Feedback, especially negative feedback, is gold in a business like The White Coat Investor. So, we are extremely appreciative of the 3,096 people who filled out our annual survey. Thank you! We learned a lot (including how to better write survey questions to make them easier to answer and to make the data more useful). In today's post, I'd like to share some of that anonymized data that I think you might find interesting.

Who Are You?

First, let's talk about the audience.

Ninety-nine percent of you live in the United States. There are people from every state. Of that 1%, 15 other countries were named, ranging from Canada to Belgium and from Japan to Tanzania.

You range from 20-89 years old. Eighty-four percent of you are currently married, and 71.7% are male and 27.6% female, which surprised me given that our Google Analytics data tells us we're 62%/38%. Either that data is bad, or men were more likely to fill out the survey.

Those who are working make up 79% of readership with 13% in training and 8% retired.

What do you do for a living? Take a look:

Yes, that's right, 13 pages worth of different professions. No surprise to see that 71% of you are physicians and 8% dentists, but I was surprised to see that there were just as many pharmacists as dentists. Maybe we need to do some more pharmacy-specific content. Other professions ranged from pilots to physical therapists to financial planners to probation officers. Every specialty of medicine and dentistry seemed to be well-represented.

Your Finances

Let's talk now about your financial issues.

Most of you are employees:

Many of you have student loans:

But most of you are paying them off fast:

We were disappointed to see that half of you still don't have a written financial plan:

I should be more positive, though. I mean, 48% of you do have a written financial plan, and that still leaves 52% of the audience to whom we can sell the Fire Your Financial Advisor course!

A majority of you are in a two-earner household:

