Doctors are way too comfortable with debt.

For most physicians, getting through the training pipeline puts you in a deep financial hole. And while your family and society tell you you’re rich, you’re actually one of the poorest people in the country due to your negative net worth. By the time you’re finished with training, you could owe hundreds of thousands of dollars. The good news is that with a high income, you have a large shovel to dig out of debt, and if you put your mind to it, you can get rid of your debt and start building wealth quite rapidly.

The most important year in a physician’s financial life is their first year out of training, and some of the most important advice that can be given is contained in just four words.

The meaning of those four words is that if you can carve out a massive difference between your newfound high income and your lifestyle, you can build wealth rapidly. You can max out retirement accounts, pay off student loans, save up a down payment on a dream house, build an emergency fund, upgrade your car, and pay off your consumer debt all at the same time.

Within 2-5 years, your net worth may swing from negative $200,000 to positive $500,000. At that point, you can mostly grow into your income (while still saving 20% of gross for retirement) and have a financially awesome life. The easiest time to live like a resident is right after you have HAD to live like a resident. You're already used to living on $50,000-$70,000 (the average American household income). It's really not that hard to do it for a little while longer.

However, the truth is that almost no white coat investors live exactly like a resident. Most inflate their lifestyle a little. A little lifestyle creep is probably OK. Heck, give yourself a 50% raise. What you're trying to avoid, however, is a lifestyle explosion. If your spending quadruples when you leave residency, you blew a golden wealth-building opportunity. And it's really hard to go back.

The biggest hurdle most physicians face are large student loans. Seeing the dollar figure of these loans can be paralyzing, and with an overwhelming amount of government programs changes, it’s far too easy to ignore your loans. Do not do that. You need a plan. Most doctors who apply the live-like-a-resident approach can get out of student loan debt AND hit other financial goals within 2-5 years out of training. You can do that, too.

Want to celebrate your milestone? Apply to be a guest!

Milestones to Millionaire Podcast

If figuring out a plan to pay off your student loans is overwhelming, we have help for you. In 2021, we partnered with Andrew Paulson, Certified Student Loan Professional (CSLP), to open Student Loan Advice. For less than $600, SLA will meet with you online, review your student loan situation, and create a blueprint to optimize your student loan management plan until they’re paid off or forgiven. Then, the SLA team will be available to you by email for one year afterward to make sure you’re completely satisfied and on the right track.

Need further proof that partnering with SLA is the right move? The average SLA client saves $160,000 on their student loans.

Student Loan Advice

Enroll in WCI Financial Boot Camp, a FREE educational email series, and learn to convert your high income to wealth

You can unsubscribe anytime using the link at the bottom of any email.

Perhaps the best advice is to avoid extreme positions. Most of the time, there is no right answer, but maybe 5% of the time, there is. If you're giving up an employer match to pay off debt, you're making a mistake and basically leaving part of your salary on the table. If you're carrying credit card debt with a 30% interest rate in hopes that your investments will outperform it, you're making a mistake. But for just about everything else in between, it might make sense to invest but where it could also make sense to pay off debt—no matter what kind of debt that might be.

