last five or six years, several companies have come up with new innovations that avoid a lot of the problems associated with past “versions” of these products, such as structured notes or fixed index annuities. While there are innumerable variations on the theme, these new products are generally called “buffered ETFs,” and if you haven't heard about them yet, you will soon, given the amount of marketing going on in this space.

Buffered ETFs

A buffered ETF is simply a basket of options placed into an ETF wrapper. The ETF wrapper is the main new innovation, and it allows for lower costs (including no commissions) and increased tax efficiency. The options are what provide the “buffer.” There is nothing in these buffered ETFs except options. Your investment is not backed by anything but the options, and you're putting your faith into the increasingly regulated Options Clearing Corporation (OCC).

The general premise of the investment is that you acquire a limited downside (how much your investment can drop) in exchange for a cap on your upside. Since options can be written in an unlimited number of ways, these can be put together with all kinds of combinations of an upside cap and a downside limit.

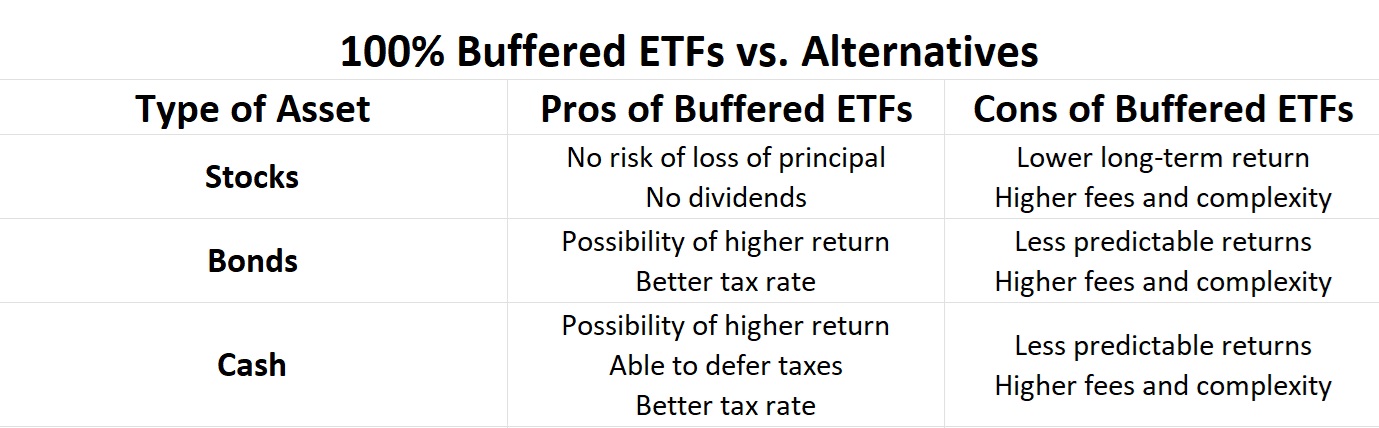

Some buffered ETFs have higher potential returns (in exchange for a higher downside). A popular type is a “100% buffer,” where the ETF is set up such that the options inside will prevent you from losing any principal no matter what the market does. These days, you can get a “guarantee” of not losing principal in exchange for a cap on your maximum return of 8% or 9%. Your return will, in essence, be between 0%-9%. Some people find this to be an attractive proposition to the available alternatives, and it's not too hard to see why.

Naturally, the marketing around these products focuses on the pros much more than the cons. Here are some examples from one of the providers, Calamos.

No surprise that Calamos thinks these products are perfect for everyone. I mean, who wants downside? Nobody. It's saying these things could replace equities, bonds, and/or cash in your portfolio. I actually don't think any of that is true. They're none of the above; they're options. I find them to be less attractive than the “real” investments for all of the usual purposes, but I know at least one informed white coat investor who doesn't feel the same way. He wrote me about them and loves them. In fact, he spends several hours a day trading them. I don't think very many WCIers have any interest in that, but he thinks they're a great option (no pun intended) for part of a buy-and-hold portfolio.

More information here:

Options, Futures, Margin, and Short-Selling: The 4 Horsemen of Your Financial Apocalypse?

Buffered ETFs vs. Fixed Index Annuities vs. Structured Notes

It should be noted that these buffered ETFs are dramatically better than prior “versions” of this sort of product, such as structured notes and fixed index annuities. You avoid commissions, get some sweet tax treatment, and avoid counterparty risk (although I suppose there is some risk associated with the use of options).