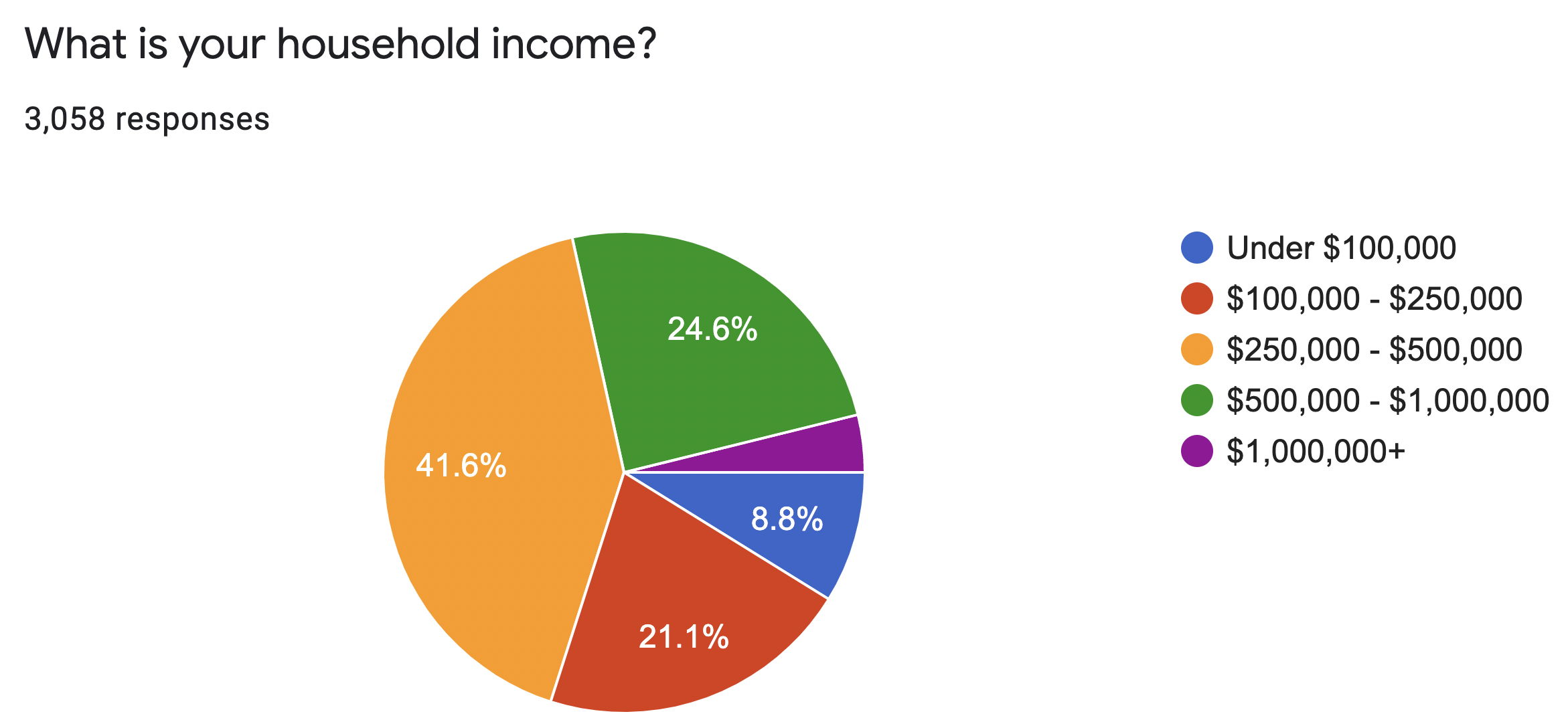

Most of you make pretty good money:

More than a quarter of you are making $500,000-plus but close to one-third are making less than $250,000.

You're pretty wealthy folks, too:

Probably because you don't spend anywhere near what you're earning:

This doesn't surprise us at all, though, as we've been in the upper end of the yellow for a long time ourselves despite earning considerably more. (Sorry about leaving the $200,000-$300,000 range out of this question. Presumably, most of you in that range chose yellow; we'll do better next year.)

Almost 1 out of 5 of you are financially independent:

Although few of you seem to have any desire to really FIRE at a super young age.

Only about 1 out of 8 of you wants to retire before 50, although I guess the data is a little confusing due to our typo.

I talk about doing your own taxes a lot, but most of you pay someone to prepare yours:

How You Invest

The data shows that:

- 99% of you own stocks

- 76% of you own bonds

- 56% of you own real estate

- 18% of you own crypto assets of some type

- 13% of you own small business investments

- 7% of you own precious metals

- 5% of you own collectibles

- 3% of you own commodities

- 2% of you own options

In the last year, the following percentages of you have invested money into the following types of investments:

- Index funds: 89%

- Passive real estate: 28%

- Individual stocks or options: 27%

- Actively managed mutual funds: 17%

- Direct real estate: 16%

- Crypto assets: 15%

- Individual bonds: 14%

Asset allocation ranges from 0% stocks to 100% stocks, with an average of 83%

Real estate allocations range from 0% to 90%, with an average of 9%.

Most of you are DIY asset managers.

I guess that's not too surprising. I suspect if we could somehow survey everyone who came by the site, not just those dedicated enough to fill out the survey, that might reverse.

Lots of you do Backdoor Roth IRAs each year:

But you're certainly not alone if you don't. In fact, the most popular reason people don't contribute is that they don't have to:

- I contribute directly: 33%

- I don't know how to do it: 23%

- I am concerned about potential consequences: 15%

- One of several dozen other reasons: 26%

Most of you carry disability insurance:

I suspect most of those who don't are either FI and don't need it or cannot qualify for it, so I'm pretty happy with that statistic. Again, I suspect the number is significantly lower among casual users who would not fill out a survey.

This one surprised me though:

That's right, 11% of you have a whole life insurance policy. Which is unfortunate, since other surveys I've done show that 75% of those who have purchased a policy regret it.

Burnout Is Really Bad

You have probably noticed our recent push over the last couple of years into more burnout prevention and treatment through courses and coaching, including our new Burnout Proof MD support program. While you can buy disability insurance, you can't buy burnout insurance. Even among white coat investors, the burnout rate is really high.

Looks like we need to continue to focus heavily there to make sure white coat investors stay mentally healthy. We know mental wellness is what leads to a long, fruitful financial life, and we’ll continue to talk about burnout because keeping up with your mental health is such an important part of everybody’s financial journey.

Content and Your Habits

We asked you how you prefer to consume content in general. This is what you said:

- Blogs: 76%

- Podcasts: 70%

- Books: 61%

- Forums: 28%

- Online courses: 26%

- Facebook groups: 21%

- E-books: 21%

- Social media: 19%

- Virtual conferences: 19%

- Newspapers and magazines: 19%

- Live conferences: 16%

I guess I was surprised to see conferences and courses as high as they are. I guess we'll keep producing them! I was also surprised to see Forums come in so far ahead of Facebook Groups and social media in general. You guys know we have a WCI Forum, right? And that dramatically fewer people participate there than in the WCI Facebook group? You should check it out.

