I prefer to invest my time actively and my money passively. But many investors assume they can add value to their investments when they actually cannot. This is a big problem. In fact, spending more time and effort on their investments, counterintuitively, can actually subtract value (not even including the value of their time) while also adding the additional tax burden of active strategies.

However, once people become aware of the benefits of passive investing, they sometimes “jump the shark” with it. You can take this concept too far.

The Data on Passive Investing

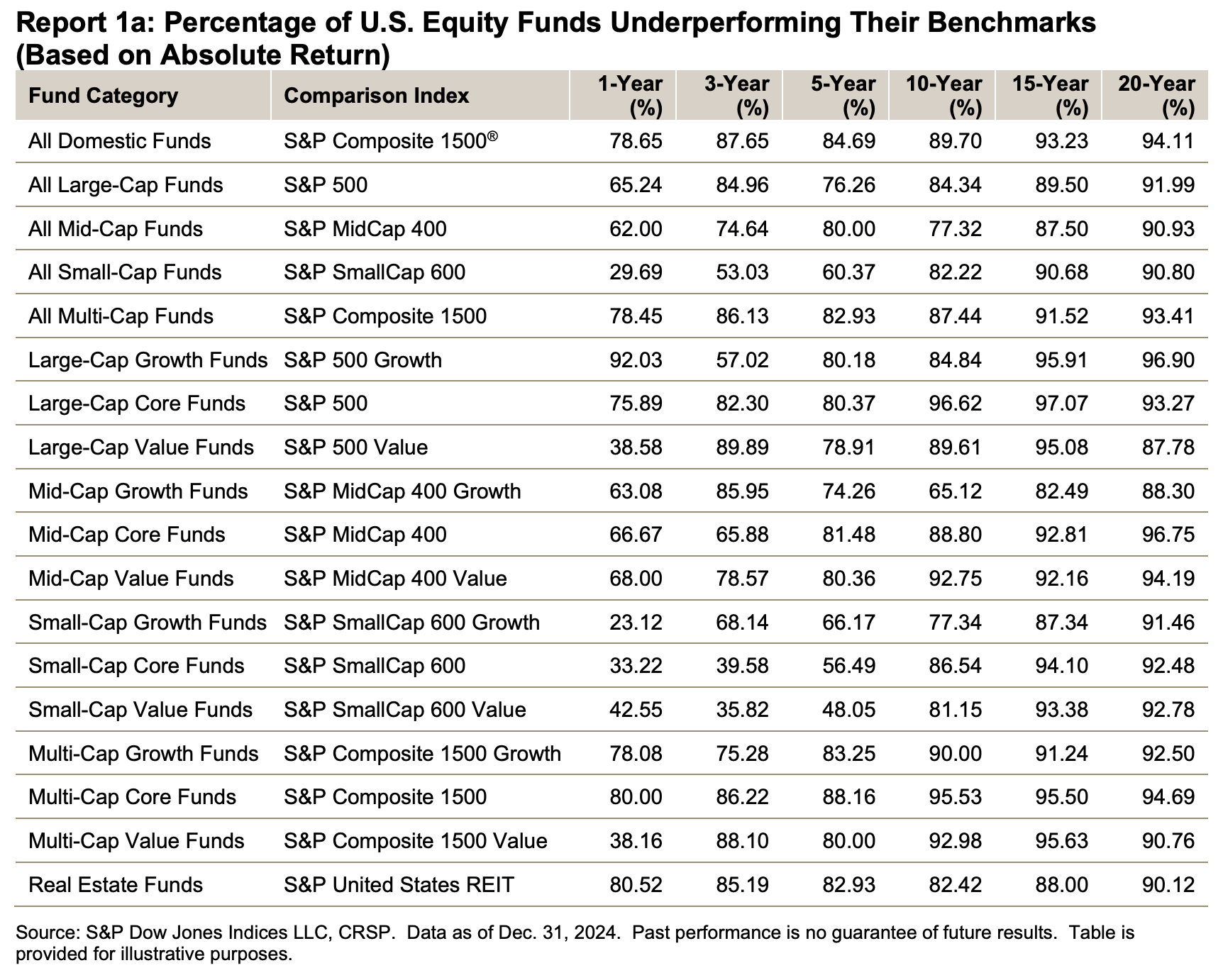

Perhaps the greatest display of passive investing benefits comes from the semiannual SPIVA reports. Here's a chart from the most recent one when I wrote this post, but trust me when I say they all have looked pretty much the same for years and years.

