For many years, I have worked multiple 1099 contract jobs outside of my full-time W-2 position. This work has included forensic psychiatry (expert witness) cases, disability evaluations, and outpatient telemedicine treatment. For a time, I was already maxing out my employer-sponsored 401(k) or 403(b) account, but I had no idea I could sock away a portion of my independent contractor earnings for tax-free savings as well. Around the end of 2018, after reading about it on WCI, I learned that I could open an individual or solo 401(k) as an additional tax-deferred savings vehicle. What I didn’t know back then was about the importance of filling out Form 5500-EZ once my solo 401(k) balance got high enough (more on that later).

Another bonus of creating a solo 401(k): it does not preclude one from completing a Backdoor Roth IRA contribution. It was a welcome surprise that I had this extra option, but I had to act quickly. Literally during the last day of the year in 2018, I headed to my local TD Ameritrade (TDA, now Schwab) office because I realized I had to open the account by the end of the calendar year (although I could fund it through Tax Day of the following year). I also made an appointment for my husband to open his own solo 401(k) that same day, and the agent promised he would process the paperwork and get our accounts opened before the clock struck midnight.

Our solo 401(k)s had officially been opened.

Using a Solo 401(k)

I’ve diligently contributed a portion of my 1099 earnings every year since then—some years more than others—based on my fluctuating extra income. However, there are some nuances or confusing elements to these contributions. First, I am considered BOTH the employer and employee of my small business. The solo 401(k) account is considered a “one-participant plan,” but it can also include a spouse or partner (again, a bit confusing). If you do not have or use an employer-sponsored 401(k)/403(b), you can contribute to your solo 401(k) as BOTH an employer and employee.

For my situation, I can only contribute as an employer since I already max out my employee contributions of $24,500 [2026 — visit our annual numbers page to get the most up-to-date figures] at my full-time job. It gets a little more complicated as I (or my accountant) have to calculate my yearly contribution amount—which is based on net earnings as a sole proprietor, with the maximum amount being 25% of the net compensation of the business. I have to calculate this based on multiple income streams, including my forensic work, for which I am “self-employed” and have to track my earnings on a spreadsheet.

For my telemedicine work, I work for a company as an independent contractor and receive a 1099 form, which is helpful. (Note: there are caps on the employee contribution AND the total annual combined 401(k) contributions based on age, under 50, and multiple brackets for those 50+. For me, the cap is $72,000 in 2026). There are also some other relatively new income and age-based stipulations that were implemented under the SECURE 2.0 Act, such as if my self-employment or W-2 income from the prior year (2025) exceeded $150,000, any age-based catch-up contributions must be designated as after-tax Roth contributions rather than pre-tax. None of these stipulations applied to me, but it's good to know about them for the future.

More information here:

Comparing 14 Types of Retirement Accounts

Form 5500-EZ

I finally reached a fun(?) milestone at the end of 2025, something that some WCIers might not even know about. If your solo 401(k) account exceeds $250,000 by the end of the calendar year, you have to fill out IRS Form 5500-EZ. Not a bad problem to have, but (yay!), I get to fill out another form. Sidenote: at the end of 2024, I was just under the threshold so I escaped this task by a smidgen. But I had already started to familiarize myself with the process.

Filling this out for the first time was not quite as “EZ” as the name implied. Just for funsies, the deadline for the form is in July, not on Tax Day, so you have to remember to file it in the middle of the summer. I was curious to know why, and it turns out it is not just to keep you on your toes. The form is due by the last day of the seventh month after the plan year ends (typically December 31), which lands on July 31 for calendar-year plans. Apparently, it gives more time for the business to reconcile its earnings and calculate its assets if there are complicated circumstances.

Who is required to fill out IRS Form 5500-EZ? The form is meant for the “Annual Return of a One-Participant Retirement Plan,” and it is required for business owners who have a self-employed retirement plan once the $250,000 threshold is met. It doesn't matter whether you consider yourself to be a “business owner,” because the IRS does for the purposes of these contributions.

The form is considered an “informational” return, meaning it is used strictly for reporting data rather than calculating or paying a tax liability. It seems to be an exercise in futility, but nobody asked me, so I proceeded to fill it out.