When it comes to social media, though, Facebook still reigns supreme. These are the percentages of you that use each platform:

- Facebook: 58%

- YouTube: 51%

- Instagram: 39%

- Twitter: 23%

- Reddit: 20%

- WhatsApp: 14%

- LinkedIn: 14%

- Snapchat: 6%

- TikTok: 5%

- Pinterest: 4%

- Nothing: 2%

A few surprises for me there, but perhaps the most surprising was that only 2% are on nothing at all. Instagram also surprised me. I guess maybe we should put even more effort there. We're actually on all of these but WhatsApp (which I thought was only a messaging app anyway) and Snapchat (hard to put a lot of effort into content that disappears the next day). I think we might have a TikTok channel, but if I couldn't find it, you probably can't either. It's kind of a no-win situation. If I don't dance, nobody will follow. If I do dance, nobody will follow. Thanks for following us wherever you do, though!

You and WCI

It was interesting to find out how you all found WCI. Lots of you have been here so long you can't remember, but of those who do, this is what you said:

Most of you “stumbled” in here while searching for something, but a significant chunk is simply word of mouth. Plus, giving out WCI books is also a great way to introduce people to the community.

Seven percent of you claim to have been here from the beginning. I don't think I believe you, given how much bigger it got in years 2-4 (apparently, nobody started following then!). Still, there are an awful lot of people who have been with us for a long time. Thank you! The great thing about long-term readers is they know your heart and they are more forgiving of your mistakes.

When it comes to what you guys actually use, this is what you say:

The fascinating thing about this to me is how little overlap there is between our audiences. While 69% listen to the podcast and 68% read the monthly newsletter, those are not the same 68%. Facebook groupers may not read the blog, and Forum users may never visit the subreddit. Those on “the gram” may not use Twitter at all. I think this poll does give a lot of insight into who fills out the survey, though. The number of registered WCI Facebook group members is 10X that of registered forum users, but the percentages here are similar. To be fair, you don't have to join the forum to lurk, but you do with the FB group.

The virtual conference format is also surprisingly popular. I guess we'll have to keep doing that! I was surprised how few like the Milestones podcast compared to the regular podcast, given that our most popular episodes of the regular podcast were the ones that were basically like the milestones podcasts!

Connecting You with the Good Guys

Thirty-nine percent of you have used a resource we recommend (i.e., an advertiser). I guess that's no surprise given that only 1.3% do not trust our recommendations:

This was an interesting question to ask. We gave you the option of “yes,” “no,” and “other” and ended up with 13 pages of “other” responses, which ranged from “I clicked ‘other' so I could say ‘Absolutely'” to “trust but verify” to “I don't feel I need them” to “not if there is a kickback involved.” There was actually a ton of great feedback in those responses that we will incorporate.

New Topics

We asked people about content they would like to see. There were tons of responses, but some trends include:

- Estate planning

- Crypto assets

- Spending and investing in retirement

- Real estate investing

- Taxes

There were also a lot of fun suggestions like getting Peter Kim and Mike Piper to debate, surrogacy/IVF costs (any volunteers for a guest post?), and living morally when wealthy. Some also want to hear more about my vacations, for some reason. Then, everyone wants more content aimed directly at them. “More for medical students.” “More for PAs.” “More for retirees.” “More for veterinarians.” “More crypto.” “Less crypto.” “More basics.” “More alternatives.” There were at least two years of blog posts and podcast suggestions in that response! Including some topics I had to Google just to know what they were. Pure gold. Keep them coming. Mostly, people wanted more, more, more. But we also got this sort of feedback from many people:

“Too much content will turn your blog into KevinMD which has become superfluous (like bringing in a bunch of new authors). The important stuff gets diluted down and harder to find/identify. Less frequent posts that are more content-rich yields interesting discussions in the comments and more devoted readership IMO.”

Less is certainly easier than more.

What You Like

We asked what you liked most about WCI. Here are the top responses:

- Honesty

- Trustworthy

- Podcasts

- Consistency

- Everything

- Easy

- Straightforward

- Practical

- Non-biased

- Great high-yield, no-fluff content

- Motivating

- Intelligent

- Transparency

You guys made me cry. Of course, nobody said I was funny. I always wanted to be funny. But I'm really not very funny. Except when I hide in my son's bed when he gets in the shower and then jump out and scare him out of his wits when he comes back to his room. That's funny, I don't care who you are.

