If you were a resident at NYU around 2011, I am publicly apologizing to you. You see, I wasn’t always financially literate, but I have always tried to advocate for my fellow doctors because I feel the utmost respect for my kindred spirits in the selfless mission of helping our patients be healthy.

To that end, I joined the Graduate Medical Education (GME) committee at NYU where I trained for the 2010-2011 residency year. I was the resident advocate on the committee that was made up of attendings. My job was to take any work-hour issues, complaints, suggestions, etc., from residents and bring them to the attention of the GME. This also made me the head of the NYU Housestaff Council, where I and a few other officers organized lectures for residents regarding wellness and, pertinent to WCI readers, resident finances.

It is this latter job for which I am apologizing.

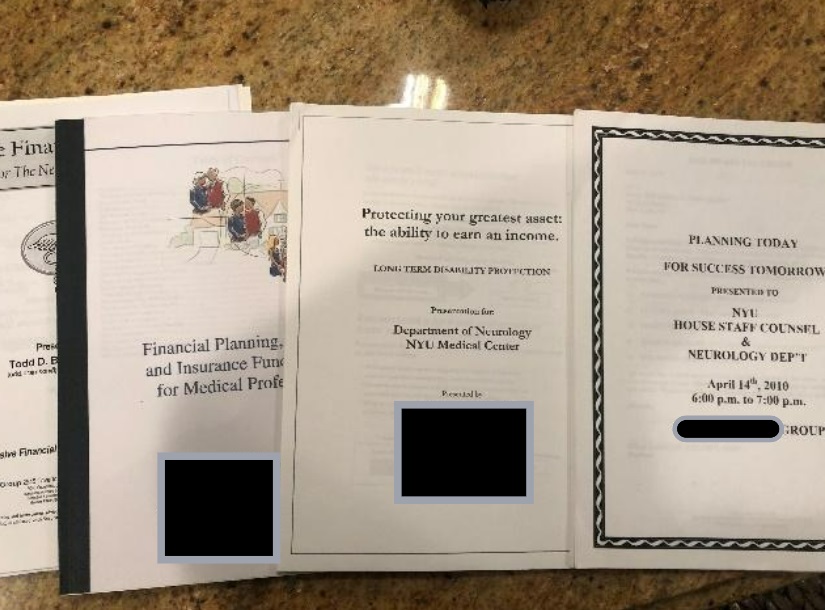

Unfortunately, I let financial advisors/salespeople come in to give finance talks to residents. This included salesmen supporting permanent life insurance as part of an optimal retirement plan, investing in actively managed funds, and selling variable annuities. I want to talk about why I let such a horrendous thing happen, exposing my fellow residents to a path that could ruin their financial lives, and to show that if you're currently a resident, you also should take caution with residency financial education at your institution.

To Go Where Salespeople Have Gone Before

OK, these non-fiduciary finance talks were not completely my fault. The GME gave me a list of previous speakers on physician finances. Unfortunately, it seemed the NYU attendings, at least on the GME committee, were also financially illiterate to suggest salespeople give financial talks to residents. But as I was setting up these lectures and contacting these salespeople, this was always how it had been done before. These salespeople had given out their information to the GME committee sometime in the past, promising that they were financial “advisors” who would help out residents with their financial lives.

In the defense of the GME, how would they vet these financial “advisors” and the material they were presenting? The White Coat Investor didn’t even exist when I joined the GME in 2010. The GME and I were doing the best we could with the information at hand. None of us knew the difference between a financial advisor and a financial salesperson. All we knew was that these salespeople had lectured to NYU residents previously, and no detrimental consequences from these talks were ever mentioned. So, these salespeople were continually allowed to have access to resident physicians.

We fell victim to status quo bias, and there was no negative feedback to stop these poor financial talks from occurring.

Free Food

It seems stupid now, but a lot of times these talks were well attended because the salesmen fed us.

Remember when you were a starving resident? Yes, amid a census of 30 patients, doing procedures, and presenting on attending rounds, there was really no time to eat. What better way to attract future victims than offering free food to residents? Just the simple act of free pizza or sandwiches would get a good crowd of residents to attend. And it was all under the guise of offering financial advice, something most residents had no knowledge of and where a salesperson could easily attract residents to their talks.