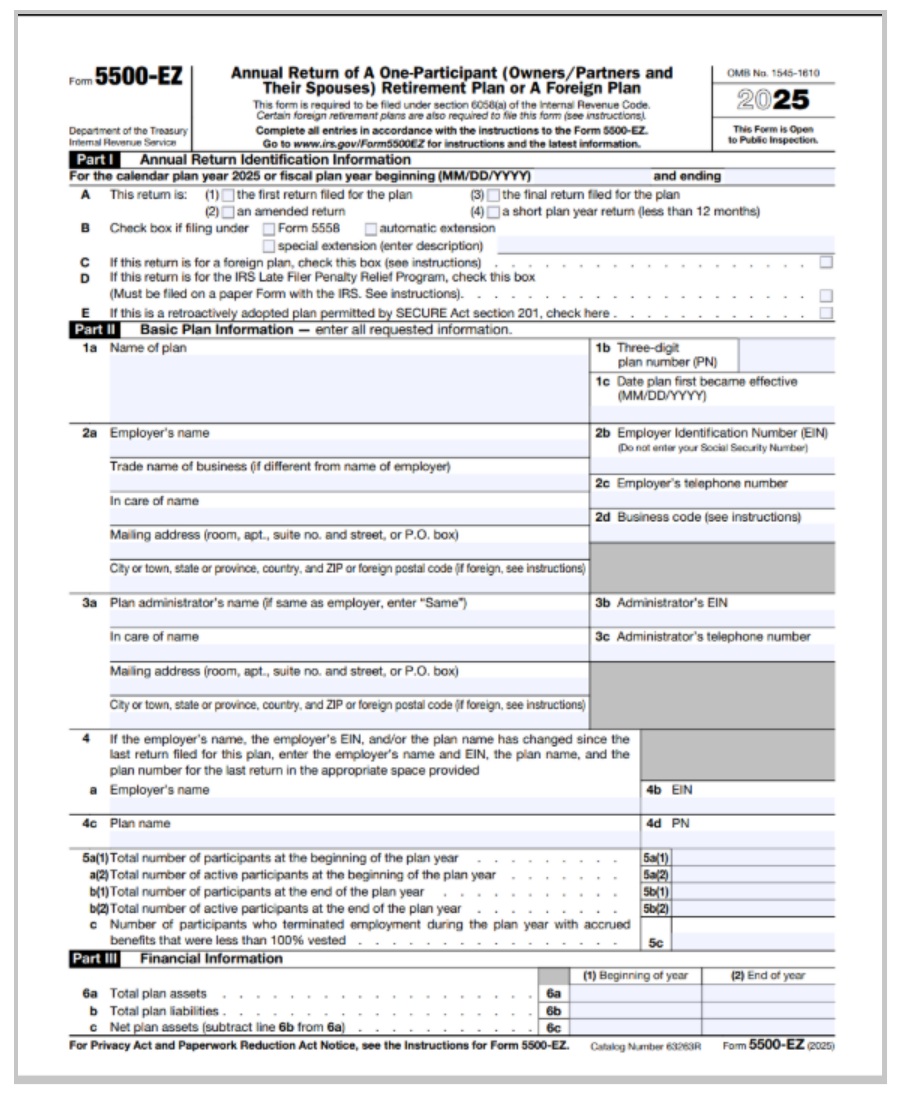

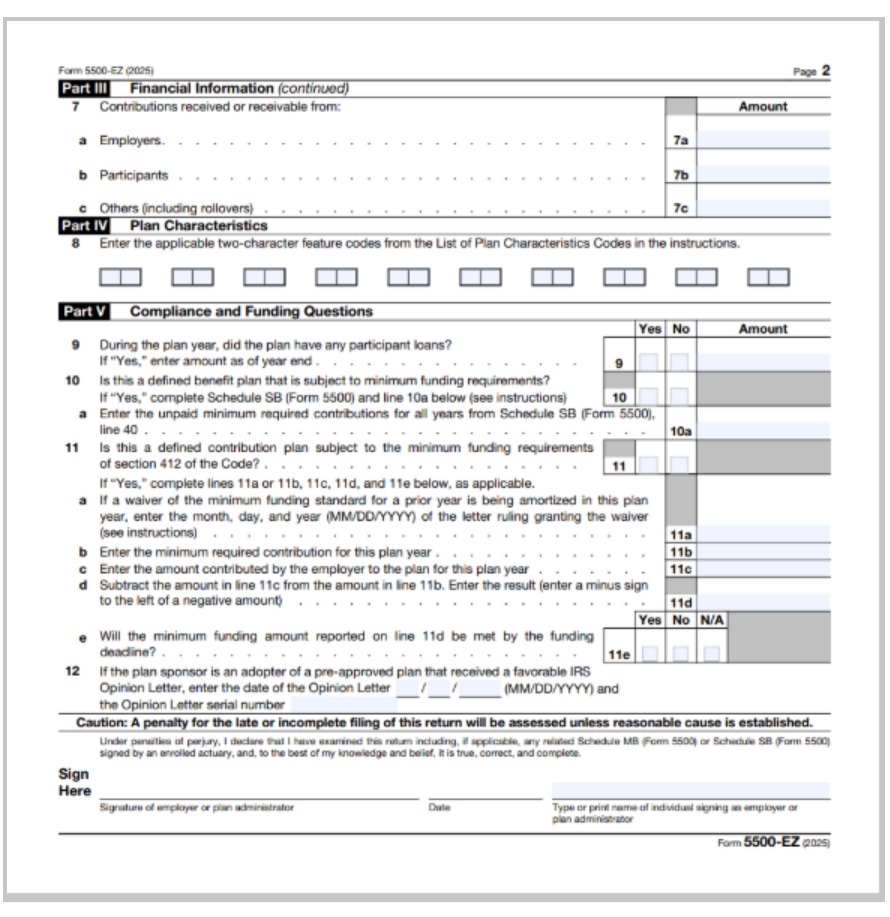

Here is where to find the form, the instructions for filling it out, and a screenshot of the two-page document:

More information here:

If You Forgot to File This 401(k) Form, Here’s How to Avoid Massive Penalties

Filling Out Form 5500-EZ

The good thing is that you can file this online for convenience (or you can send it via snail mail). However, there is a steep penalty for not filing the form on time once you reach the threshold ($250 per day up to $150,000, plus interest). Luckily, there is a process to reduce the penalty significantly if it has only been a few years of not filling it out. But as with many things in life, ignorance of the task is not a valid excuse.

Before beginning, I downloaded my Schwab “Tax Year 2025 Account Summary” and the account statement from December 31, 2025, for the individual 401(k), which had the starting and ending balances for the year. When I opened the account at TDA, an EIN (Employer Identification Number, a specific type of tax ID number) was not required, so I opened it under my Social Security number. However, when Schwab acquired TDA in 2020 and eventually transferred our accounts in 2022, it required that my husband and I both file for an EIN. I had that information ready to go, as well.

Part I — Annual Return Identification Information. This part was easy. I filled in the calendar dates and checked off the box for this being the “first return filed for the plan.”