Golden Feedback

We asked what we could do better. Most of you said some variation of “nothing.” Aaaahhh. You guys are so kind. A fair number said they wanted fewer ads. Nobody said “more ads” for some reason. Feedback about ads, promotions, products, etc., is really helpful. While we're a for-profit business (always have been and always will be), getting that balance right is really important. Sounds like we need to cut back even more on ads on the podcast and maybe the main site, too. We'll be talking about ways to do that. There were some other nuggets in there like these:

“Feel that standards and investment advice has changed over the years. As the site has become more prosperous, the topics have tilted towards the wealthier.”

Guilty as charged. Now you know why I have been trying to focus more on other WCIers rather than my own financial life.

“Please don’t get too polished. I know you’ve hired a team, and needed to, but keep the direct connection with the reader. Don’t develop the impersonal feel of a magazine.”

“Too many blog posts written by people other than WCI. I come here for his content primarily.”

“More guided conversations in FB group.”

“Comment on the WCI Forum more often.”

I'm not really sure what to do with those, but I'm still answering your emails personally, so that'll have to do, I guess. I certainly can't create all the content and steer all the FB group and Forum conversations. Plus, I want to make sure WCI can survive if I get hit by a bus.

“I feel like Jim has gotten a little too political on the podcast lately. I find myself rolling my eyes sometimes when he goes on his republican tangents.”

“I want to learn finances, not virtue signaling. Return to your religious roots and cut the crap about white privilege, racism, and sexism and having every sentence include “her”—it’s patronizing.

“I can do without the Lesbian articles. I like my financial information without a side of liberal wokeness.”

“Get more perspectives from older physicians that are toward end of career and what they struggle with but also include diverse viewpoints (gender/cultural).”

I'm probably not going to be able to make everyone happy. I guess I'll just be me and let the chips fall where they may. We're still going to push for more viewpoints on the blog and podcast, if for no other reason than so WCI doesn't die with me. But I think there are a lot of people out there who need the WCI message who won't hear it from me. Remember the term “white coat investor” refers to you, not me.

“Some political views don’t necessarily align with mine (I recognize that I lean far to the left), but can easily look past this and still really find the website helpful.”

I wish more were like you. Most of what I have ever learned I have learned from people who did not share my political views, religion, etc. The likelihood of someone's political views aligning with my weird mix is highly unlikely.

“More entertaining podcast.”

That's definitely not me. I'm not going to lie. I still can't believe anyone listens to my podcast. Heck, I can't listen to it myself. But we'll see what we can do.

“Tough to pin it down in a succinct manner but I feel like the recent episodes have a bit too much fluff. I know there’s a thought that WCI podcasts need to be more entertaining but I believe people who follow WCI follow it for Jim’s advice, insight, experience, and dry humor.”

Never mind, we'll keep it boring.

“Jim should stop saying he's not funny, I think he's hilarious :)”

You're weird.

“I think get rid of the salesy stuff. Jim used to be the guy you could send an email and he would reply 3 hours later at 3 in the morning! Still makes me smile. I don't suggest that continues as the site and following are too big. But it's the personal connection directly back to him with trust that sells this site.”

Now, I sleep at 3am. Weird, I know. FI will do that to you. You'll have to wait until 10am to get your emails returned.

Lots of Facebook Forum complaints like:

“Hard to search Facebook forum.”

Blame Zuckerberg.

“The Facebook group is so toxic. People shaming one another for their current step in their journey.”

Maybe blame Zuckerberg for that, too. Or blame yourselves. I dunno why people can't be nice online. It's weird.

“Social media (Facebook) . . . may be a bit too apt to kick out people who voice differing opinions or (allegedly) try to promote some outside product. (Allegedly, because I never get to see the post that people complain about having been removed or having gotten them banned.) WCI Facebook group gets a lot of bad press in other physicians’ groups on FB for these reasons. I would prefer it if the FB group tried to improve its public image by remembering what social media is about and trying to be more tolerant.”

Less moderation, got it.

“The FB group is not so great . . . lots of snarky people on there.”

“Filter FB posts. Too much redundancy.”

“The Facebook group can be redundant and individuals can make me feel negative toward the group as a whole. Very nice job of reducing this recently by WCI admins!”

More moderation, got it.

“More expert involvement in Facebook group.”

“Honestly, the people in the Facebook group are pretty annoying. Not sure if there's a way to better screen them but they continuously give terrible advice. Otherwise no complaints!”

“Better Facebook content.”