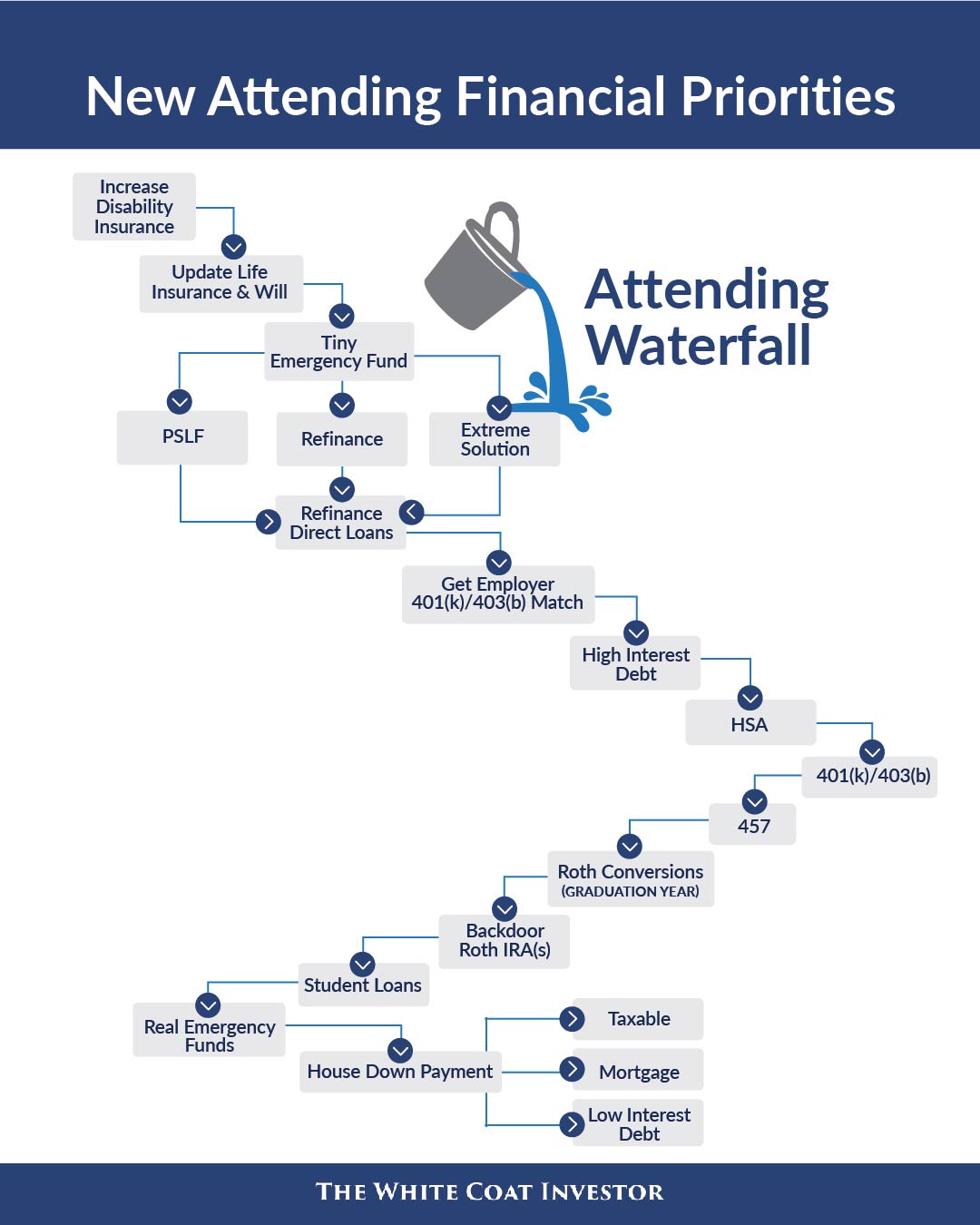

After you’ve tripled or quadrupled or even 10x’d your salary following your residency graduation, you’ll surely have plenty of uses for your new attending salary. But that debt isn’t going away, and you need to prioritize how to get rid of it while still finding ways to build wealth.

You can do that by following the attending waterfall, which you can see below. After increasing disability insurance, doing some estate planning, starting an emergency fund, and building a plan for your student loans, these are the next steps you take:

There’s more nuance and options if you look at the attending waterfall below, but the above list is a great place to start thinking about how to pay off your debt.

Medical school may not have taught you about money, but we will.

We will never sell your information. Modify your preferences or unsubscribe at any time.

Get ready to take control of your financial life. You can do this, and we can help.

We won't sell your information. Modify your preferences or unsubscribe at any time.