Basically, over long periods of time, most actively managed stock funds underperform their respective index. Since an index fund passively matches the index, index funds will beat the vast majority (90%+) of the actively managed funds over long periods of time before taxes. After taxes, the data looks even worse for the active managers. That's it. That's pretty much all you can say about active and passive. The best way to invest in stocks for the vast majority of investors is via index funds. It beats the pants off choosing active managers, much less being your own active manager by picking your own stocks.

However, it's important to understand WHY this is so. Here are a few reasons that I rank more or less in order:

- Lower costs

- Fewer behavioral mistakes

- Lower turnover

- Lower time requirements and potentially advisory fees

- Broader diversification

- Lower taxes

Mostly, it's lower costs. You don't have to pay for all the buying and selling and analyzing and staff. Investment advisors who use index funds often charge less, too. The lower resulting tax bill due to avoiding capital gains distributions, especially short-term capital gains, is because of that low turnover. These factors all still matter as you step away from stock investing. In fact, they matter a lot more than whether an investment is technically active or passive. Let me give you a few examples of when people get too carried away about passive investing.

More information here:

People Still Believe In Active Management?

10 Reasons I Invest in Index Funds

Vanguard Bond Funds

I got an email recently that read like this:

“Been your reader for over 10 years. If I can be nosey, for muni bond funds I believe you prefer VWIUX over VTEAX? I’m curious as to why because VWIUX is listed as active by Vanguard, whereas VTEAX is listed as passive . . . and your principles are generally to invest in passive over active funds.”

VWIUX is the Vanguard Intermediate Tax-Exempt Bond Fund. It has an expense ratio of 0.17%, holds more than 15,000 bonds with an average duration of nearly six years, and has 20% turnover. It is technically an actively managed bond fund, like many of Vanguard's excellent bond funds.

VTEAX is the Vanguard Tax-Exempt Bond Index Fund. It has an expense ratio of 0.07%, holds nearly 10,000 bonds with an average duration of 7.2 years, and has 22.8% turnover. It is technically a passively managed bond fund. It's an index fund.

I really have no preference between these funds and treat them as essentially the same thing. They are tax-loss harvesting partners in my portfolio, and at the time I got the email, our muni bond money was actually all in VTEAX. But when I first started buying intermediate-duration municipal bonds, VTEAX didn't exist. So, we used VWIUX. To be frank, the most important difference between the two is the small duration difference, not the expense difference or even the style of management. At the time, the five-year returns were 0.74% vs 0.07%, and most of the difference was explained by the shorter duration of VWIUX colliding with the rapid, severe rise in interest rates back in 2022.