An Example CPSM

Let's take a look at an example of a 100% buffered ETF, the Calamos S&P 500 Structured Alt Protection ETF (CPSM). This is a one-year investment that came out on May 1, 2024. It guarantees you won't lose money from May 1, 2024-April 30, 2025 in exchange for capping your upside at 9.12%. So, your return will be between 0%-9.12%, all in exchange for an expense ratio of 0.69%, approximately 23X what you would pay to Vanguard to invest in its 500 Index Fund. Your actual return would be determined by the performance of the S&P 500 index (without dividends reinvested). If it had a negative return over that time period, your performance would be 0%. If it had a return of more than 9.12% over that time period, your return would be 9.12%. If it had a return between 0%-9.12%, you would get that return. Does that seem attractive? You don't know? Let's consider the alternatives.

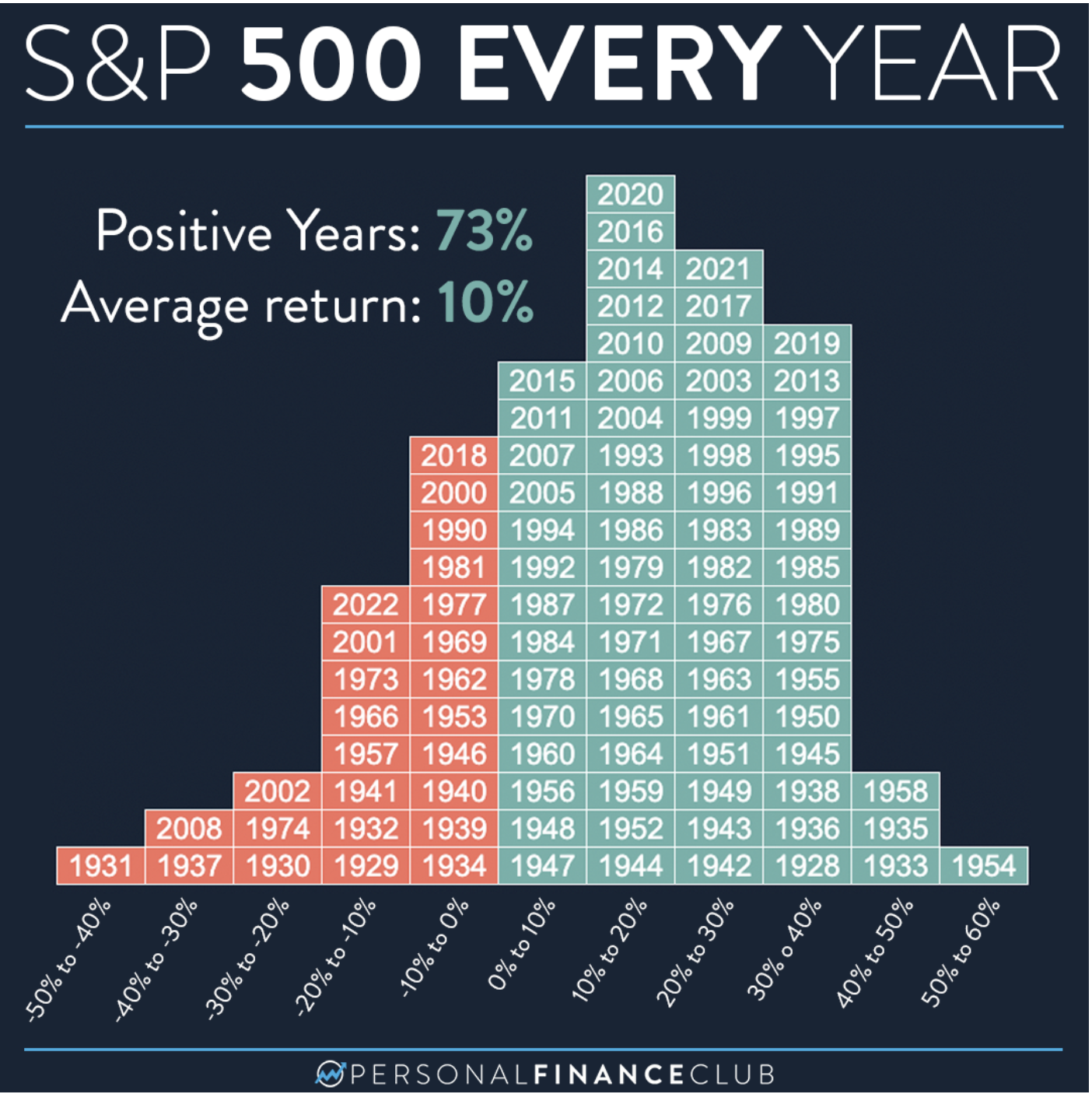

You could invest in stocks via a simple index fund or ETF. You would have an unlimited upside and an unlimited downside. However, you could get some historical data that would give a sense of what would be likely. Consider this handy chart put together by Personal Finance Club.