“#1 complaint is the FB group—the YOLOs, the terrible and inaccurate advice that a new doc/investor won’t recognize as bad advice (although this has greatly improved with extra moderators and the ban on speculative “investing” talk), and the guilt-tripping from people in the group about ‘the greedy rich' when topics like excessive taxation come up—these people clearly can’t relate to the years of life lost to intense training and shortened lifespan from shift work and stress. I have found the WCI Forum to be a much more useful place but I haven’t yet made it a habit to go there as often as the FB group.”

I'm all ears for a solution here. But I could literally spend 24 hours a day just reading and responding to posts in the WCI Facebook Group. I would hope that group members would have more expertise (and hopefully be less annoying) all the time. Maybe we could add more screening questions to get in the group: “Are you annoying? Do you give terrible advice? Will you just shut up and listen for the first six months?” Who knew the Facebook Group would be such a challenge? Everyone else makes it look so easy. Maybe we need more moderators. If you're interested, email [email protected].

“Producing a more detailed book or blog posts would be interesting to me.”

Longer posts, got it.

“Shorter daily emails.”

Shorter posts, got it.

“Quit saying cocaine and hookers when talking about when your kids get access to their UTMAs.”

Message heard loud and clear. A fair number of you actually said this. Now, I feel bad about it. Someone send me a less offensive phrase to use that conveys the same thing.

“I don't know if it is enough of a complaint to really change anything, but I do feel the quality of some of the guest posts does not match the quality of the site as a whole. I understand this reduces the load on the rest of the WCI team, and the posts might still be helpful to someone, but I can think of a few occasions where the posts didn't sit right because of tone or the message and it just wasn't something Jim would have posted on his own, which might be the point.”

“WCI has made positive strides in improving diversity of voices and blog/podcast subjects to more things that intersect with medicine and finance . . . however, I think there could be more improvement here, especially on occasional slip ups on tone/side remarks.”

Man, this one is going to be tough to get right. We'll do our best.

“Please never retire!”

I'll think about it, but I've already been telling my kids I am retired for the last couple of years. They don't believe me, for some reason.

“This is a silly complaint, but whenever you take questions off the speak pipe, I feel like 30 seconds are spent thanking you for all you do. Don't get me wrong, I am very thankful for WCI!!! You do great work and I enjoy learning everything, but sometimes I think people could be more concise with their thanks to you. This is a ridiculous complaint, I know. For you I'm sure that it feel great to receive the thanks and it is well deserved.”

I've thought about this one. People do the same thing on live call-in shows, though, so we've never cut them out in the past. But you're right, it doesn't need to be said a half-dozen times an episode. Hey everybody, just leave your questions from now on without all those compliments. We could probably do a better job trimming them down, too. Great feedback. Solid gold in this survey, I tell you.

“I know you all know how poor Med students and residents are. Just keep us in mind for pricing structures.”

Remember the online courses and conferences (the expensive stuff) are our premium products. We price them for people whose time is worth hundreds of dollars an hour. The blog, podcast, newsletters, communities, videocasts, etc., are all free, and the books are only $9.99 on Kindle. We do have some plans to develop some courses for med students and residents at a much lower price point, but it's tough to make it pencil out as a business decision. We'll figure something out, though.

“Individual one on one sessions.”

Nope. These folks do that, though.

“Politics consistently GREAT.”

“Keep your personal political opinions out of your posts. They show through lately especially and it's unnecessary and irrelevant to the financial advice you are providing.”

“Less tribal politics.”

Another can't-win issue. People want me to talk about what's going on in Congress but without discussing politics. Maybe I should just tell you what my politics are, so you know and can interpret accordingly. But I'll probably try to be more apolitical. It's tough these days when everything seems to be politicized, including public health measures.

“Would be nice to occasionally go deeper into the math.”

“Be a little more basic—start at the beginning.”

I included both of these because they came in right after one another. Seriously can't win.

“The music theme on the podcast is jarring and makes me tachycardic.”

Several comments about this. I'd love to have a regular listener come up with some (non-copyrighted) theme music for us. Consider this an invitation.

“No need to dis the Teslas.”

You don't know about my Tesla?

I think that's enough of them. I hope you enjoyed spending time with me on the survey. I seriously cannot thank you all enough for taking the time to fill this out. It really means a lot to us and will guide what we do moving forward. Those of you who won the raffles for cash and prizes have all been contacted, so if you have not been contacted, I'm sorry you didn't win. Congrats to Natasha Shapiro who won the grand prize (an online course). The rest of you winners enjoy the T-shirts.

What do you think? What surprised you about the survey? Any other feedback you want to provide? Comment below!