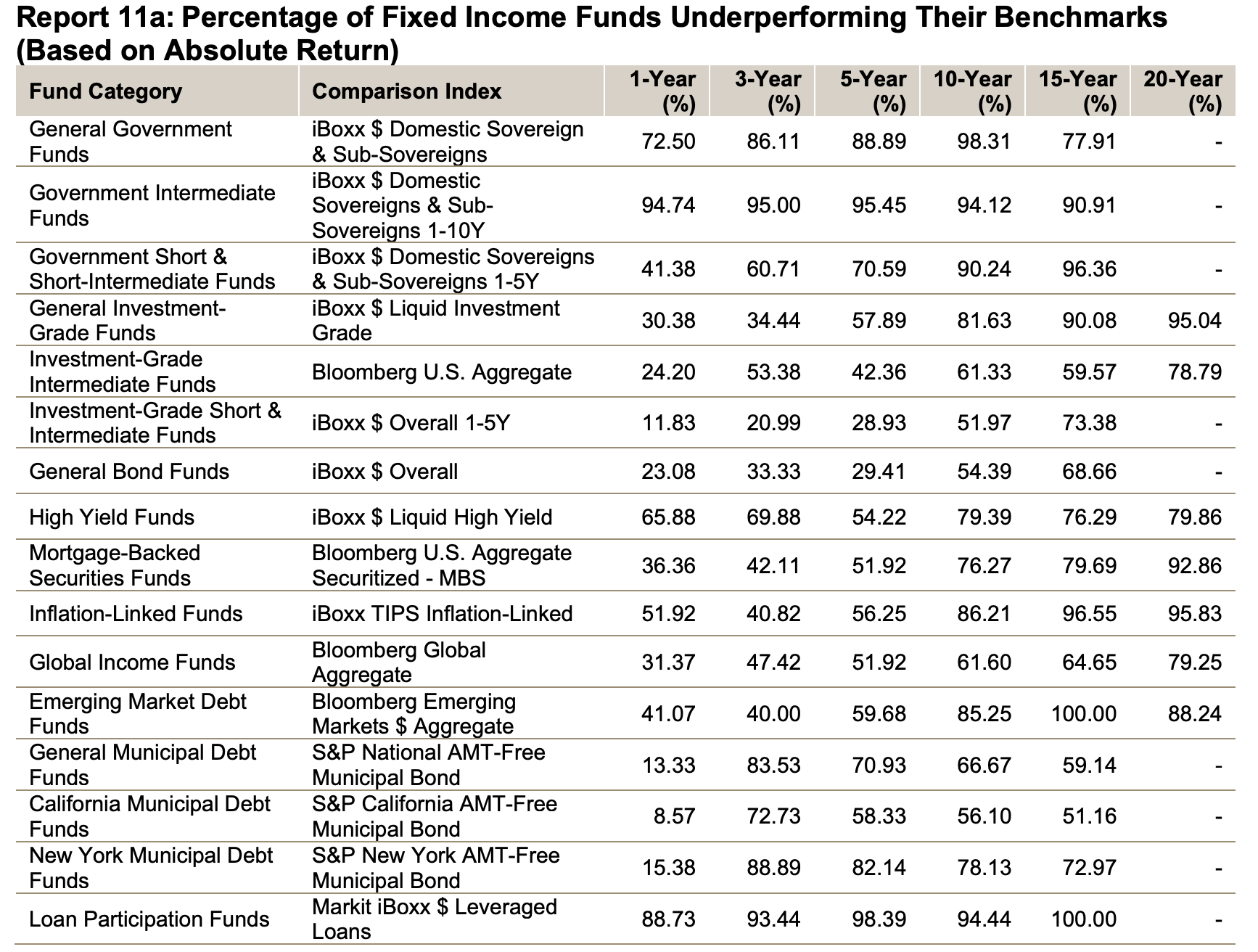

It's important to understand WHY passive is generally better than active, so you can see when it doesn't matter so much (as well as any exceptions). Note also that the data on passive beating active isn't quite as strong among bond funds as among stock funds.

Hypersensitivity to Costs

Another thing I frequently see among passive investing converts is a hypersensitivity to costs. They think differences of a few basis points matter. They don't, as I wrote about here back in 2018 when Fidelity came out with their Zero index funds with a 0% expense ratio. Back then, everyone wondered if they should switch from their Vanguard index funds with expense ratios of 0.03% or 0.05% to the Fidelity ones with expense ratios of 0%. A quick look at the performance tape since then shows I was right to tell people not to worry much about it. I've used both funds over the years with very similar performance. The five-year performance numbers for the various high-quality index funds are essentially equal.