Many of these talks were within the hospital itself—maybe as a noon lecture—but there were also other times they might be a dinner at a fancy restaurant. Think of that, going to a free fancy New York City restaurant that was way outside the budget of any NYU resident.

Free Books/Material

Many times the food was not the only free offering. I got a free financial book for attending one of these lectures, which was basically an advertisement for the salesman’s firm that was promoting the benefits of permanent life insurance. I still have that book.

I am not recommending this book. I'm not even going to show you a photo of it. Like many other books written by financial salespeople, it's a promotion of their firm and the terrible products they might be selling. For example, this book has an example of how a dual-physician couple might utilize whole life insurance to accomplish their financial goals. Unbeknownst to me back in 2011, the better solution for this hypothetical couple would have been to buy term life insurance and invest the rest to make millions more for retirement. But alas, no such comparison was made.

The book only showed examples of successful uses of whole life without mentioning that buying term and investing the rest in low-cost index funds would have been far superior. And it wasn’t only this book. All materials these people brought in were for high-cost investment products.

Lecture handouts were all trying to sell you something.

Chocolate-Covered Poison

What made the poor advice so difficult to uncover is that these salespeople actually sprinkled in some correct and sound financial wisdom among their BS. All of them recommended contributing to work retirement accounts. All of them made mention of budgeting, not giving into lifestyle inflation, and saving for retirement. Even the selling of terrible insurance products was veiled with great advice on needing life and disability insurance for those dependent on your income or having an umbrella policy as protection above the max limits offered by underlying insurance policies.

Maybe you can’t really blame me for not seeing the evil products these salesmen were peddling since much of their advice otherwise was pretty spot on, exuding a façade of righteousness that any good salesperson builds that lay financial people like myself fail to see through. These guys sure know how to put lipstick on a pig.

More information here:

Is Whole Life Insurance a Scam?

Mistaking a Salesman for a Financial Advisor

Money Talk Was/Is Taboo

Another reason these salespeople got away with giving poor advice is that none of us residents talked about money and what the difference was between good and poor advice. When I first started neurology residency, I distinctly remember my senior resident talking about this magical company called “Vanguard” and getting disability insurance through Guardian because it was the best (I believe he was alluding to Guardian being one out of six companies at that time offering a “true own occupation” definition of disability).

At the time I was curious how much he was investing in Vanguard and why he chose that company, but I was hesitant to continue the conversation given the taboo nature of money. Instead, I did something even worse: I asked my high school friend who had just become a financial “advisor” for a company that rhymes with Porpestern Cutual, and the rest is history. If I had just continued the conversation with my senior resident, I might have learned that whole life insurance is evil and that low-cost index funds are the way to go. I would have gotten true own occupation disability at the time I was the youngest and healthiest, not a decade later when my premium was higher.

More information here:

Should You Keep Whole Life Insurance Policy and How to Cancel

The Best Way Out of Permanent Life Insurance: The 1035 Exchange

A Call to Action

To anybody reading this please, please avoid what I did. I led my wife and myself down the path of losing $50,000 to whole life insurance and other poor financial decisions, and I led a whole host of good docs and future attendings down a similar dark path by opening the door for financial salespeople to harpoon their marks. The road to hell is paved with good intentions, and all I wanted to do was help my fellow residents become the best docs we could be while also living our best lives. Our sacrifices for patient care deserve nothing else. And I failed the residents of NYU in 2011.

If you are a resident right now—maybe even a member of your hospital Housestaff Council or something equivalent—don’t just let in any salespeople. Please only allow vetted financial advisors like the ones that WCI recommends into your hospital to speak. DO NOT LET THEM SELL WHOLE LIFE INSURANCE! Just ask them about whole life and if they tell you that it's the best way to save for retirement or that it is totally appropriate for the majority of doctors, this is an easy tell that they do not have your best interest in mind. Ask them if they are a fiduciary. Ask them if they know about WCI and agree with WCI investing tenets.

As doctors, we have to look out for each other. The financial industry is using our undying commitment to our patients, where we don’t even spend an extra second thinking about finance in pursuit of perfect patient care, against us. I failed as a trainee to help my fellow trainees. Don’t let this happen at the hospital where you train.

What do you think? Have financial salespeople been allowed into your institution? Did anybody recognize that they were giving tainted financial advice? Does your hospital or residency program know about WCI? Is it still taboo to talk money at your hospital?