Part II — Basic Plan Information. I filled in the name of my plan under 1a (as indicated on the tax statement). The three-digit plan number (1b) is 001, as this is the first and only plan for the business. The effective date was when the plan was opened (1c). Under #2, I added in the employer name (me) and my business address (2a), the aforementioned EIN (2b), and the business phone number (2c). Under 3a (plan administrator), I entered “same” and left the fields under #4 blank. For the 5a(1), 5a(2), 5b(1), 5b(2), and 5c fields, I put 1, 1, 1, 1, and 0.

Part III — Financial Information. For section 6a, I entered the assets of the plan at the start of the year and the end of the year per my brokerage statement. (Note: I checked, and the balance was listed as the same for December 31, 2024, and January 1, 2025, since the markets were closed because of New Year’s Day). I did not have any liabilities to list in 6b, so line 6c had the same values listed as in 6a. For section 7, I found my total contribution amount for the year on the brokerage statement and entered that into 7a.

Part IV — Plan Characteristics. I had to look at the “List of Plan Characteristic Codes” on the instruction document to fill in Line 8 and picked the codes that applied to me. The long list of over two dozen codes was confusing, and I had to reference an old WCI post and ask the internet to figure it out.

Part V — Compliance and Funding Questions. I answered “no” to questions 9, 10, and 11 and then left 11 a-d and 12 blank.

The “Sign Here” part may have been the easiest section, and I was ready to submit it well ahead of the deadline. Although it did take about 30-60 minutes to download the statements, read through the instructions, and fill in the form, it was still relatively simple. And now for next year, it really will be EZ-breezy!

Do you have any questions about Form 5500-EZ? Do you know anybody who has had to pay the penalty for not filling it out for the IRS? What happened?