- FZROX (Fidelity Zero Total Stock Market): 12.94%

- FSKAX (Fidelity Total Stock Market Index Fund that charges a tiny expense ratio): 12.67%

- VTSAX (Vanguard Total Stock Market): 12.66%

- ITOT (iShares Total Stock Market ETF):13.07%

That's a rounding error as far as performance goes. Most will conclude the performance advantage isn't worth the fact that the fund has to be held at Fidelity and the additional tax cost due to not having an ETF share class to flush out capital gains. Certainly, it wasn't worth realizing any unnecessary capital gains to switch funds. A similar story is seen on the international stock side:

- FZILX (Fidelity Zero Total International Stock Market): 10.22%

- FTIHX (Fidelity Total International Stock Market Index Fund with a tiny expense ratio): 9.69%

- VTIAX (Vanguard Total International Stock Market): 9.80%

- IXUS (iShares Total International Stock Market ETF): 9.92%

Don't get too fixated on costs. Once you get below about 10 basis points, you're basically investing for free. The difference in index followed probably matters more than the expense ratio. If it were all expense ratio, the difference between the various funds would exactly mirror the expense ratio differences, and that certainly isn't the case. The Zero funds could easily underperform slightly over the next five years (and there was a time in 2019 and 2020 when they did).

DFA and Avantis Funds/ETFs

I also chuckle when I see people deride funds/ETFs like those from DFA and Avantis as evil because they're “actively managed.” Well, kind of. The argument made by these fund companies is that they use an active implementation of a passive philosophy.

They see where true index funds do little things that cost their investors money and try to avoid doing those things. Does it work? The jury is still out, but it's not hard to compare performance numbers. The closest thing Avantis has to a total stock market ETF (AVUS) certainly compares favorably to Vanguard's VTI.

AVUS owns 1,940 US stocks, has a turnover of 1%, a P/E ratio of 22.93, an expense ratio of 0.15%, and a five-year return of 14.39%.

VTI owns 3,511 US stocks, has a turnover of 2.1%, a P/E ratio of 27.3, an expense ratio of 0.03%, and a five-year return of 12.66%.

I would argue the main difference is that the average stock in AVUS is smaller and more valuey than the average stock in VTI. I would NOT argue that AVUS is an evil actively managed fund. That's just being dogmatic.

Markets Without Index Funds

It gets even worse when you get into markets/asset classes where index funds don't exist at all. Imagine you want to invest in cryptoassets or precious metals. There is no index fund. There is no index fund for private real estate or private equity, either. If you want to invest in these asset classes, you've basically gone back five decades in time to the years before index funds existed. You might be perfectly happy to get the “market return” for the asset class, but there is no way to guarantee it. You either have to hire an active manager or become a manager yourself.

Yet I see people trying to compare private real estate returns to index fund returns and deriding the real estate investors as the equivalent of stock pickers. There is no alternative in the asset class. You can avoid the asset class for that reason, or you may, like me, basically do the equivalent of buying an index fund. You pick experienced managers, diversify broadly, keep costs (including taxes) down, control your investing behavior, and move forward. You might also recognize that active management probably still works in these asset classes, at least to a far greater degree than in the publicly traded stock world.

The reason active stock fund managers can't beat index funds very often is not because they stink. It's because they're too good and there are too many of them. So, the passive investors get a free ride in a pretty efficient market. That's not necessarily the case in less-analyzed markets like your local real estate market.

When you see a $100 bill on the ground, pick it up. There are plenty more of them when there are 10 investors competing with a bunch of regular Joe homeowners than when 100 million investors are competing.

More information here:

A Die-Hard White Coat Investor Buys an Individual Stock — An M&M Conference

Picking Individual Stocks Is a Loser’s Game

Nonsense

Sometimes, I even see people try to apply the “active is bad” mantra to stuff that has little to do with investing at all. Like estate planning or running your own business or making moves to reduce taxes. Ignoring your rental properties when you can raise rent or otherwise increase their value is foolish. Add value where you can.

The Bottom Line

Passive investing works, especially in the publicly traded stock markets. But be careful not to stretch the concept too far. It is also critical to understand WHY index funds work so much better than actively managed funds and apply those principles to all of your investing activities.

What do you think? When did you become convinced of the merits of passive investing? Have you ever found yourself “jumping the shark” with the idea of “be passive, not active?”

The White Coat Investor may receive compensation from White Coat Insurance Services, LLC; licensed in all states including MA and DC; CA license #6009217; NY license #1758759 (exp. 6/2027); Registered address: 10610 S. Jordan Gateway, #200 South Jordan, UT 84095. This does not affect the cost or coverage of insurance.