As you can see, the S&P 500 goes up about three-fourths of the time. The average is about 10%. But what percentage of the time would you be capped out? From 1928-2022, there were 94 years. In about 55 (the chart includes dividends, unlike the buffered ETFs) of those years, you would be capped out—sometimes severely. Imagine how painful that would be to watch stocks earn 30% and be capped at 9%. No, buffered ETFs are a terrible stock alternative. Instead of getting 10% in the long run, you might only be getting 5%. You don't get any of those really great years to offset all those 0% years.

What about cash? At times of low interest rates, I can see the appeal. Taking on some risk to get 5% instead of 1% might not be a bad idea. However, we're not currently in a time of low interest rates. As I write this, you can earn 5.28% in the Vanguard Federal Money Market Fund and as much as 5.37% in eight-week T-bills. While your exact cash return over the next year is unknown, it's going to be pretty close to that. It certainly isn't going to be 0%. The attractiveness of cash is not just that your principal is guaranteed, it's also that your return is relatively predictable. That's not the case with a buffered ETF. Why deal with the volatility of 0%-9% returns just to get the same 5% expected return you could get in a money market fund? When it comes to cash, I don't want to speculate on my returns. Buffered ETFs are a lousy cash alternative.

What about bonds? Well, a 0%-9% return is pretty similar to what you might expect from the annual performance of a typical bond fund. If you look at annual returns for the Vanguard Total Bond Market Index Fund for the last 15 years, you'll see returns ranging from 8.71% (2019) to -13.16% (2022) with essentially 12 of the 15 years between 0%-9%. If you want to compare a buffered ETF to something, comparing it to the bond portion of your portfolio seems most appropriate to me. But is it any better? Depends on what you value.

What Are These ETFs Actually Doing?

If we look under the hood of these products, what do we see? We see options. Sometimes a really complicated set of options. Buffered ETFs are created using FLEX options, customized to the strike prices, underlying asset, and expiration dates. These options are traded on an exchange in Chicago and backed by the OCC. As long as the OCC can meet its obligations, the ETFs should perform as advertised. I don't know how significant the risk is of the OCC not doing that, but given the newness of these products, it is something to consider.

Buffered ETFs are simply an actively managed basket of FLEX options that all expire on the outcome period end date (six months, one year, two years, etc). Portfolio manager Marc Odo explains:

“Most buffered outcome ETFs employ some version of a trade known as a put-spread collar . . . A buffered outcome ETF typically has four components:

- A long, deep-in-the-money call position to give the ETF market exposure

- A long put to hedge the downside

- A short, out-of-the-money call

- A short put that is further out of the money than the long put

The premium collected from the two short positions (i.e. #3 and #4) is used to offset the cost of the hedge (#2). Often these trades are constructed to be “zero cost,” meaning the premium collection from the two short positions is meant to net out the cost of the hedge as closely as possible. This begets the question: ‘If most buffered outcome ETFs use this basic put-spread collar trade, how can there be so many different products on the market?'

It is true that buffered outcome ETFs share many core characteristics. Across the range of 100+ products, there are more similarities than differences. That said, the primary difference in the various buffered ETF products has to do with the trade-off between upside and downside. How much upside does a buffered ETF have before it is capped out vs. how much downside does the ETF experience before the hedge start to prevent losses? There are dozens of variations of buffered outcome ETFs designed for outcomes ranging from conservative to aggressive.”

Interestingly, Marc also says that in a really bad equities market, you could still lose principal. I'm not enough of an options guru to understand how and when that could happen, and that's actually my biggest problem with these products. He continues:

“The risks to most buffered ETFs lie in the extremes . . . If markets sell off too much, the buffered ETF is exposed to open-ended losses. [This] is a very real risk to capital.”

The general rule in financial markets is that additional return can only come through additional risk. Just because you can't see the risk doesn't mean it isn't there.

Complex enough for you? But wait, there's more!

More information here:

“Day Trading” My Way to Retirement

What If You Buy a Buffered ETF During the Year?

Here's the other issue. These caps and this performance only apply if you buy the product on the day it is issued. If you buy it later, you'll get something different, and you have to pay attention to all kinds of things like:

- Remaining cap

- Remaining buffer

- Remaining loss to buffer

I also think you give up the long-term capital gains tax treatment if you don't own the thing for at least a year.

The Tax Benefit

Speaking of tax treatment, the most interesting aspect of the buffered ETF structure is its tax efficiency. While the terms on the options are generally something like 6-24 months, they automatically renew into similar options within the ETF, so there are no dividends or capital gains distributions until you sell the ETF—which could be many years down the road. You would then pay at long term capital gains rates. The ETF can also “flush out” some of its capital gains to the Authorized Participants (APs). This is a significant improvement over the taxation of bonds, cash, and annuities. While you shouldn't let the tax tail wag the investment dog, it's always nice to get some improved tax treatment.

Could These Things Blow Up?

Complex financial instruments have a bad habit of blowing up (and don't kid yourself; this is a complex instrument). Everybody wants a free lunch, but history has shown that even rare underlying risks sometimes show up. Consider the story of LTCM, the highly leveraged hedge fund that almost crashed the global financial system in the late '90s, in part because they were using a form of “portfolio insurance” similar to what these buffered ETFs use. More recently, consider the shenanigans of 2008, when numerous risky loans were packaged up into financial instruments that were somehow then considered safe. While there is no counterparty risk, the author of the most comprehensive book on this subject says this:

Does any entity guarantee I will not lose my investment?

“No. Unlike certain insurance products and structured products, ETFs are not backed by the faith and credit of an issuing institution like an insurance company or a bank. This also means that buffer ETFs are not exposed to credit risk. The options held by the ETFs are guaranteed for settlement by the Options Clearing Corporation (OCC). In the unlikely event the OCC becomes insolvent or is otherwise unable to meet its settlement obligations, the ETFs could suffer significant losses. However, regulators have heightened their oversight of the OCC due to its designation as a Systemically Important Financial Market Utility (SIFMU).”

After reading that, I'm left to ponder how I might quantify the “unlikely” risk that something happens to the OCC or that its regulation is inadequate. The OCC describes itself as . . .

“The world's largest equity derivatives clearing organization. Founded in 1973, OCC is dedicated to promoting stability and market integrity by delivering clearing and settlement services for options, futures, and securities lending transactions. As a Systemically Important Financial Market Utility (SIFMU), OCC operates under the jurisdiction of the US Securities and Exchange Commission (SEC), the US Commodity Futures Trading Commission (CFTC), and the Board of Governors of the Federal Reserve System. OCC has more than 100 clearing members and provides central counterparty (CCP) clearing and settlement services to 20 exchanges and trading platforms.”

I understand what I'm getting when I buy an index fund. I literally own very small pieces of the most profitable companies in the world. With a buffered ETF, I just own some options. Maybe I'm just options-phobic or maybe it's the fact that I lost 100% of my first investment (an option) as a teenager, but I'm not quite so sure I know what I'm buying exactly when I buy a buffered ETF. And if I'm not sure, I can't imagine most of its purchasers (or even their advisors) understand them.

They've really only been around a few years. Like in medicine, you never want to be the first or the last to adopt a “new improvement” for a reason. Many “new improvements” turn out to be no better or even worse than previously available treatments. Like with many investments that have shown up during my investing career, I'm content to sit on the sidelines and watch for a while. Maybe if these things still haven't blown up a decade or two from now, I'll have more interest in them.

More information here:

A Moderate-Income Physician’s Approach to Alternative Investments

A Neurologist’s Road to Becoming a Bitcoin Maximalist: Why Bitcoin Is Not the Next AOL

The Bottom Line

Katie and I aren't going to be investing our money into buffered ETFs any time soon. Options are on a long list of things we don't invest in, even if they get packaged up into an ETF wrapper. Basically, you're paying a fund manager to manage a portfolio of options for you for 50 or 100 basis points a year. You don't have to invest in everything to be successful.

That doesn't mean YOU can't use them in your portfolio, though. I think the most attractive version is probably the 100% buffer ETFs, which guarantee no loss of principal, as a substitute for muni bonds in a taxable account. Certainly, they have a more attractive tax treatment than taxable bonds while providing similar returns, and they theoretically could be used for similar purposes (reducing portfolio volatility, helping people stay the course, reducing sequence of returns risk, etc.) Aside from the risk of the options blowing up and higher expenses, the other downside is a higher correlation with the stocks in your portfolio than bonds have. Just remember the principles of investing that always apply.

- The less you buy and sell, the less you pay in fees.

- Fees matter—they can only be paid from one place, your return.

- There are no free lunches—higher returns come from taking on higher risk, even if you can't see the risk.

- For every buyer (including options buyers), there must be a seller who thinks they're getting the better end of the deal. Only one of you can be right.

What do you think? Are you investing in buffered ETFs? Are you interested in them? Why or why not?